Reporting of real GDP Is what most investors will see But nominal data Is what could create a New narrative reality Combining both growth and inflation This number could be the foundation For further yield gains And many more pains Inflicted on stock adoration

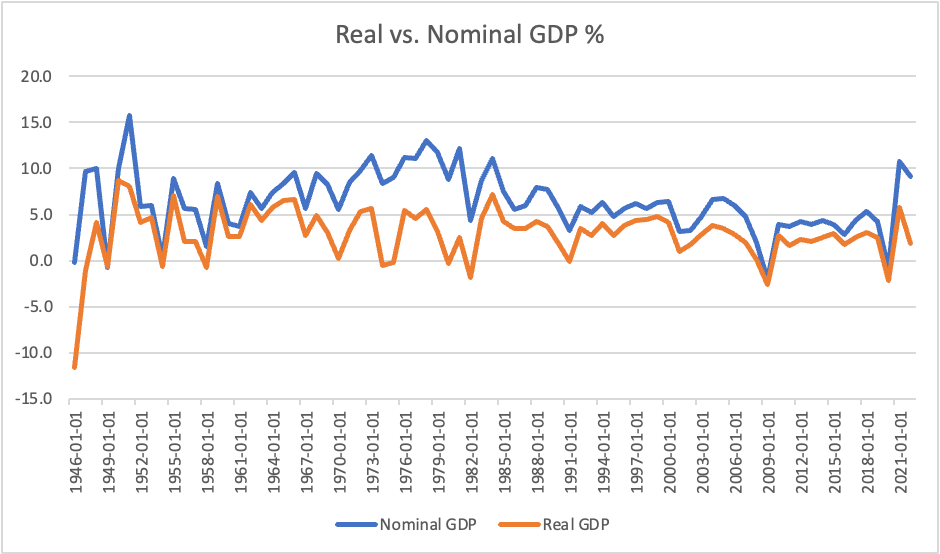

After another lousy day in the equity markets, today the first Q3 GDP data will be released. The current consensus forecast is for a 4.3% gain while the Atlanta Fed’s GDPNow number is up to 5.4%. And that’s the real GDP (rGDP) number, which removes inflation from the discussion. However, given all that is ongoing, it may be worthwhile to take a look at nominal GDP (nGDP), which is simply the change in total activity including price changes and economic output. As you can see from the below graph (data source, FRED database), in the post-WWII era, we’ve had 10 periods where rGDP fell below zero, better known as recessions, but only 3 periods where nGDP was negative, with the GFC in 2009 being the worst at -2.0%. The gap between the two lines is inflation, and you can also see how that has ebbed and flowed over time.

But turning to the current period, it is noteworthy that in the wake of the GFC, which was rightly called the worst financial crisis since the Great Depression and up through the Covid recession in 2020, nGDP had been pretty modest overall. In fact, a quick look at the data shows that the average nGDP during that decade was just 3.4%. This compares quite unfavorably with the long-term historical average of 6.4% since 1946. Looking at rGDP data, the average between the GFC and Covid was just 1.8%, again comparing quite unfavorably to the long-term growth of 2.9%.

The thing is, we have all gotten quite used to that economic environment of slow growth and low inflation and there are many professional investors, let alone non-investment professionals, who believe that is the way the world works. Well, let me tell you, that was the exception, not the rule. Instead, if you look at the very right side of the chart, you can see that both nGDP and rGDP have risen sharply in the wake of the Covid recession as the deluge of fiscal spending combined with, first supply chain constraints and now reshoring/deglobalization efforts, has changed the framework. In fact, I would contend that it is in the government’s best interest to continue down this path of high nominal growth and high inflation in order to try to outgrow the increase in debt. After all, if nGDP can grow faster than the fiscal deficit, the real value of US debt will ultimately decline. Of course, while it would be fantastic if the bulk of that high growth was a function of gains in productivity and high real growth, the FAR more likely outcome will be persistent high inflation.

What does this mean for markets? As we have seen over the past several sessions, equities can quickly come under pressure in this scenario, and I believe they have further to decline. While top-line revenues can continue to grow, the problem will come from a market that is going to derate the market multiple, especially in the tech sector, from its current nosebleed levels. High inflation will also continue to press on bond prices and the value of the long-term 60/40 portfolio is likely to continue to be eroded. In my view, the best place to hide will be in commodities as during inflationary periods, they tend to hold their value.

An anecdote from my early days in trading is that bond traders used to believe that the “natural” yield for 10-year Treasuries was right around nGDP. If yields rose above that level, bonds were probably a buy, and below that level, they would have a short bias. Nominal GDP for the past two years has been 10.7% in 2021 and 9.1% in 2022. On this basis, there is considerably further for bond prices to fall and yields to rise. Something to keep in mind as the talking heads work to convince you to catch the falling knife that is the bond market.

Ok, so how have things behaved ahead of today’s data, and ahead of the ECB’s rate decision this morning? Equity markets around the world have been under pressure with the Nikkei (-2.1%) leading the way as most regional markets fell sharply, notably in South Korea and Taiwan, although Chinese shares held their own on the back of still more stimulus promised by the government there. It is clear that President Xi is growing increasingly worried about the financial situation at home. In Europe, we are also seeing weakness, with red across the screen on the order of -1.0% or more and US futures are also pointing lower at this hour (7:30) down by -0.75% or so across the board.

Bond markets are little changed this morning with most seeing yields creep very slightly higher, maybe 1bp or so, but that is after another bond sell-off yesterday which saw Treasury yields continue their rebound from Monday’s sharp drop. As I type, we are back at 4.97% on the 10-year and the curve inversion is down to -15bps. As an FYI, the 2yr-30yr curve is back to flat now and I expect it is only a matter of days before the 2yr-10yr is there as well. Yesterday’s 5yr auction was particularly poorly received with a very wide tail and concern is growing that will be the case for all coupon auctions going forward. Yields are heading higher folks.

Oil prices are falling this morning, down -1.8%, which has basically reversed yesterday’s rally. EIA data showed inventory builds and it seems the longer Israel holds off on its ground invasion of Gaza, the more people are willing to believe that there will be no escalation. However, gold prices continue to rally, up another 0.4% this morning and getting ever closer to the $2000/oz level. Meanwhile, this morning, ahead of the GDP data, both copper and aluminum are in good spirits and rising.

Finally, the dollar is clearly back in the ascendancy with USDJPY finally breaking through that 150.00 level with no sign of intervention yet, while the euro is pressing back toward 1.05 and the pound is below 1.21. We are seeing strength across the board for the greenback, against both G10 and EMG currencies as the yield story continues to be the driver. As to the ECB today, expectations are for no change in policy, and the real question will be whether Madame Lagarde can maintain a hawkish bias, or if the obvious weakening in the data will reveal her inherent dovishness. If it is the latter, look for the euro to break below 1.05 before tomorrow’s close.

In addition to the rGDP data (exp 4.3%), we see Initial (208K) and Continuing (1740K) Claims as well as Durable Goods (1.7%, 0.2% ex transports). The ECB Press conference starts at 8:45 and will be carefully watched. Yesterday’s New Home Sales data was much stronger than expected and the BOC left rates on hold with a hawkish commentary, although the CAD was unable to gain much in the wake. The world continues to point to higher yields to fight structural inflationary pressures. At the same time, the dollar will retain its status and remains in demand. While it may not rally that sharply, I see very little case for any substantive weakness in the near and medium term.

Good luck

Adf