For weeks, things appeared to get better

As yields slipped and helped every debtor

But we’ve seen some changes

With yields breaking ranges

And oil back to the pacesetter

So, stocks are not really embraced

While bonds have left all a bad taste

The dollar’s moved higher

While gold’s back to dire

With analysts worldwide disgraced

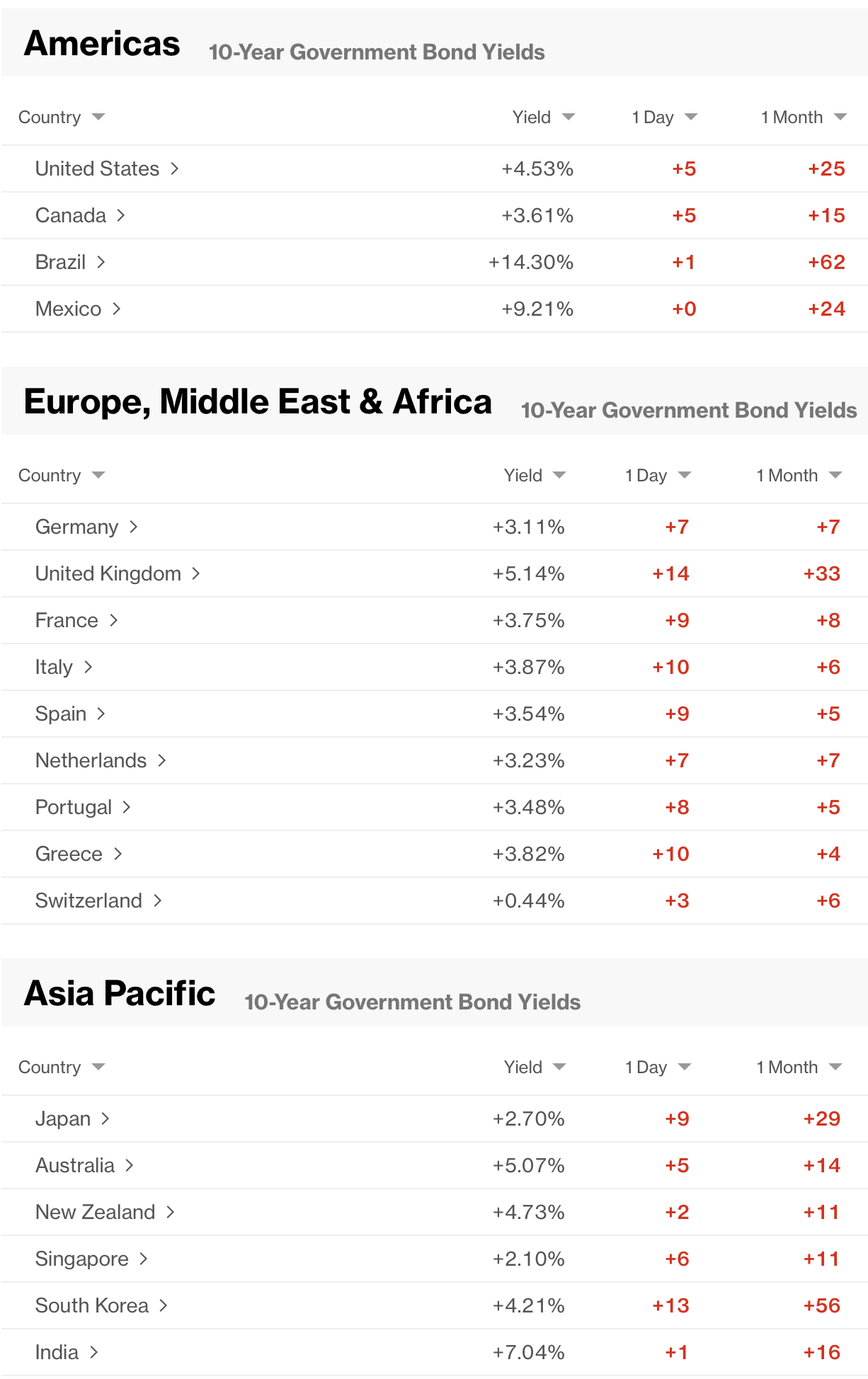

Investors are not as happy this morning as they had been for the past several weeks as the situation in Iran and the Middle East appears to be deteriorating again. The US continues to attack Iranian missile launchers and fortifications on a daily basis while Iran continues to fire missiles at targets throughout the Gulf region. As well, the Houthis are back at it in the Red Sea restricting oil flows through there as well. Arguably the chart below of oil (+4.0%) is the most descriptive view of what is driving everything.

Source: tradingeconomics.com

Crude is higher by 29% in the past month and back above $90/bbl. This makes things tough on everybody but the oil companies. Does this mean we are running out of oil? I don’t think that is the case. Rather, the short-term impediments to shipping it are driving the price. But the price is rising nonetheless and that is impacting everything else. If you recall when things kicked off in this war back in March, the oil price was the primary catalyst for movement in every market. As things seemed to settle down and it appeared there was an opportunity for a resolution, focus turned back to things like earnings for equities and interest rate differentials for currencies with oil in the background. But it appears we are back to, as oil goes, so goes every other market.

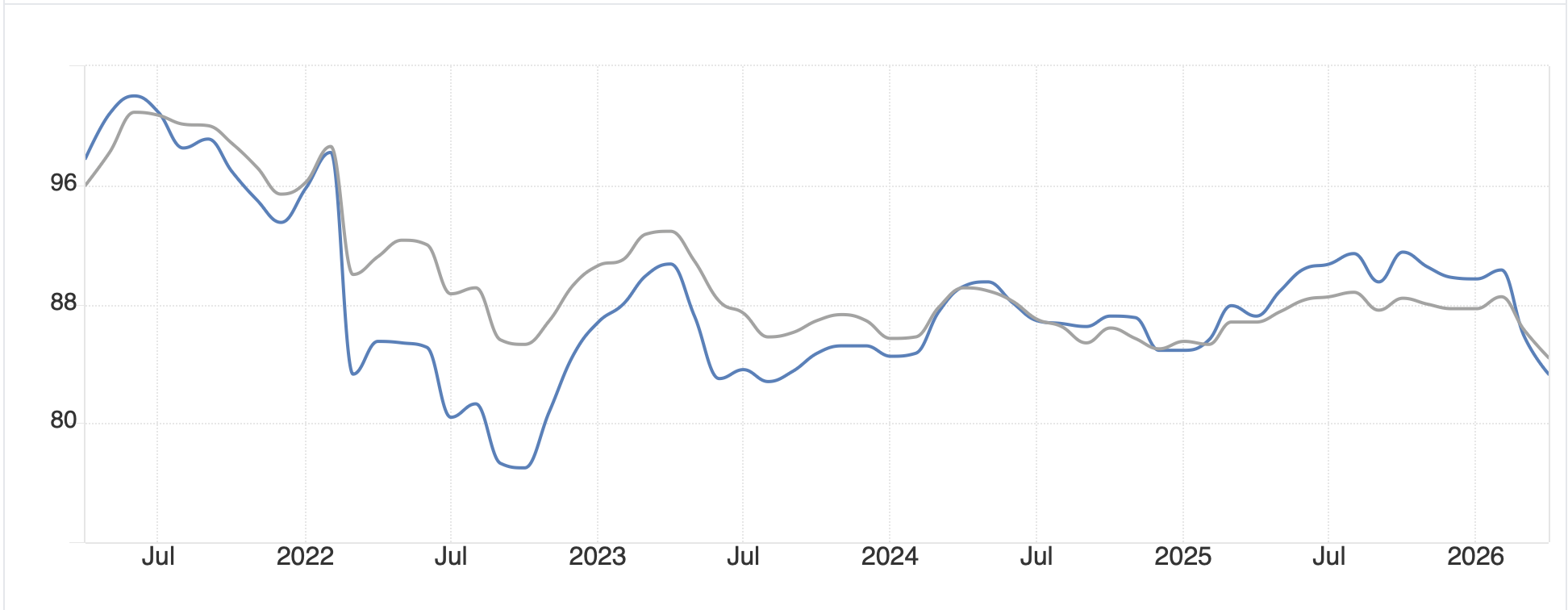

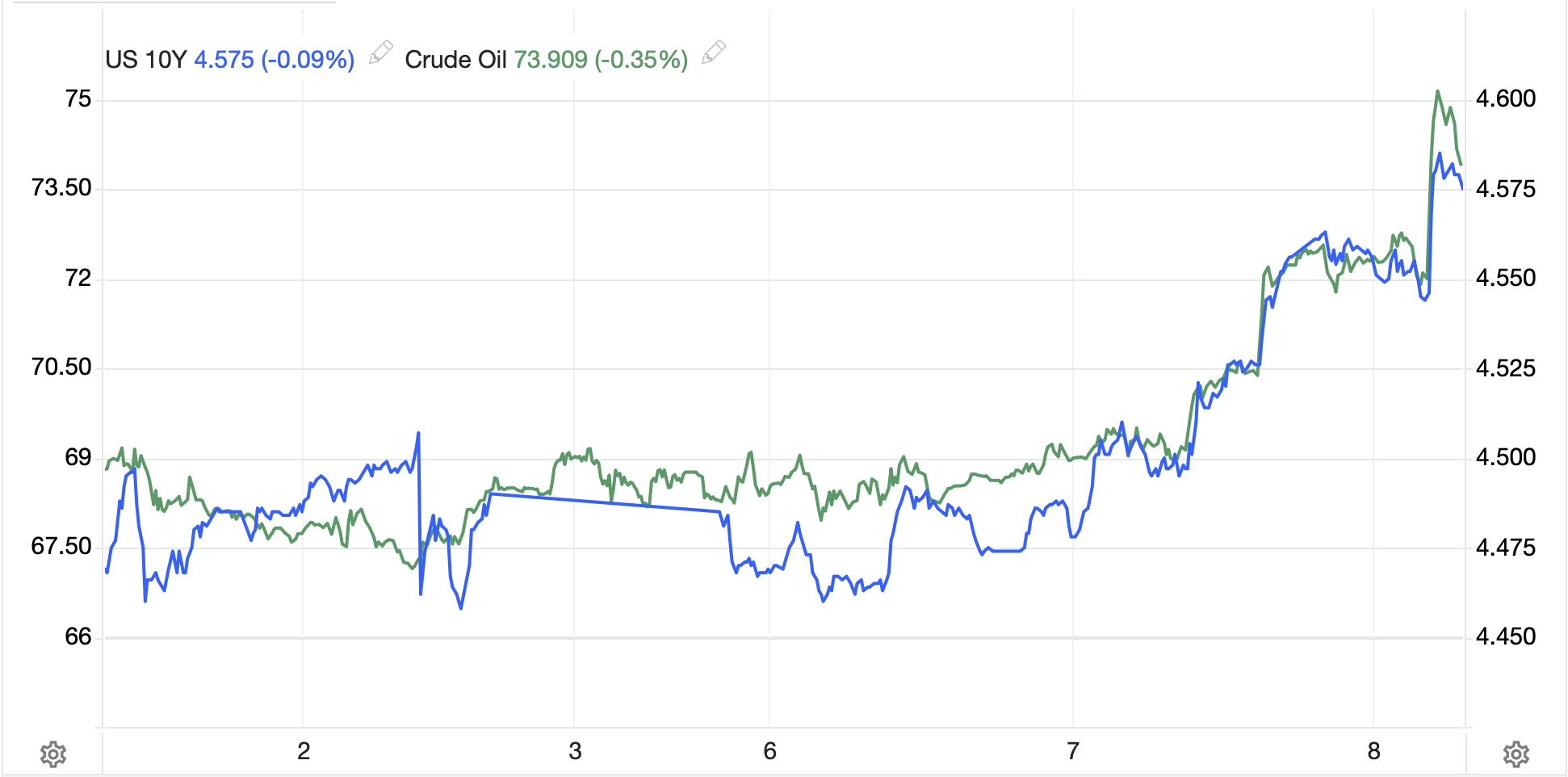

For instance, here is a chart of oil and 10-year Treasury yields over the past month. As you can see, the trajectory, especially over the past several sessions, is quite similar.

Source: tradingeconomics.com

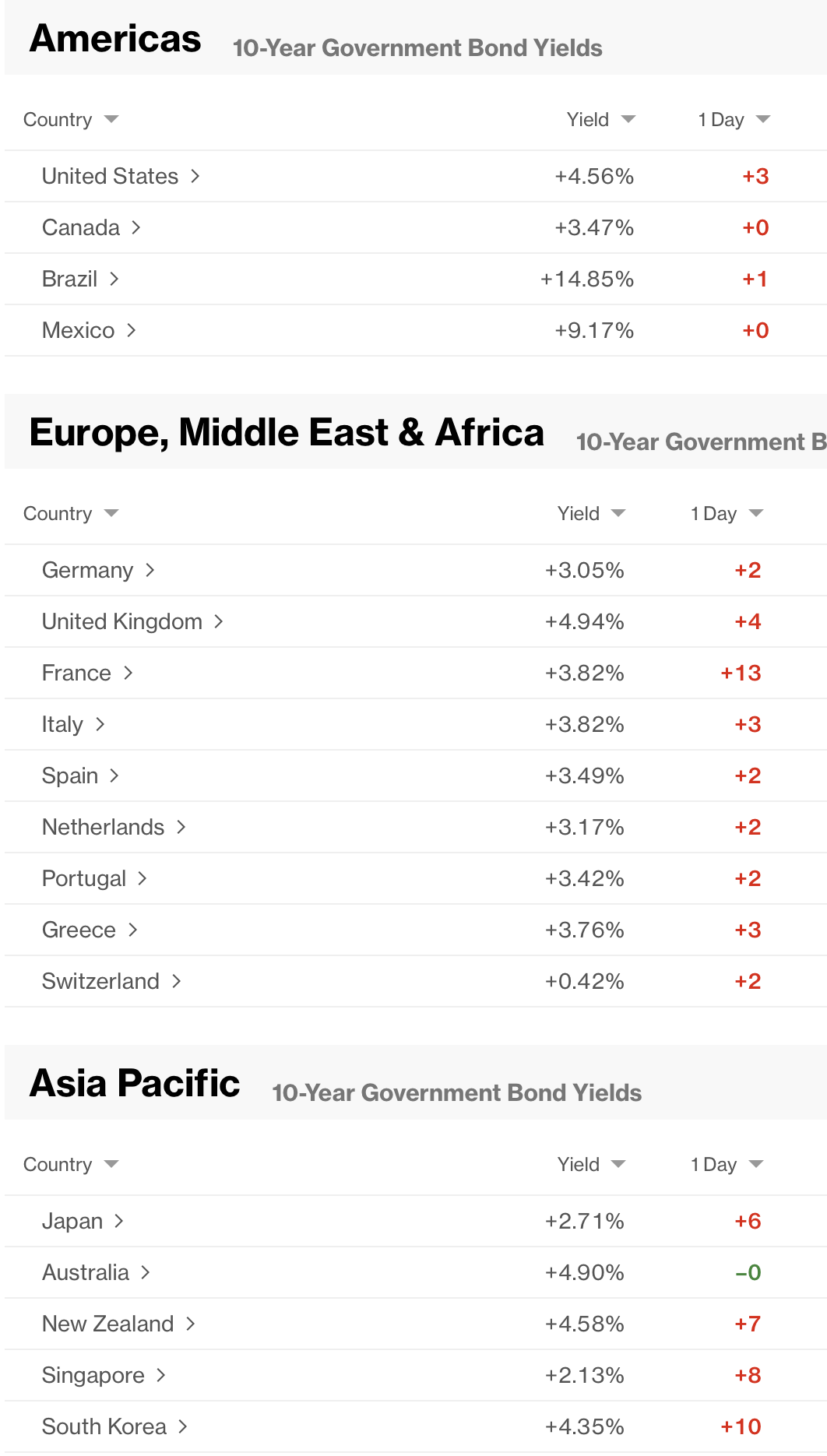

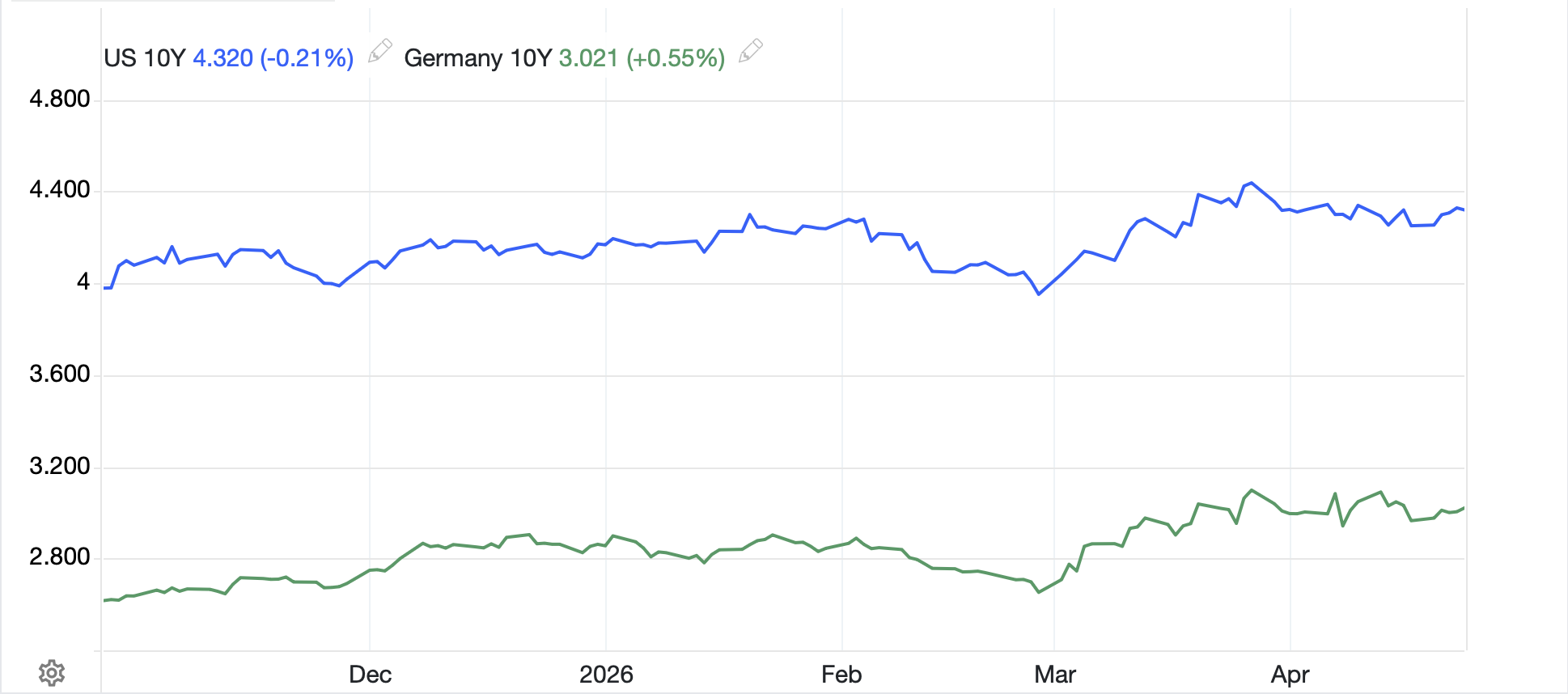

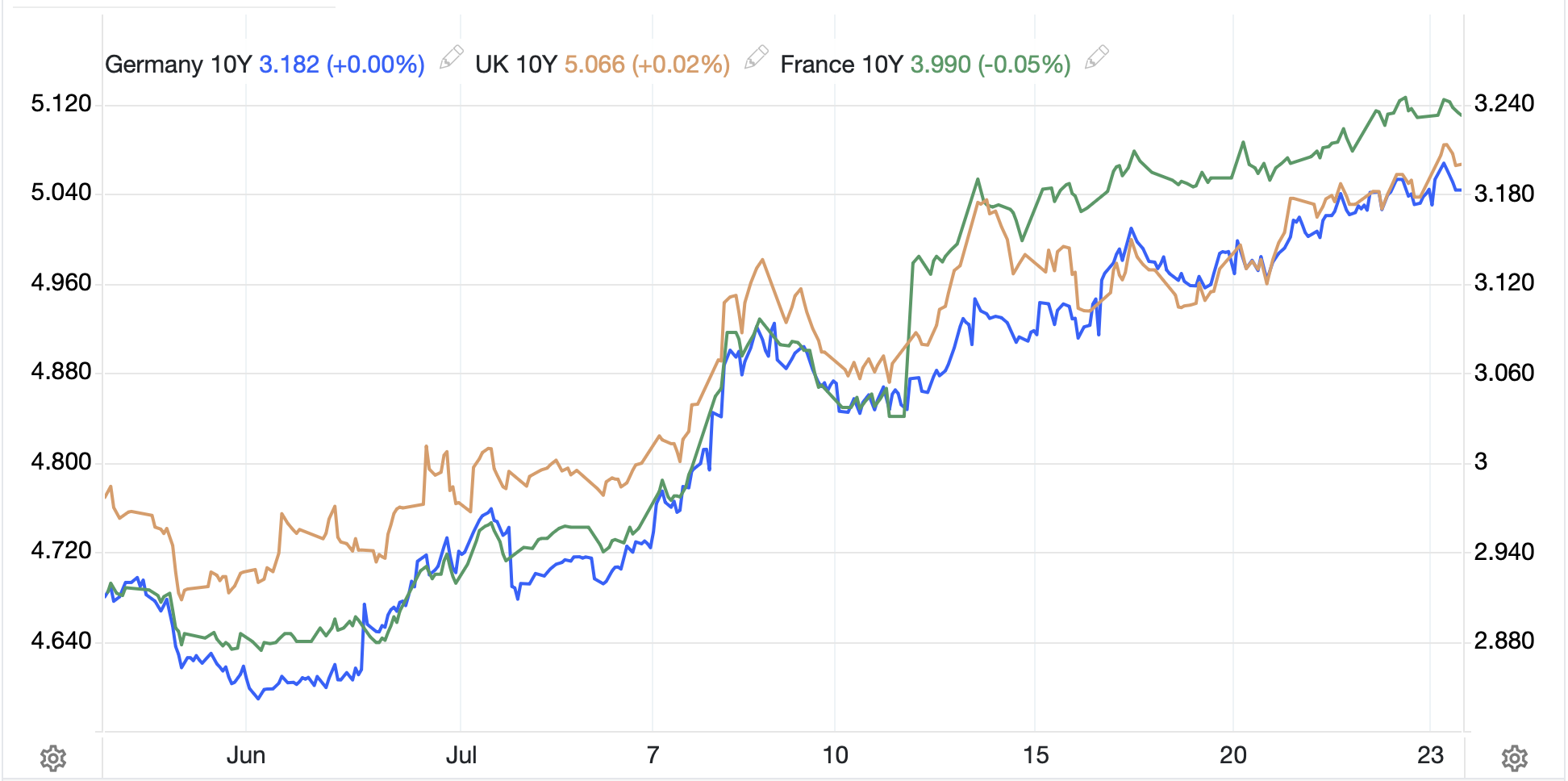

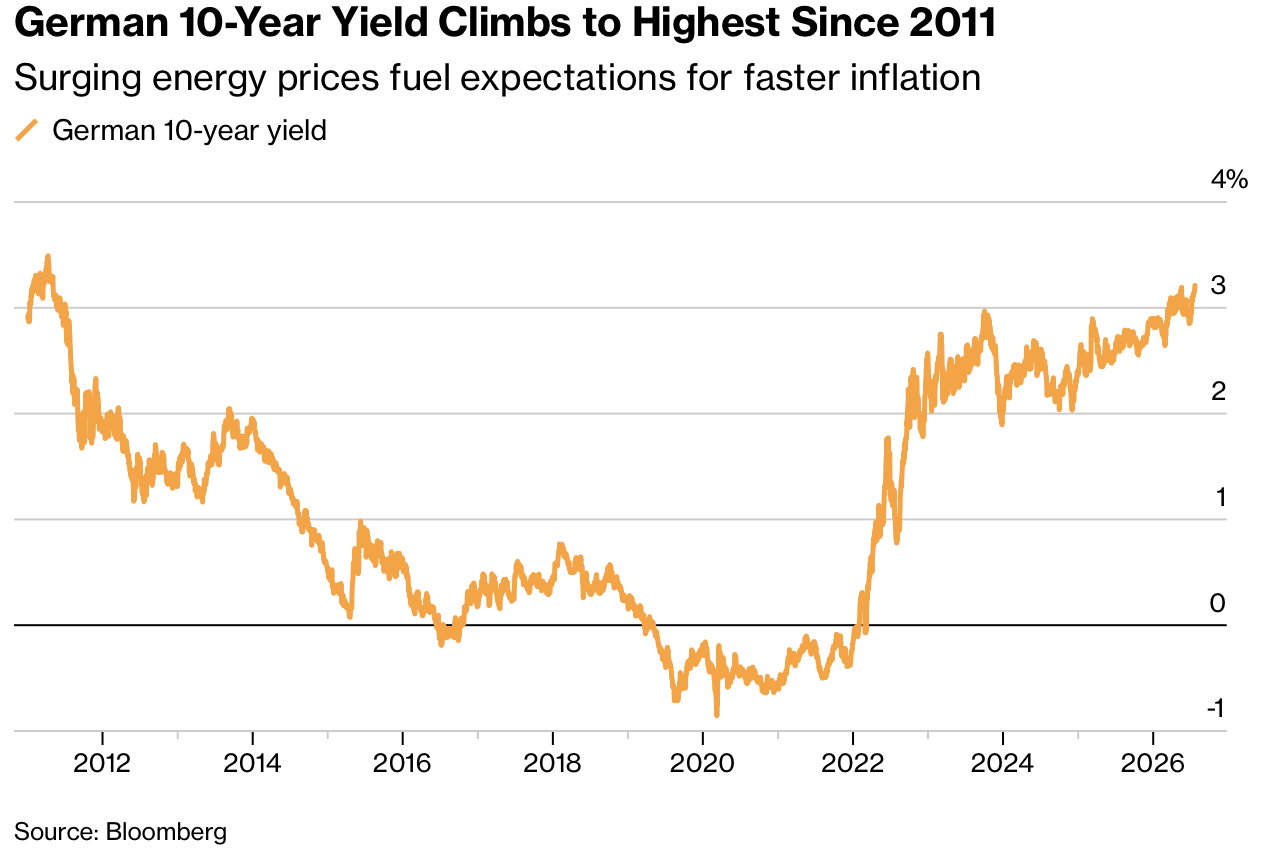

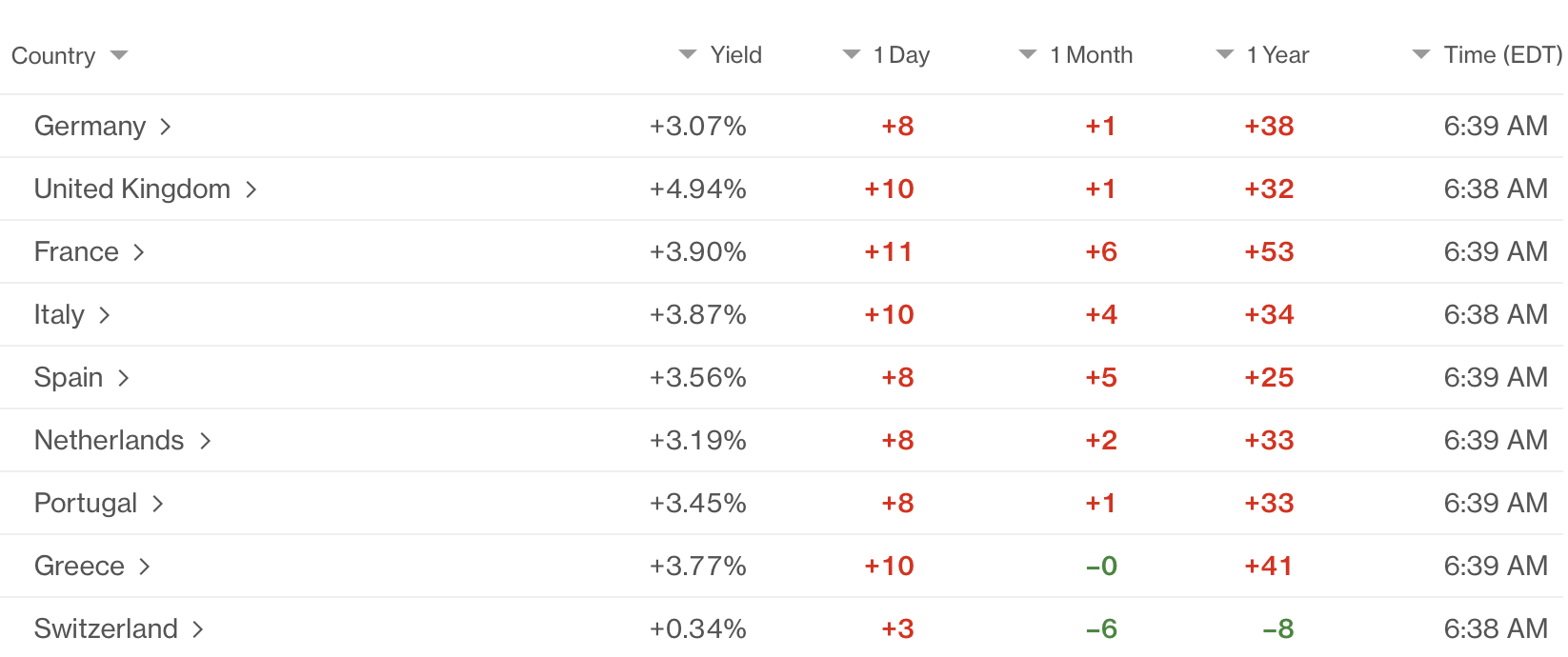

But if we look at 10-year yields across Europe, we can see that they are all climbing in sync as well.

German yields have reached their highest level in 15 years according to Bloomberg.

The entire moderation story is falling apart. So, now instead of conversations discussing the relative merits of AI and whether it will be a boon for mankind or end it, we are discussing the probability that the world will end soon. I guess it’s no surprise that risk is under pressure. Of course, the latter conversation doesn’t seem that coherent to me as if there is concern over the end of the world, I would have thought gold would have a better bid!

At any rate, oil is the main story and the driver of every market. It underpins the question of whether the ECB will hike rates today (they won’t) or whether the FOMC will do so next week (also, they won’t) but the probabilities for those moves have risen. It has also detracted from the earnings stories, or perhaps exacerbated the negatives, or perceived negatives.

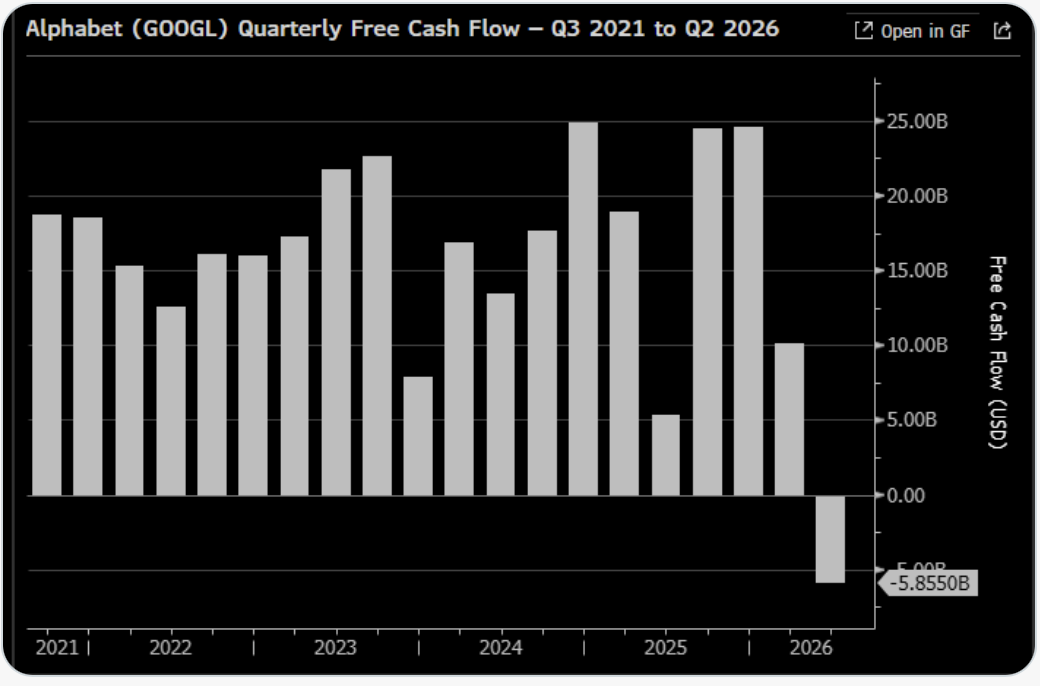

For instance, Alphabet reported last night and Q2 revenues beat estimates coming in at $119.8 billion. But all the talk is of free cash flow, which in this Bloomberg chart shows how much they are spending on the AI buildout.

Here’s my question, is it bad that Alphabet is spending its money to improve its future? If it recognizes the criticality of AI to the future of its own existence, it seems like a reasonable move. Of course, the naysayers claim that spending all that cash is a waste. I don’t know the answer, and I suspect nobody does yet, but companies spending their cash flow on improving their business seems to be the whole idea behind having companies in the first place.

It begs the question, on what did investors base the value of Alphabet before AI? If it was seen as only a cash cow, it certainly traded at a very high multiple for a boring business. But today, it will be tarred with the oil brush along with all stocks.

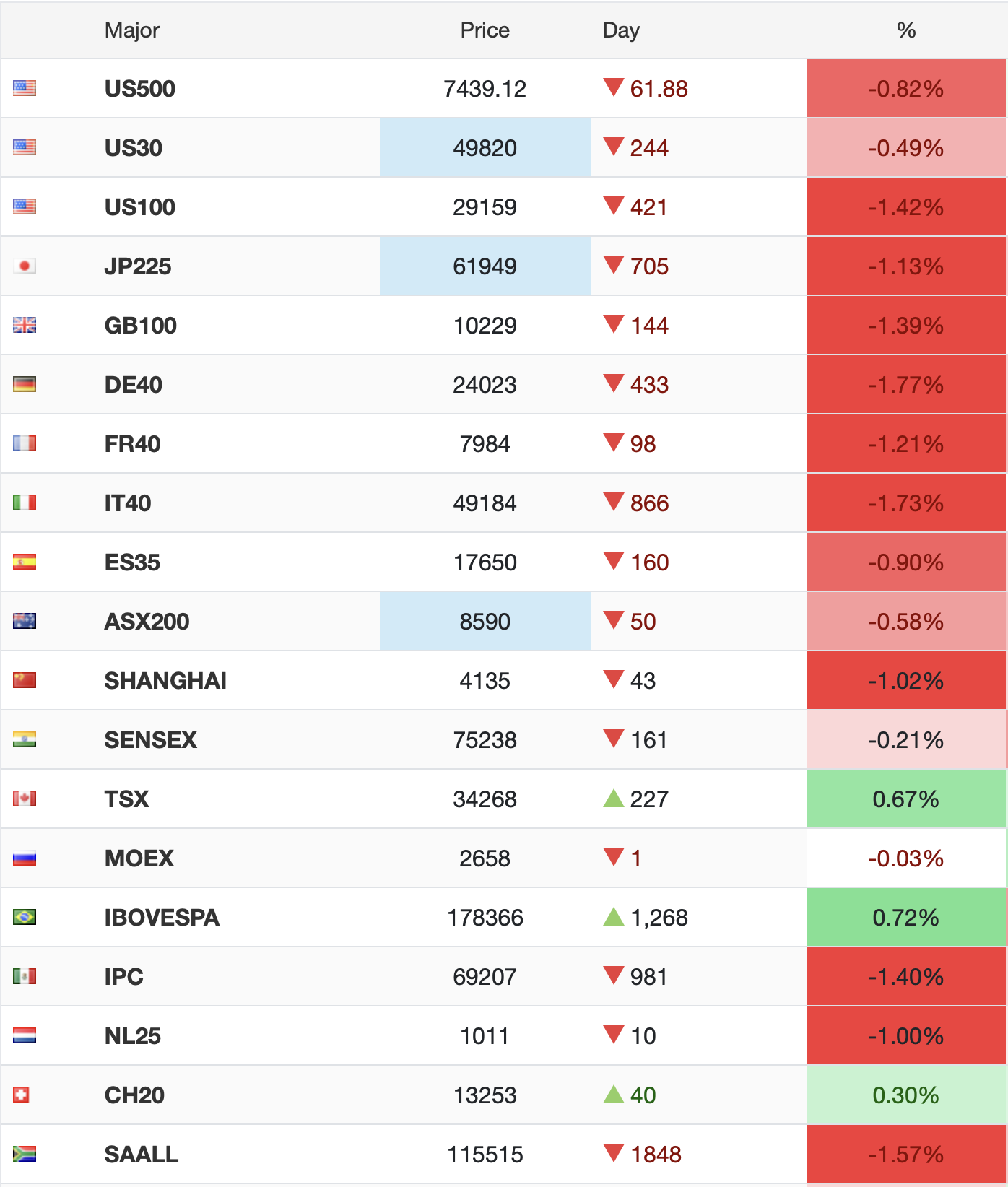

Ok, I have gone far afield here, let’s get back to markets overnight. Yesterday’s lackluster US session was followed by strength throughout most of Asia. Tokyo (+0.5%), China (+0.25%), HK (+1.3%) and Korea (+4.4%) all had solid sessions with Korea continuing to define what volatility means in equity markets. Look at the expansion in the daily ranges in this barchart.com chart of the KOSPI over the past month. It’s remarkable!

European bourses, though, are having a much rougher go of things this morning as Brent crude approaches $100/bbl. France (-1.1%), Italy (-1.9%), Spain (-0.6%) and Germany (-0.6%) are under real pressure this morning as earnings numbers there have been lackluster and the broader macro picture deteriorates all the while. As to US futures, right now (7:40), they are pointing lower led by the NASDAQ (-1.2%) although it has not yet breached that critical support level as per the below chart.

Source: tradingeconomics.com

We’ve already discussed bond markets, with yields higher this morning by between 2bps and 3bps across Treasuries and all European sovereign markets. Turning to the metals, while we had a couple of days where they rallied alongside oil, this morning they have reversed course with gold (-1.3%), silver (-2.6%) and copper (-0.7%) all under pressure. It seems the interest rate story is today’s discussion as higher yields are the topic du jour.

Finally, the dollar is stronger across the board this morning, although most of this strength just materialized over the past few hours with the Asia session broadly unchanged. But no matter how you slice it, the dollar is firmer vs. all its G10 counterparts by about 0.25% and almost all of its EMG counterparts by a similar amount. The exceptions this morning are BRL (+0.25%) and KRW (+0.3%). Regarding Brazil, you must remember they are an oil exporter, so benefit from high oil prices and have amongst the highest real interest rates around, so draw capital for that as well in the carry trade. The real has appreciated about 8.5% during the past year, so this is nothing new. As to KRW, the government’s efforts at internationalization continue to be paying off and a look at the chart below shows that this trend is quite strong right now.

Source: tradingeconomics.com

There was an interesting article in Bloomberg this morning explaining how the dollar’s weakness vs. LATAM currencies has begun to bite for local companies but I find it quite interesting when it comes to discussions about the dollar; some find it too strong and are looking for it to tumble while others complain it is too weak! Seems nobody is ever happy here!

On the data front we see Chicago Fed National Activity (exp 0.14) as well as Initial (212K) and Continuing (1809K) Claims. Of course, we have the ECB announcement shortly, although no change is expected. Something getting very little press is the fact that Crude Oil stocks rose in the US last week, but I guess that doesn’t suit the narrative!

This market is entirely focused on oil, and as it moves, so will everything else. If oil keeps climbing, look for stocks and gold to fall while yields and the dollar rise. If oil reverses, so with those moves.

Good luck

Adf

source: tradingeconomics.com

source: tradingeconomics.com