Said Kevin, the Fed’s now MY house And views that we choose to espouse Will no longer guide So, when we decide To move, we expect some to grouse

As well, we are set to review Our policies all the way through So, comms will be changed And data arranged In truth, it is quite the to-do

This is an evening note as I will be unavailable to write tomorrow morning as we head off to show GCH Nubia’s Take Your Breath Away, aka Marvel to a show. That is his handler and the judge who awarded him Best of Breed that day.

But not surprisingly, the only thing that really mattered today was the FOMC meeting. I have to say, having watched the entire press conference I am really impressed with Chairman Warsh. I love the fact that he shortened the statement and that they are ending forward guidance. And it was quite interesting that half the reporters’ questions were trying to get guidance about what the Fed may do in the future, despite him repeating that there was no more forward guidance. My take is Fed reporters are going to have to learn about how markets work and more importantly, market practitioners are going to make up their own minds rather than rely on the Fed to bail them out. This is all really positive!

The most noteworthy thing was the creation of five task forces to address issues with the way the Fed currently does things on the following subjects:

Communications

Balance Sheet

Data Sources

Productivity and Jobs

Inflation Framework

So, it strikes me that Chairman Warsh is going to look to reprogram the Fed, something that has been sorely in need. Do not be surprised when much of the commentary is negative on these subjects because those are the folks who benefitted from the old way of doing things. They now need to change their models and their narratives and they are unhappy. Another benefit.

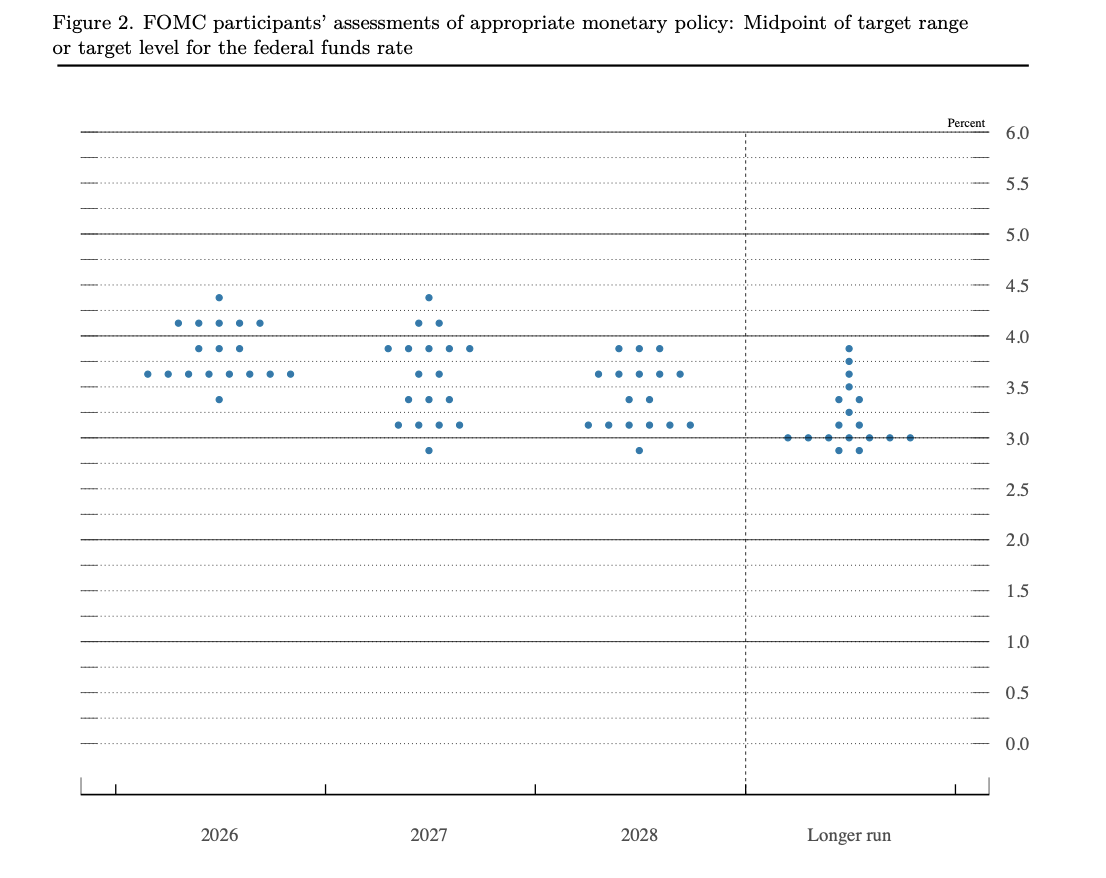

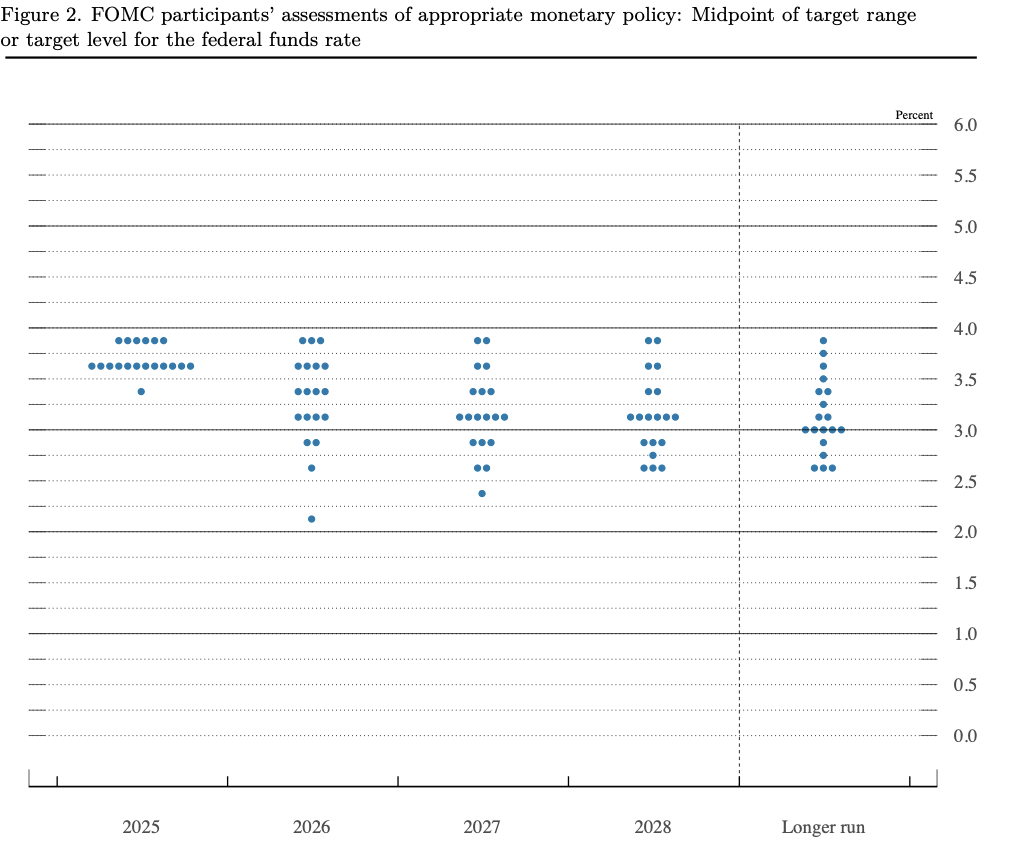

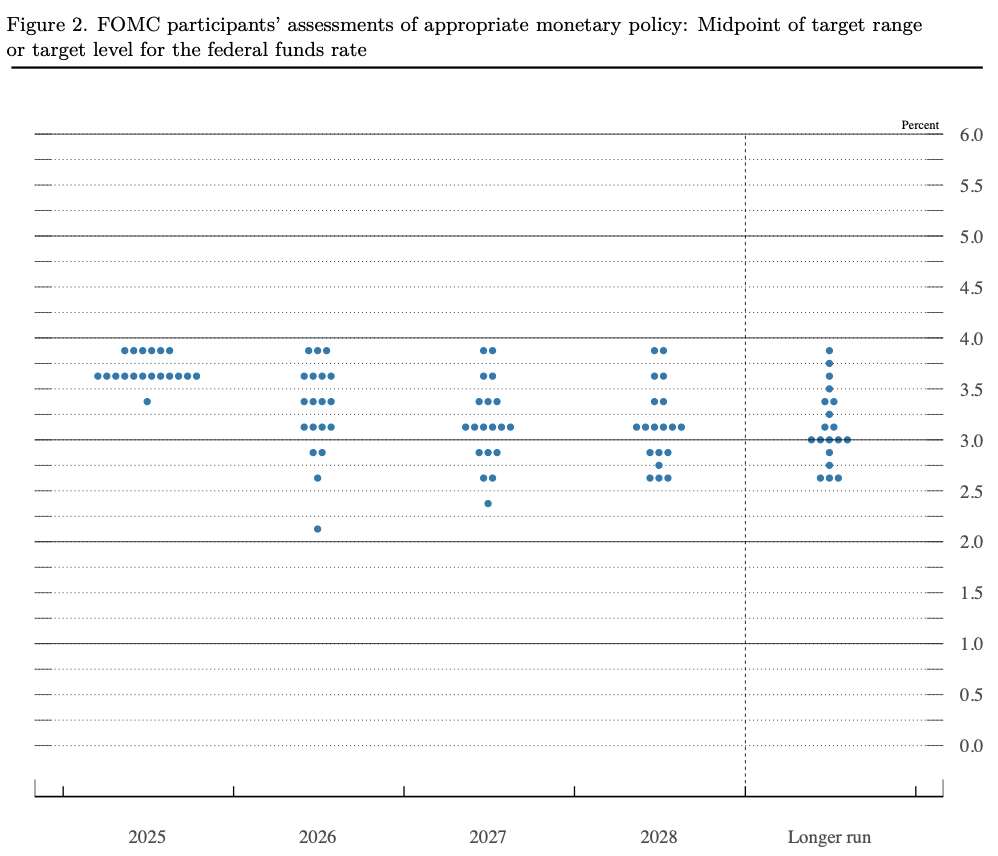

The upshot of the meeting was that rates were left on hold and the dot plot, where Warsh did not supply a dot, showed that half the committee thought rates appropriate, and half thought they would be higher by the end of the year.

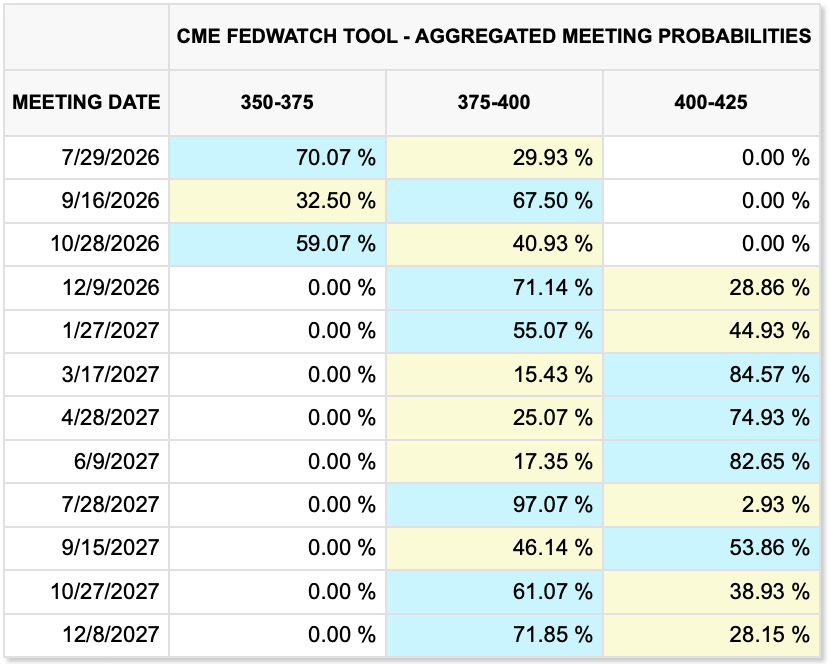

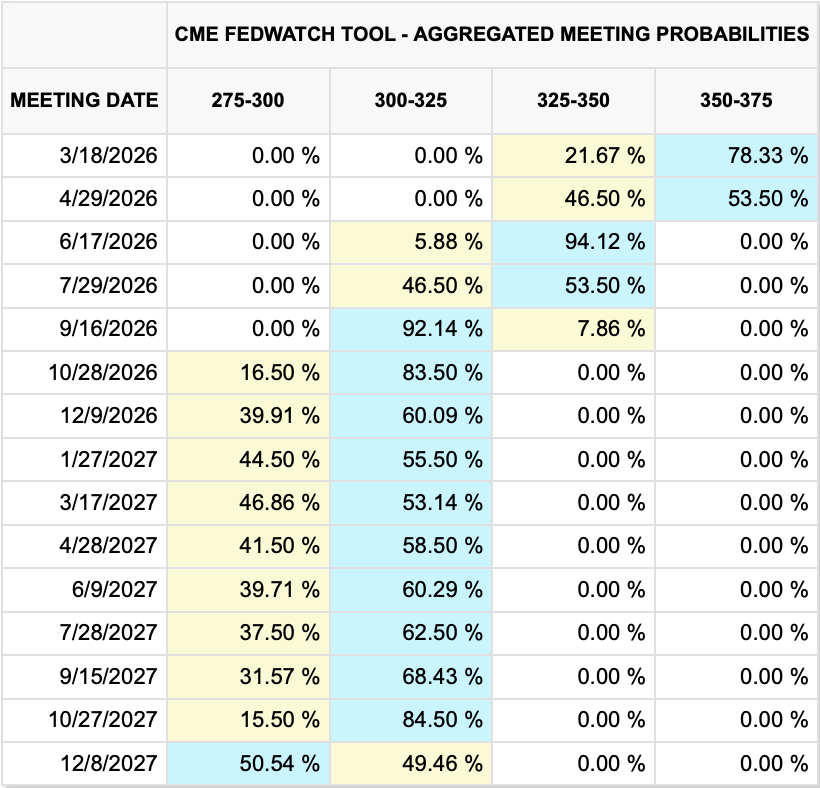

Of course, this largely jibes with the Fed funds futures market as you can see in the latest table from the CME.

Of course, looking at this table, something seems amiss for September, perhaps there was a large position put in place that drove the market. At any rate stock markets were unhappy with the major indices slipping -1.0% or more after the FOMC although bonds did very little and commodities continue to show oil slipping while gold and silver rise. As to the dollar, it rallied pretty much across the board.

It is way too early to anticipate exactly how things are going to play out, but I am encouraged. I strongly believe a little price volatility is a small price to pay to reduce systemic risk by reducing leverage in the system, and that is very likely to be the outcome if Mr Warsh has his way. My forecast is the “ample reserves” balance sheet program is going to change before he is done. If that is the case, I think they will have a real opportunity to get inflation under control. As well, I believe that prospect will undermine much of the ‘death of the dollar’ narrative. It truly will be significant. We shall see.

The story today is the Fed And whether, when looking ahead Inflation they see Stays well above three Or if it just might fall instead

Meanwhile, every comment I’ve read Discussing the ‘deal’ have all said Too much was conceded The US retreated And look to the future with dread

Starting with the MOU with Iran, and having read the text of the agreement, at least the one published by Bloomberg, Iran has sworn to never have a nuclear weapon and then will effectively be readmitted to polite society, with sanctions and restrictions eventually removed. The several comments I have read on the deal highlight numerous potential loopholes and semantics regarding tolls and fees and are uniformly unhappy with the deal. But I’ve also read that many on Iran’s side are unhappy with the deal. Arguably, the best sign the deal is going to last is just that, neither side got everything they wanted, but both got some of the things they wanted. Time will tell how this all plays out, but certainly the oil market remains positive that the direction of travel is toward a normalization of flows through the Strait of Hormuz.

However, while the political pundits are going to continue to focus on that issue, markets have turned their focus to the FOMC meeting and how things play out under new Chairman Kevin Warsh. The previous Fed whisperer, Nick Timiraos at the WSJ, continues to push Governor Powell’s message as there is not yet a new Fed whisperer. My take is Timiraos will not be the one simply because his loyalties will not lie with Warsh.

The thing in which we can be most confident is there will be no rate change at today’s meeting although the market continues to price a rate hike in December as per the below CME table.

All the drama will come with the release of the SEP (Summary of Economic Projections) which is the quarterly document the Fed publishes showing the range of economic forecasts by the individual FOMC members regarding GDP, Unemployment and interest rates. This document also includes the dot plot. It is important to note that the SEP only started to be released in 2007, so this is not a long-standing tradition, but part of Ben Bernanke’s changes to the institution.

And this is a key feature of what makes Kevin Warsh different. He has indicated that the Fed talks too much (I agree) and believes that some ambiguity in what is going on is a desired outcome. This is a controversial stance as Wall Street has minted money on the back of forward guidance, recognizing the Fed has their back whenever they blow up because they built up huge leverage and were wrong.

While I completely understand the idea that political discussions need to be in the open, I am far more suspect with respect to monetary policy discussions. Prior to forward guidance, market participants were far more cautious in their positioning as the probability of getting the direction of a trade wrong was far greater. But once the Fed says, ‘rates are going to stay low for a very long time’, traders can lever up positions massively relying on the fact that their funding costs are going to remain in check. And it is the massive leverage where the risks to the market lie, not the level of rates per se.

So, the question today is how Chairman Warsh will handle his desire to reduce communications compared to the previous actions of publishing the data and numerous FOMC members speeches. One thought is he may refuse to put his own forecasts into the document, a sign of what he wants going forward but I am confident he has other ways to move forward.

The other issue is the question of the tone of the statement, which had ostensibly been leaning dovish but seems now likely to be neutral. My sense is whatever he does, it will be incremental, at least at the beginning, but I anticipate that he is going to make substantial changes to the way the FOMC operates during his tenure as that is why he was put in the role.

So, with that as our backdrop, let’s see how markets have absorbed the text of the deal as we all await the FOMC this afternoon. Yesterday’s mixed US performance, with only the DJIA managing a gain while tech stocks dragged down both the NASDAQ and the S&P, was followed by more positivity than not in Asia with gains in Japan (+0.7%), China (+1.0%), Korea (+1.6%) and India (+0.5%) while HK (-0.75%) slipped a bit. It is always a bit of a surprise when HK and China move in opposite directions, and it seems today’s split arose from different interpretations from a policy conference regarding future PBOC activities as well as potential future government support for a clearly weakening consumer economy. Other regional exchanges had a mix of gainers and laggards as well, as the overall session was directionless.

In Europe, the picture is also mixed although the movement has been more muted than those in Asia. Both Germany and the UK are flat to slightly lower this morning with the former under pressure after BMW offered a terrible profit forecast while the latter, despite lower-than-expected inflation readings, is lagging on growth concerns. However, France (+0.2%) and Spain (+0.5%) have both managed to rally a bit on some slightly positive earnings news. As to US futures, at this hour (7:15), they are modestly higher across the board.

Bond yields are generally little changed this morning with only UK gilts (-5bps) and JGBs (-4bps) showing any movement at all. Gilts responded positively to the inflation data while JGBs seemed to take solace in the trade data showing Japan was back to a deficit.

In the commodity markets, oil (+0.7%) is having a very quiet session after several sharp declines in a row while metals markets are largely unchanged this morning. It appears even traders here are awaiting the FOMC outcome. One thing I have seen is a recent report from the World Gold Council showing 45% of central banks surveyed plan to buy the barbarous relic in the next 12 months.

And finally, the dollar is slightly stronger this morning, but like most other markets, not showing much movement at all. The below chart of the DXY for the past month shows just how lackluster price action has been with a total range of just 1.5%. The red line is the midpoint of that range showing there is just not a lot of pressure in either direction right now.

Source: tradingeconomics.com

Meanwhile, USDJPY has basically spent the past two weeks hovering just above 160.00 with nary a peep from the MOF or BOJ. Again, the situation there is the policy changes necessary to strengthen the yen are likely to have very negative economic consequences initially, and that is not something any government is likely to do.

On the data front, ahead of the Fed we see Retail Sales (exp +0.5%, +0.5% ex-autos) and then the EIA oil inventories with more draws expected. And that’s really all there is. I anticipate a very quiet session ahead of the Fed and then all will depend on how the market interprets Warsh’s signals.

Said Jay, I will not be ignored And so, I ain’t leaving the board When my time as Chair Is up, and I swear I will see the president gored

So first off, we ain’t cutting rates ‘Cause here in the United States Inflation’s a worry And I’m in no hurry To help Trump escape dire straits

I guess we cannot be surprised that Chairman Powell was combative during his press conference yesterday after the Fed left rates on hold, as expected. There was only one dissent this month, Governor Miran, still looking to cut rates. However, while standing pat given the high level of uncertainty that exists from the war situation makes sense, compare the dot plot from this meeting to the December meeting below it. The dispersion of views on the committee has really tightened up a lot. While the median for 2026 continues to point to one cut, it appears that the Fed now believes we are near r*, although they didn’t say that exactly.

March 2026 dot plot

December 2025 dot plot

The other noteworthy comment from the Chair was when he explained he had “no intention of leaving” the Fed until the Justice Department investigation is completed. And, if Kevin Warsh is not confirmed by the Senate by the end of Powell’s term as Chair on May 15th, he will remain as Chairman pro tempore, the same situation as his previous nomination when the Senate delayed his confirmation.

The market response to both the combative tone and the hawkish rhetoric overall was a further 1% decline in the S&P 500 from an already weak place as per the below chart where I highlighted the time of the Statement release. You can see how things behaved thereafter.

Source: tradingeconomics.com

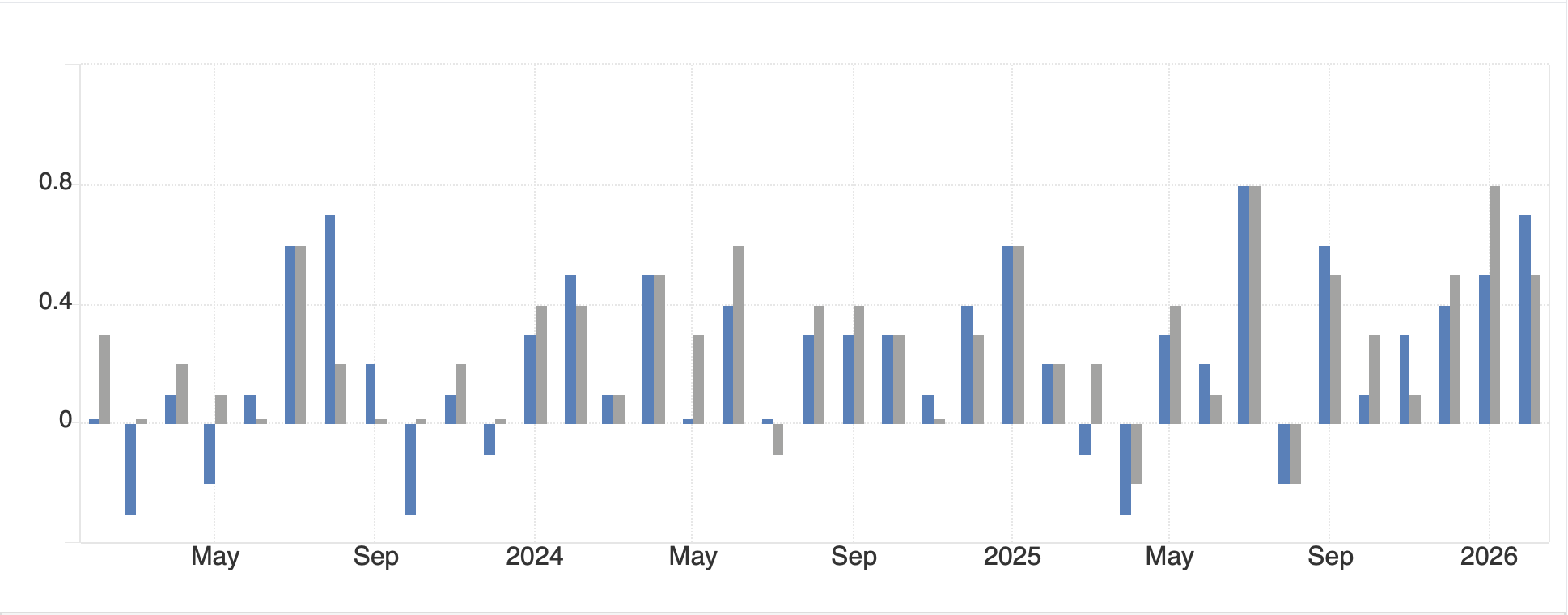

But that wasn’t all that happened yesterday, PPI came out MUCH hotter than forecast with headline at 0.7% (3.4% Y/Y) and core at 0.5% (3.9% Y/Y) as inflation concerns rose to the fore. If you look at the PPI chart below showing both headline (blue bars) and core (gray bars), it is very difficult to discern a pattern of declining producer prices.

Source: tradingeconomics.com

In fact, it is hard to look at this data and reconcile it with the Fed’s SEP forecasts describing the view that inflation, even their measure of core PCE, is going to smoothly return to their 2% target over any particular timeline.

One last event of note was the Iranian response to an attack on its main Natural Gas field, South Pars, where they inflicted serious damage to the Ras Laffan LNG facility in Qatar, which happens to be the largest in the world and is on the wrong side of the Strait of Hormuz to boot. The result has been a significant rise in the price of European (and UK) natural gas, with both soaring more than 20% this morning while, Brent crude has jumped 7.2% as opposed to WTI’s unchanged status today. This has taken European NatGas to ~$22.MMBtu compared with the US price of $3.15. Ask yourself how long Europe can afford to pay 7x US prices for NatGas and maintain any competitive ability to manufacture anything. (As an aside, this remains a key reason that I see long-term prospects for the euro so dimly.) But if we look at the longer-term chart of European NatGas, despite the dramatic increase since the Iran conflict began, it is nothing compared to what we saw in the wake of Russia’s invasion of Ukraine.

Source: tradingeconomics.com

Summarizing yesterday’s session in one word, I would say, Aaaaaaggggghhhhhh!

I assume I have depressed you enough with yesterday’s activities, but I will run through market responses overnight. You won’t be surprised to learn they have not been positive.

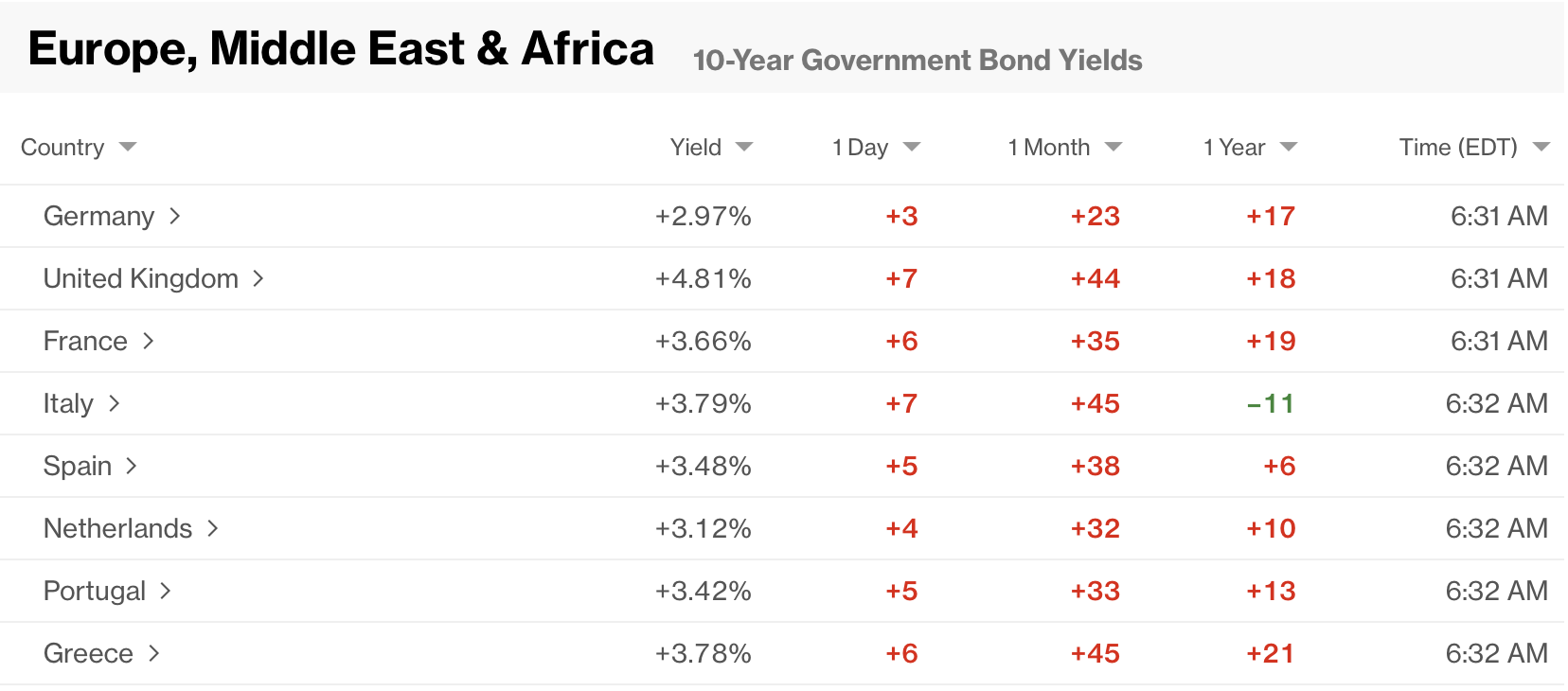

In fact, I guess I will start with bonds this morning, which I didn’t discuss above, but not surprisingly given the high PPI readings and the sharp rise in oil and gas prices, have suffered a lot. Yesterday, Treasury yields reversed their early declines and closed higher on the day by 6bps. They have edged up another 1bp this morning and are back above that 4.20% range I have focused on. Meanwhile, European sovereign markets were all closed when the FOMC meeting concluded, which added to the pressure on bond yields which started with the US PPI data. Net, yesterday, German bunds rose 4bps and this morning they are higher by a further 3bps. But as you can see from the below Bloomberg screenshot, they are the champs in Europe today.

JGB yields also rose sharply, up 6bps and we saw similar rises throughout Asian bonds. Right now, it is very clear that inflation is a bondholder’s concern, not recession.

As to equity markets, you will not be surprised to know that every market in Asia declined, most by more than -1.0% with the Nikkei (-3.4%) the worst performer followed closely by India’s Sensex (-3.1%), but there was no place to hide in Asia. In Europe, the damage is equally broad, although there is one outlier, Norway (+0.5%) which is obviously benefitting from the sharp rise in oil prices. But otherwise, -1.5% to -2.5% is today’s story across the board there. Interestingly, at this hour (6:45) US futures are little changed to slightly lower, just -0.1%. Perhaps this is a sign that all is not lost. Or maybe the algorithms just haven’t started their day yet. One noteworthy decline is South African shares (-4.0%) which is suffering from gold getting sold off yet again yesterday and today.

Since we already touched on energy, a quick trip through metals markets sees a major rout ongoing with gold (-2.75%) and silver (-5.2%) both suffering greatly, as is copper (-2.5%) and platinum (-6.1%). I continue to believe that gold is being liquidated to pay for other losses as the primary attraction of the barbarous relic remains. One thesis is that Middle Eastern central banks are liquidating their holdings as, given the dramatic decline in their oil revenues, they need money for continuing operations, and arguably, that’s what the gold is for. Essentially, gold is the rainy-day fund. As to the other three metals, those hint more at slowing economic activity rather than forced liquidation. After all, there was a lot of euphoria on the way up, so if the narrative is changing, as that dissipates, so will demand.

Finally, the dollar has given back a small portion of yesterday’s solid gains but remains at the top of its 96.00 / 100.00 trading range as defined by the DXY and shown in the chart below.

Source: tradingeconomics.com

Again, considering energy policies and availability around the world, the US, which is the largest energy producer in the world and a net exporter of energy products, seems better positioned than any of its competitors to weather the current economic gyrations. However, if we look across specific currency pairs this morning, we see relative strength elsewhere on the order of 0.2% to 0.3%. Frankly, it is a bit surprising to see ZAR (+0.4%) rally given what is happening in both gold and the South African equity market, but stepping back slightly, given the rand’s weakness since the end of January, I guess we cannot be that surprised that there is consolidation. Certainly, there is nothing about the chart for the last month that indicates the rand is about to reverse course and strengthen dramatically.

Source: tradingeconomics.com

The big picture here remains, in my view, that the US has more pluses than minuses vs almost all its counterparts.

On the data front, I didn’t even mention last night’s BOJ meeting, where they left policy on hold, as it didn’t seem to have a major impact. Perhaps, Ueda’s mildly hawkish comments have helped the yen a bit this morning. As well, the Swedish Riksbank left policy on hold and in a short while we expect both the BOE and ECB to leave policy rates on hold. The one which might move is the UK, where last time they voted 7/2 to leave policy unchanged but analysts think 4 members could vote for a cut. However, my sense is that cutting rates at this time, before there is evidence that the economy is truly suffering from the war, would be a surprise. Otherwise, we get the weekly Initial (exp 215K) and Continuing (1850K) Claims as well as the Philly Fed (10.0) and then at 10:00 we see New Home Sales (720K). One other thing to note is that yesterday’s EIA data showed a substantial build in crude inventories, but a large draw in gasoline and distillates. It is this activity that helps explain the rise in crack spreads, and why the refiners should be having a very good quarter.

And that’s it for today. Quite frankly, that’s enough for me. As it happens, there will be no poetry tomorrow, so I will get to recap today and tomorrow on Monday and see what has changed in the Persian Gulf as well as any other new news.

The focus has turned to the data And whether it’s good or it’s bad-a We all want to see Today’s NFP Then listen to punditry chat-a

It’s funny, cause generally speaking Most pundits are strongly critiquing The numbers released Declaring they’re greased To help Trump and havoc he’s wreaking

It’s NFP day today, which given it is Wednesday is a bit odd, but that’s what happens when the government shuts down for a few days. At any rate, this is the biggest data week we’ve had in a while as not only did we see Retail Sales yesterday, which disappointed at 0.0% despite showing the largest actual jump, $80 billion, ever between November and December, although that was completely removed by the largest seasonal adjustment ever, (Read about it here at WolfStreet.com) we also get CPI on Friday. For good order’s sake, here are the current consensus forecasts for NFP:

Nonfarm Payrolls

70K

Private Payrolls

70K

Manufacturing Payrolls

-5K

Unemployment Rate

4.4%

Average Hourly Earnings

0.3% (3.6% Y/Y)

Average Weekly Hours

34.2

Participation Rate

62.3%

Source: tradingeconmomics.com

As the market continues to adjust to the recent gyrations, there is hope that the data will lead to unequivocal conclusions about the economy, which could drive Fed decisions and then coalesce around a clear direction of travel. I’m not holding my breath.

The first thing to remember is that the data is revised virtually every month, and when the economy is at an inflection point, or even when it is showing more pronounced activity in one sector than another, those revisions can tell a very different story than the original print. But even beyond that, while the algorithms are clearly programmed to respond to the data, longer term investors have a much tougher time discerning what is happening. All that is a long way of saying, nobody still has any idea where things are headed!

While I dismiss the FOMC speaking circuit, yesterday’s two speakers, Logan and Hammack, who are both voting members this year, said that they felt the current rate is at neutral. Remember, right now Fed funds are 3.75%, which is a far cry from the Longer run neutral rate they have been feeding us in the Dot Plot!

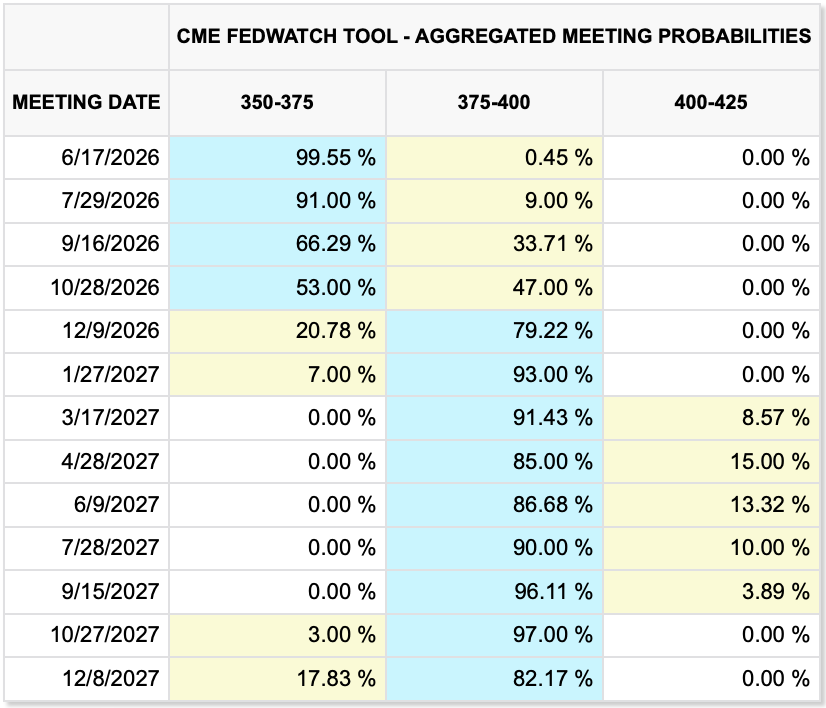

In fact, their median expectation is 3.0%, so the fact that two voting members think 3.75% is neutral is somewhat confusing especially as both indicated they expected inflation to continue to decline and exhibited concern over the employment situation. My views of where things are headed don’t matter nearly as much as theirs do, but there seems to be a little inconsistency involved here. As it happens, the current Fed funds futures market pricing shows that there is a 22% probability of a rate cut in March and then it’s 50:50 in April as per the below chart fromcmegroup.com.

At this point, I suspect we will need to see negative NFP numbers along with continuing declines in CPI/PCE for the Fed to cut as I think Chairman Powell is so miffed at President Trump, he doesn’t want to do anything that Trump wants. It would also not surprise me if that attitude has suffused the bulk of the FOMC. The irony remains that Governors Cook and Jefferson are raging doves but would rather keep policy tight to stymy Trump rather than act as they otherwise would. At least that’s my take.

Anyway, that’s what we have to look forward to this morning. So, how have things behaved overnight? Let’s look. Tokyo (+2.3%) continues to be the star of the show, continuing to rally on excitement and optimism that PM Takaichi is going to solve Japan’s problems. Maybe she will, but they have a lot of them, so it will take time. But the tech story is strong there and it appears that foreign buying is picking up, which has been one of the drivers of the JPY (+0.5%) lately. In fact, this week, the yen is leading all currencies having gained more than 2.3% so far.

Source: tradingeconomics.com

As to the rest of Asia, China (-0.2%) and HK (+0.3%) did little although the tech-based Korean (+1.0%) and Taiwanese (+1.6%) exchanges did well, as did Australia (+1.6%) on the back of stronger metals prices. One other interesting note is Indonesia (+2.0%) where the government just restricted mining of Nickel (+1.7%) in order to raise the price of their largest export!

Europe is a lot less interesting with the continent under some pressure (France -0.2%, Spain -0.3%, Germany -0.2%) although the UK (+0.7%) is performing well on the back of strength in mining and natural resource shares. US futures at this hour (7:35) are pointing slightly higher, about 0.15%.

In the bond market, things have gone back to sleep with 10-year yields lower by -1bp pretty much throughout the US and Europe. JGB yields also did nothing last night, and it appears that despite the massive debt that continues to grow around the world, bond investors are comfortable right now. Perhaps they see deflation in our future, but that doesn’t feel right to me.

Turning to the markets that continue to show the most volatility, commodities, let’s start with oil (+2.1%) which is demonstrating concern over re-escalating tensions regarding Iran, the negotiations and the potential for military activity there. There are reports that the US may intercept Iranian tankers and if you look at the chart below, a pretty good uptrend has developed over the past two months. You won’t be surprised that NOK (+0.6%) has benefitted from today’s move either.

Source: tradingeconomics.com

As to the precious metals, after yesterday’s modest decline, we are back on the rise with gold (+0.85%), silver (+5.5%), copper (+2.1%) and platinum (+3.3%) all nicely higher. The silver story is about declining inventories in Shanghai, which was the last place that can afford it since both the COMEX and London are already light on available ounces. While we saw a dramatic decline nearly two weeks ago, I have to say things appear to be shaping up to recoup all those losses and then some!

Finally, the dollar is back under pressure this morning across the board. I’ve already mentioned the two biggest movers and AUD (+0.5%) joins the list on the back of commodity strength. Otherwise, the movements are not terribly large here, with the euro (+0.1%), pound (+0.3%), KRW (+0.3%), and ZAR (+0.2%) indicative of the situation. I expect that the dollar will be responsive to today’s NFP data with a strong print helping the dollar and a weak one pushing it down a bit further. However, remember that it remains within its trading range, albeit nearer the bottom than the top of that range as per the below.

Source: tradingeconomics.com

And that’s really it for today. The NFP should drive the first movement and after that, there is still White House bingo for fun and surprises. While the dollar is soft, I don’t see a collapse coming, and in the end, the more I read about EU energy policy, I can only expect that any collapse will be that of the euro, not the dollar. But that is a ways into the future I think.

There once was a time when the Fed When meeting, and looking ahead All seemed to agree The future they’d see And wrote banal statements, when read

But this time is different, it’s true Though those words most folks should eschew ‘Cause nobody knows Which way the wind blows As true data’s hard to construe

So, rather than voting as one Three members, the Chairman, did shun But crazier still The dot plot did kill The idea much more can be done

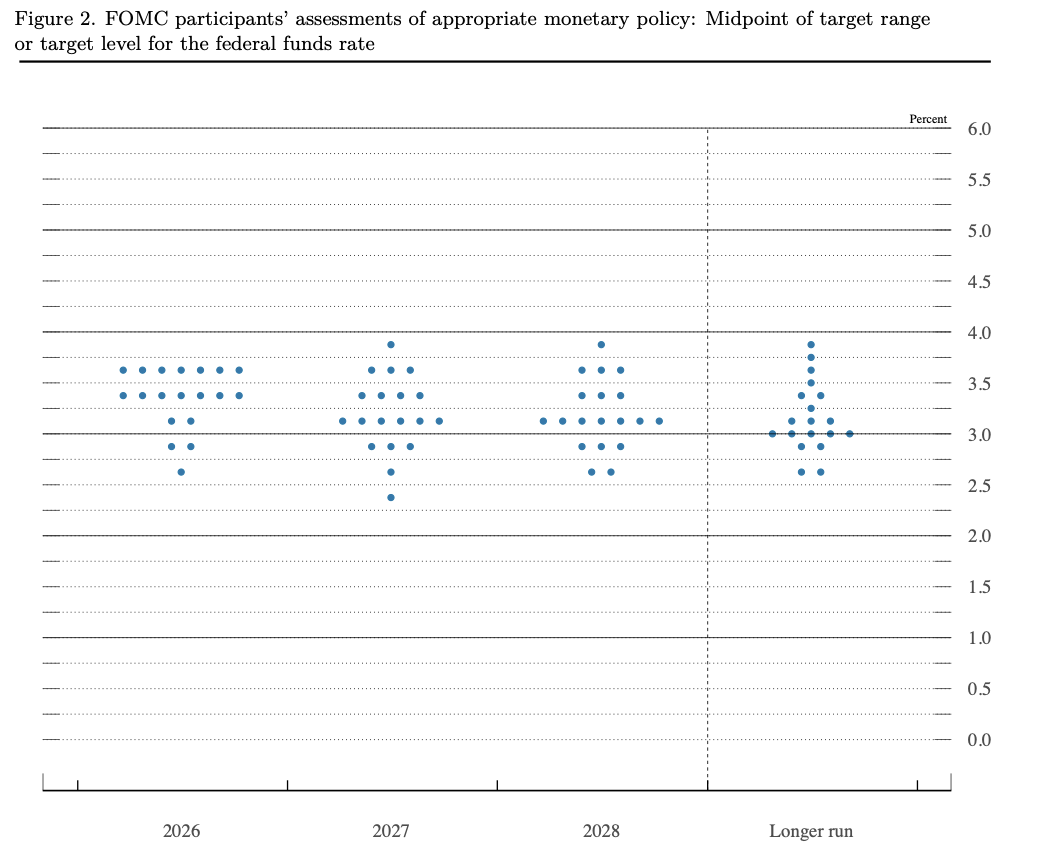

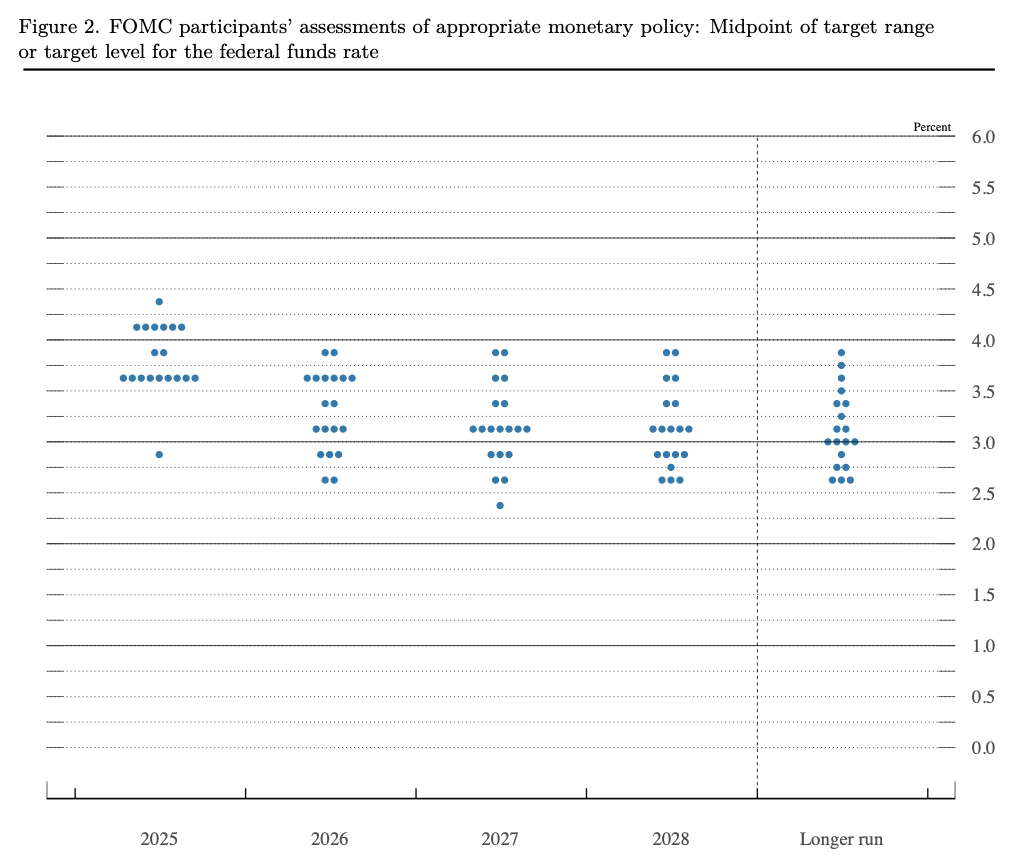

I think it is appropriate to start this morning’s discussion with the dot plot, which as I, and many others, expected showed virtually no consensus as to what the future holds with respect to Federal Reserve monetary policy. For 2026, the range of estimates by the 19 FOMC members is 175 basis points, the widest range I have ever seen. Three members see a 25bp hike in 2026 and one member (likely Governor Miran) sees 150bps of cuts. They can’t all be right! But even if we look out to the longer run, the range of estimates is 125bps wide.

Personally, I am thrilled at this outcome as it indicates that instead of the Chairman browbeating everyone into agreeing with his/her view, which had been the history for the past 40 years, FOMC members have demonstrated they are willing to express a personal view.

Now, generally markets hate uncertainty of this nature, and one might have thought that equity markets, especially, would be negatively impacted by this outcome. But, since the unwritten mandate of the Fed is to ensure that stock markets never decline, they were able to paper over the lack of consensus by explaining they will be buying $40 billion/month of T-bills to make sure that bank reserves are “ample”. QT has ended, and while they will continue to go out of their way to explain this is not QE, and perhaps technically it is not, they are still promising to pump nearly $500 billion /year into the economy by expanding their balance sheet. One cannot be surprised that initially, much of that money is going to head into financial markets, hence today’s rally.

However, if you want to see just how out of touch the Fed is with reality, a quick look at their economic projections helps disabuse you of the notion that there is really much independent thought in the Marriner Eccles Building. As you can see below, they continue to believe that inflation will gradually head back to their target, that growth will slow, unemployment will slip and that Fed funds have room to decline from here.

I have frequently railed against the Fed and their models, highlighting time and again that their models are not fit for purpose. It is abundantly clear that every member has a neo-Keynesian model that was calibrated in the wake of the Dot com bubble bursting when interest rates in the US first were pushed down to 0.0% while consumer inflation remained quiescent as all the funds went into financial assets. One would think that the experience of 2022-23, when inflation soared forcing them to hike rates in the most aggressive manner in history, would have resulted in some second thoughts. But I cannot look at the table above and draw that conclusion. Perhaps this will help you understand the growth in the meme, end the fed.

To sum it all up, FOMC members have no consensus on how to behave going forward but they decided that expanding the balance sheet was the right thing to do. Perhaps they do have an idea, but given inflation is showing no signs of heading back to their target, they decided that the esoterica of the balance sheet will hide their activities more effectively than interest rate announcements.

One of the key talking points this morning revolves around the dollar in the FX markets and how now that the Fed has cut rates again, while the ECB is set to leave them on hold, and the BOJ looks likely to raise them next week, that the greenback will fall further. Much continues to be made of the fact that the dollar fell about 12% during the first 6 months of 2025, although a decline of that magnitude during a 6-month time span is hardly unique, it was the first such decline that happened during the first 6 months of the year, in 50 years or so. In other words, much ado about nothing.

The latest spin, though, is look for the dollar to decline sharply after the rate cut. I have a hard time with this concept for a few reasons. First, given the obvious uncertainty of future Fed activity, as per the dot plot, it is unclear the Fed is going to aggressively cut rates from this level anytime soon. And second, a look at the history of the dollar in relation to Fed activity doesn’t really paint that picture. The below chart of the euro over the past five years shows that the single currency fell during the initial stages of the Fed’s panic rate hikes in 2022 then rallied back sharply as they continued. Meanwhile, during the latter half of 2024, the dollar rallied as the Fed cut rates and then declined as they remained on hold. My point is, the recent history is ambiguous at best regarding the dollar’s response to a given Fed move.

Source: tradingeconomics.com

I have maintained that if the Fed cuts aggressively, it will undermine the dollar. However, nothing about yesterday’s FOMC meeting tells me they are about to embark on an aggressive rate cutting binge.

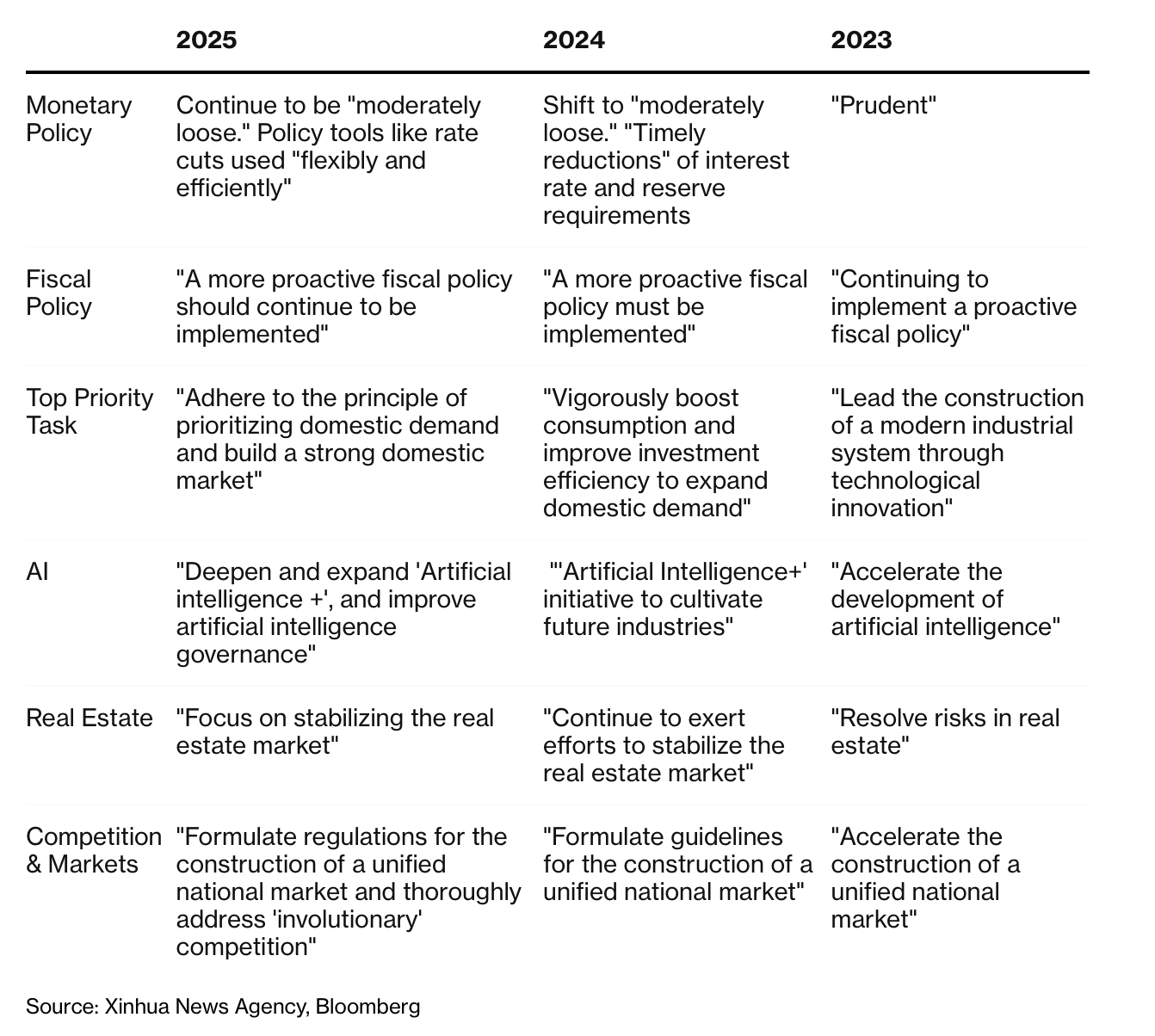

The other noteworthy story this morning is the outcome from China’s Central Economic Work Conference (CEWC). I have described several times that the President Xi’s government claims they are keen to help support domestic consumption and the housing market despite neither of those things having occurred during the past several years. Well, Bloomberg was nice enough to create a table highlighting the CEWC’s statements this year and compare them to the past two years. I have attached it below.

In a testament to the fact that bureaucrats speak the same language, no matter their native tongue, a look at the changes in Fiscal Policy or Top Priority Task, or even Real Estate shows that nothing has changed but the order of the words. The very fact that they need to keep repeating themselves can readily be explained by the fact that the previous year’s efforts failed. Why will this time be different?

Ok, a quick tour of markets. Apparently, Asia was not enamored of the FOMC outcome with Tokyo (-0.9%) and China (-0.9%) both sliding although HK managed to stay put. Elsewhere in the region, both Korea (-0.6%) and Taiwan (-1.3%) were also under pressure as most markets here were in the red. The exceptions were India, Malaysia and the Philippines, all of which managed gains of 0.5% or so.

In Europe, things are a little brighter with modest gains the order of the day led by Spain (+0.5%) and France (+0.4%) although both Germany and the UK are barely higher at this hour. There was no data released in Europe this morning although the SNB did meet and leave rates on hold at 0.0% as universally expected. There has been a little bit of ECB speak, with several members highlighting that ECB policy is independent of Fed policy but that if Fed cuts force the dollar lower, they may feel the need to respond as a higher euro would reduce inflation. Alas for the stock market bulls in the US, futures this morning are pointing lower led by the NASDAQ (-0.7%) although that is on the back of weaker than expected Oracle earnings results last night. Perhaps promising to spend $5 trillion on AI is beginning to be seen as unrealistic, although I doubt that is the case 🤔.

Turning to the bond market, Treasury yields have slipped -2bps overnight after falling -5bps yesterday. Similar price action has been seen elsewhere with European sovereign yields slipping slightly and even JGB yields down -2bps overnight. Personally, I am a bit confused by this as I have been assured that the Fed cutting rates in this economy would result in a steeper yield curve with long-dated rates rising even though the front end falls. Perhaps I am reading the data wrong.

In the commodity markets, the one truth is that there are no sellers in the silver market. It is higher by another 0.5% this morning and above $62/oz as whatever games had been played in the past to cap its price seem to have fallen apart. Physical demand for the stuff outstrips new supply by about 120 million oz /year, and new mines are scarce on the ground. This feels like there is further room to run.

Source: tradingeconomics.com

As to the rest of the space, gold (-0.2%) which had a nice day yesterday is consolidating, as is copper. Turning to oil (-1.1%) it continues to drift lower, dragging gasoline along for the ride, something that must make the president quite happy. You know my views here.

As to the dollar writ large, while it sold off a bit yesterday, as you can see from the below DXY (-0.3%) chart, it is hardly making new ground, rather it is back to the middle of its 6-month range.

Source: tradingeconomics.com

This morning more currencies are a bit stronger but in the G10, CHF (+0.45%) is the leader with everything else far less impactful. And on the flip side, INR (-0.7%) has traded to yet another historic low (USD high) as the new RBI governor has decided not to waste too much money on intervention. Oh yeah, JPY (+0.2%) has gotten some tongues wagging as now that the Fed cut and the BOJ is ostensibly getting set to hike, there is more concern about the unwind of the carry trade. My view is, don’t worry unless the BOJ hikes 50bps and promises a lot more on the way. After all, if the Fed has finished cutting, something that cannot be ruled out, this entire thesis will be destroyed.

On the data front, Initial (exp 220K) and Continuing (1950K) Claims are coming as well as the Trade Balance (-$63.3B). There are no Fed speakers on the docket, but I imagine we will hear from some anyway, as they cannot seem to shut up.

It would not surprise me to see the dollar head toward the bottom of this trading range, but I think we need a much stronger catalyst than uncertainty from the Fed to break the range.

There once was a Fed Chair named Jay Who fought ‘gainst the prez every day He tried to explain That tariffs brought pain So higher rates needed to stay

But data turned out to expose The job market, which had no clothes So, he and his friends Were forced, in the end To cut ere recession arose

The Fed cut 25bps yesterday, as widely expected (although I went out on a limb and called for 50bps) and markets, after all was said and done by Chair Powell, saw equities mixed with the DJIA rising 0.6% while the S&P 500 and NASDAQ both slipped slightly. Treasury yields rose 5bps which felt much more like some profit taking after a month-long rally, than the beginning of a new trend as per the chart below.

Source: tradingeconomics.com

Gold rallied instantaneously on the cut news, trading above $3700/oz, but slipped back nearly 2% as Powell started speaking and the dollar fell sharply on the news but rebounded to close higher on the day as per the below chart from tradingeconomics.com. See if you can determine when the statement was released and when Powell started to speak.

Did we learn very much from this meeting? I think we learned two things, one which is a positive and one which is not. On the positive side, there is clearly a very robust discussion ongoing at the Fed with respect to how FOMC members see the future evolving. This was made clear in the dot plot as even the rest of 2025 sees a major split in expected outcomes. But more importantly, looking into the future, there is certainly no groupthink ongoing, which is a wonderful thing. Simply look at the dispersion of the dots for each year.

Source: federalreserve.gov

The negative, though, is that Chairman Powell is very keen to spin a narrative that seems at odds with the data that they released in the SEP. In other words, the flip side of the idea that there is a robust discussion is that nobody there has a clue about what is happening in the economy, or at least Powell is not willing to admit to their forecasts, and that is a problem given their role in policy making.

It was a little surprising that only newly seated Governor Miran voted for 50bps with last meeting’s dissenters happy to go with 25bps. But I have a feeling that the commentary going forward, which starts on Monday of next week, is going to offer a variety of stories. If guidance from Fed speakers contradicts one another, exactly where is it guiding us? (Please know I have always thought that forward guidance was one of the worst policy implementations in the Fed’s history.)

Moving on, the other central banks that have announced have done exactly as expected with both Canada and Norway cutting 25bps. Shortly, the BOE will announce their decision with market expectations for a 7-2 vote to leave rates on hold, especially after yesterday’s 3.8% CPI reading. Then, all eyes will turn to Tokyo tonight where the BOJ seems highly likely to leave rates on hold there as well.

If you think about it, it is remarkable that equity markets around the world continue to rally broadly at a time when central banks around the world are cutting rates because they are concerned that economic activity is slowing and they seek to prevent a recession. Something about that sequence seems out of sorts, but then, I freely admit that markets move for many reasons that seem beyond logic.

Ok, having reviewed the immediate market response to the Fed, let’s see how things are shaping up this morning. Asian equity markets had both winners (Tokyo +1.15%, Korea +1.4%, Taiwan +1.3%, India +0.4%) and laggards, (China -1.2%, HK 1.4%, Australia -0.8%, Malaysia -0.8%) with the rest of the region seeing more laggards than gainers. The China/HK story seems to be profit taking related while the gainers all alleged that the prospect of another 50bps of cuts from the Fed this year is bullish. Meanwhile, in Europe, while the UK (+0.2%) is biding its time ahead of the BOE announcement, there has been real strength in Germany (+1.2%), France (+1.15%) and Italy (+0.85%) while Spain (+0.25%) is only modestly firmer. While there was no data of note released, we did hear from ECB VP de Guindos who said the ECB may not be done cutting rates. Clearly that got some investors excited. As to US futures, at this hour (6:55), they are solidly higher, on the order of 0.8% or more.

In the bond market, Treasury yields are backing off the highs seen yesterday and have slipped -4bps, hovering just above 4.0% on the 10-year. European sovereign yields are essentially unchanged this morning as were JGB yields overnight. It seems investors were completely prepared for the central bank actions and had it all priced in. I guess the real question is are those investors prepared for the fact that the Fed is no longer that concerned about inflation and will allow it to rise further? My guess there is they are not, but then, that’s where QE/YCC comes into play.

In the commodity markets, oil (-0.25%) is slightly lower this morning despite Ukraine attacking two more Russian refineries last night. What makes that particularly interesting is that the EIA inventory data showed a massive net draw of oil and products last week of more than 11 million barrels, seemingly a bullish signal. But hey, I’m an FX guy so maybe supply and demand in oil markets works differently! In metals, gold (+0.2%) and silver (+0.4%) continue to rebound from their short-term lows from yesterday. It is abundantly clear that there is growing demand for alternatives to fiat currencies.

Speaking of which, in the fiat world, rumors of the dollar’s demise remain greatly exaggerated. After yesterday afternoon’s gyrations discussed above, it is largely unchanged this morning with some outlier moves in smaller currencies, NZD (-0.5%), ZAR (+0.3%), KRW (-0.3%) while amongst the true majors, only JPY (-0.25%) has moved any distance at all.

***BOE Leaves rates on hold, as expected, with 7-2 vote, as expected.***

Turning to this morning’s data, we see the weekly Initial (exp 240K) and Continuing (1950K) Claims as well as Philly Fed (2.3), then at 10:00 we get Leading Indicators (-0.2%). Something I read was that last week’s Initial Claims number of 263K was caused by a data glitch in Texas, implying it was overstated. I imagine we will find out more on that this morning.

Recapping all we learned yesterday and overnight, the Fed seems reasonably likely to cut at both of their last two meetings this year, but expect only one cut in 2026, which is at least 50bps less of cuts than had been expected prior to the meeting. Meanwhile, equity markets don’t seem to care and continue to rally while bond investors remain under a spell, believing the Fed will fight inflation effectively. Gold is under no such spell, and the dollar is the outlet for all of it, toing and froing on the back of various theories of the day. If forced to guess, I do believe there is a bit more weakness in the dollar in the near-term, but do not look for a collapse. In fact, I suspect that as investment flows into the US pick up, we will see a reversal of note by the middle of next year.

The US has not yet been drawn To war, though it’s not yet foregone That won’t be the case While Persians now brace For busters of bunkers at dawn

But until such time as we learn That outcome, the current concern Is Jay and the Fed And what will be said At two o’clock when they adjourn

So, every top headline this morning discusses the idea that President Trump is considering whether to initiate US military action in Iran, specifically to drop the so-called bunker buster bombs to destroy Iran’s nuclear enrichment and bomb-making facilities. There is certainly a lively discussion on both sides of the argument with the best description of the problem that I’ve seen being a poll showing that 74% approve Trump’s position that Iran must not get nuclear weapons, but 60% oppose US involvement in the war. I’m glad I don’t have to thread that needle!

Obviously, there are market implications if the US does get involved but given the complete lack of clarity on the situation at this point, I do not believe I can add much to the discussion. The only thing I will say is that the longer-term trends for both oil (lower) and metals (higher) are still intact, but we are likely to see some significant volatility along the way.

Which takes us to the next most important market discussion, the FOMC meeting that ends today and the potential market impacts. It is universally assumed that there will be no policy change at the meeting, either interest rates or QT, which means that now the punditry is focused on the arcana of Fed policy. As this is a quarter end meeting, the Fed will release its latest SEP (summary of economic projections) and dot plot, and with nothing else to discuss until the war in Iran either ends or intensifies, those are the key discussion points in the market.

I have long maintained that one of the greatest blunders of the Bernanke era was the institution of forward guidance. While it may have served its purpose initially, it has now become a major distraction. Far too much attention is paid to the dot plot, where if one member adjusts their view by 25bps, it can impact markets which have built algorithms to respond to the median outcome.

Below is the March dot plot which showed a median “expectation” of Fed funds for the end of 2025 at 3.875%, or 50 basis points lower than the current level. However, if two more FOMC members (out of 17) thought there was only going to be one cut, that would have shifted the median “expectation” as well as the narrative.

As such, the importance of the dot plot feels overstated compared to its actual value. After all, no FOMC member has an impressive track record with respect to their analysis of the economy and its future outcomes, let alone what the appropriate rate structure should be at any given time. In fact, nobody has that, which is the argument for restricting the Fed’s duties to be lender of last resort and allow markets to determine the proper level of interest rates based on the supply and demand of money. But this is the world in which we live. My one observation is that the post GFC era has greatly distorted views on the economy and appropriate monetary policy. It is hard not to look at the below history of Fed funds and see the anomaly that occurred during the initial QE phase.

Concluding, regardless of my, or anyone not on the FOMC’s, views on appropriate policy, it doesn’t matter one whit. They are going to do what they deem appropriate, and while I don’t doubt their sincerity, I do doubt they have the tools for the mission. Perhaps the most interesting thing that could come from this meeting is further information on their assessment of the current Fed process, including their communication policy. I remain strongly in favor of them all shutting up and letting markets do their job although that seems unlikely. But perhaps they will get rid of the dots which seem to have outlived any value they may have had initially.

Before we go to markets, I have to highlight one other market discussion this morning with Bloomberg publishing two different articles, here and here, on the end of the dollar’s hegemony. The first highlights a speech by PBOC governor Pan Gongsheng and his vision of a multicurrency world which, of course, includes the renminbi as a major part of the process. I will believe that is a possibility as soon as China opens its capital accounts completely and allows flows into and out of the country with no restrictions. (I’m not holding my breath.) The second takes the Michael Bloomberg Trump hatred in the direction of the president is destroying the dollar’s reign because of his policies and to highlight the dollar has fallen 10% already this year! But let us look at a long-term chart of the dollar, using the DXY as a proxy, and you tell me if you can see the recent move as being outsized in any sense of the word. In fact, the dollar’s recent price action is indistinguishable from anywhere in its history, and it is not anywhere near to its historic lows. In fact, it is just a few percent below its long-term average.

Ok, now let’s look at markets. Yesterday’s selloff in equities seemed to be based on concerns over the escalation in Iran, but as that drags out, traders don’t know what to do. They are certainly not pushing things much further. In fact, overnight saw the Nikkei (+0.9%) have a solid gain although HK (-1.1%) followed the US lower. Elsewhere in the region, South Korea and Taiwan performed well, while India and Indonesia lagged and the rest were +/-20bps or less. Europe, though, is softer this morning with declines on the order of -0.4% on the continent across the board. I think investors here are also waiting on the potential events in Iran. But US futures are actually pointing slightly higher at this hour (7:30).

In the bond market, yields around the world are slipping with Treasuries falling -2bps and most of Europe seeing declines between -1bp and -3bps. This is after a few basis point decline yesterday as well. I guess the fear of too much US debt is in abeyance this morning.

In commodity markets, oil, which rallied sharply yesterday on fears of the US entering the war, is little changed on the day after that climb as while there has been lots of talk, oil continues to flow through the Strait of Hormuz, and everybody is pumping nonstop to take advantage of the current relatively high prices. Gold is unchanged although the other metals (Ag +0.25%, Cu +0.7%, Pt +2.4%) continue to see significant support. In fact, platinum this morning has broken above the top of an 11-year range and many now see an opportunity for a significant rally from here.

Finally, the dollar is somewhat softer this morning, slipping about 0.2% against the pound, euro and yen, with similar declines against most other currencies. The exceptions to this are the KRW (+0.45%) which seems to be benefitting from a growing hope that a trade deal will be completed between the US and Korea shortly, and ZAR (-0.5%) as CPI data release there this morning shows inflation under control and no reason for SARB to consider tightening policy further.

On the data front, because of tomorrow’s Juneteenth holiday, we see Initial (exp 245K) and Continuing (1940K) Claims as well as Housing Starts (1.36M) and Building Permits (1.43M). And of course, at 2:00 it’s the Fed. My sense is absent a US escalation in Iran, it will be quiet until the Fed, and probably thereafter as well given the lack of reason for any policy changes. After all, there is no certainty as to either war or trade policy right now, so why would they do anything.

If I had to opine, I would say the dollar is likely to decline over the next year, but that in the longer run, it will be firmer than today.

The answer to yesterday’s question Is CPI’s seem some regression Both stocks and bonds soared The dollar was floored But Powell now has indigestion

To no one’s surprise he left rates Unchanged, while the dot plot translates To higher for longer Though pressure’s grown stronger To cut to achieve his mandates

Unequivocally, the CPI data was cooler than market forecasts. Month over month prices were unchanged at the headline level and grew only 0.16% on a core basis, with the year-on-year numbers each coming in one tick below expectations. It took absolutely no time for markets to run with this data as the following charts from tradingeconomics.com for the NASDAQ 100, 10-year Treasury yields and EURUSD demonstrate. See if you can determine when the CPI data was released.

Now, as I explained, and has become abundantly clear to anyone watching, the equity market is in a world of its own. While yields backed up and the dollar rebounded (euro fell) after the somewhat more hawkish than expected FOMC statement, dot plot and Powell press conference, the NASDAQ ignored everything and kept on rallying. While that is remarkably impressive, I remain of the opinion that trees still don’t grow to the sky, although apparently, they can get really tall!

At any rate, a quick look under the hood at the CPI shows that core goods prices continue to fall, which was largely why today’s data looked so good, but primary rents and OER continue to climb at about 0.4% monthly despite many assurances by many pundits, analysts and economists that rental inflation was sure to begin declining soon. It has been rising at this pace or faster for more than two years, and while the actual pace has backed off from the rate a year ago, if you annualize 0.4% you come up with just under 5.0% inflation. It remains hard to believe that shelter costs can rise at that pace and the general price level is going to get back to 2.0%. Yesterday’s data was good, but we are not out of the woods yet.

Turning to the FOMC, the statement was virtually unchanged from the May statement, which makes sense since the mix of data that we have seen in the interim shows some hot and some cold numbers and no clear line of sight to the end game. As such, it is not surprising that Chairman Powell tried to veer hawkish at the press conference in what appears to have been an attempt to offset the (over)reaction to the CPI data. In fact, a look at the dot plot shows that, as I suggested, the median expectation for rate moves in 2024 is down to a single cut, although they are more confident that inflation will continue to fall next year with the median expectation for an additional 4 cuts. However, as I also suggested, the longer-term outlook continues to rise with the median there now up to 2.80% from 2.60% in March, and 2.5% or below for the 3 years prior to that.

Interestingly, in their Summary of Economic Projections they expect PCE inflation to be 2.6% this year, up from 2.4% in March, with core PCE to be at 2.8% this year, up from 2.6% in March. They did, however, maintain their views of GDP growth (2.1%) and Unemployment (4.0%). At least, unlike Madame Lagarde who cut rates despite raising inflation forecasts, the Fed’s inaction made far more sense.

But pressure is building on Powell and the Fed to cut rates. Today, several senators wrote (and released) a letter to Powell exhorting him to cut rates because everybody else is doing it. They claim that his intransigence is hurting the economy, although the whole point of higher for longer is that there is scant evidence that the economy, as a whole, is in trouble despite rates where they are, although certainly some sectors are feeling a pinch. As an aside, given the extreme degree of financial and economic ignorance that is routinely demonstrated by virtually every member of the House and Senate, this letter is simply political grandstanding. But pressure is pressure, and Powell will certainly feel it, although I don’t think he is too concerned by this group overall.

While this morning brings PPI (exp 0.1%/2.5% headline and 0.3%/2.4% Core) as well as the weekly Initial (225K) and Continuing (1800K) Claims data, it is hard to believe that either of those data points are going to have any substantive impact given everything we learned yesterday. So, let’s look elsewhere to see what is happening.

One of the interesting stories right now is the ongoing situation in France with the snap elections called by President Macron. Apparently, the quick timing has resulted in significant confusion on both the left and right of the spectrum as to who will be allying with whom, and what they stand for. While this is amusing in its own right (see this Twitter thread), the ramifications are greater for the impact on the French OAT market and the euro.

Briefly, the issue is that France has been slowly sliding from the figurative north of Europe to the South, meaning that it used to be considered a country with almost Germanic fiscal sensibilities and now it is much more akin to the PIGS than Germany. The WSJ had an interesting article this morning describing the situation. Ultimately, the market response has been for French yields to rise compared to German yields, adding pressure to the country as it needs to continue to finance its 5%+ budget deficit. Now add to that the absolute trainwreck that is the current government leadership (as evidenced by that Twitter thread) and investors have decided that there are better places to invest with less credit risk. After all, S&P Global downgraded French debt last month due to their profligate spending and I assure you, whatever the election outcome, there will be more spending not less.

If we view this through a FX lens, the combination of clear dysfunction in Europe, lower interest rates in Europe and a Fed still committed to seeing the whites of 2%’s eyes before cutting rates here, it is very easy to anticipate the euro will be biased downwards over time. While I know there are many who continue to write the dollar’s obituary, the fact remains that it is still standing with no competitors of note. In fact, part of the raison d’etre of the euro was to be able to replace the dollar as a reserve currency. It seems that hasn’t worked out all that well.

Ok, let’s see how global markets responded to the US data yesterday. Perhaps the most interesting thing was that even in the US, the DJIA fell slightly, despite the conviction that rates are heading lower. In Asia, the picture was mixed with Japan (-0.4%) and China (-0.5%) sliding while Hong Kong (+1.0%) rallied on the tech rally. Many consider the Hang Seng to be China’s NASDAQ with respect to the weight of tech companies in the index. As to European bourses, they are all in the red this morning by more than -1.0% with France (-1.4%) leading the way lower. Of course, based on the above discussion, that can be no surprise. Lastly, in the US, futures at this hour (6:45) are mixed with NASDAQ higher by 0.6% while DJIA futures are -0.4%. Apparently, the prospect of lower rates doesn’t help more mature companies.

In the bond market, after yesterday’s wild ride (see above chart), Treasury yields have edged lower by -1bp, but in Europe, yields are continuing higher from their closing levels, catching up to the Treasury yield rebound in the wake of the FOMC meeting. Not surprisingly, French OATs are leading the way with yields higher by 4bps while Germany has seen only a 2bp rise.

This morning, commodities are uniformly under pressure with oil (-0.8%) sliding after a solid weekly performance while metals markets are also slipping (Au -0.1%, Ag -0.8%, Cu -0.6%) as traders try to come to grips with the next interest rate moves and adjust their positions. An interesting story this morning is that a shipment of copper from Russia to China for 2000 tons apparently never arrived in China. This is simply the latest quirk in the metals markets where confirmation of what is being traded is limited. You may recall the story last year about nickel inventories at the LME actually being bags of painted rocks. In this space, the broad trend remains that there is excess demand for metals, especially copper, silver and aluminum, as all three are critical to electrification of systems and grids, but it is going to be a bumpy ride higher!

Finally, the dollar, which was decimated in the immediate wake of the CPI data yesterday, managed to claw back some of those losses in the afternoon thanks to the more hawkish Fed and this morning, that slow rebound continues with the greenback higher vs. almost all its counterparts in both the G10 and EMG blocs. However, nothing really stands out as having moved significantly, with a general trend of about 0.2% or so across the board.

And that is really all we have today. The first post-FOMC speaker is NY Fed president Williams at noon, although I suspect his message will be identical to Powell’s yesterday. As to the rest of things, the BOJ meets tonight and while there is no expectation of a policy change, Ueda-san’s comments will be carefully parsed for any clues to when a change may be coming.

Since nothing seems to matter to the NASDAQ and everyone wants to own it, I suspect that the dollar will maintain its gradual strength until further notice.

Well, Jay and the Fed cooed like doves And treated the bulls with kid gloves But under the hood Was it quite so good? It’s clear number up’s what he loves!

The upshot is stocks really soared As everyone’s sure Jay’s on board To cut first in June And thrice when Cold Moon Is seen, near the birth of our Lord

Whatever the pundits thought about the hottish inflation readings in January and February, they clearly did not read the room properly, at least not the room in the Eccles Building. Despite raising their 2024 forecasts for GDP growth (2.1% from 1.4%) and Core PCE (2.6% from 2.4%), as well as maintaining their forecast for the Unemployment Rate to remain quiescent (4.0% to 4.1%), they are hell-bent on cutting rates this year, with June still the most likely starting point. I created a little table to show, however, that perhaps the consensus is not quite what the headlines would have you believe.

Dec

Mar

Median

Avg

Median

Avg

2024

4.625

4.704

4.625

4.809

2025

3.625

3.612

3.875

3.783

2026

2.875

2.947

3.125

3.066

Longer Term

2.500

2.586

2.625

2.813

Source: Data FRB, calculations @fx_poet

The highlighted points show that while the median for 2024 remained the same, the average was nearly a full cut less. In fact, if one more member had adjusted their forecast higher, the median would have come out for just 2 cuts this year. But as I wrote yesterday, perhaps of more importance is the Longer Term view, where not only did the median rise by 12.5bps, but the average is substantially higher, a full 25bps higher than the December views.

However, the market has ignored this wonkish number crunching and accepted the numbers at face value; three cuts this year and three more next year helping drive equity prices to yet another set of new all-time highs.

Regarding the tapering of the balance sheet, Powell explained at the press conference that they had, indeed, discussed the topic as they were trying to determine the best way to continue the process without any untoward events, but that is not the issue. The issue is…BUY STONKS!!!

I would estimate that Chairman Powell is pretty happy with the outcome and am certain that Secretary Yellen is very happy with the outcome. After all, the equity rally continued while bond yields managed to drift lower by a couple of basis points. But the really happy campers are the holders of gold which rallied more than 1% and traded above $2200/oz for the first time ever. The market has reviewed this outcome and decided that the biggest risk going forward is a further devaluation of the dollar vs. stuff, although vs. other fiat currencies it is likely to hold its own. In other words, inflation ain’t dead. I expect the bond market to determine this is the case over the next several weeks and see yields rising further, especially if the PCE data next week is hot again.

While Jay may have had the most press In Switzerland, Tom did aggress He cut twenty-five In order to drive Their growth with a bit more largesse

This morning, we have seen three more G10 central banks and the only surprise comes from Switzerland, where soon-to-retire President, Thomas Jordan, cut their base rate by 25bps to 1.50%. While there were several analysts who had suggested this might be the case (including this poet on Monday), the bulk of the market was in the no change camp. However, cut they did, and the result was an immediate 1.1% decline in the Swiss franc, arguably a key part of their goal. In the statement, they explained that inflation had been well within their target range, and they would have the tool of further currency intervention if they felt the franc was weakening too much.

One theory on the surprise cut is that the SNB wanted to get ahead of the pack as they only meet 4 times each year and their next meeting is after the June Fed and ECB meetings. As well, many pundits are now saying this is the “proof” that the Fed and ECB are going to cut in June. My take is that while I agree the ECB is a done deal come June, I think the Fed may have a tougher time as there is still no evidence that inflation is heading back to their 2% target. We have two more CPI and PCE reports before the June meeting, and if the recent price activity continues (and given energy prices remain buoyant I expect they will), it will be very difficult for Chair Powell to explain the need to cut rates unless Unemployment is surging. Perhaps that will be the case, but right now, the data does not indicate things are collapsing. The next three months should be quite interesting.

Ok, let’s see how other markets have responded to Powell and the SNB surprise. Equity markets are in a happy place right now after records fell in the US yesterday. The Nikkei (+2.0%) also set a new record and the Hang Seng (+1.9%) continued its recent rebound. In fact, only mainland Chinese stocks couldn’t muster a rally last night, with every other nation in APAC in the green, often by more than 1%. In Europe, though, the picture is a bit more mixed with more gainers than losers, but still several nations seeing modest pressure on their equity indices. It should be no surprise that Swiss stock markets are higher, but France and Denmark are suffering somewhat today. The best performer is the UK (+0.9%) which seems to be benefitting from a solid uptick in its Flash Manufacturing PMI (49.9, exp 47.8). Lastly, in what should not be a surprise at all, US futures are pointing higher across the board.

In the bond market, all is right with the world this morning as there are bids everywhere with yields declining correspondingly. Treasury yields slipped another 4bps overnight and throughout Europe, we are seeing declines between 3bps and 5bps with Swiss bonds lower by 7bps. In fact, Asia is where things were modestly different as JGB’s remain unchanged (tighter policy remains an idea not a reality yet) and Australian yields rose after much stronger than expected employment data was released last night.

In the commodity space, oil (-0.25%) is a touch softer after a decline of more than 1% during yesterday’s session. With all the focus on the Fed, there was not a lot of news driving things here specifically. But the real winner in the commodity space is gold (+1.0%) as the market appears to be calling BS on the Fed’s inflation and QT forecasts. The thing to remember about gold is it is not so much a good hedge for consumer inflation, but it is a very good hedge for monetary inflation (i.e. the excess printing of money). While those two inflations tend to be correlated, they are not tick for tick, so gold seems to be amiss at times. But the very idea that despite ongoing inflationary pressures, and the continued supplying of liquidity by the global central banking cast, is the right time to cut interest rates is a step too far for gold markets. I believe this has room to run higher. As well, copper (+0.7%) is also rebounding, and I expect that we will see most commodities continue to perform well going forward in this environment.

Finally, the dollar is under some pressure this morning, adding to yesterday’s declines in the wake of the Fed meeting. Recall, the dollar had rallied the first half of the week as the punditry was looking for the Fed to seem more hawkish. But that was not to be and this morning it is broadly, though not universally lower. AUD (+0.3%) and JPY (+0.2%) are the biggest gainers in the G10 while CHF (-0.65%) is the laggard after the rate cut, although has rebounded from its worst levels. In the EMG space, PHP (+0.4%), MYR (+0.5%) and IDR (+0.4%) are the leading gainers although we are seeing weakness in EEMEA with ZAR (-0.3%) and CZK (-0.3%) lagging.

On the data front, as it is Thursday, we see Initial (exp 215K) and Continuing (1815K) Claims as well as the Current Account deficit (-$209B) and Philly Fed (-2.3) all at 8:30. Then as the morning progresses, we see the Flash PMI data (51.7 Manufacturing, 52.0 Services), Existing Home Sales (3.94M) and Leading Indicators (-0.2%). As well, we get our first Fed speaker post the meeting, vice-chairman for regulation Michael Barr, this afternoon, but given my assessment that the Fed is happy with the market response, I don’t imagine he will say anything new.

Overall, the bulls and doves are walking hand in hand (what a terrible metaphor, sorry) and that means that risk assets are likely to continue to perform well for now and the dollar seems likely to come under a bit more pressure. I maintain that the bond market is going to figure out the inflation story is not great and react, but that is not today’s story.

The Fed is the talk of the town

Are dots set to move up, or down?

At this point it seems

Those with dovish dreams

Will finish the day with a frown

The other discussion of note

Is balance sheet size and its bloat

Will QT soon end?

Or will it extend?

It seems this idea’s still inchoate

Yesterday I offered my view that the most important potential changes in today’s FOMC statement and releases was the Longer Run median interest rate estimate. Any change there will imply that the framework in which the Fed has been working is changing. And one thing we know about changes in frameworks is they bring volatility. But there is another issue I did not discuss yesterday, QT. Currently, the Fed is allowing up to $60 billion/month of Treasury securities to mature from their balance sheet without being replaced and up to $35 billion in mortgage-backed securities. This process has seen their balance sheet decline in size from a shade under $9 trillion in March 2022 to a shade over $7.5 trillion as of last week.

Doing the math, if the balance sheet had declined in size each month by their capped amounts, the current size would have been ~$6.7 trillion, so they have not kept up their desired pace. The reason is that their mortgage portfolio is not rolling off very quickly since mortgages are not being prepaid at anywhere near the previous rates. This is due to the impact of the Fed’s actions on the housing market. Mortgage-backed securities get prepaid when the mortgages underlying are paid off. That happens in one of two situations, either the house is sold or the homeowner refinances. With so many homeowners having refinanced when rates were much lower, they have no incentive to do so now, so that channel has been essentially closed. At the same time, given the dramatic slowdown in the sales of existing homes, that channel is moving at a much slower pace as well.

Prior to the quiet period, Governor Chris Waller gave a speech where he discussed the idea that he would like to see all the mortgages off the Fed’s balance sheet, and the balance sheet hold a far larger percentage of T-bills rather than the current construction of mostly longer-dated coupons. If this is the consensus view at the FOMC, that means they have a lot of work left to do. As well, many have questioned whether they can continue to shrink the balance sheet at the same time they are cutting interest rates. When any FOMC member has been asked that question, they maintain the two issues are separate. However, I would contend if they do operate in that manner, the results may not be what they want. It would be a classic pressing on the accelerator and the brake at the same time type of situation. Another framework change and the chance for more volatility.

It is not clear if the Fed will even discuss the end of QT in their statement although I suspect Powell will have to address the question in the press conference regardless. But as I look at today’s potential outcomes, the thing that jumps out at me is the chance for several of their decisions to lead to more volatile markets going forward. And that is across asset classes, so stocks, bonds and the dollar. It is for times like these that hedging policies are important. Properly constructed hedges can be very effective at reducing market driven volatility of results, whether corporate or trading profits.

Ok, let’s turn to the overnight session to see how things are shaping up heading into the meeting today. Equity markets in Asia were generally positive with the Nikkei (+0.65%) recapturing the 40K level. Chinese markets were ever so slightly firmer despite the fact that the PBOC left the Loan Prime Rate unchanged. There seemed to be a lot more hope for a change than evidence the PBOC would act. Europe, on the other hand is having a little more trouble this morning with most markets softer led by the CAC (-0.6%). The outlier here is the DAX (+0.2%) which seems to be responding to a larger than expected decline in German PPI to -4.1% Y/Y. The implication is German corporate margins may improve. As to the US, at this hour (7:15), futures are edging higher by about 0.1% across the board after another solid session yesterday.

In the bond market, Treasury yields have edged down 1bp in the 10yr with similar movement across the curve. In Europe, yields have fallen a bit more, between 3bps and 5bps with UK Gilts (-5bps) leading the way after CPI data this morning printed at a softer than expected 3.4% headline, 4.5% core. With the BOE on tap tomorrow, investors believe this improves the odds of a more dovish outcome, although no rate cuts are likely at all.

As to the continent, Madame Lagarde regaled us this morning with the following: “Our decisions will have to remain data dependent and meeting-by-meeting, responding to new information as it comes in. This implies that, even after the first rate cut, we cannot pre-commit to a particular rate path.” In other words, she continues to sing from the same hymnal that all the G10 central bankers are using. Once again, I don’t understand why anyone would believe that the central banks will be able to pivot on a timely basis if/when recession is coming. By maintaining their data dependence, they are assured that they will be reactive, not proactive, since all data is backward looking. And one more thing, JGB yields have been unchanged since the BOJ policy change. Tighter policy is not in the cards here either.

In the commodity market, everything is under a bit of pressure this morning with oil (-0.8%) slipping back a bit on what seems more like a trading response than a fundamental change in anything. EIA data later today can certainly have an impact if the recent drawdown in inventories continues because production does not appear to be increasing anywhere. In the metals markets, gold is a hair softer, although remains within spitting distance of its recently traded all-time highs while copper (-1.0%) has been slipping the past several sessions and is basically right back at $4.00/lb. This market remains beholden to the growth story overall, and China’s lack of activity last night is probably weighing on the red metal here.

Finally, the dollar is still kicking butt and taking names with the DXY back above 104 this morning. The yen has not found its footing yet, trading to 151.65, down another -0.5%, and really getting hammered on the crosses vs. the euro and the pound, at all-time lows there. But really, this remains a dollar strength story as hopes continue to recede for the Fed to start easing policy very soon. On a relative basis, the US economy continues to be the best performing major economy (7% budget deficits will do that for you), but the reality is reasons for the Fed to start cutting rates remain scarce. Until those change, the dollar should continue to perform well. And remember, when that does change, we are likely to see every G10 nation cutting rates aggressively, so the dollar should still hold up well.

And that is it. There is no data ahead of the Fed so I imagine we will all collectively hold our breath until the statement at 2:00 and Powell’s presser at 2:30. Until then, I foresee little in the way of movement. After that, it all depends on what he does and says.