The rate of inflation expanded

Though core came out more evenhanded

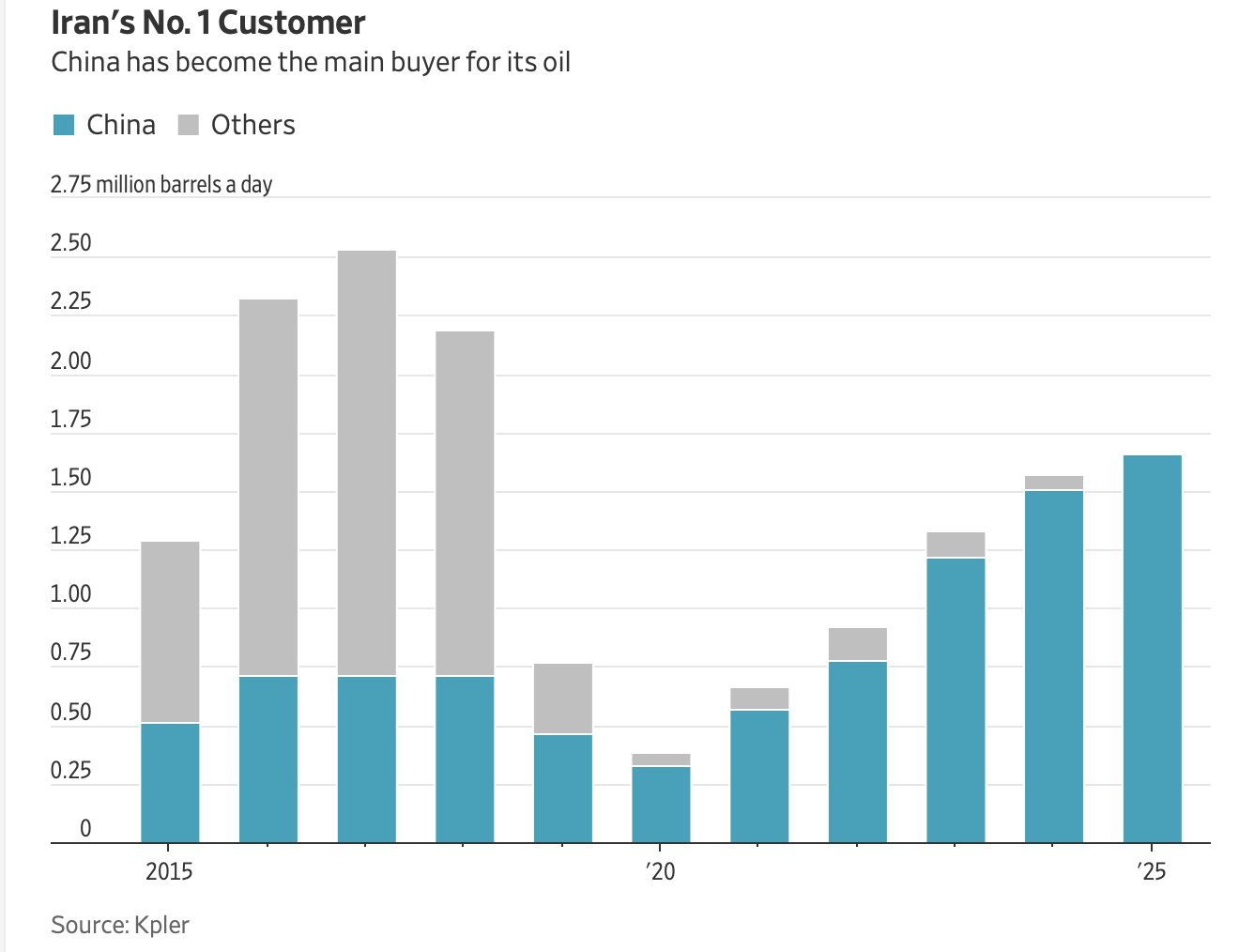

The war in Iran

Ain’t going to plan

But oil’s not over demanded

However, the story today

Is SpaceX shares soon on their way

To stock market listing

Though some are insisting

Its value is, frankly, outré

It’s a funny thing lately, there has been quite a bit of market activity, but the narrative storylines are changing so quickly that they don’t seem to have a real impact. So, every day there is some new thesis as to why prices are behaving in whatever manner they are. It is almost as if the market is trying on different stories to see which one fits best.

As I am wont to do, I always like to step back and take a longer-term view on things as regardless of the daily wiggles, my experience is that those very big picture issues are what drive markets over time. So, let’s review what I see as the key long-term drivers;

- FX – ultimately, the combination of monetary and fiscal policies is critical in this space with a good rule of thumb being tight monetary and loose fiscal policy strengthen a currency while the opposite settings tend to weaken them. When both policies are on the same setting, it is far less clear, although I would err on the side of monetary policy being the driver. Key to this is that monetary policy tends to drive short-term flows.

- Equities – earnings are still the ultimate issue here as, remember, shares represent ownership in a company (although the recent gamification of markets has certainly obscured that view). Too, equities tend to be forward-looking, anticipating how future earnings are going to evolve. The biggest change in this space has been the steady growth of passive investing, though, which represents more than 50% of the market now. Passive investing simply means that as money flows into funds, like 401K’s, the funds buy stocks with the S&P 500 the most popular destination regardless of earnings and prospects. So, flows are the other critical issue, just like in FX.

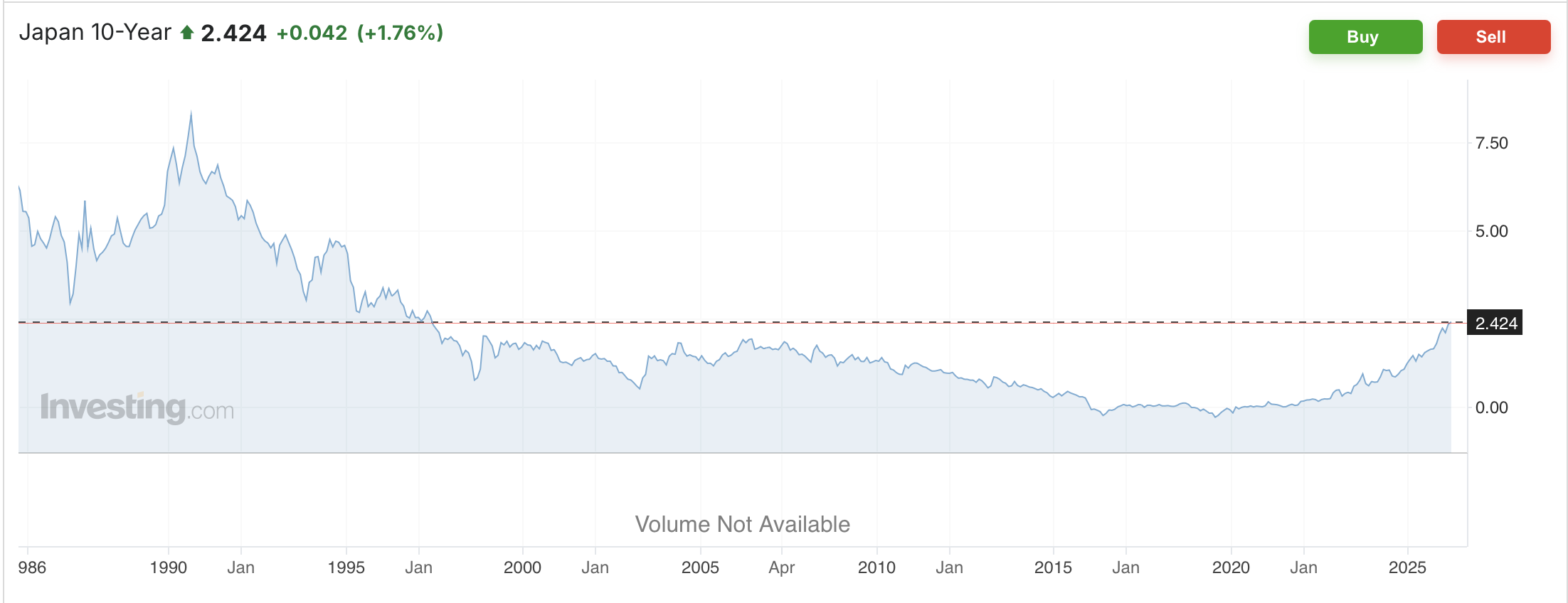

- Bonds – despite much recent angst, Treasuries remain a haven asset and benefit from that status. However, especially as you move out the maturity ladder, inflation expectations are the primary driver in an unencumbered market. While much hay has been made regarding the extraordinary size of the US outstanding debt, now approaching $40 trillion, I do not believe we have reached a point where anyone believes they will not get their money back, albeit money that has been devalued by inflation.

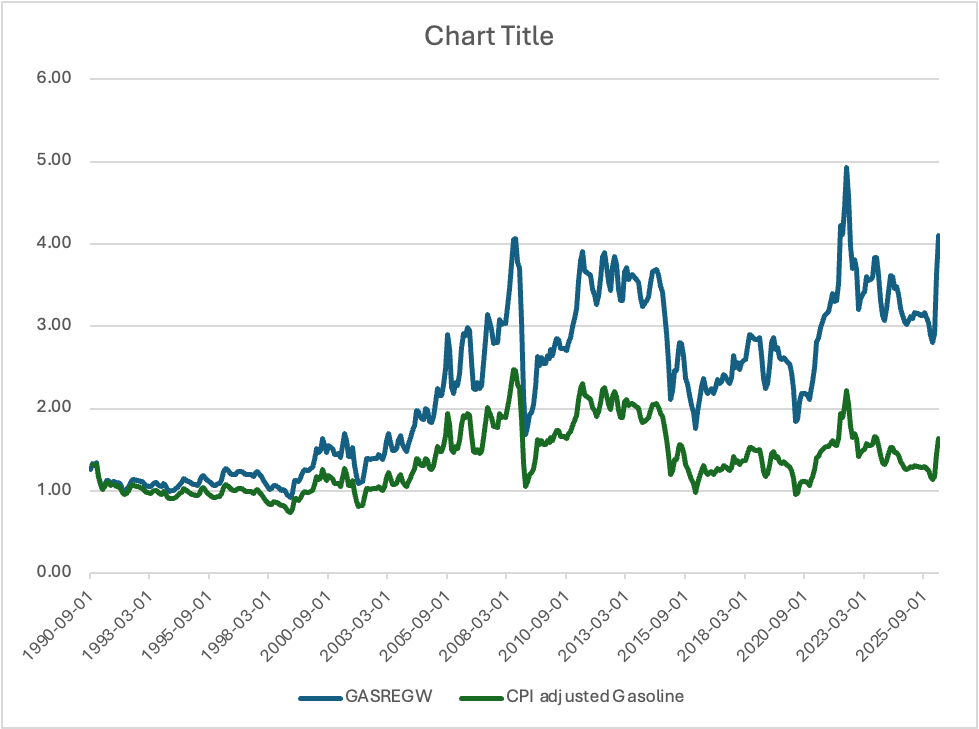

- Commodities – this is the space where supply and demand remain paramount, and really, it’s current supply and demand. As such, the fact that oil is back below $90/bbl this morning tells us that a combination of increased non-OPEC supply plus some measure of demand destruction has found a new equilibrium level. This remains far below the levels anticipated by many after the closure of the Strait of Hormuz, and there are still many analysts calling for a sharp move higher when all the mitigating factors that have prevented a much bigger move run out. This morning, Javier Blas at Bloomberg had an excellent piece describing his view of why oil prices aren’t higher despite the war.

Every narrative is an attempt to either describe or hide the longer-term issue, with much more hiding than describing in my experience. But I stand by these concepts.

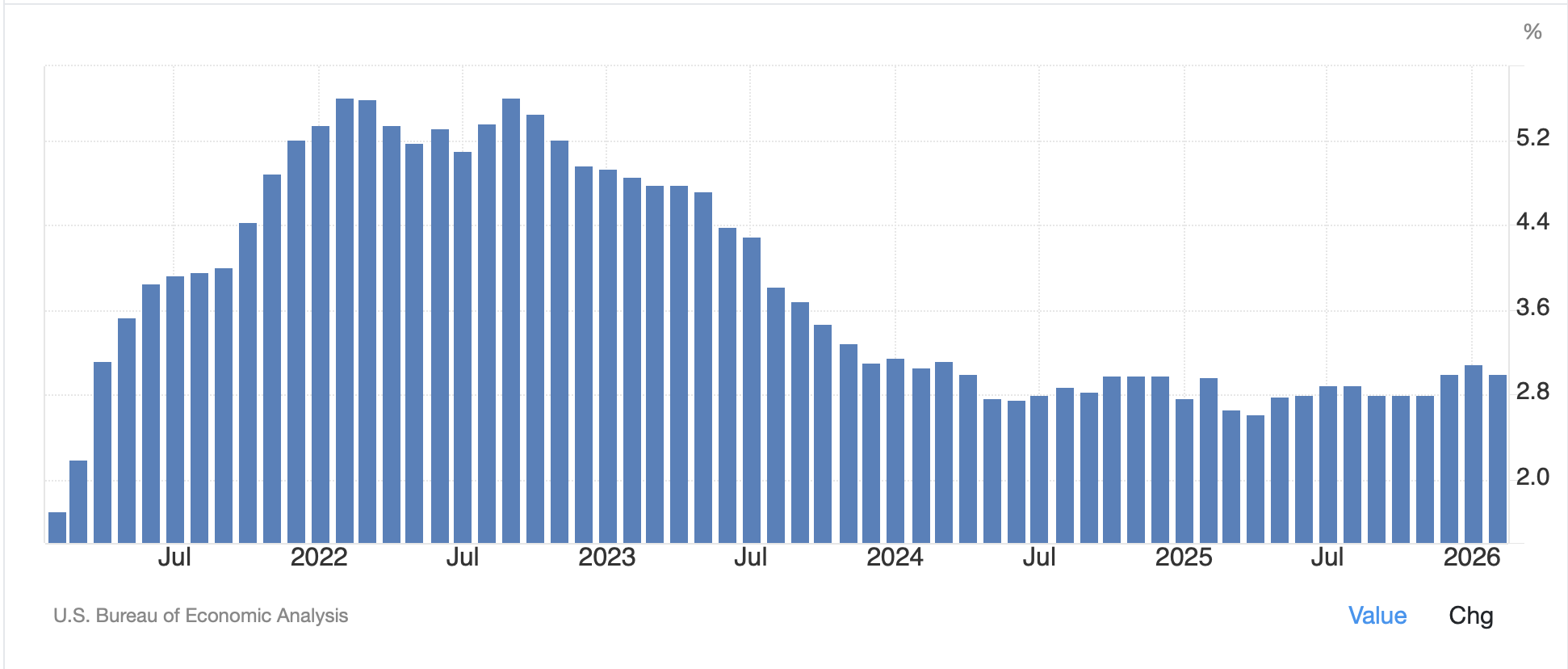

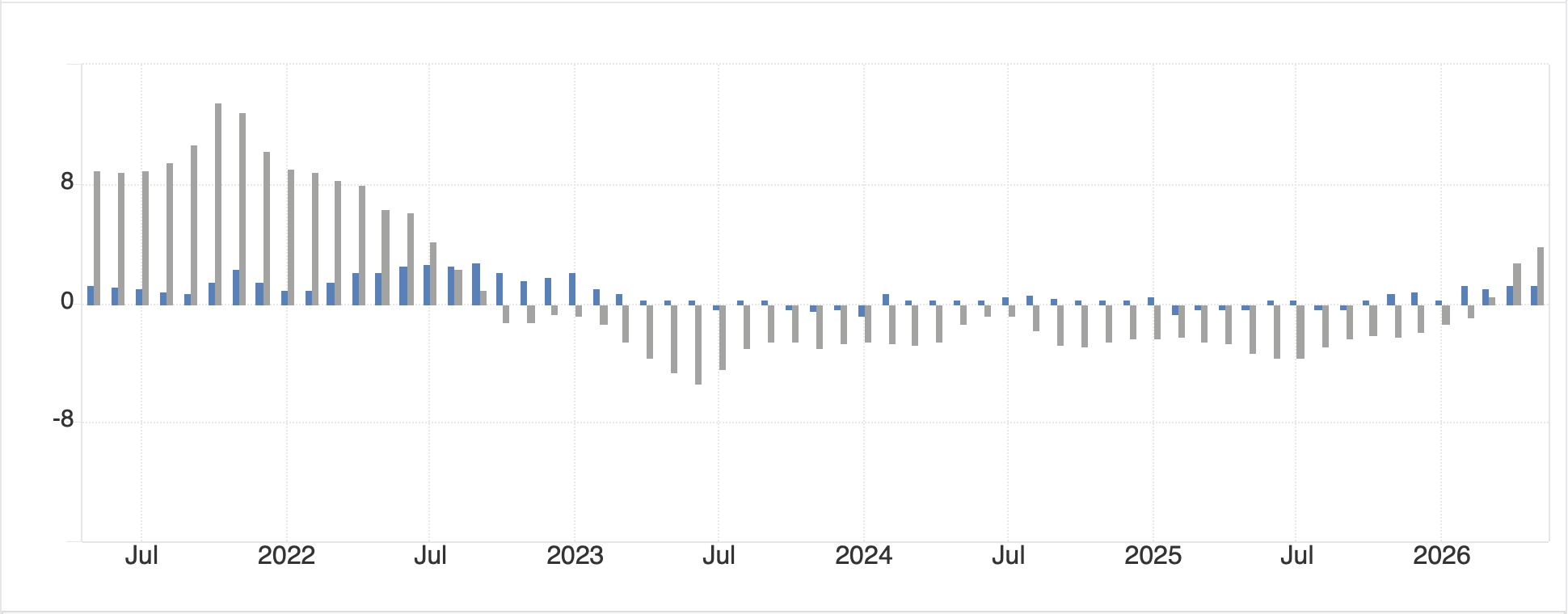

Which takes us to today’s narratives. CPI yesterday was largely as expected, actually the core number at 0.2% M/M came in a bit light, but that stopped mattering about 2 minutes after the release. Inflation has become a favorite subject about which to bitch, but very few do anything about it. (if you want to do something, go to www.usdicoin.com and you can buy some USDi which is a fully backed inflation tracking cryptocurrency).

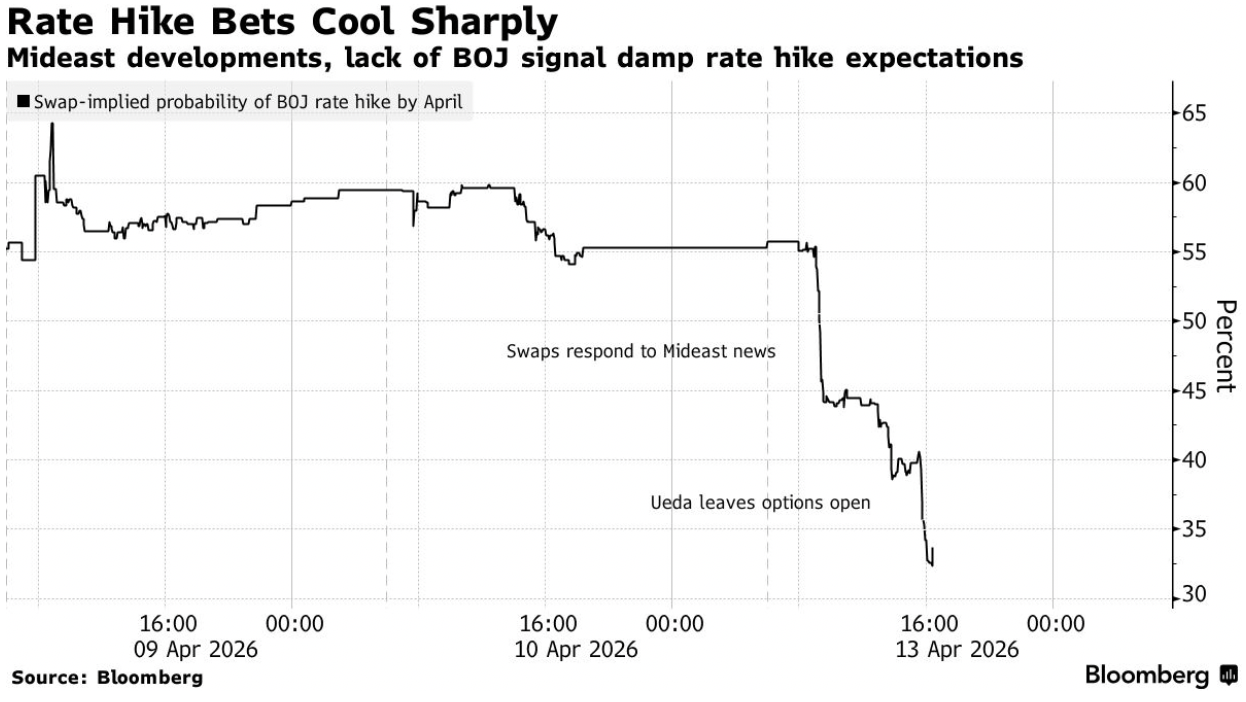

There was a short resumption of military activity in the Gulf after a US helicopter was shot down by Iran and the US retaliated. Frankly, I didn’t even read the details as they just don’t matter to the big picture. It is unclear whether negotiations are ongoing, but the stalemate continues.

And finally, the truly big story, the SpaceX IPO this evening. It is the one thing that has the most tongues wagging in the markets and if you read X, it appears there are many more analysts who believe the price is absurdly high than that it represents value. I have no opinion on the deal but anecdotally, I did speak with someone last evening who just put money into a Fidelity VC fund that has stakes in all the big names (SpaceX, Anthropic, OpenAI) and a 10-year lockup and is very excited.

So that’s where I see things this morning. Yesterday’s US equity declines were followed by more weakness (China, HK, India, Australia, New Zealand) than strength (Korea, Singapore) in Asia. Tokyo was essentially unchanged. However, in Europe this morning things are much brighter with solid gains across the board. US futures, too, are higher this morning by about 0.7% across the board as I type at 7:15.

In the bond market, yields have edged back down with Treasuries (-3bps) leading the way and European sovereigns right there with them. Whatever longer term concerns about inflation exist are not showing up aggressively at this point.

In the commodity markets, oil (-1.1%) continues to underperform all the calls for catastrophe and another anecdote, I saw diesel below $5.00/gallon yesterday for the first time in several months. Products are available. As to the metals, they are uniformly hated although this morning both gold (+0.4%) and silver (+0.6%) have edged a touch higher. However, the trend here in gold (and silver) is clearly back down for now.

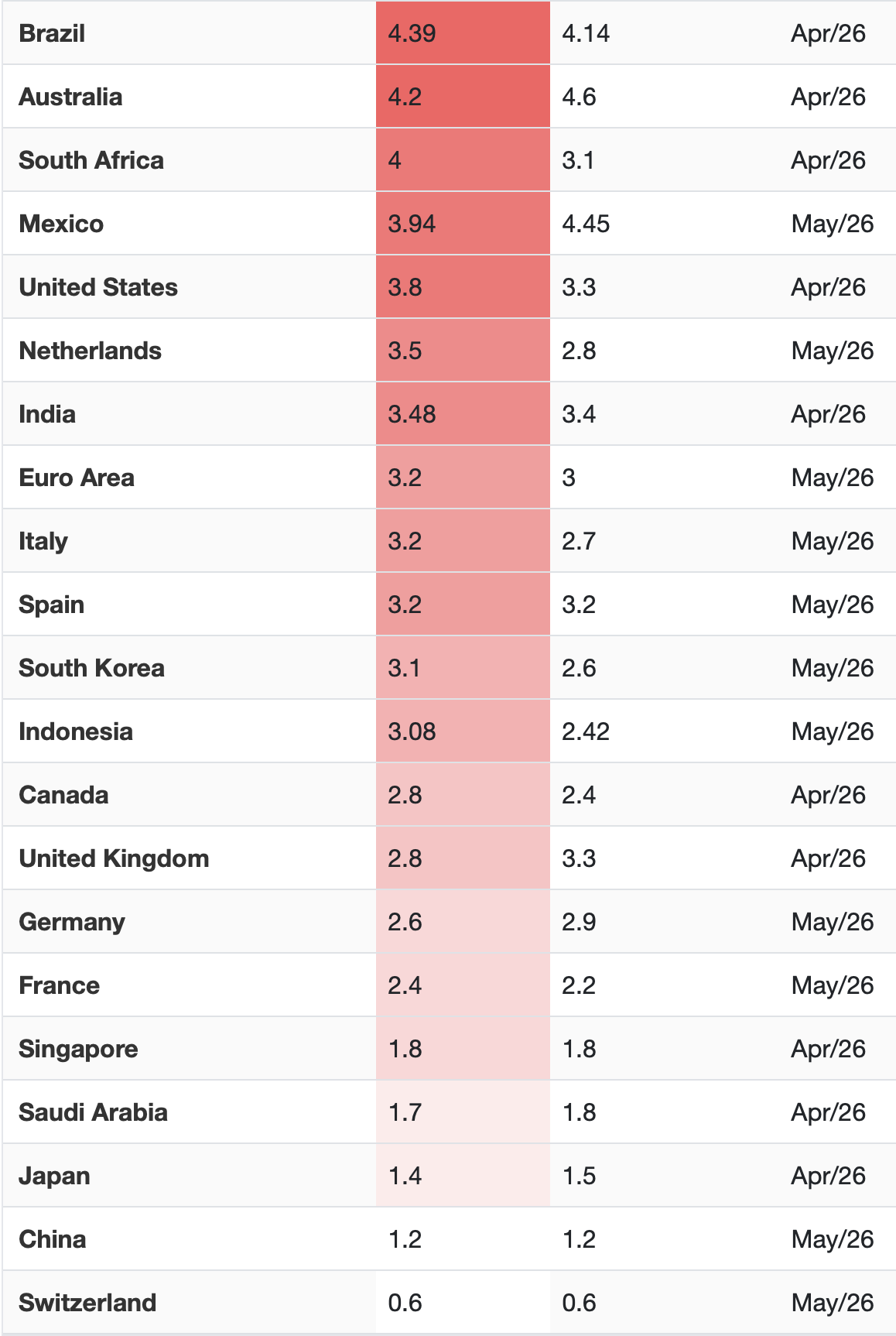

Source: tradingeconomics.com

Nothing has changed my longer-term concerns over fiat debasement, but for now, gold is not the play.

Finally, the dollar is somnolent this morning, with the euro, pound and yen all basically unchanged but sticking near recent dollar highs. No matter how I slice it, I cannot come up with a significant dollar down story despite many having that view. The US economy, by most measures, continues to drive global growth and I suspect that will remain the case for a while yet.

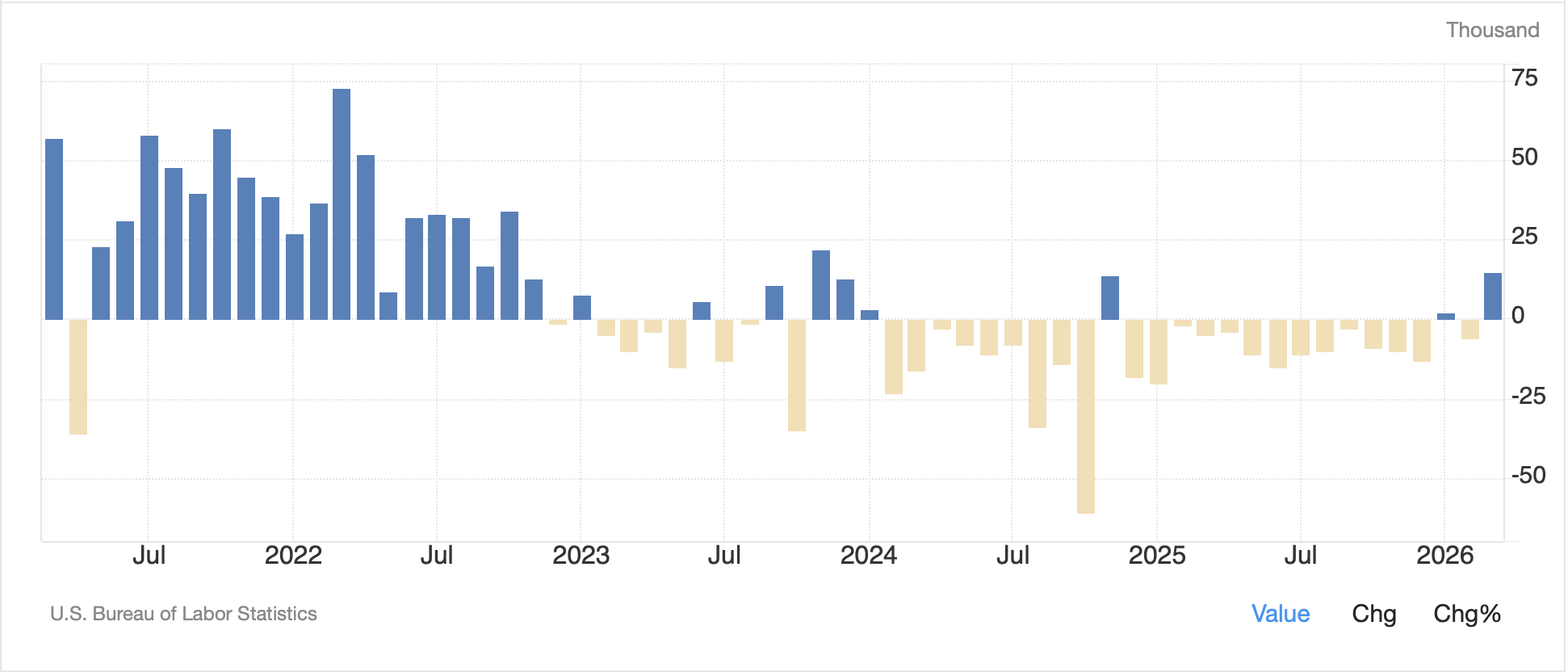

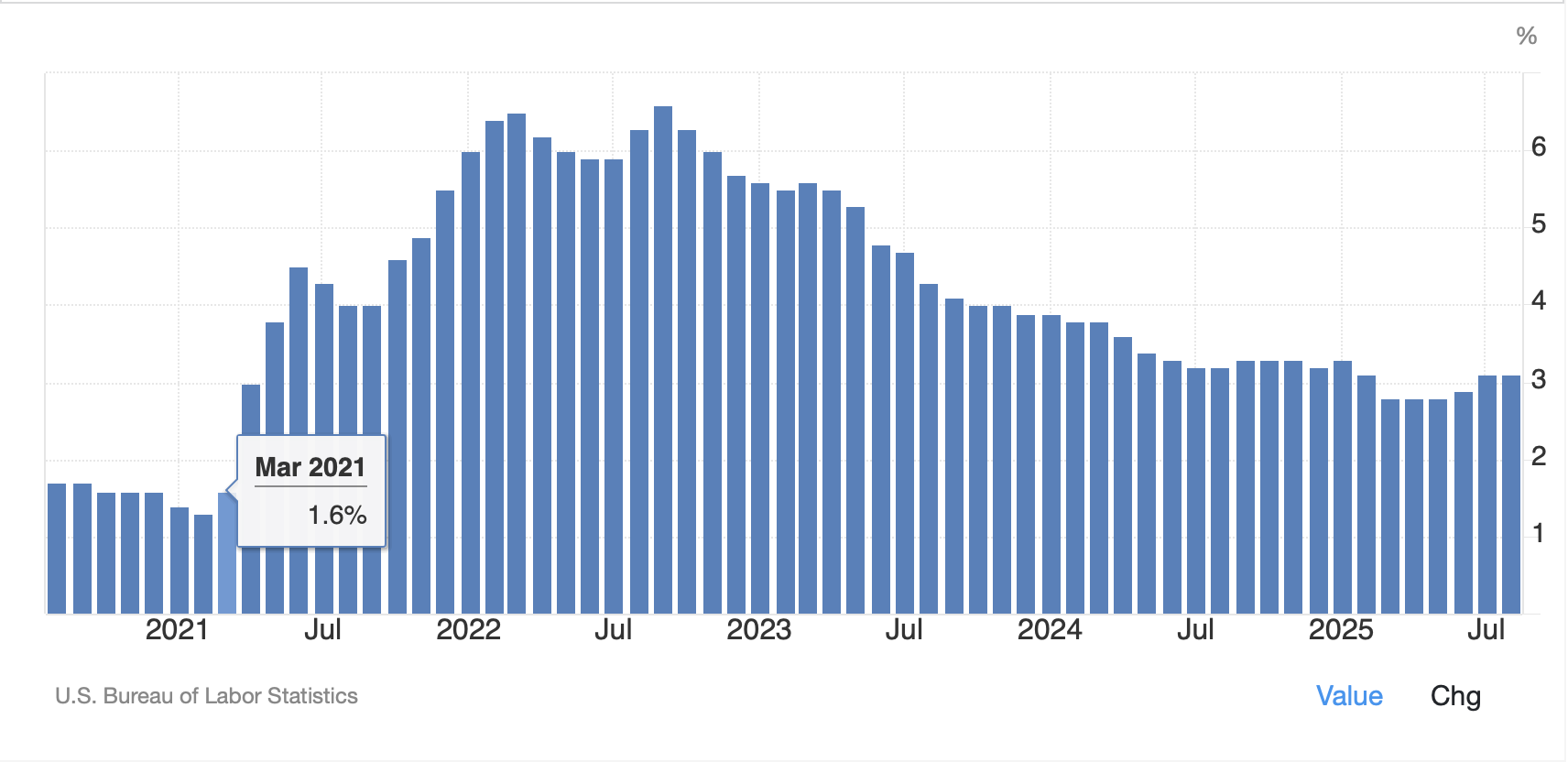

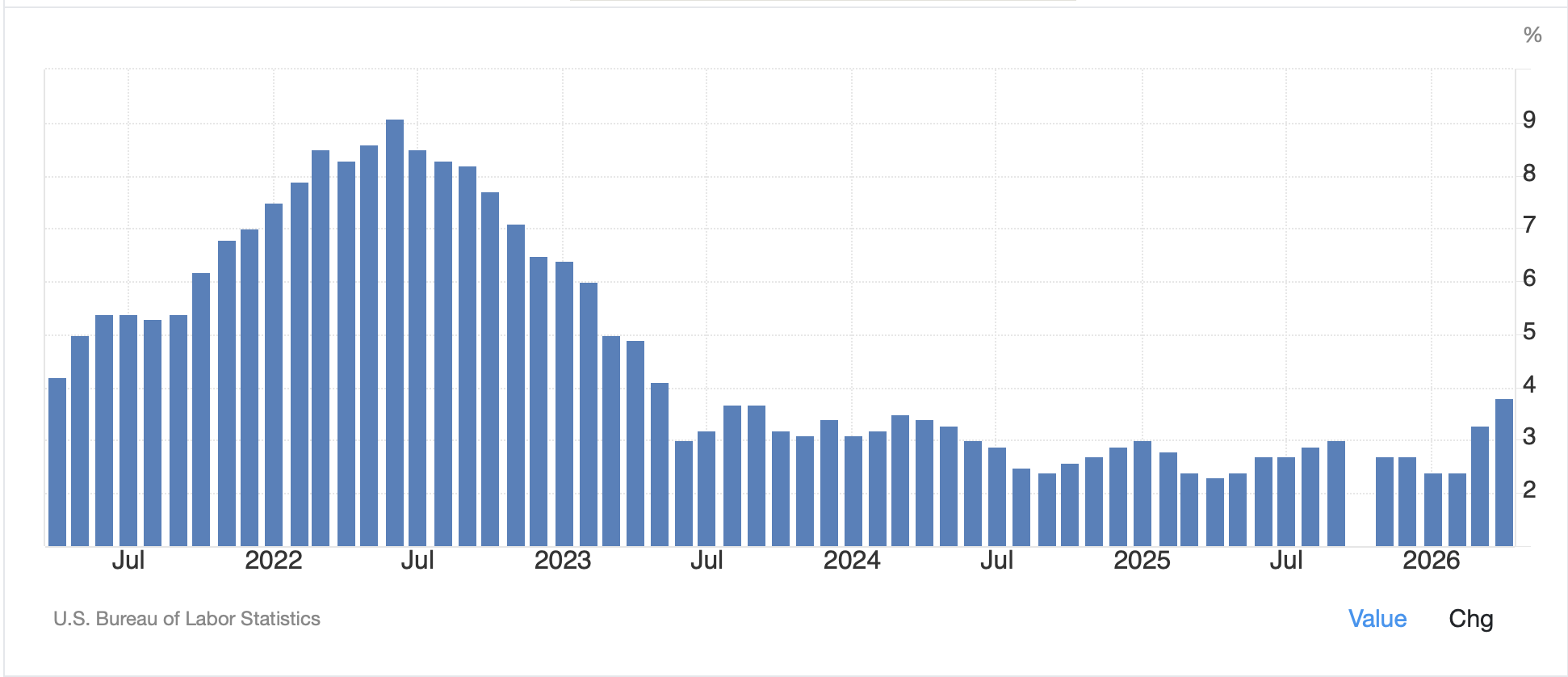

On the data front, this morning brings the weekly Initial (exp 219K) and Continuing (1780K) Claims data as well as PPI (0.7% M/M, 6.4% Y/Y) and core (0.5% M/M, 5.4% Y/Y). We also hear from the ECB shortly, with a near universal belief that they will be hiking 25bps in order to drill for more oil push back against the recent energy induced price rises. The beginnings of a major error in my view.

And that’s really it. It has been getting more difficult to find interesting things to discuss, that’s for sure, and as we head deeper into the summer, the doldrums have a history of keeping things dull.

Good luck

Adf

source: tradingeconomics.com

source: tradingeconomics.com