The yen slid further

Is it accelerating?

Or just keeping up?

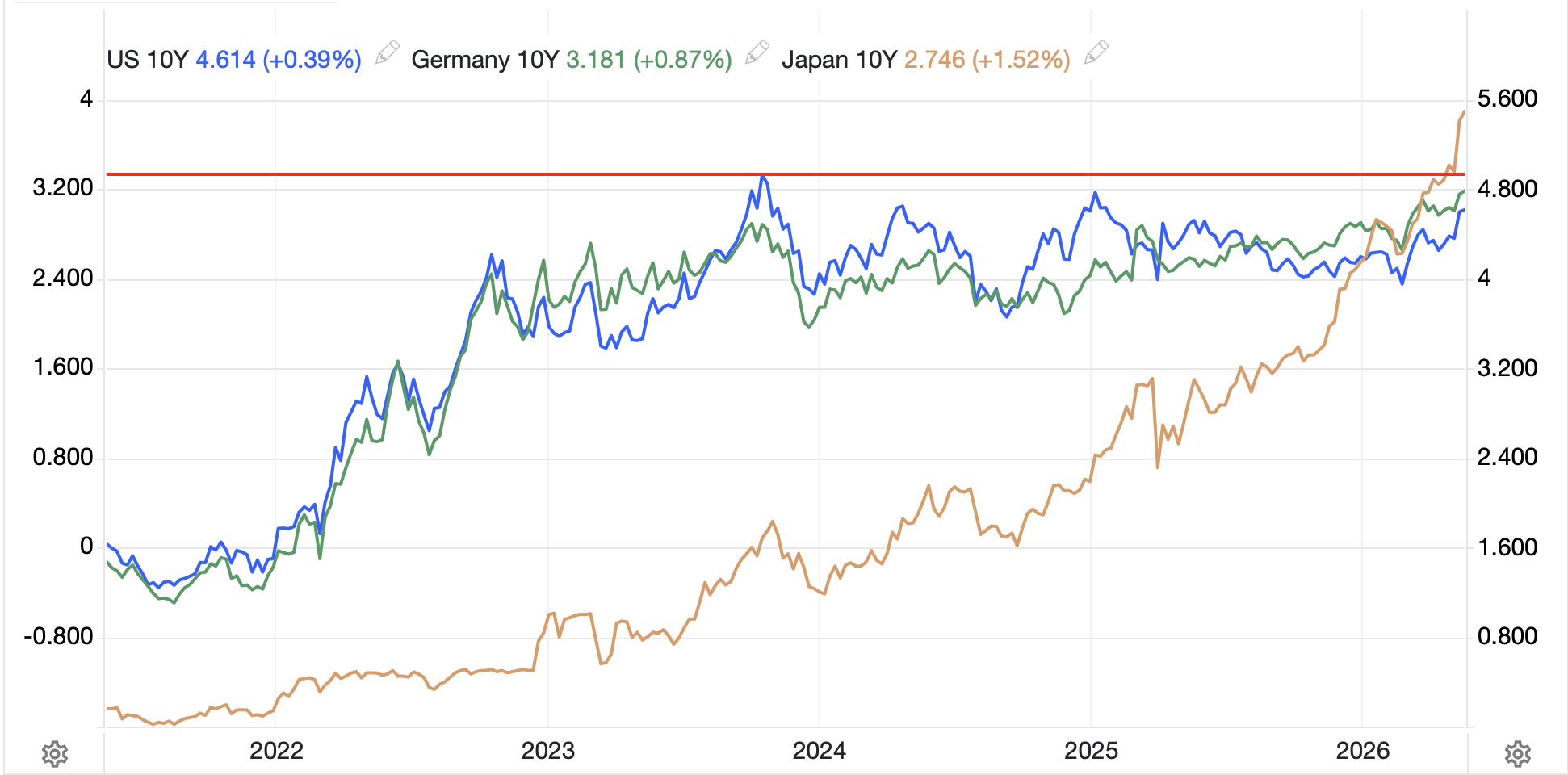

There has been a lot of press this morning regarding the yen (-0.25%) which as you can see has weakened a bit, but hardly an extraordinary move. Thus, the press is all about the level at which it now trades, 162.30ish which is a new high for the move, although it has yet to break above its 1986 levels. The nature of the articles has been a question as to when the BOJ is going to be back intervening again which then morphs into a discussion as to whether intervention is effective. (While I don’t know if they will be back in, I imagine that will be the case at some point, we know it is not effective.) At any rate, I have created the following chart on tradingeconomics.com so that you can (hopefully) see why they have not yet intervened.

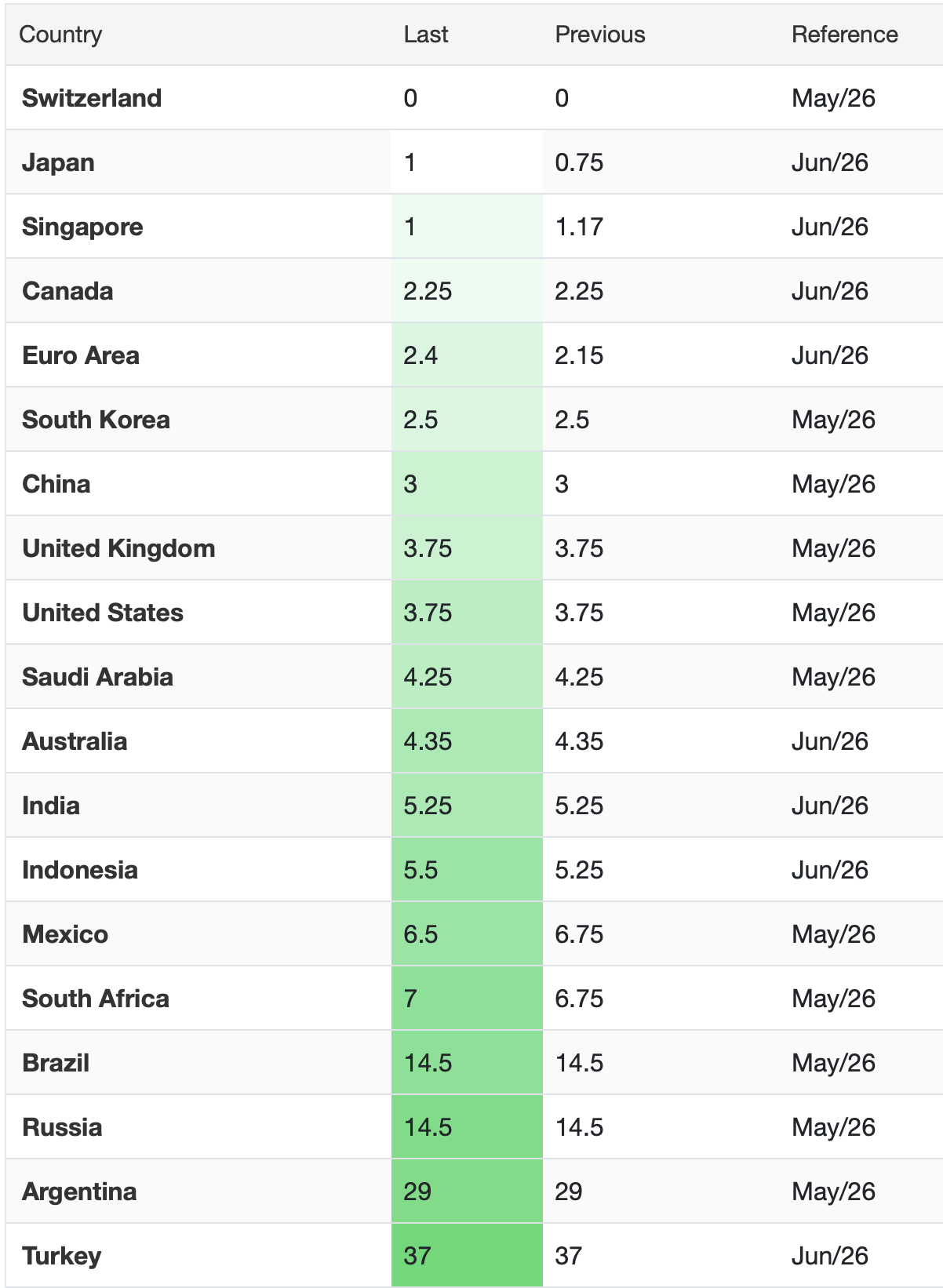

One of the key features of the MOF seven step program to intervention is the pace of the yen’s movement. A rapid decline is far less tolerable than a gradual movement. As well, there is the question of whether the yen is declining across the board, or it if is declining specifically, or at least more rapidly, vs. the dollar. It is no surprise to me that the MOF remains on the sidelines as the dollar is rallying everywhere right now, so yen weakness is really more about dollar strength. If you look at the chart above, I tried to show the slope of the movement in USDJPY vs. DXY back in the beginning of 2024 which was the previous time the yen started to show serious weakness and the BOJ intervened. To my eye, the slope of the two lines in 2024 are far different than the slope of the current movement. In fact, the table below shows that the yen’s weakness over the past week and month is hardly an outlier. In fact, it has basically held up better than its major counterparts.

My point is much is being made about the yen’s breech of the 162 level, but the movement has been quite gradual, hardly the rapid and volatile movement that has driven intervention decisions in the past. Frankly, there is little reason to believe that with the dollar strong across the board, the BOJ can do anything other than waste money in an intervention effort.

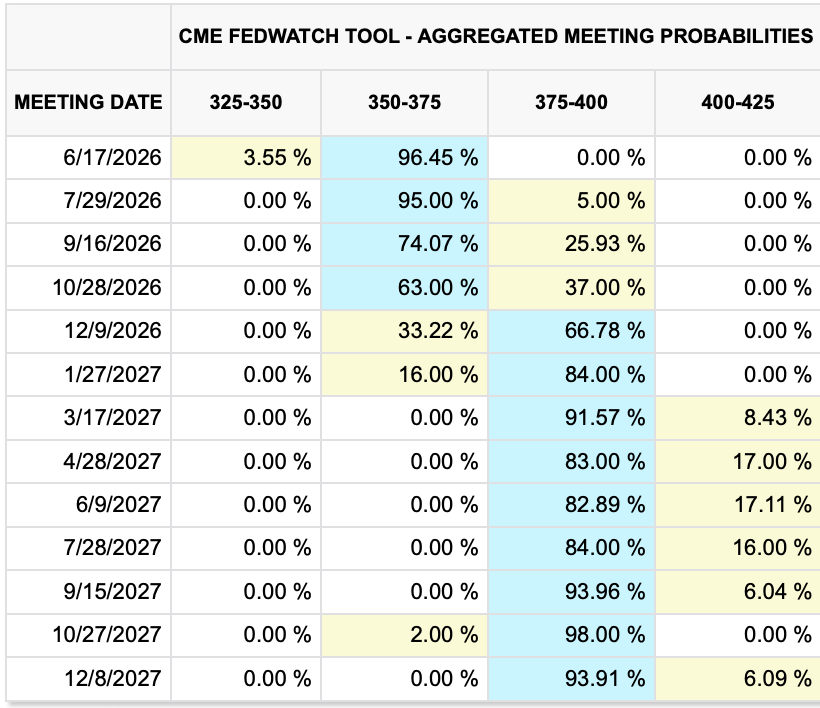

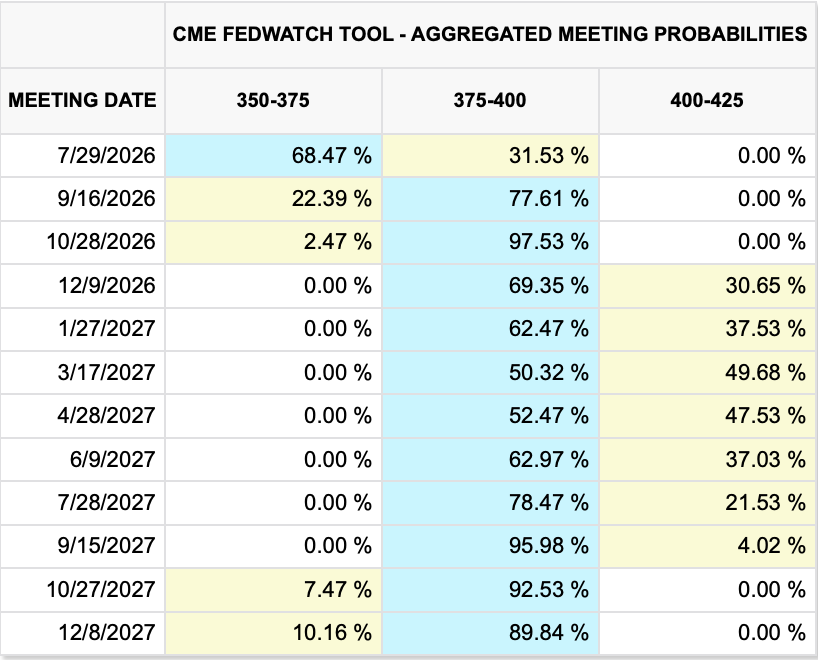

Which begs the question, why is the dollar performing so well? The pat answer remains that the market is pricing in a suddenly hawkish FOMC with the Fed funds futures market pricing an October rate hike now, with a one-third chance of a second one in December. See below from the CME.

But I still don’t understand that pricing. Despite all the ongoing chatter about the imminent shortage of oil/diesel/gasoline/jet fuel that has yet to appear and has now been delayed to H2 of this year, markets continue to price limited further interruption to energy availability. In addition, one need only look at today’s raft of Eurozone inflation data where France (1.8%), Italy (3.0%) and every German state (between 2.1% and 2.4%) all printed lower than last month, as well as lower than forecast, and recognize that the significant decline in energy prices over the past month is going to push down measured inflation. Nothing has changed my view that the Fed is on hold for now, and over the next several months the idea of rate cuts will come back into vogue. At that point, I assume the dollar will give up its recent gains, although I do not foresee a reason for a substantial decline. After all, investment flows into the US are going to remain robust.

And with that, let’s look at other markets. As proof positive that nothing is ongoing, oil is unchanged this morning, just above $70/bbl and there has been precious little new news about the situation in the Gulf. Metals are edging higher (Au +0.4%, Ag +1.3%, Cu +1.3%) but the precious set remain in downtrends although copper is in demand.

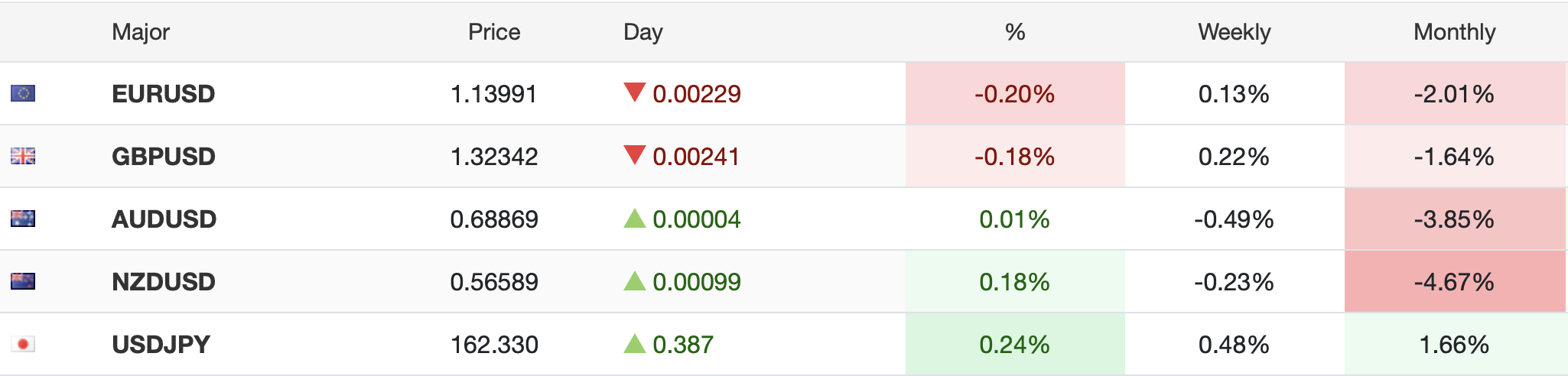

You’ve already seen the dollar movement above, at least vs. the bulk of the G10. But elsewhere, it is not a very interesting picture either. Perhaps the fact that ZAR (+0.3%) is firmer this morning on the back of both the modest rise in gold and the fact that their fiscal situation looks a bit better (significantly reduced budget deficit in May) is the outlier of note.

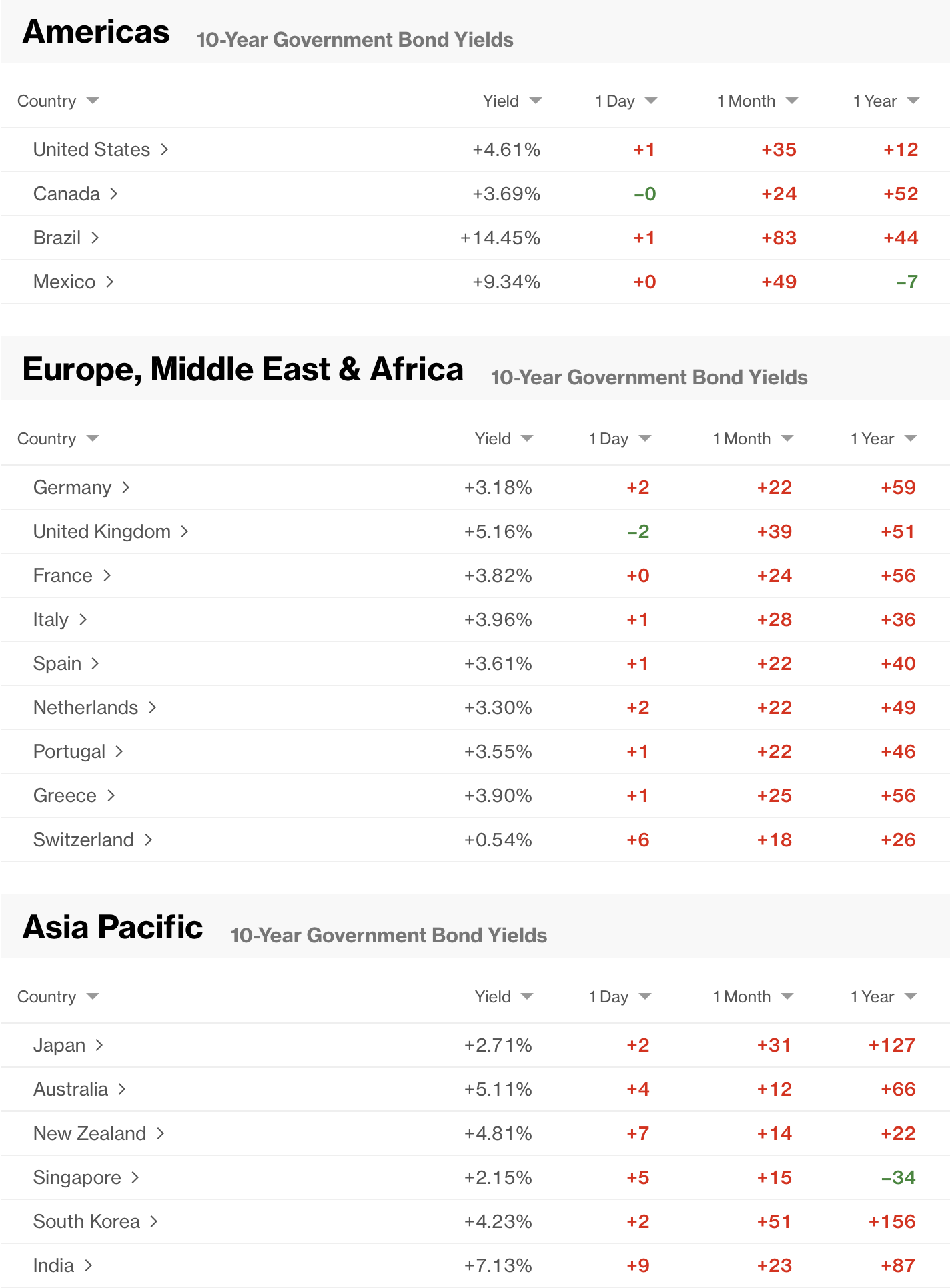

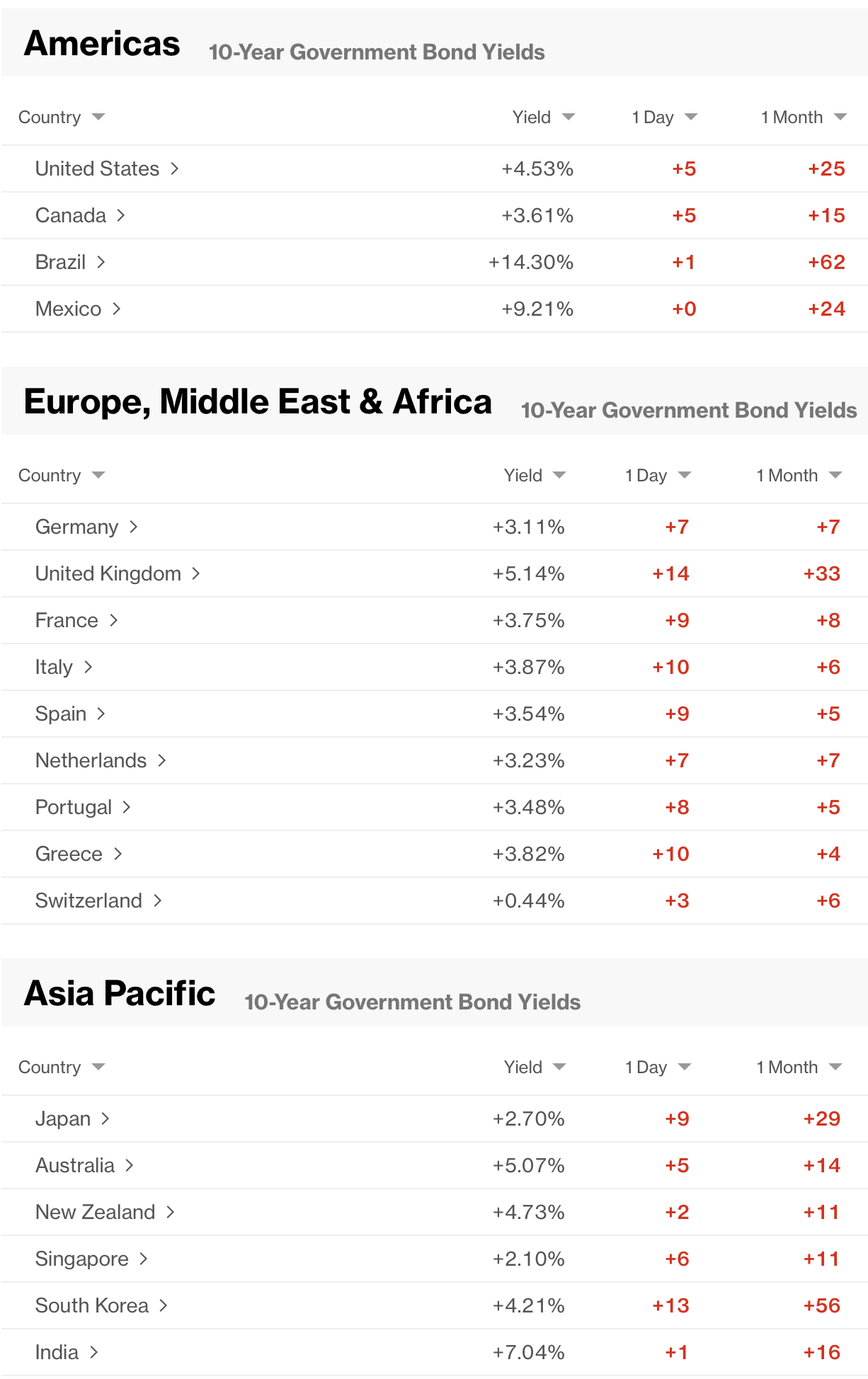

Bond markets continue to drift as 10-year Treasury yields slip -1bp and we see similar price action across most of Europe. The outlier here is Italy (+3bps) which given the better-than-expected inflation data is confusing and I have seen no other cogent explanation. As well JGB yields (+4bps) overnight reacted to the yen’s weakness as well as to comments by the newest BOJ member, Ayano Sato, who sounded modestly dovish.

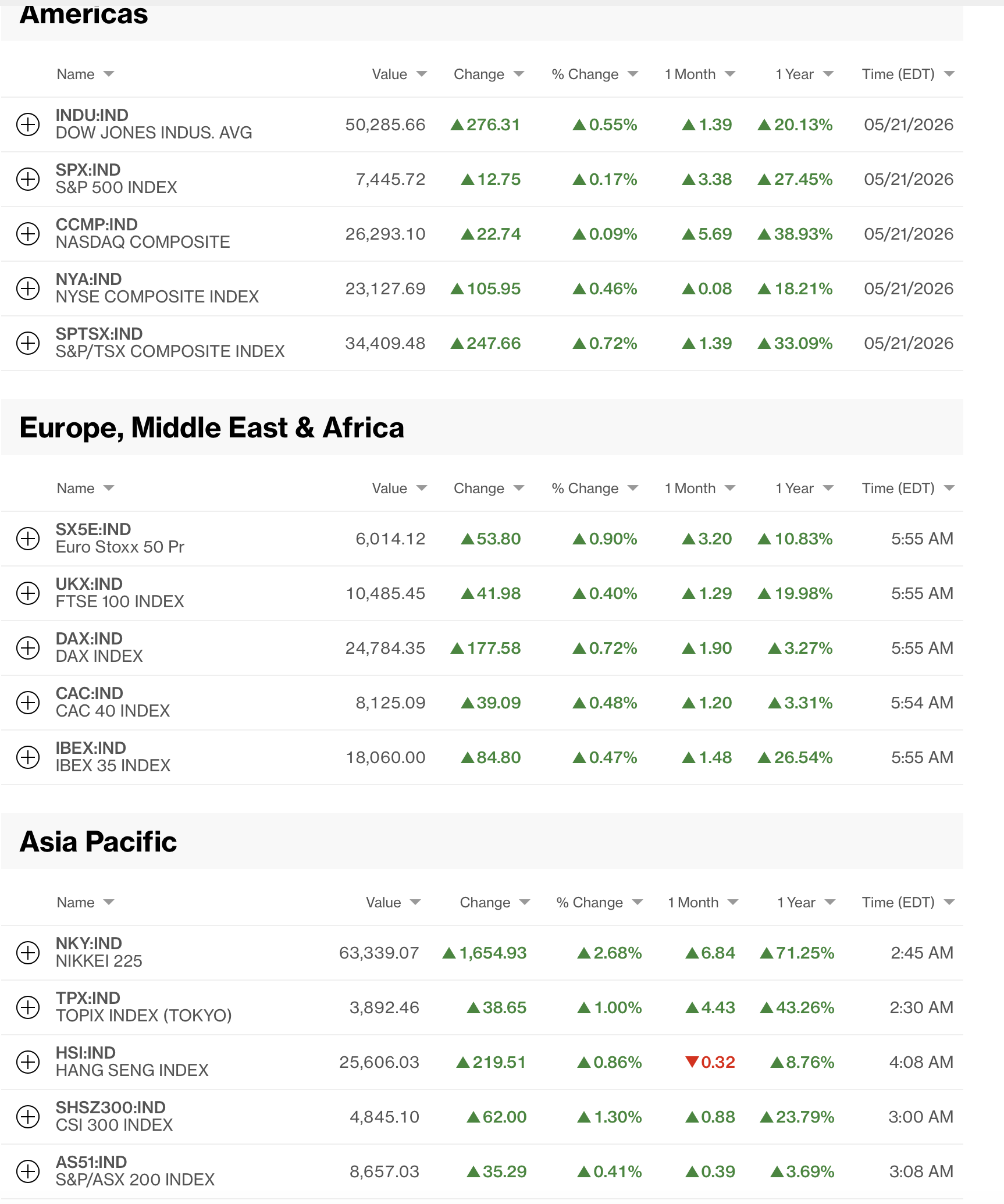

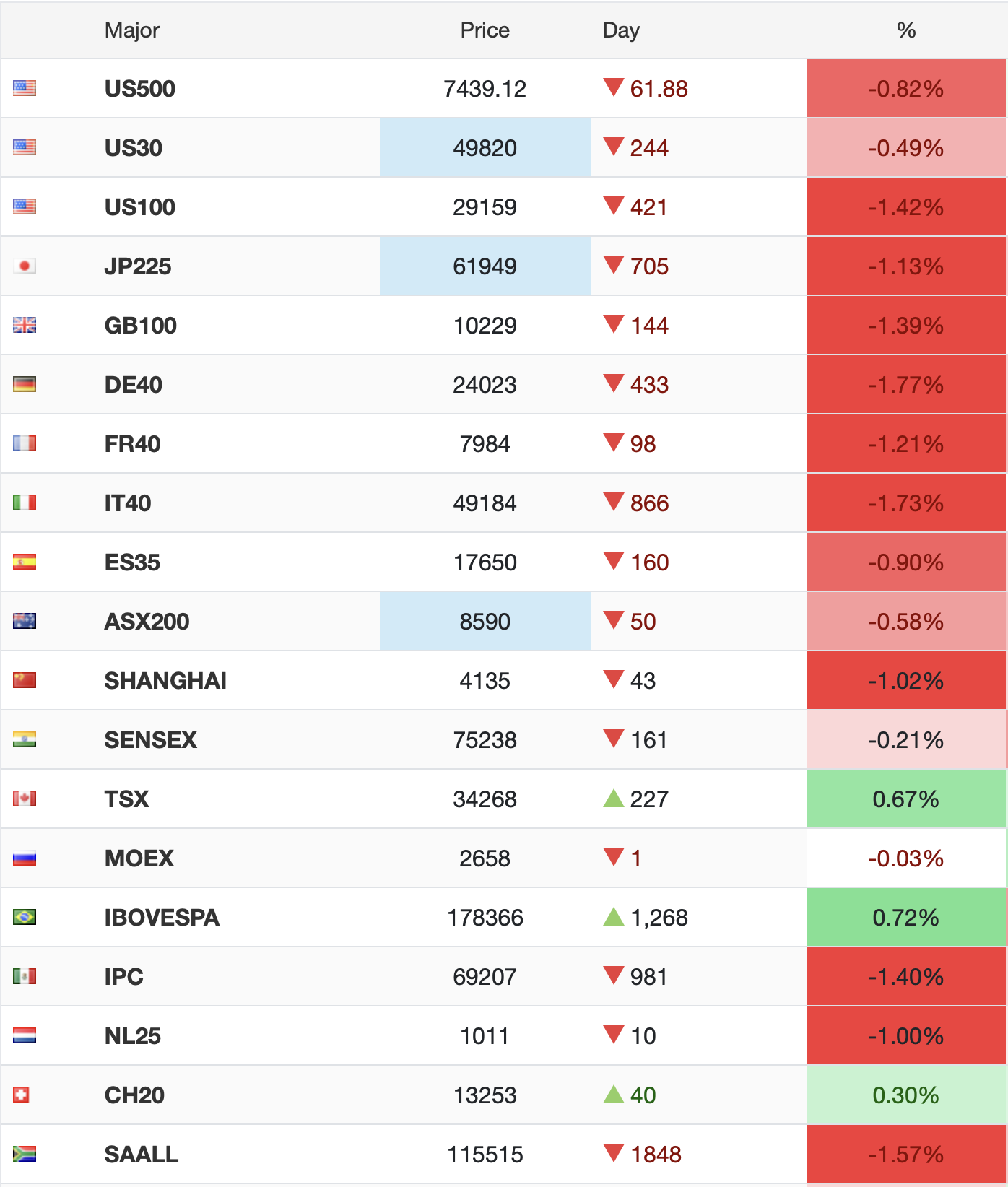

Finally, turning to the equity markets, another record setting day in the US was followed by a mixed picture in Asia with both gainers (Tokyo +0.9%, China +1.1%, Korea +1.0%, Taiwan +2.5%) and laggards (HK -0.6%, Australia -0.5%, India -0.3%, Indonesia -3.1%) with the latter a response to a legal verdict of corruption which the market has taken as a major government intrusion into the economy and frightened investors.

Turning to Europe, though, everybody is happy this morning with gains across the board (Germany +1.5%, UK +1.2%, Spain +0.7%, France +0.6%) as those slipping inflation numbers help the overall sentiment. As to US futures, you will not be surprised that at this hour (7:25) they are marginally higher.

One must be impressed with the consistency of equity market gains. It is enough to make you reconsider your prior ideas as to how markets work. Arguably, the key feature of the recent equity market performance is that earnings data continues to improve. Now, if you look at the ongoing growth in money supply, both in the US and around the world, it is no surprise that nominal results continue to rise. It is also not surprising that people are feeling stressed by inflation regardless of the data that is printed as all that money has to find a home somewhere. And the Cantillon effect tells us that the first folks who get the newly printed money (banks and institutions) are the ones who benefit the most while the rest of us simply watch our cost of living increase. This is the entire wealth/income inequality story and, arguably, the reason that the idea of socialism is making a comeback. And socialism does have a perfect record in its economic outcomes; it has failed 100% of the time it has been tried. But right now, I fear that record is not going to be a problem. There is much potential trouble ahead.

Today’s data brings Case-Shiller Home Prices (exp 0.9%) as well as Chicago PMI (58.1), JOLTs Job Openings (7.30M) and Consumer Confidence (94.7). But with Warsh on the tape tomorrow morning and then NFP on Thursday, I don’t see today’s data having much impact.

While the Iran situation is in the background right now, it remains the issue with the biggest potential impact going forward. A successful conclusion of a deal and resumption of flows of energy through the SOH will put additional downward pressure on energy prices, and by extension general inflation. In that scenario, central banks will be quick to turn away from rate hikes. However, if things collapse there, then we will need to be prepared for another major hiccup, that’s for sure.

Good luck

Adf