The clock has been wound and rewound

And meantime stock buyers dumfound

The good and the great

Who mostly, Trump, hate

And fear that their power’s southbound

But still the blockade is in force

And info depends on your source

Will Trump send marines

To take Iran’s means

And break them as matter of course?

Another day and nothing has changed in the Persian Gulf or the Strait of Hormuz. The US’s naval blockade is still in force with several Iranian tankers being stopped on outbound routes. As well, Iranian small gunboats have attacked several freighters seeking to exit the Gulf. No negotiations are on the calendar, although Pakistan, Egypt and Turkey are ostensibly working to get the two sides together. This has become a waiting game, it seems, to see if Iran can suffer the loss of 90% of its revenue for longer than President Trump can suffer the political damage that higher oil prices are inflicting on the economy.

The funny thing is the economy doesn’t seem to be that bad overall. Clearly, nobody is happy to pay more for a tank of gas, but the data has yet to show a major disruption in the US economy. And in fact, this morning’s Flash PMI data from around the world has shown a pickup in manufacturing activity as per the below table (data from tradingeconomics.com):

| Country | Actual | Previous |

| Australia | 51.0 | 49.8 |

| Japan | 54.9 | 51.6 |

| India | 55.9 | 53.9 |

| France | 52.8 | 50.0 |

| Germany | 51.2 | 52.2 |

| Eurozone | 52.2 | 51.6 |

| UK | 53.6 | 51.0 |

| US | 52.5 expected | 52.3 |

The narrative on this improvement centers on the idea that people/companies are trying to get ahead of the future where price hikes and shortages of goods become extant, similar to the front-running of the tariffs in Q1 last year and that is certainly part of the story. But it also appears that, in the US at least, there is real manufacturing growth occurring.

Freightwaves is a company that tracks trucking and freight movement around the US, and its latest data show solid increases in activity along with a tighter market (rising costs) as demand rises. Too, this activity is emanating from the center of the country not the West coast, indicating this is domestic production and not imports. Anecdotally, I have a friend in the trucking business, and I asked him about this situation yesterday. He confirmed that the trucking business is booming.

Remember, too, that in the last NFP report, Manufacturing employment rose 15K, far surpassing expectations. I make these points to highlight that the US economy continues to perform pretty well despite the angst over the war and rising gasoline and diesel prices. One last tidbit is Retail Sales, which rose a greater than expected 1.7% last month, and 0.7% in the control group which excluded gasoline. Those numbers do not confirm economic weakness.

And you know what helps confirm that the US economy is ticking over nicely? The continued equity market rally. Since the war began, after the initial fears that rising oil prices were going to collapse the global economy, the market has completely reversed course as you can see in the below. Chart.

Source: tradingeconomics.com

From the nadir on March 30th, the S&P 500 has rebounded 12.5% to new all-time highs. Earnings data that has been released for Q1 thus far has shown significant growth, upwards of 18% profit growth, again not a sign of a struggling economy. And perhaps the key feature of my argument is the following cover of The Economist magazine, which seems to have an almost perfect track record in terms of its cover articles, it is wrong nearly 100% of the time.

There continues to be a great deal of doom porn available if you like that type of stuff, but I am having a hard time seeing the depth of the damage that many claim. Certainly, things can get worse if Iran lashes out in final death throes of the regime and seeks to destroy as much GCC infrastructure as possible, but right now, I don’t see that outcome. My belief is the marines go for Kharg island shortly and are better than even odds to be successful. If that is the case, then we will be in the final stages of this conflict and people will move on. After all, who remembers Venezuela as a major crisis today? Most people have very short attention spans.

Ok, let’s see how things stacked up overnight after yesterday’s continued US equity rally. This morning, feelings are not as buoyant although it is not clear why. Equity markets in both Asia and Europe were broadly lower although that could simply be a bit of profit taking after some strong runs all around. Tokyo (-0.75%), HK (-1.0%) and China (-0.3%) all slipped as did Australia (-0.6%), India (-1.1%) and Taiwan (-0.4%). But Korea (+0.9%) bucked the trend along with Malaysia (+0.6%) while the rest of the region was weak. The Korean economy showed surprising strength in Q1 with GDP last night released at 3.6% annualized in Q1 supporting the market there.

As to Europe, despite the solid Manufacturing PMI data, Services data has been under more pressure and equity markets seem to be following that with Spain (-1.3%), the UK (-0.9%) and Germany (-0.5%) all slipping although France is unchanged this morning. As to US futures, they are softer as well at this hour (6:55), down by -0.5% or so across the board.

In the bond markets, Treasury yields have backed up 2bps this morning with European sovereign yields higher by between 1bp and 3bps. The outlier here is UK gilts (+5bps), which seems to be responding to general financing concerns in the UK as the budget deficit there continues to grow faster than forecast. JGB yields also backed up 2bps.

Oil (+1.2%) is beginning to get concerned again about the Iran situation as we are currently in the midst of a 3-day rally. While the WTI price, at around $94/bbl, is sitting in the middle of its range since the inception of the war, clearly there is some concern.

Source: tradingeconomics.com

The EIA inventory data showed a build in crude inventories but a pretty large draw of gasoline and distillates. Perhaps it was the latter that is the driver. As to the metals markets, the negative correlation between oil and gold is back with the barbarous relic (-0.8%) slipping while silver (-3.8%) is really having a rough session. It is key to remember, though, that silver is an inherently more volatile commodity than gold given the market’s much smaller size. In truth, looking at the chart over the past six months, it is hard to get the sense that it is doing too much at all right now.

Source: tradingeconomics.com

Finally, the dollar is rebounding a bit this morning, with the DXY (+0.2%) continuing to trade in its broad range from the past year as per the below chart.

Source: tradingeconomics.com

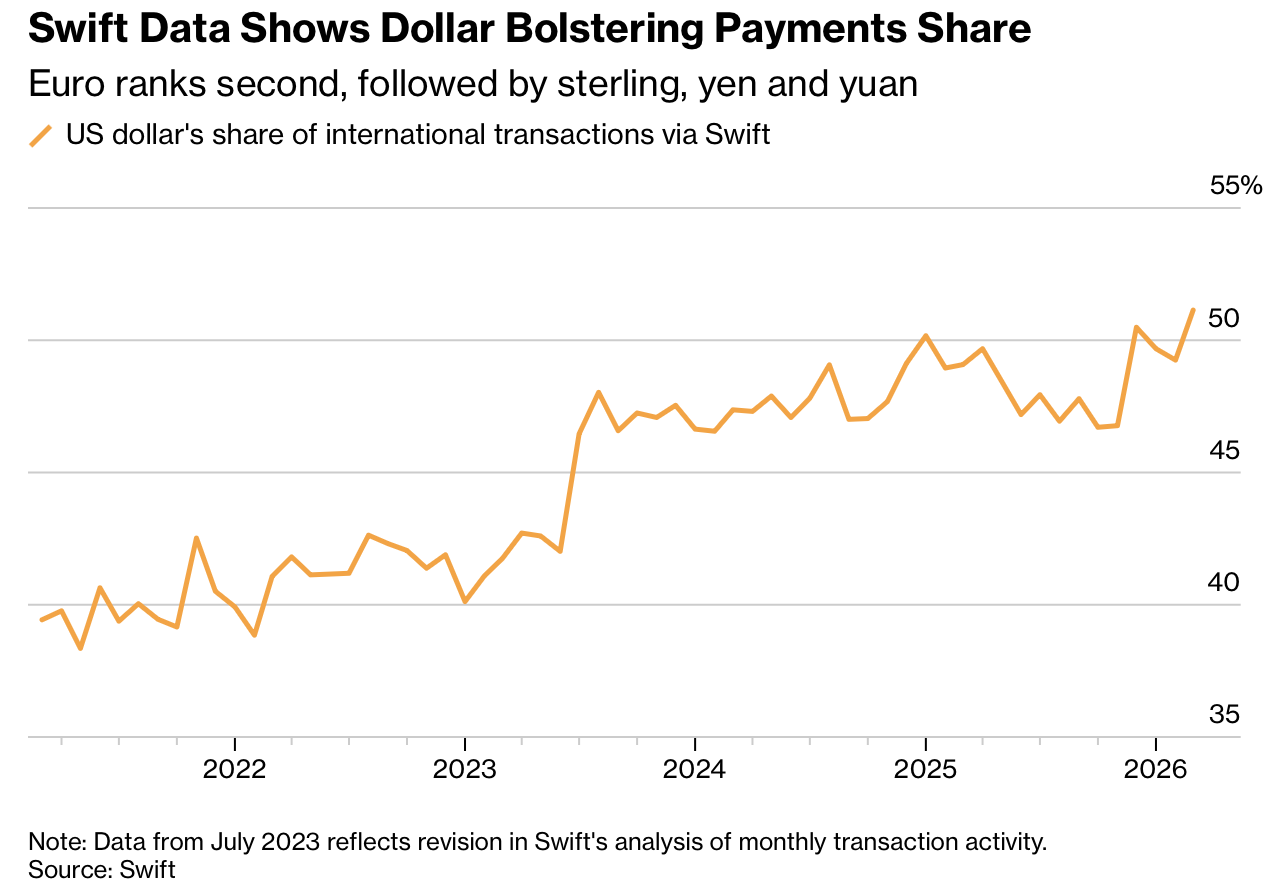

While the death of the dollar and de-dollarization narratives remain popular amongst a broad set of analysts, data outovernight from SWIFT shows that the dollar’s portion of international transactions rose to a record 51.1% in March, its highest level since SWIFT revised its procedures.

Source: Bloomberg.com

I regularly read analysts who are very smart explaining all the reasons why the dollar is destined to collapse amid concerns over the unsustainable debt and the use of the dollar as a political tool, and those things are true as far as they go, but for the foreseeable future, TINA is the rule. No other fiat currency is going to be an effective substitute because no other nation has the heft and strength of capital markets to do so.

The dollar’s strength today is pretty universal with nothing terribly noteworthy regarding specific moves. Perhaps the one surprise is NOK (-0.3%) which is not following oil higher.

On the data front, this morning brings the weekly Initial (exp 212K) and Continuing (1820K) Claims data as well as the above-mentioned Flash PMI data. Again, despite all the teeth gnashing, the labor market seems to be holding in quite well overall. Perhaps my glasses are tinted rose and I don’t see that, but the data releases that we continue to see do not point to an imminent collapse in the US economy. Rather, continued strength seems the most likely result. With that in mind, I do not see the dollar falling sharply under any scenario and suspect that a test of 100 on the DXY and 1.15 in the euro may be on the horizon.

Good luck

Adf