For Holmes, when the dog didn’t bark

He recognized that was the spark

To solving the case

And so, we must brace

For narrative changes quite stark

This morning, no headline appeared

Regarding Iran, which is weird

Have markets moved past

This problem, at last?

And if so, what’s next to be feared?

So, perusing the WSJ on-line this morning, the notable absence was any story on Iran and the current situation regarding the ongoing peace talks. There was a throwaway article about Trump and what he has said about Iran, but nothing of substance. Part of me is amazed that this is the case as the conflict would still seem to be the most important issue in the markets given the impact on oil prices and inflation, as well as its general geopolitical impact. But part of me cannot be surprised at all. It’s not just traders who have the attention span of a fruit fly, apparently so does the general public.

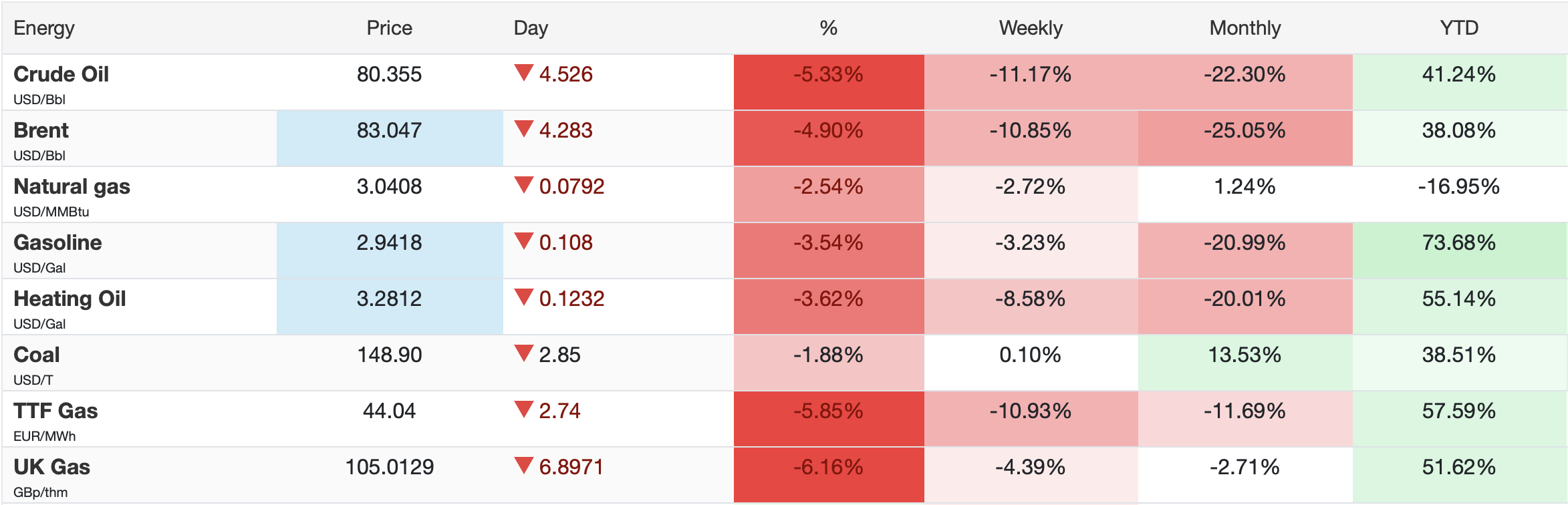

I made the point several weeks ago that this conflict would fade into history quickly when it was ending based on the fact that the Venezuela incursion, back in January, fell from headlines within about three days. Given the generic MO for most publications of, if it bleeds, it leads, the fact that bombs are no longer falling, and peace talks are ongoing is no longer that interesting. Add to that the generic TDS of most of the media, where they loved to play up rising oil prices as a major policy failure for Trump, now that those prices have been falling for the past 11 weeks and have slipped >30% in that period, and quite frankly, have further to fall, most editors have moved on. If they cannot tar Trump with a policy failure, they would rather not discuss the subject at all.

Source: tradingeconomics.com

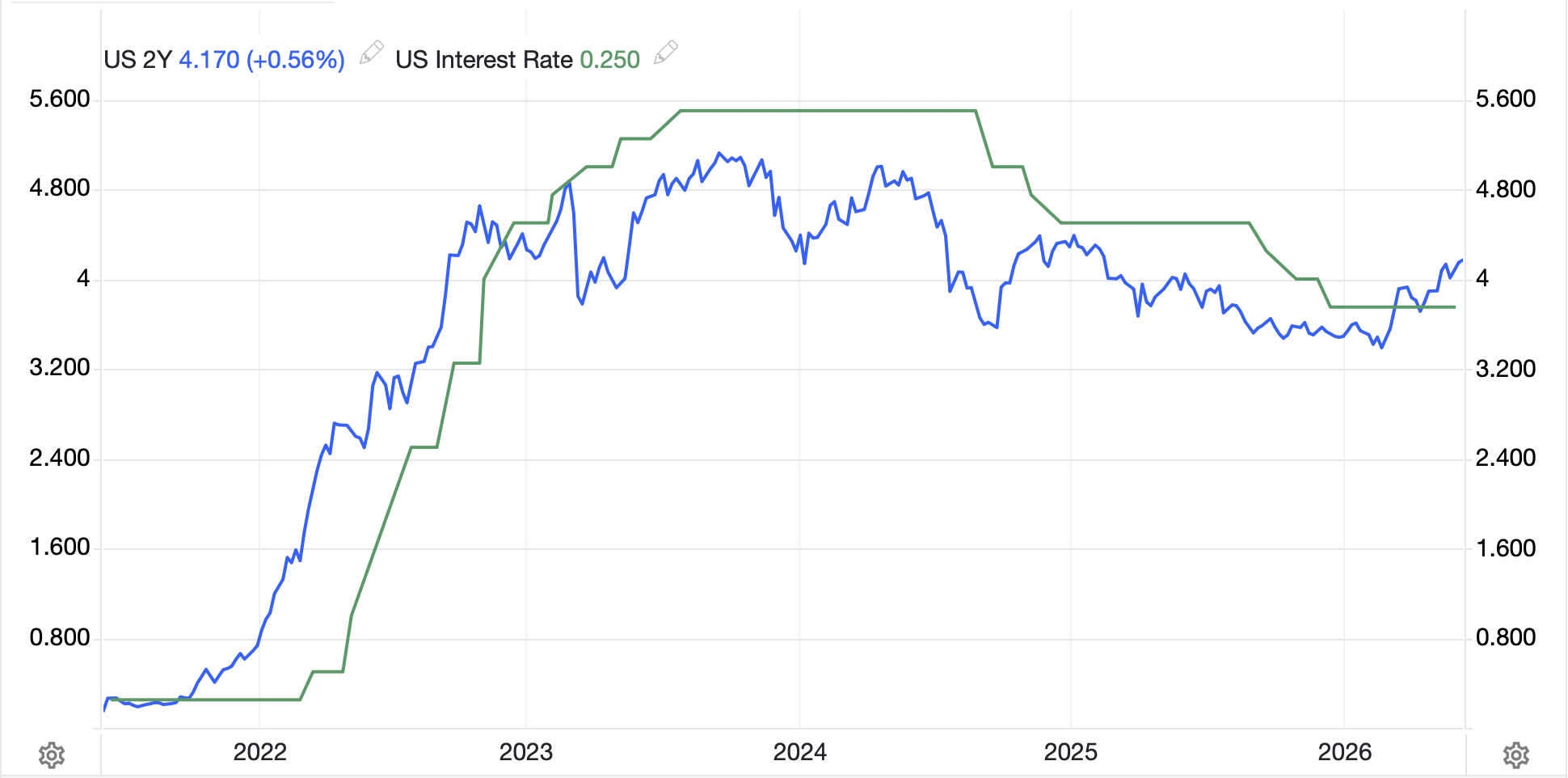

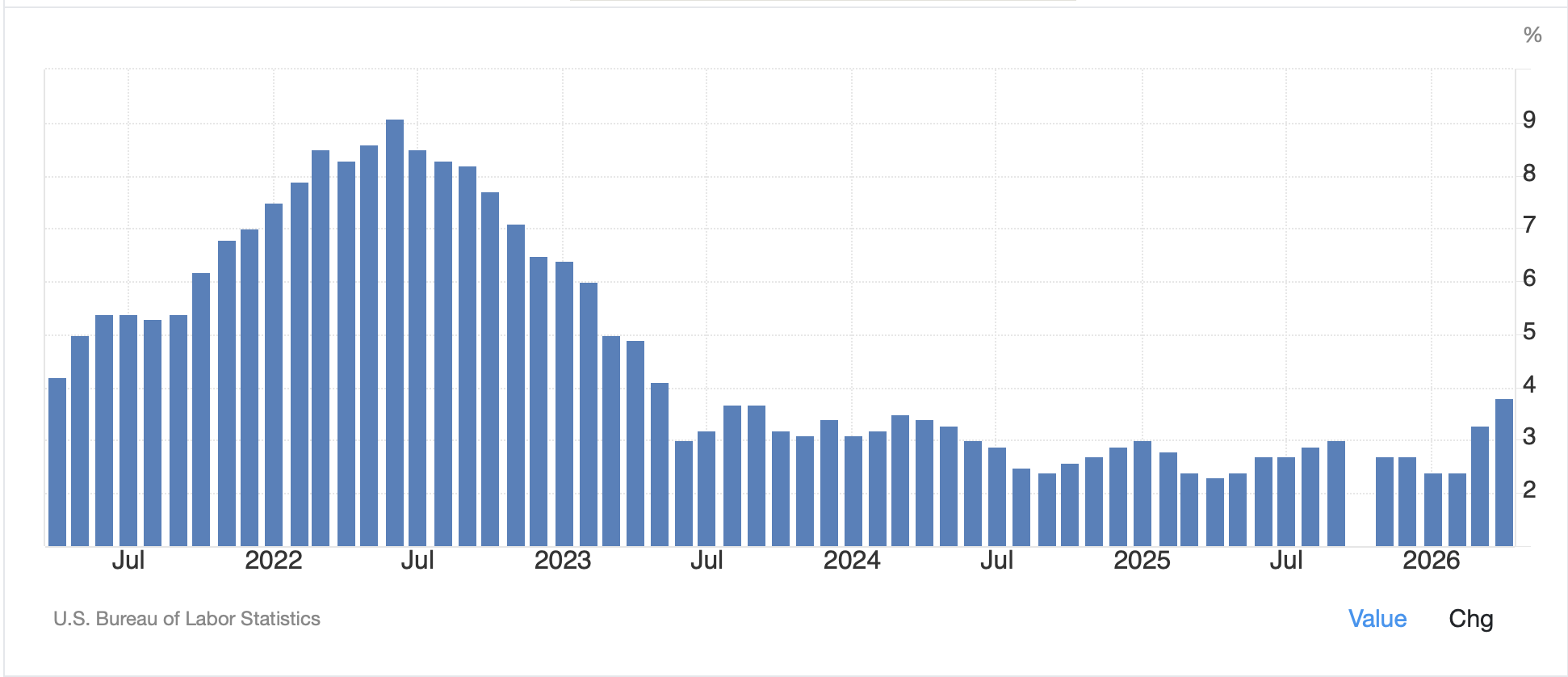

So, here we are this morning with the market now turning its focus to an ostensibly hawkish Fed despite the recent analysis by the BLS indicating that more than 60% of the recent uptick in inflation was driven by the rise in energy costs. So, with energy costs reversing course dramatically, what does that say about their impact on inflation and exactly how hawkish does the Fed need to be in that case.

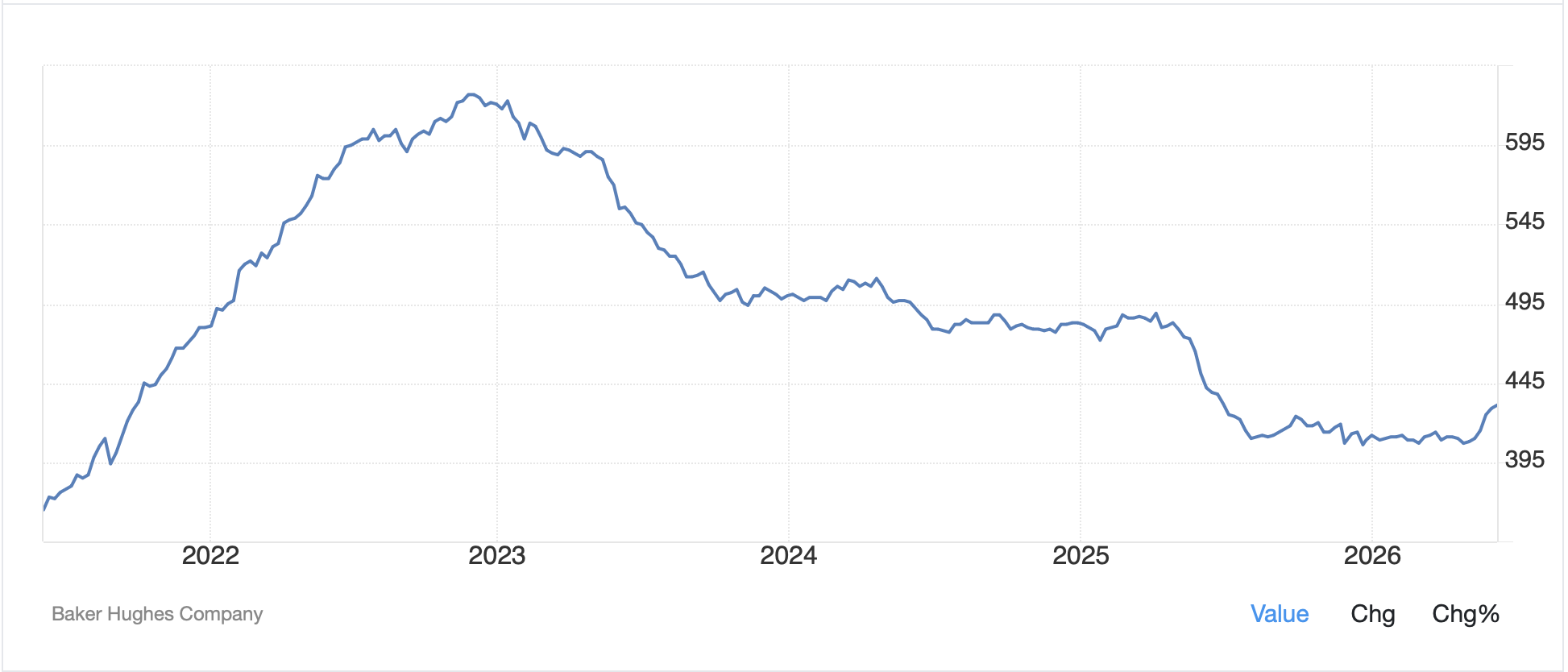

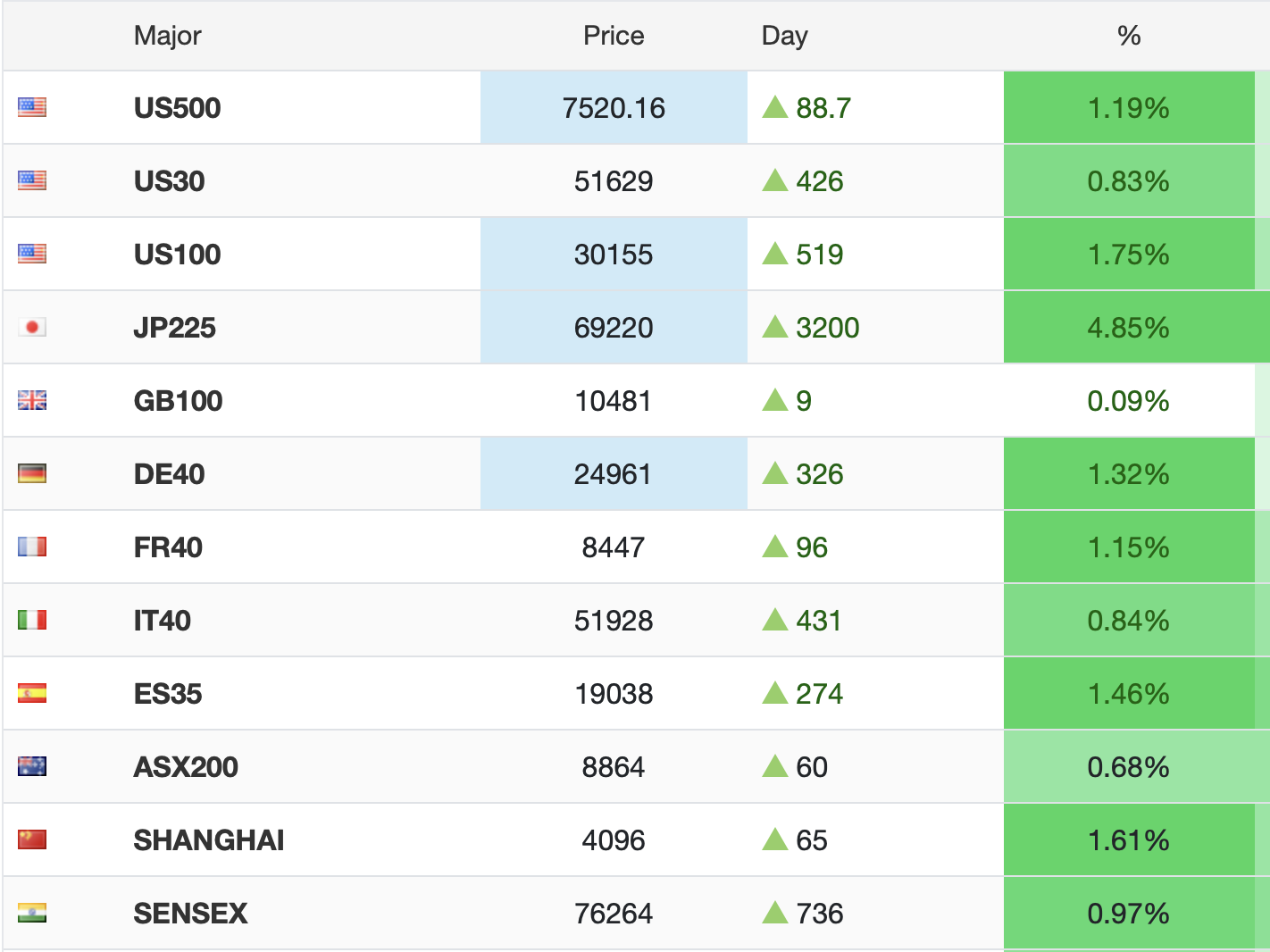

Right now, equity markets are under some pressure as some of the euphoria associated with the rising tech sector’s stock prices and the ongoing AI mania, is wearing a little thin. And let’s face it, things certainly seemed a bit bubblicious. But the combination of ongoing fiscal support from the OBBB and tax cuts and declining energy prices is likely to help support things going forward. No matter the timeline you observe, we have seen a remarkable rally in tech stocks, as evidenced by the NASDAQ’s chart below. A correction to the 50-day moving average would hardly be surprising, nor would it be damaging to the overall market structure, I think, although it would almost certainly result in ‘end of days’ headlines!

Source: tradingeconomics.com

So, while futures this morning are lower across the board (NASDAQ -2.9%, SPX -1.4%, DJIA -0.6%) as of 6:40am, and we could easily see some weakness for a few more days/weeks as positions shake out, I am not in the camp of things are about to collapse.

Speaking of equity markets, the overnight session was filled with red ink led by the KOSPI (-10.0%) in South Korea, although there was weakness pretty much everywhere (Nikkei -3.6%, CSI 300 -2.8%, Hang Seng -1.8%) with India and Taiwan also slipping more than -1.0% although Australia, NZ and Singapore had more muted declines. Tech was clearly under pressure. Of course, we cannot be surprised that European shares are also lower in a generally weak risk scenario, but given the lack of tech companies headquartered there, the declines have been far less significant (DAX -1.0%, CAC -0.6%, IBEX -0.2%, FTSE 100 -0.2%) although the Netherlands (-1.3%) home to ASML, the only tech name of note on the continent, is underperforming as well.

Meanwhile, the bond market has peeked at the oil market and decided, perhaps inflation is not a chronic condition, or at least not as bad as previously feared. Yields are lower across the board with Treasuries (-3bps) leading the way while European sovereigns are all lower by between -3bps and -4bps. Overnight, though, JGB yields could make no headway lower as the yen continues to be under enormous pressure.

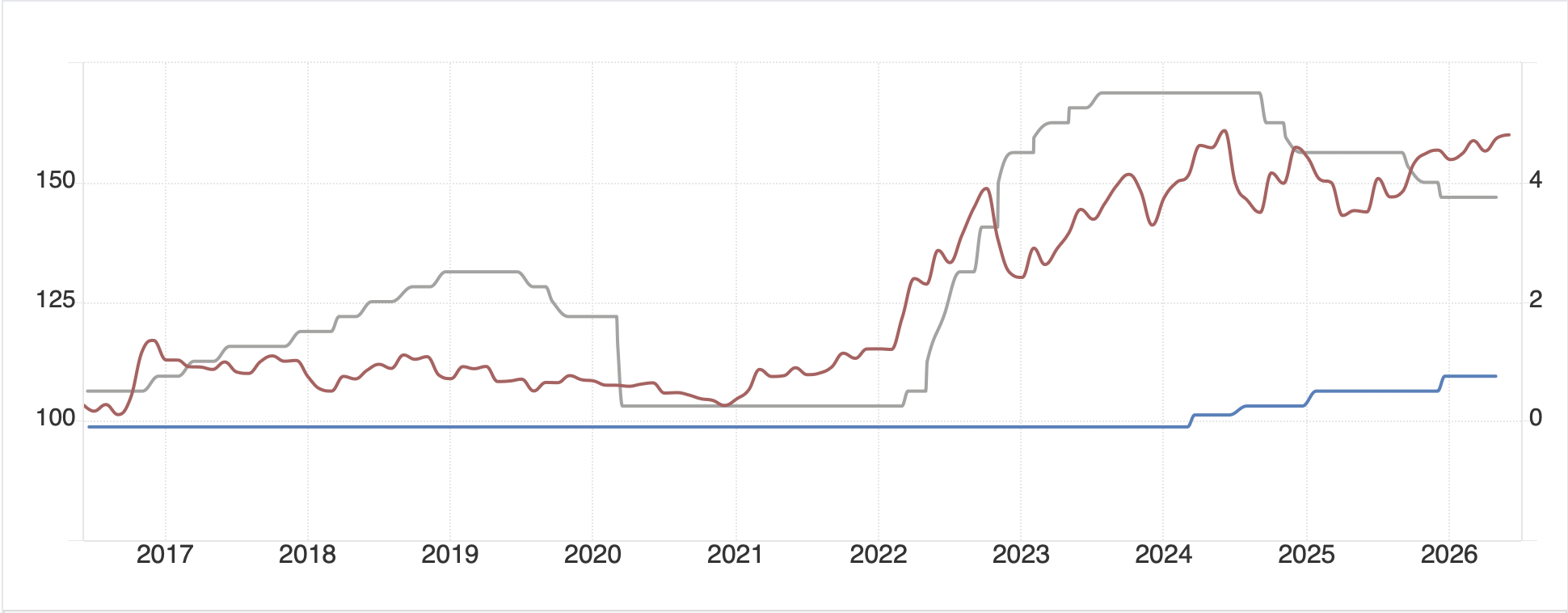

Speaking of the yen, it continues to slowly weaken despite prominent statements by Japanese FinMin Katayama about her discussions with Treasury Secretary Bessent and their agreement to have the US coordinate with Japan in the event it is decided something needs to be done in the markets. But so far, no signs of actual intervention. A look at the chart below shows a very slow and steady climb in the dollar, and frankly, I do not see what will change this trajectory.

Source: tradingeconomics.com

While interest rates aren’t the only driver, they still have a key impact, and they are the one thing that can be changed quickly. In fact, the best hope for the yen, in my view, is the fact that at some point soon, the market is going to understand the Fed is not about to raise rates again, and the next move will likely be lower, albeit not until later in the year. but that change in tone will change a lot of opinions on how the yen should behave, and a move back toward 155 amid modest overall dollar weakness could easily be seen. But right now, everybody is of the opinion that the FOMC is going to hike this year, and Japan cannot afford to be aggressive in that context, hence the yen’s weakness.

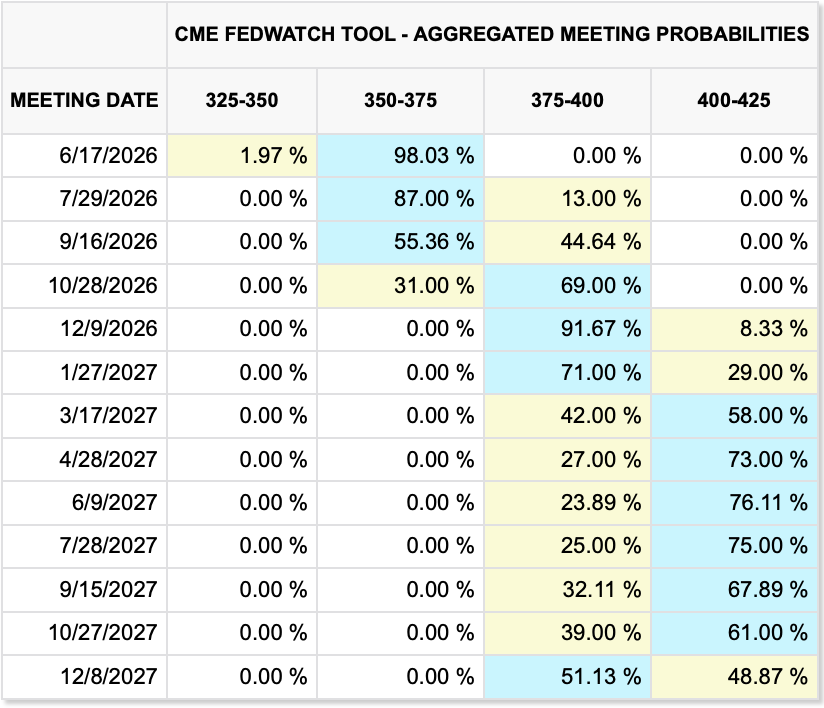

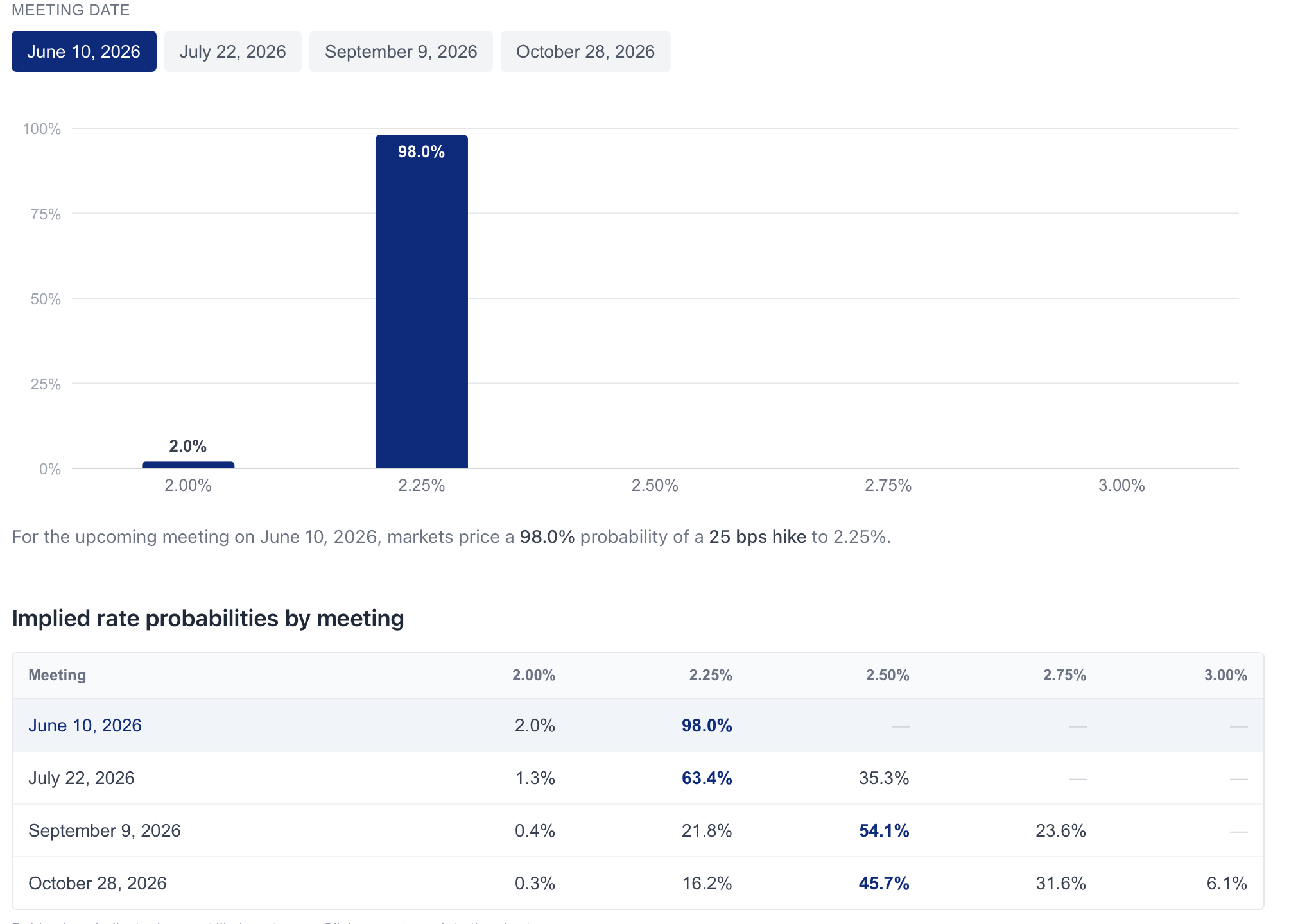

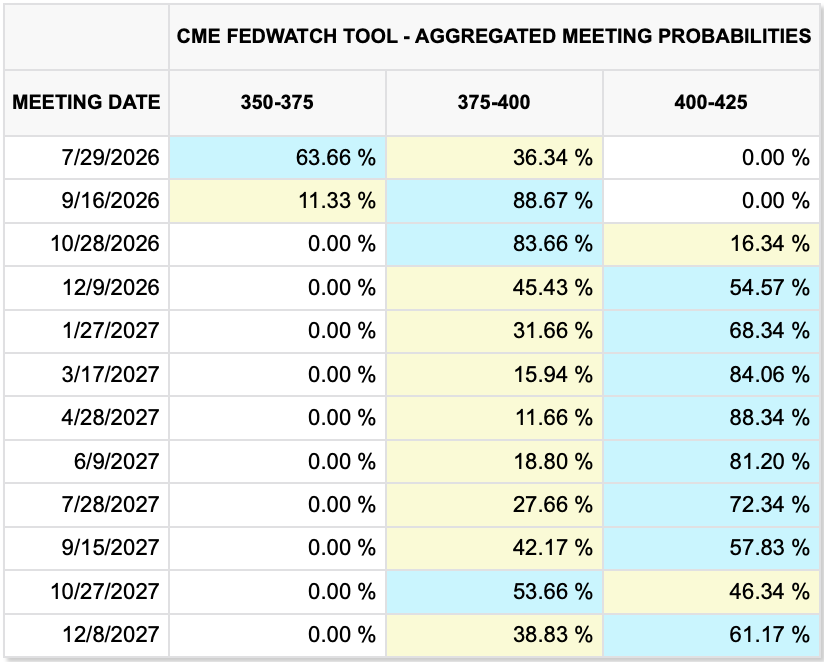

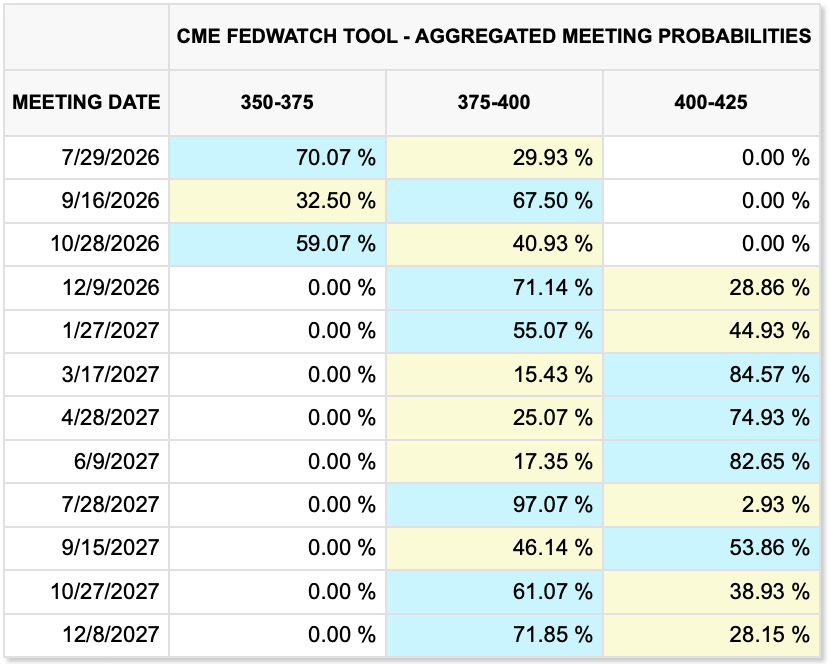

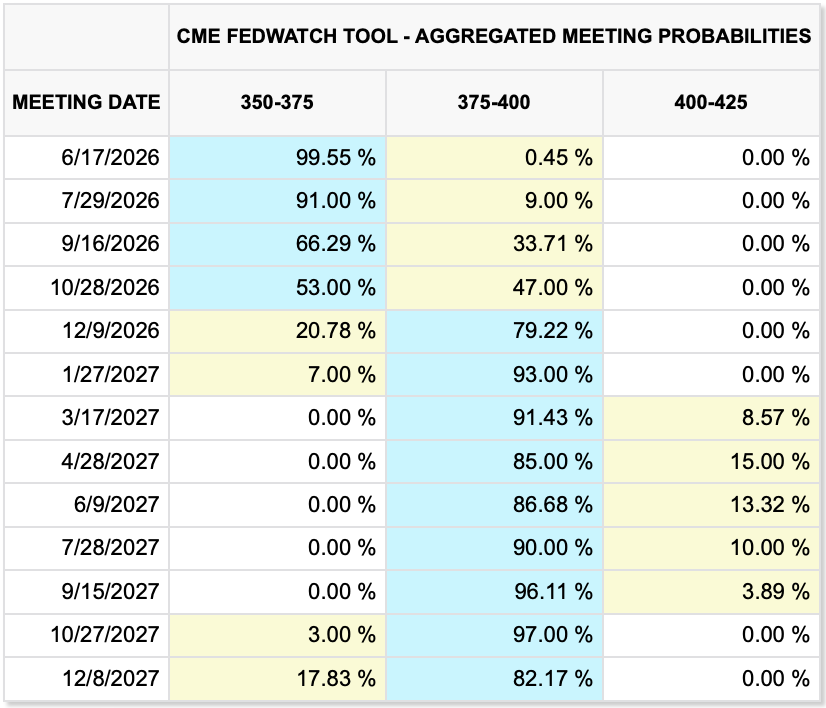

Here is a forecast I do not make lightly, Fed funds will finish the year lower than they are now, probably 3.25%-3.50%. And the current Fed funds futures market has bottomed (rates peaked) as per the CME table below.

As to the rest of the FX world, the dollar reigns supreme this morning as the euro (-0.3%) is below 1.1400 this morning, its weakest in more than a year as the Flash PMI data did it no favors, but the new hawkish Fed, higher US rates strong dollar narrative has been the driver. We have seen the same type of movement elsewhere, except where the dollar has moved further, with AUD (-0.8%) the worst performer in the G10 although HUF (-1.0%) is actually the biggest laggard. However, given the overall decline in commodity prices, those currencies that benefit from rising commodities are also under pressure (NOK (-0.7%, ZAR -0.5%, SEK -0.8%, MXN -0.7%) and we already discussed AUD.

Lastly, the metals markets are also under serious pressure with gold (-1.6%), silver (-4.5%) and copper (-3.3%) all tumbling on the same new view of higher rates and a stronger dollar. The thing about the commodities story is the fundamentals still seem positive to my eyes, and this seems like the last of the fluff getting taken out.

On the data front, Thursday’s PCE data is the big day and here’s what we have overall:

| Today | Flash Manufacturing PMI | 54.8 |

| Flash Services PMI | 51.0 | |

| Wednesday | New Home Sales | 640K |

| Thursday | Initial Claims | 225K |

| Continuing Claims | 1800K | |

| Q1 GDP Final | 1.6% | |

| Personal Income | 0.4% | |

| Personal Spending | 0.6% | |

| PCE | 0.5% (4.0% Y/Y) | |

| Core PCE | 0.3% (3.4% Y/Y) | |

| Durable Goods | -4.3% | |

| -ex Transport | 0.7% | |

| Friday | Michigan Sentiment | 50.3 |

Source: tradingeconomics.com

In addition to the data, we start to hear from some of the FOMC members, although I am confident Chairman Warsh won’t be out and about. Some analysts claim that Warsh’s view of less communication is going to weaken him as others will get to make their point and he won’t be able to counter it. But I think that Warsh has a plan, and if we continue to see oil prices decline, which seems the likely outcome, then all the inflation fears are going to dissipate and by the time the next meeting rolls around, it will be far harder to make the case that tighter policy is necessary. Historically, hiking into an energy price shock has been a central banking mistake, and I think Warsh knows this and is keen not to repeat it.

Net, for now, everybody loves the dollar and hates risk on this new hawkish Fed narrative. But going forward, I like the dollar on the back of a better economy and better investments and expect that the hawkish Fed narrative is going to fade away. But I’m just an FX poet.

Good luck

Adf

source: tradingeconomics.com

source: tradingeconomics.com