There once was a fire that ceased

Which many hoped would lead to peace

But recent attacks

On ships did climax

In poking the milit’ry beast

The market’s response was direct

With oil bears’ theses all wrecked

The dollar, it rose

While risk takers chose

Their stocks and bonds, now, to reject

While we had all become accustomed to the gradual decline in the price of oil as it appeared there was a solid chance that an agreement would be reached between Iran and the US, that all came a cropper yesterday after Iran attacked 3 different ships exiting the Strait and the US responded with attacks on more than 80 targets, including (according to the WSJ) “air-defense systems, command and control networks, antiship missile sites and more than 60 Iranian small boats near the waterway.” This was a significant uptick in the nature of the response from previous skirmishes and according to President Trump, the ceasefire is over.

“To me, I think it’s over, I don’t want to deal with them anymore,” Trump told reporters at a NATO summit in Ankara on Wednesday. “They’re liars, they’re cheats, they’re sick people.”

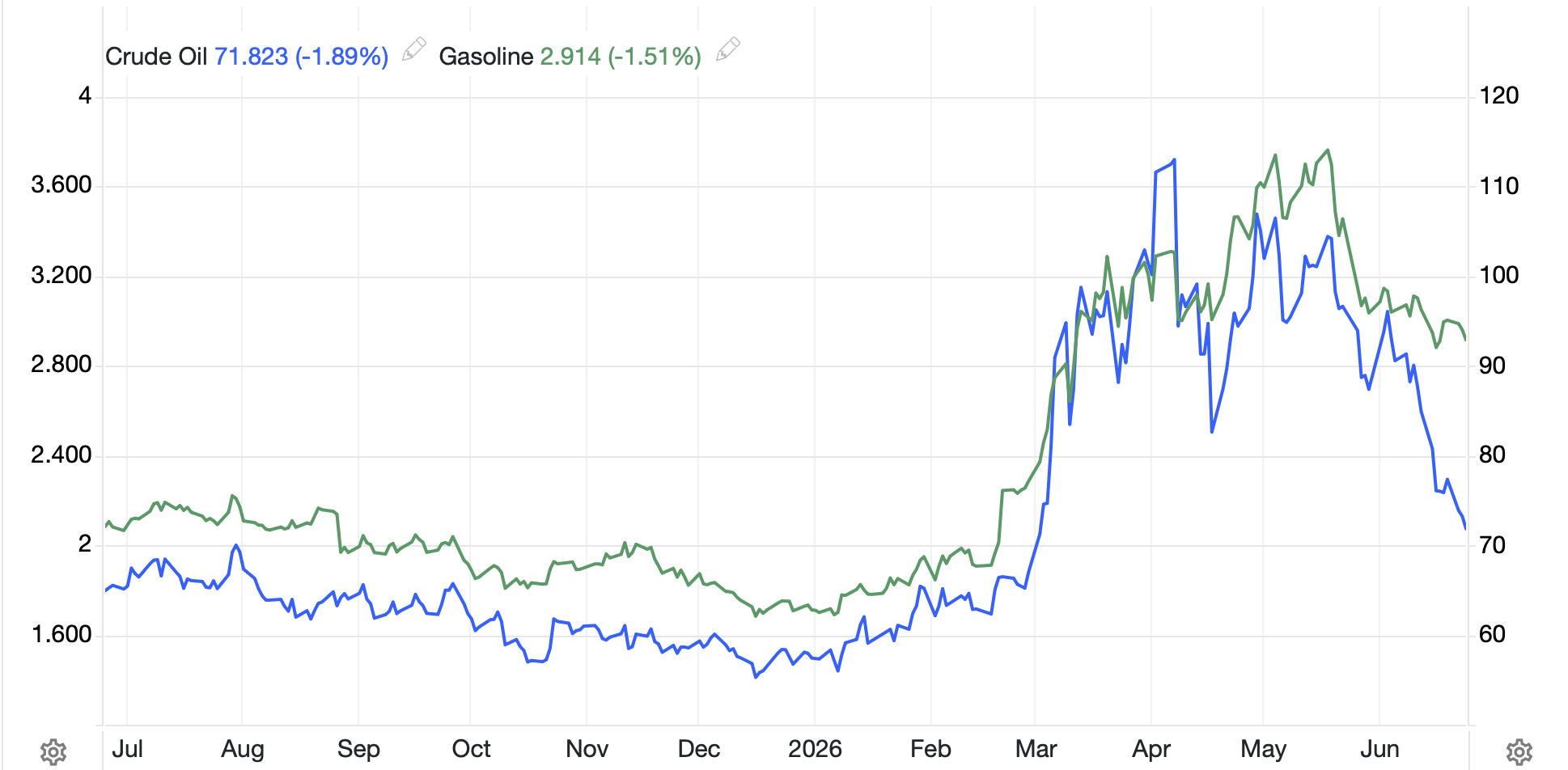

Given the sudden change in the status in the Gulf, we cannot be surprised by the market response. WTI (+6.0%) rocketed higher as you can see in the chart below.

Source: tradingeconomics.com

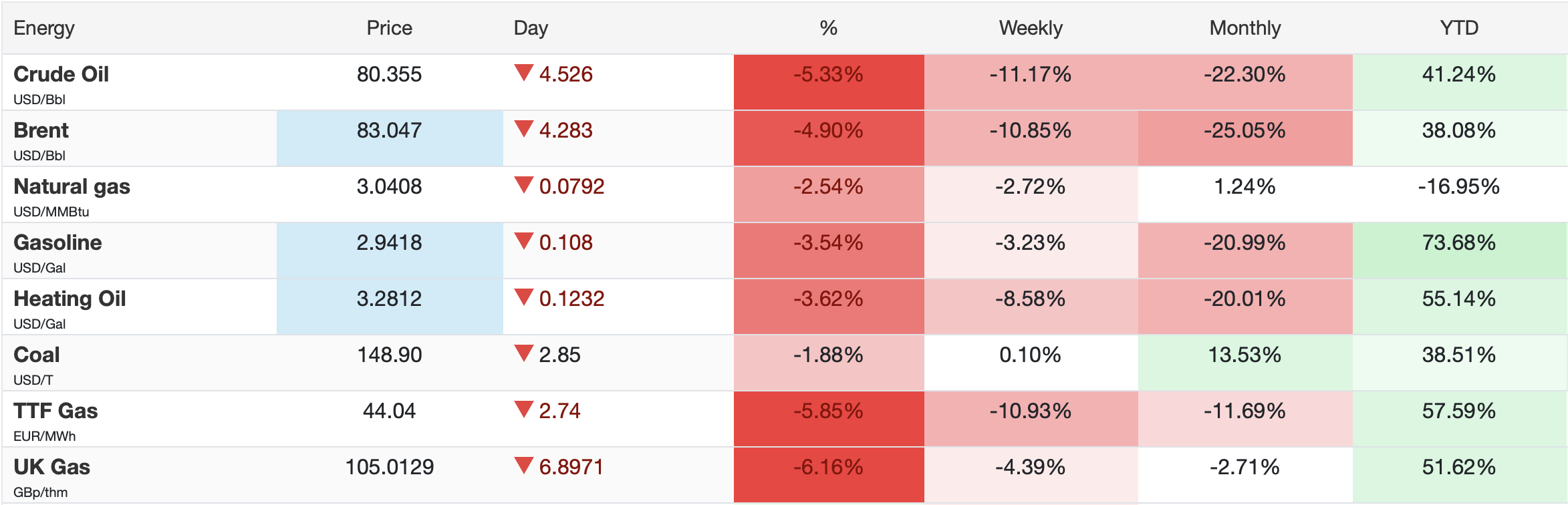

And while that is clearly a significant move, and has changed attitudes in the market, I think it is worth stepping back slightly and looking at the price action over the past month, just to remind ourselves that though things may be changing, we have still seen a dramatic decline in price.

Source: tradingeconomics.com

Here’s the thing, right now there is no way to know if we are going back to the situation in early March, where there was substantial fighting, or at least bombing and missile attacks, each day, or if this, too, is going to pass like the previous minor skirmishes. Certainly, President Trump appears tired of the current situation, but it is not clear what type of further response is in the offing.

In the meantime, given the new military action and the limited prognosis for a quick return to the previous status of ships moving through the Strait, it can be no surprise that investors decided to dump a lot of risk. So, let’s take a look at how things behaved overnight.

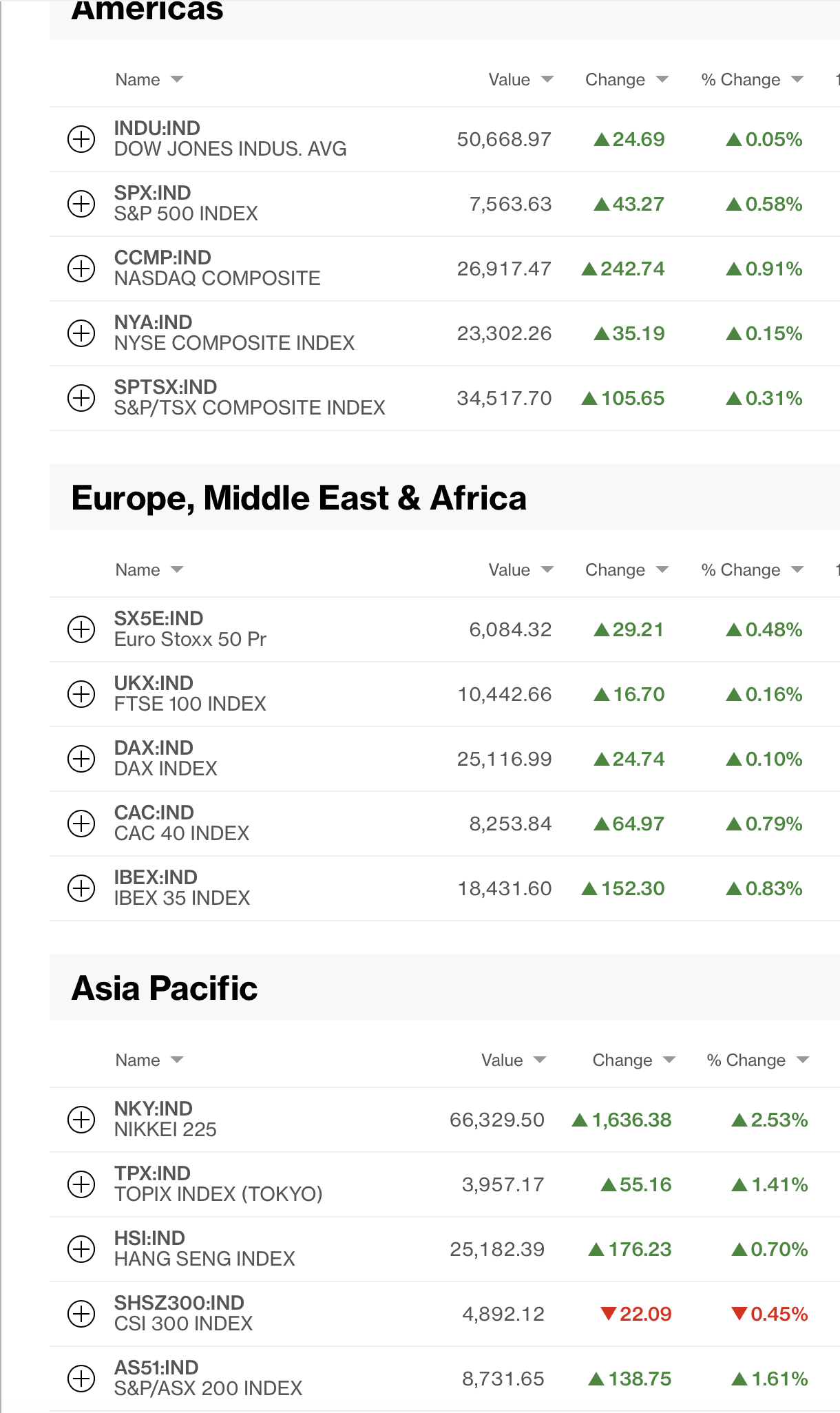

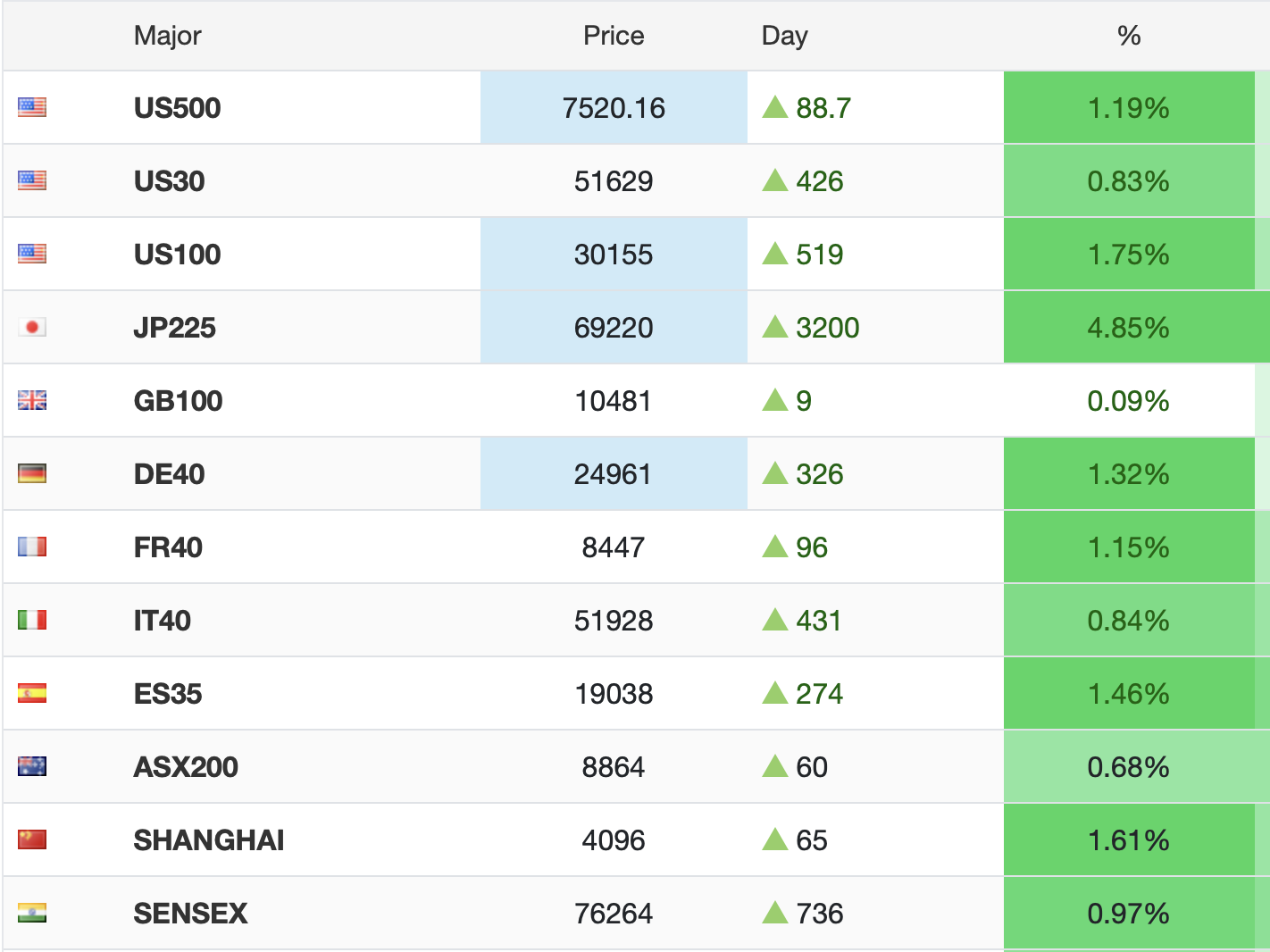

You will not be surprised that equity markets are broadly lower this morning. Yesterday’s US session was soft on concerns over the tech sector and that was before the resumption of hostilities in Iran. So, Tokyo (-2.1%), China (-0.8%), Korea (-5.4%) and India (-2.2%) all fell sharply amongst major markets in Asia with most of the smaller exchanges under pressure as well. The outliers here were HK (+3.0%) and Taiwan (+0.6%) as both saw continued demand for semiconductor and tech shares. It feels to me that these two markets will have difficulty maintaining this positivity under the current circumstances.

In Europe, it is a bloodbath with all major bourses lower led by Germany (-2.4%) and Spain (-2.7%) while France (-2.2% and the UK (-1.6%) are not far behind. The NATO meeting ongoing in Ankara is not helping anybody’s views as President Trump continues to add pressure to NATO to pay their own way. Ultimately, the NATO transition continues, and it is anybody’s guess as to how involved the US will be going forward. As to US futures, at this hour (6:35) all the major markets are lower by -1.0% or more.

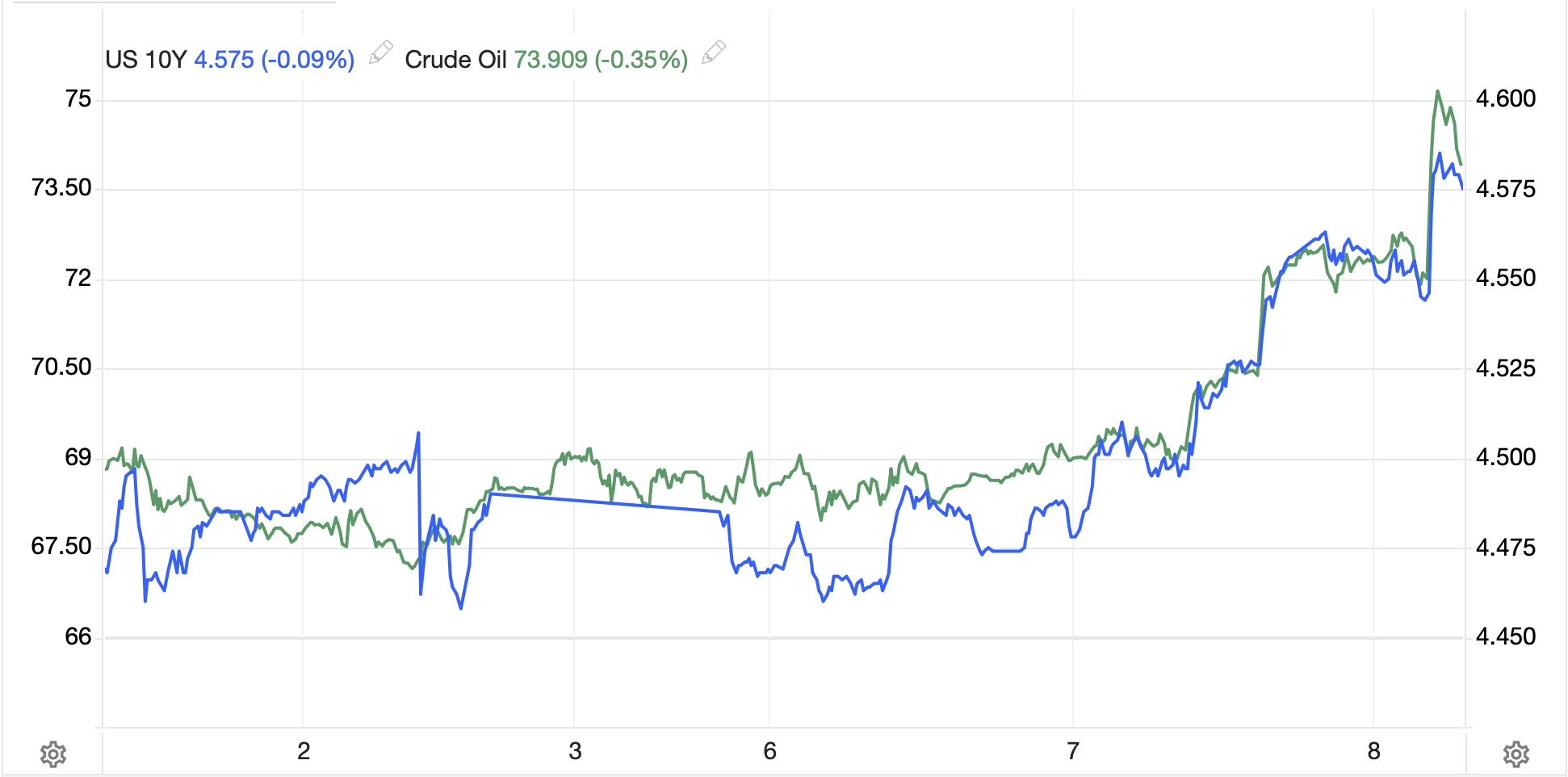

In the bond market, yesterday saw Treasury yields rise 6bps during the session as yields tracked the oil move pretty closely.

Source: tradingeconomics.com

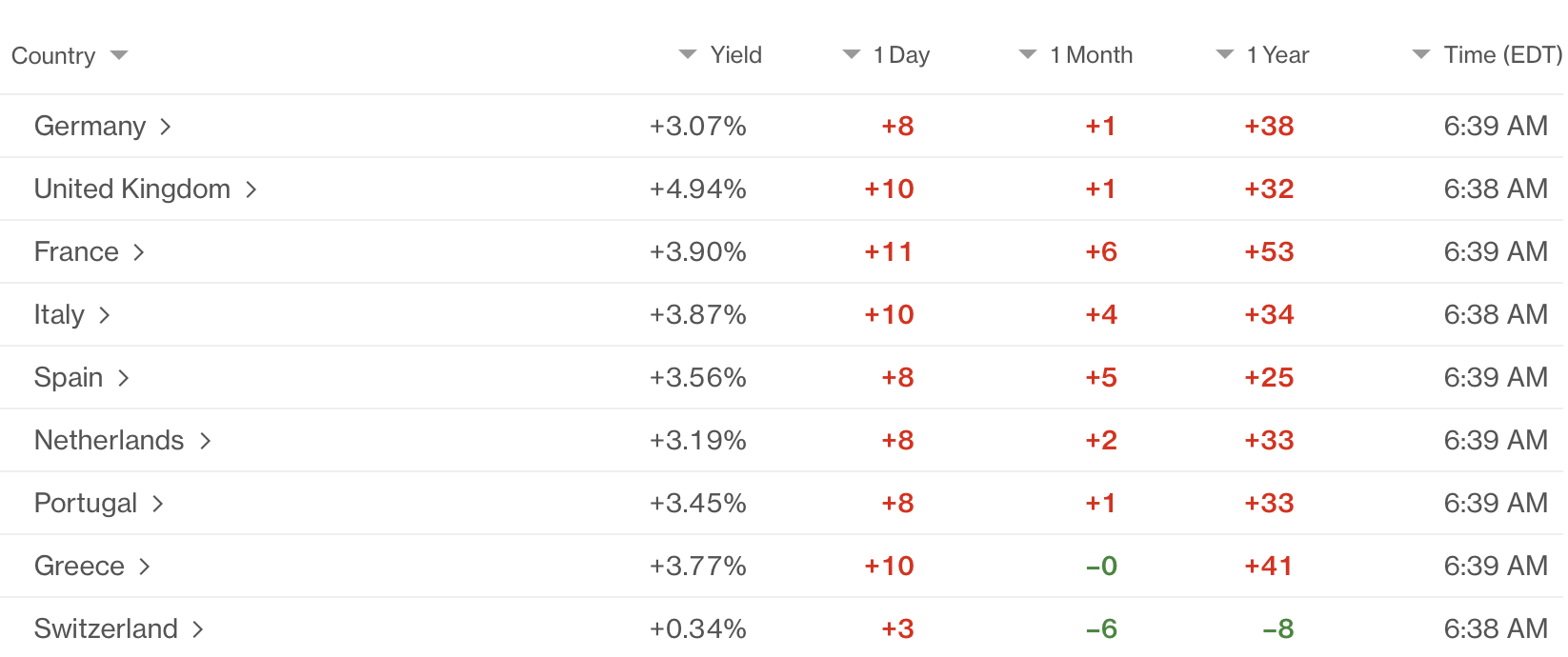

This morning, Treasury yields are higher by 2bps more but that is nothing compared to the European sovereign markets, which as you can see from the below Bloomberg.com screenshot are substantially higher this morning.

All those visions of inflation finally starting to decline were abruptly altered after the renewed activities in the Gulf. Adding to the pressure on bonds is the concern over the increased spending promises from governments around the world which has seen traders increase short positions in the bond market to near record levels.

We cannot be surprised that gold (-1.2%), silver (-2.2%) and copper (-2.2%) are lower in response to the renewed fighting and rise in oil prices as that relationship has been very consistent. We also cannot be surprised that the dollar is a bit firmer this morning, although not universally so. For instance, JPY (-0.2%) is now pushing back to its recent lows (dollar highs) although the pace of movement remains quite modest. As well ZAR (-0.6%) is also under pressure amid the decline in gold prices and rising oil prices (they are an importer of oil). On the flip side, though, NOK (+0.4%) is benefitting from oil’s rally as is CAD (+0.25%) while KRW (+0.6%) seems to be benefitting from money flowing home after the recent equity rout there (covering margin calls?). NZD (+0.4%) strengthened on the back of the RBNZ raising their base rate by 25bps as they continue to have some concern over inflation, but that only takes it back to 2.50%, hardly tight money. As to the other main currencies, they have not really done that much, although lean slightly lower this morning.

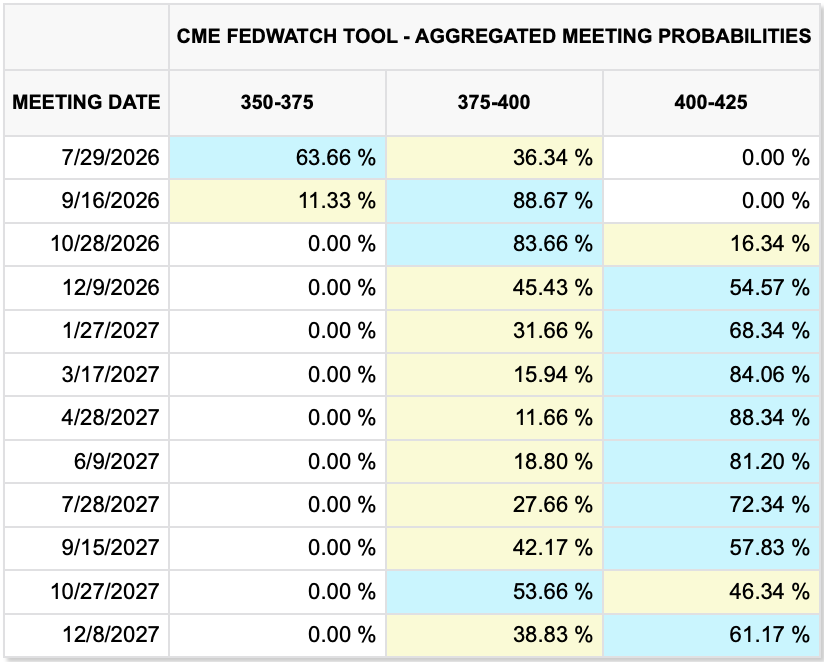

On the data front, we see the EIA oil inventory data with draws still expected, as well as a 10-year Treasury auction, where it will be quite interesting to see if investors are keen on the extra yield now available. And we get the FOMC Minutes, which despite the Iran situation, will still be keenly watched and read as the analyst community tries to get a better understanding of the way the Fed will be behaving going forward. What is the new reaction function?

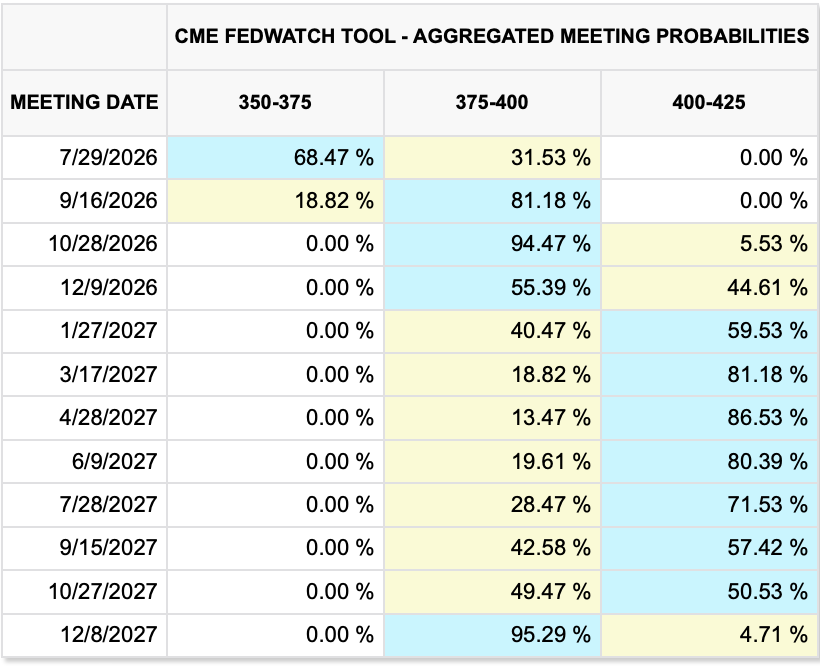

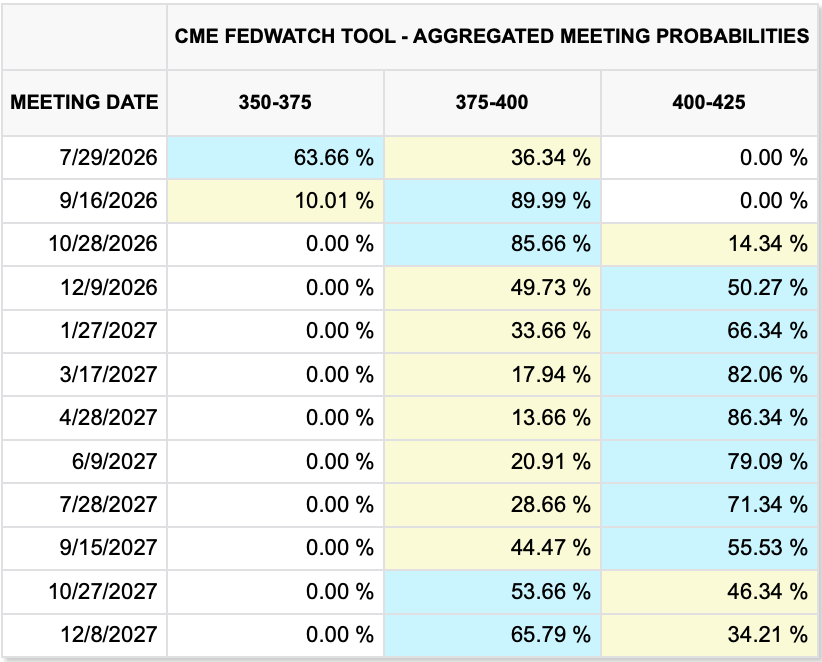

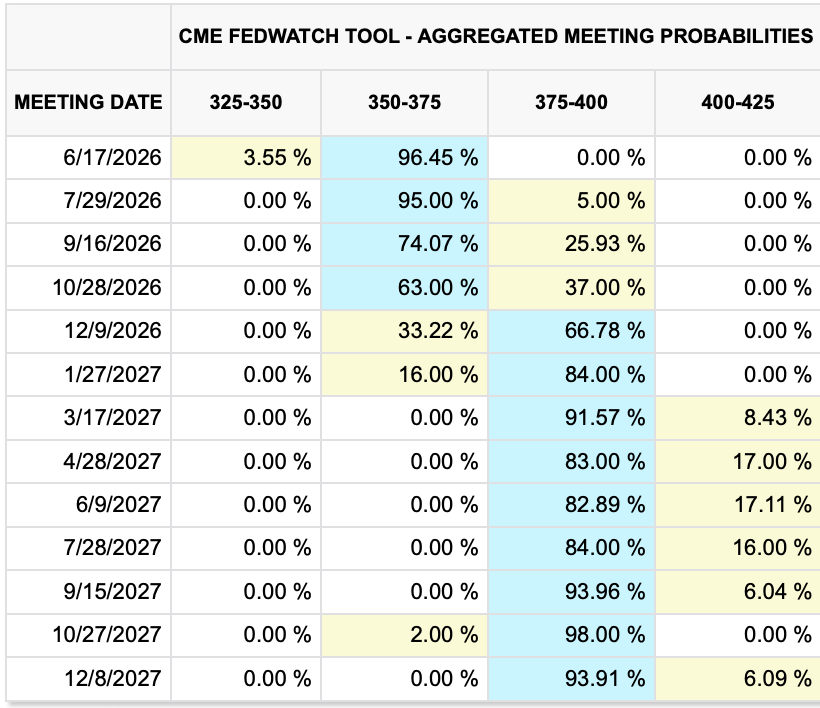

Looking at the Fed funds futures market, pricing for that first rate hike has moved to September from the previous October timeframe, and a second hike is back in the cards as well.

However, nothing has changed my view about the way things will evolve. Certainly, the increased hostilities are a negative for markets, but I suspect that this will be a short-lived episode and things will calm down again sooner rather than later. With that in mind, I have not changed my view about no rate hikes this year with a potential cut. However, if this fighting does increase and the oil price creeps higher over the next weeks and months, I will be rethinking this stance.

Right now, we are back to being hostage to events on the other side of the world. All we can do is watch and respond.

Good luck

Adf

source: tradingeconomics.com

source: tradingeconomics.com