The drumbeat grows louder each day

Catastrophe’s soon on its way

Yet markets ignore

The impact of war

On how things, in future, will play

Right now, Iran says they need U

Although one might ask what they’ll do

As well, on the Strait

They want a toll gate

Methinks this deal, Trump, will eschew

So, are oil tanks running dry?

Will phosphate’s price rise to the sky?

Will food soon run out?

Again, I’m in doubt

But pundits, good times, need deny

This is either setting up to be the greatest market pricing mistake of all time, or the global situation is not as bad as many pundits would have you believe. There are a bunch of very smart analysts out there who have great expertise in the commodity space, who have continuously explained that the closure of the Strait of Hormuz is setting the world up for catastrophe. Amongst them are Luke Gromen (@lukegromen), Craig Tindale (@ctindale), Adam Rozencwajg (from Goehring & Rozencwajg Associates) and Javier Blas from Bloomberg. I read all of them periodically as they have some excellent insights as to what is going on in commodity markets. And, to a man, they are all singing the same tune that even if the Strait were reopened tomorrow, the damage done is so great that we are heading into a major global economic recession.

Undoubtedly, all of them are smarter than me, a simple FX poet, and while I read a lot, market price action is far too important to ignore, especially as the current situation is not exactly hidden from traders and investors. Thus, at the end of the day, while I understand their thesis, market prices are telling a completely different story. Oil and gas production is growing elsewhere in the world and deals are being signed all over the world for new opportunities (Alaska, Brazil, Guyana, Venezuela). The oil market remains in a steep backwardation which is another sign that markets are not overly concerned about the future. I’m sorry, I cannot get worked up about this stuff without some clearer price signals, perhaps WTI at $150/bbl or something like that.

As to the Iran news, it is impossible to tell truth from fiction regarding the negotiations as it remains unclear, who in Iran is negotiating and what power they have. The uranium issue remains key, in my mind, as a nuclear weapon cannot be considered defensive, and given their stated goals of destroying the great Satans of Israel and the United States, I very much fear if they were to create one, they would launch it the next day. Even Xi agreed they cannot get one.

All this leads me to believe that there is still quite a bit more back and forth before things end, and if I had to pick a date, I am still in for July 4th as a time to announce an agreement. We shall see.

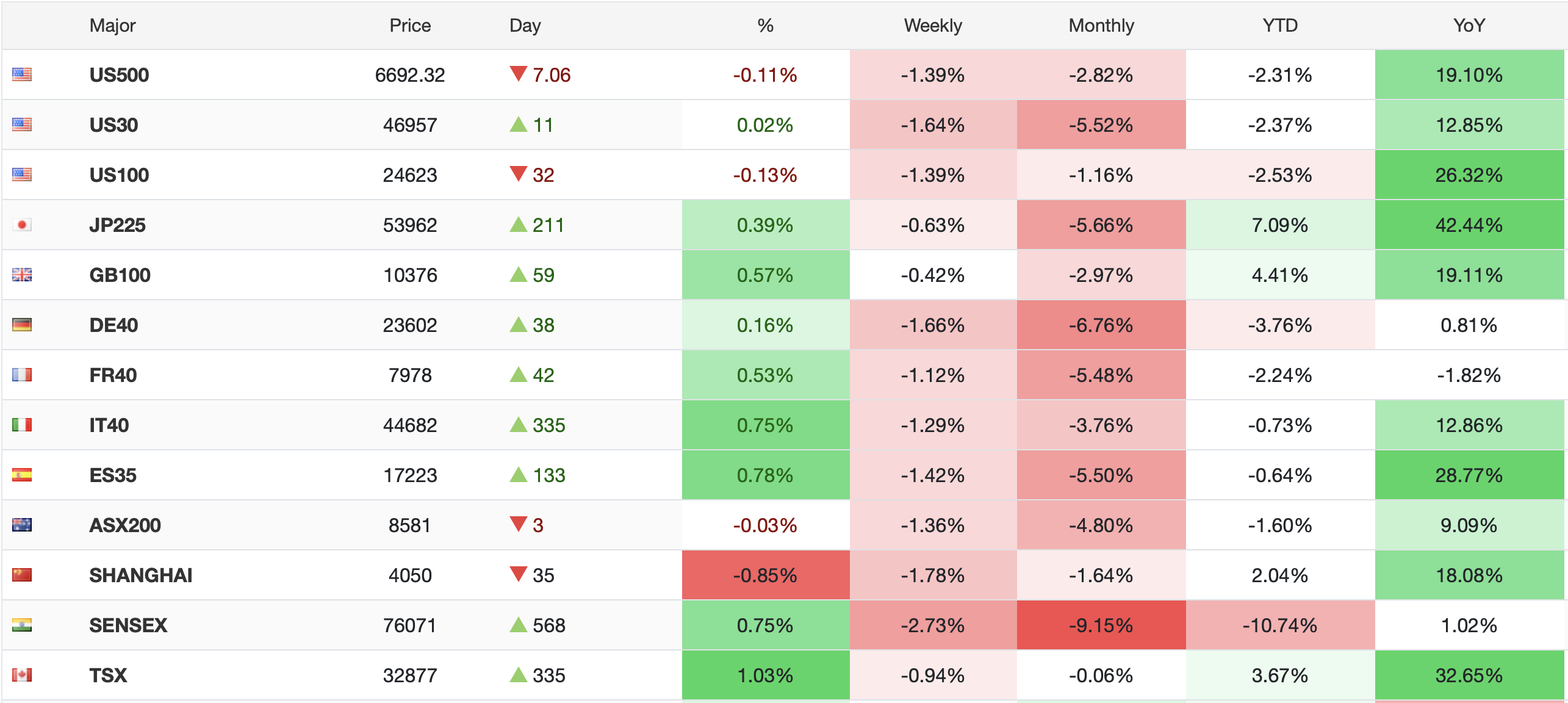

So, given we are not going to solve the Iran conflict here, it’s time to observe how markets are behaving. And frankly, there is not very much to observe. Starting with equity markets, as you can see from the Bloomberg screenshot below, things look pretty good right now, regardless of the Iran situation. Yesterday’s US rally (the concerns raised regarding Iran and its uranium were set aside, it seems) were followed by strength in Asia and this morning in Europe.

Earnings data continues to be released in a generally positive manner, and despite the ongoing angst amongst the punditry, as discussed above, there is, as yet, no sign that fear is growing amongst the investing set. Below is a chart of the CNN Fear and Greed Index over the past year. the current reading is 57, firmly in the Greed bucket and as you can see, the fear over the war began to dissipate at the end of March.

If you think about it, this is really no different than the Ukraine War, which for a relatively short time was seen as catastrophic, and eventually faded into the background. Honestly, when was the last time you saw an article on the subject?

As to the bond market, it continues its recent uncertainty as to what the future holds. This morning yields are lower across the board with Treasuries (-2bps) after slipping -3bps yesterday, while European sovereign yields are all lower by between -4bps and -6bps. The bond market appears to be caught between fears of rising inflation because of the impact of higher oil prices, not only on direct things like transportation, but also secondary impacts as those costs are passed on and adding in the potential for higher food prices if the fertilizer situation is as bad as some forecast. However, the other side of that coin is the potential for a significant recession, which historically has resulted in substantially lower yields as governments around the world add both monetary and fiscal stimulus. Place your bets!

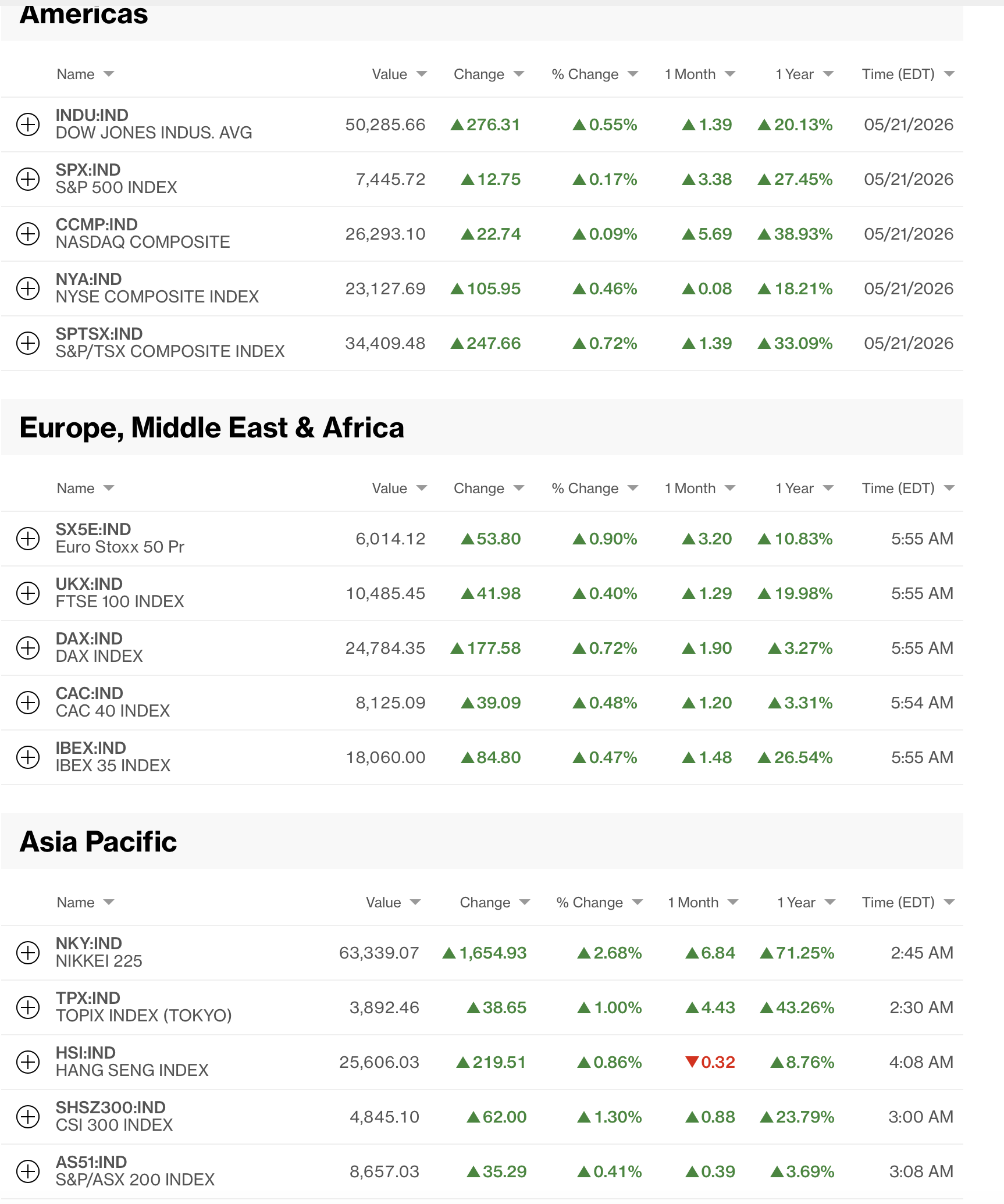

Turning to the oil market, while WTI is higher by 1.8% this morning, as you can see in the chart below, it continues to go nowhere overall. If the apocalypse is coming, the market is certainly not ready. Either that, or there is a lot more oil around than people give it credit for.

Source: tradingeconomics.com

Of course, as has been the case, when oil’s price rises, gold (-0.6%) and silver (-1.1%) slide as that negative correlation has become firmly entrenched. Copper (+0.7%) though, is bucking that trend this morning, albeit hardly running away. I expect that these relationships are likely to hold until there is a resolution of some sort in the Gulf.

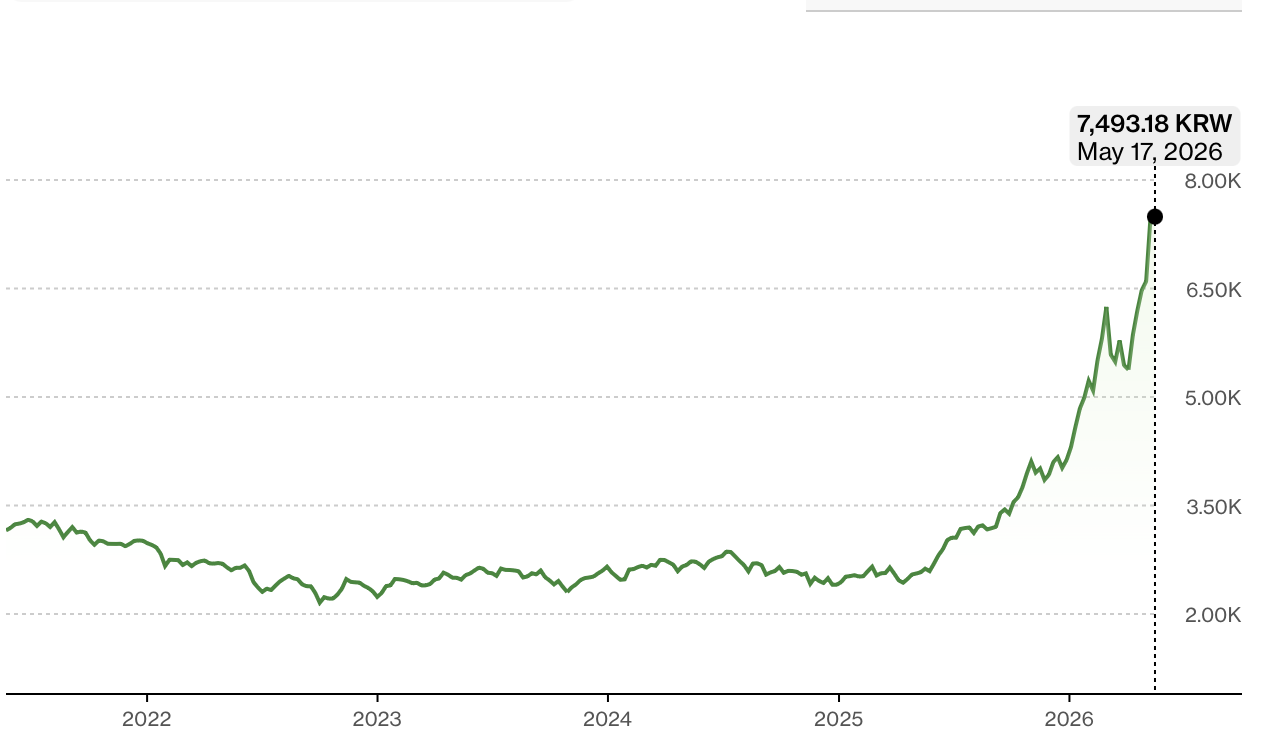

Finally, the dollar is generally firmer this morning despite the decline in yields. In fact, if we look across markets, bonds are today’s outlier. But back to FX, in the G10, all the currencies are weaker by between -0.1% and -0.3% although in the EMG bloc, there are two more substantial movers, INR (+0.5%) as the RBI continues its intervention process amid fears the rupee will collapse, while KRW (-0.8%) continues to see foreign outflows despite its equity market continuing to be one of the best performing in the world as you can see in the Bloomberg chart of the KOSPI below.

And that’s really it as we head into the weekend. Perhaps the conflict will heat up during the long weekend, which would likely drive some real movement. But for now, there is nothing new under the sun.

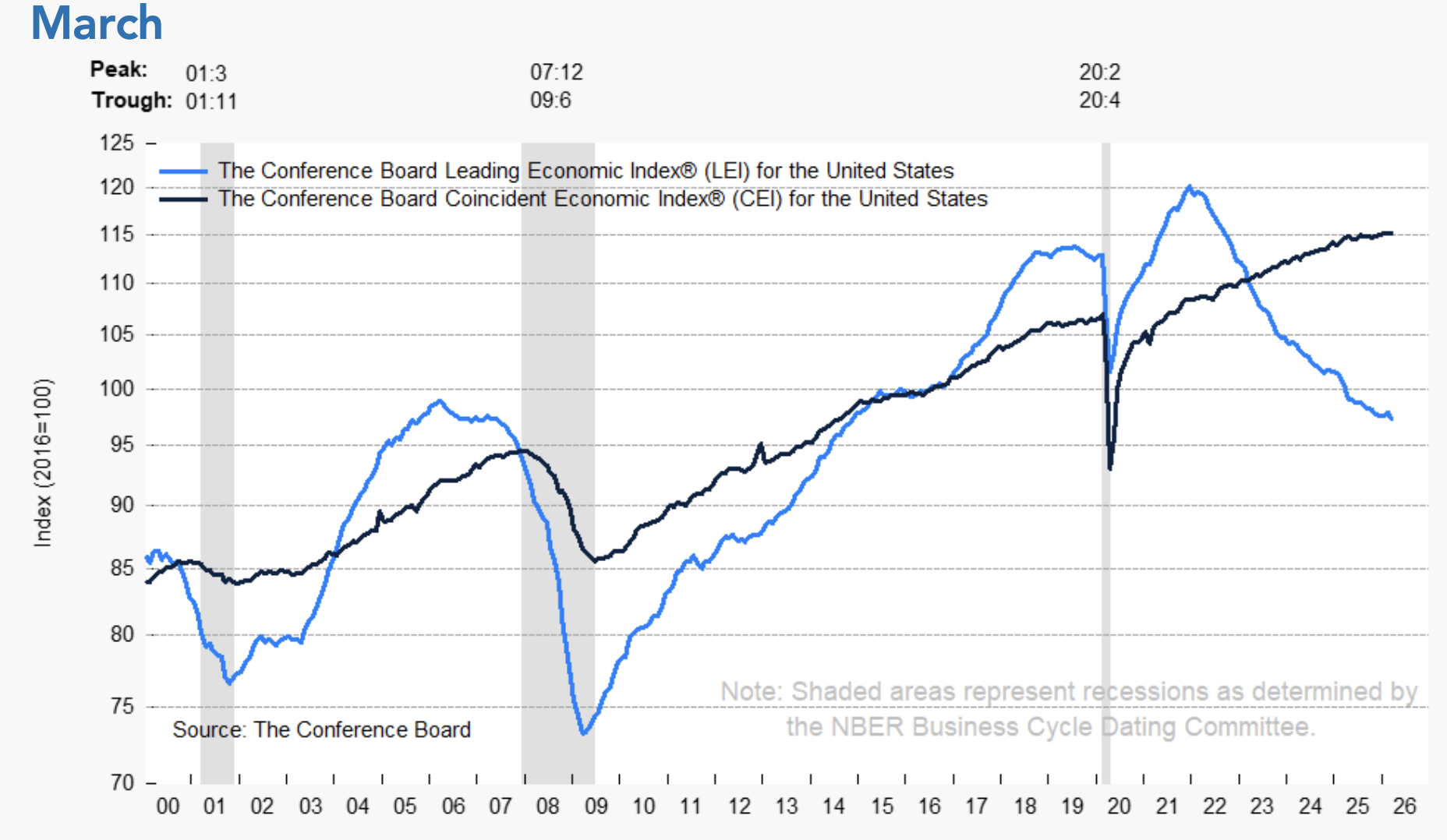

On the data front, yesterday saw generally solid data with the Philly Fed the lone, weak, exception. Last night, Japanese CPI was released at a much lower than expected 1.4% for both headline and core. While there is still a strong expectation that the BOJ is going to raise rates next month, if inflation is truly at 1.4%, that seems like it might be a mistake. This morning we see Michigan Sentiment (exp 48.2) and Leading Indicators (-0.2%). Here’s the thing about the Leading Indicators, though, as you can see from the chart below from the Conference Board’s website, it appears they may not be telling us the whole story anymore.

After all, they have been declining steadily since early 2022 despite an economy that has grown solidly during that period. Again, maybe this truly is a harbinger for the future, but I am not convinced.

And that’s all there is. Have a wonderful Memorial Day weekend and let’s see what the world looks like on Tuesday morning!

Good luck and good weekend

Adf