The Payrolls report was a mess

But job losses added no stress

And so, once again

We’re back to the yen

As reason for doomsters to press

The claims being made are dramatic

Describing T-bonds as asthmatic

Explaining that Scott

Has now lost the plot

While calling his viewpoint erratic

So, what’s really happening here?

Is it true the end point is near?

I’m happy to say

Those fears I’d allay

At least through the end of next year

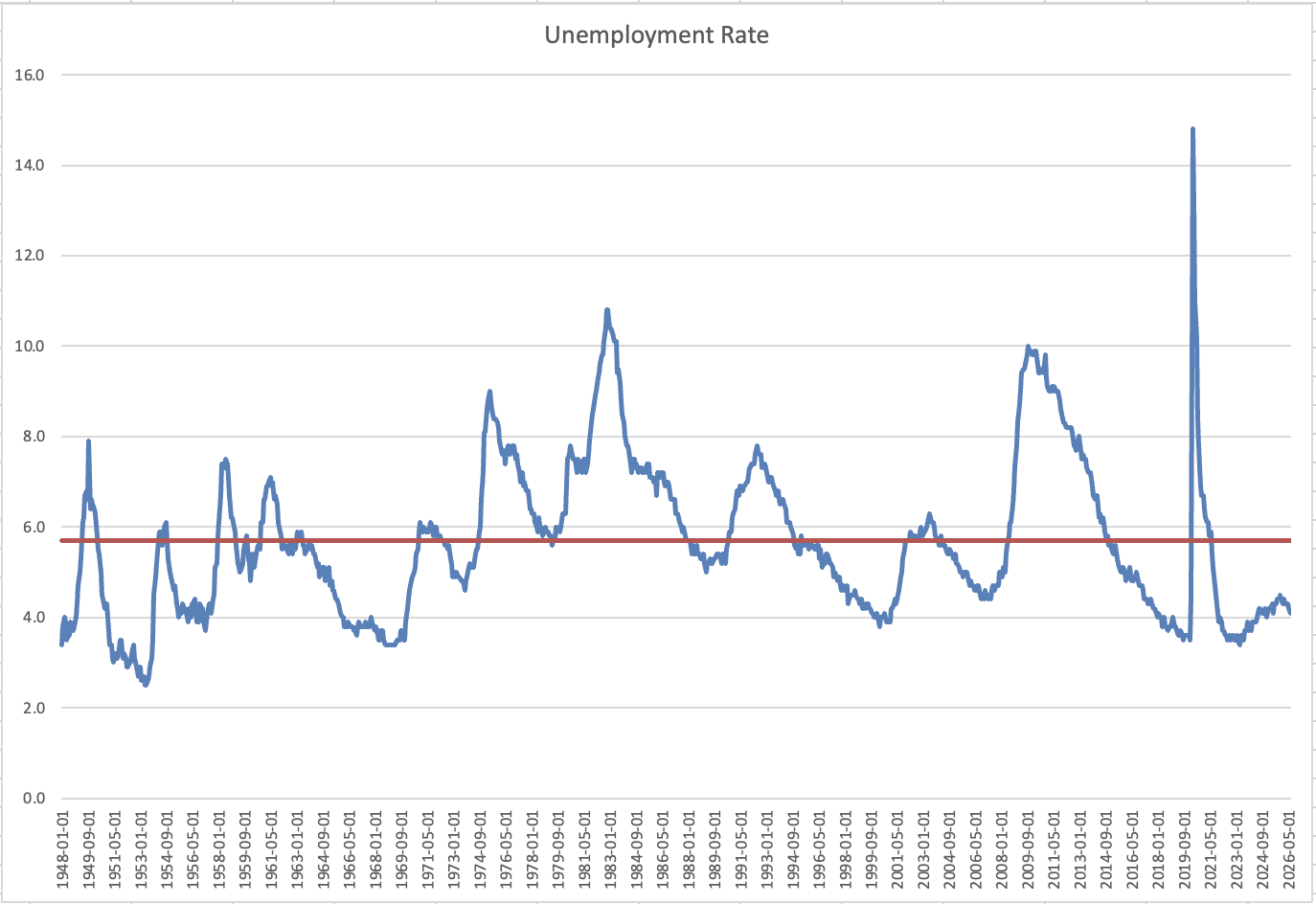

Once upon a time, a very smart economist, Larry Kantor, explained to me that the best signal for the economy to follow over time was the Unemployment Rate. When it was falling, it was a strong indication that economic activity was increasing and vice versa. But I think that is a world which no longer exists. I make that point because Friday’s NFP report showed that the Unemployment Rate fell to 4.1% despite the fact the payrolls shrank. Below is a chart of the Unemployment Rate since 1947 along with the average (5.7%) during that period. The data comes from FRED although I calculated the average

Arguably, the first thing you notice is that the current Unemployment Rate is quite low relative to history, in fact it is in the bottom quintile. But Mr Kantor’s observation was based on the then prevailing, and historical thesis of steady population growth, a thesis that has been called into question lately. Between the aging of the population and the significant changes in immigration activity (i.e. the 2 million or so deportations recently), it is not clear that a declining Unemployment Rate is indicative of strong economic activity. It could simply be a signal that the population is falling more quickly than job growth.

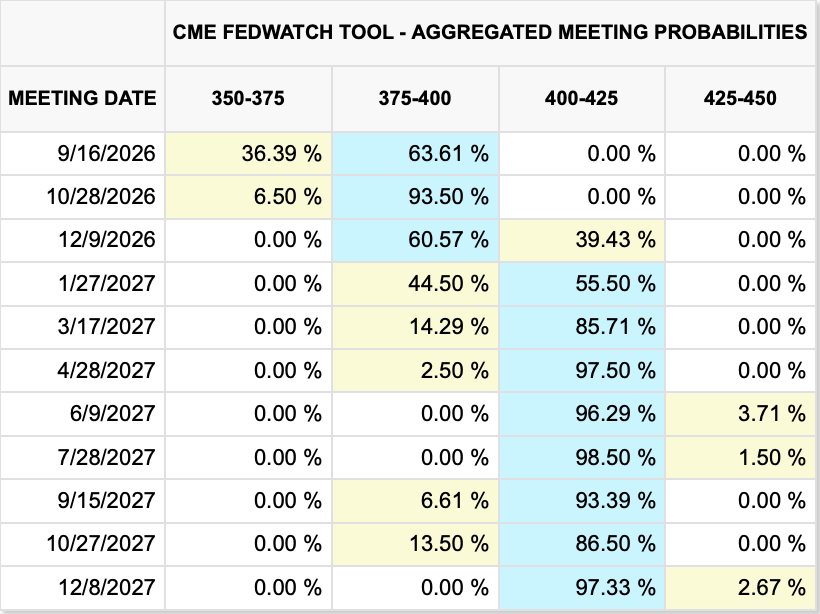

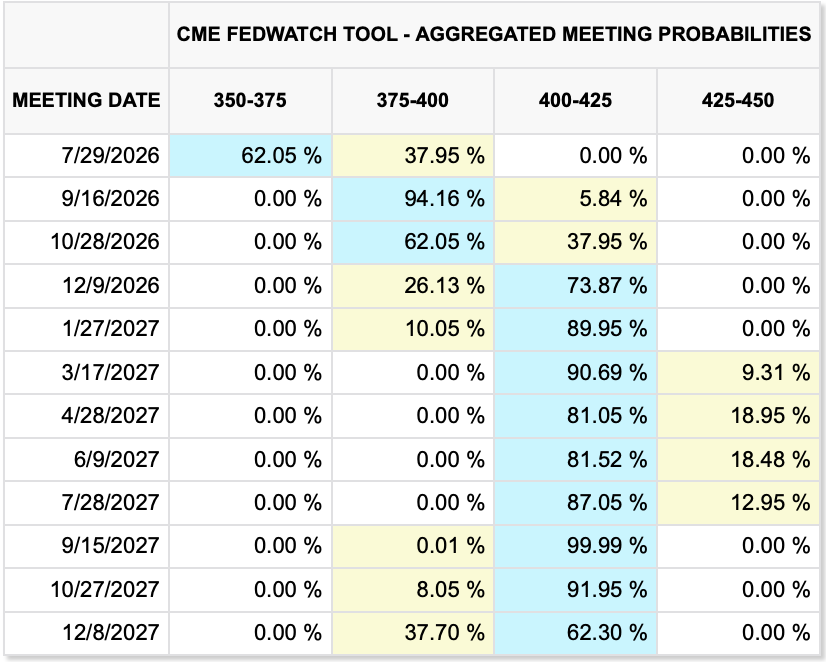

But looking at the report as a whole, it was quite confusing. While Payrolls decline by -23K, Private Payrolls rose 30K and Manufacturing Payrolls rose 5k. A shrinkage in government jobs seems quite positive to me. However, Earnings data was a bit soft falling to 3.2% Y/Y, lower than the inflation rate. Net, it is hard to draw many conclusions from the report although we did see the Fed fund futures market reduce the probability of a September hike to 56% from 66% prior. Certainly, on the surface it hardly strikes that this is encouraging a rate hike. And the stock market was non-plussed, rallying across the board.

Which takes us to the other story that continues to garner huge amounts of attention, the yen and the rationale behind the US joining Japan to intervene as well as what that will mean going forward.

I will try to boil this down. The angst is attached to the carry trade, which, neatly defined, is borrowing JPY and paying a very low interest rate, converting the yen into another currency, typically USD, although AUD, MXN and BRL are also popular, and then earning the higher interest rate in those currencies. It can be a highly profitable trade when currency volatility is low as the trader simply earns the difference between the interest rates each day. The risk is there is a sudden move in the FX rate which can wipe out weeks or months of carry. Hence the concern over intervention when we see the FX rate move 5% in a day like the end of July.

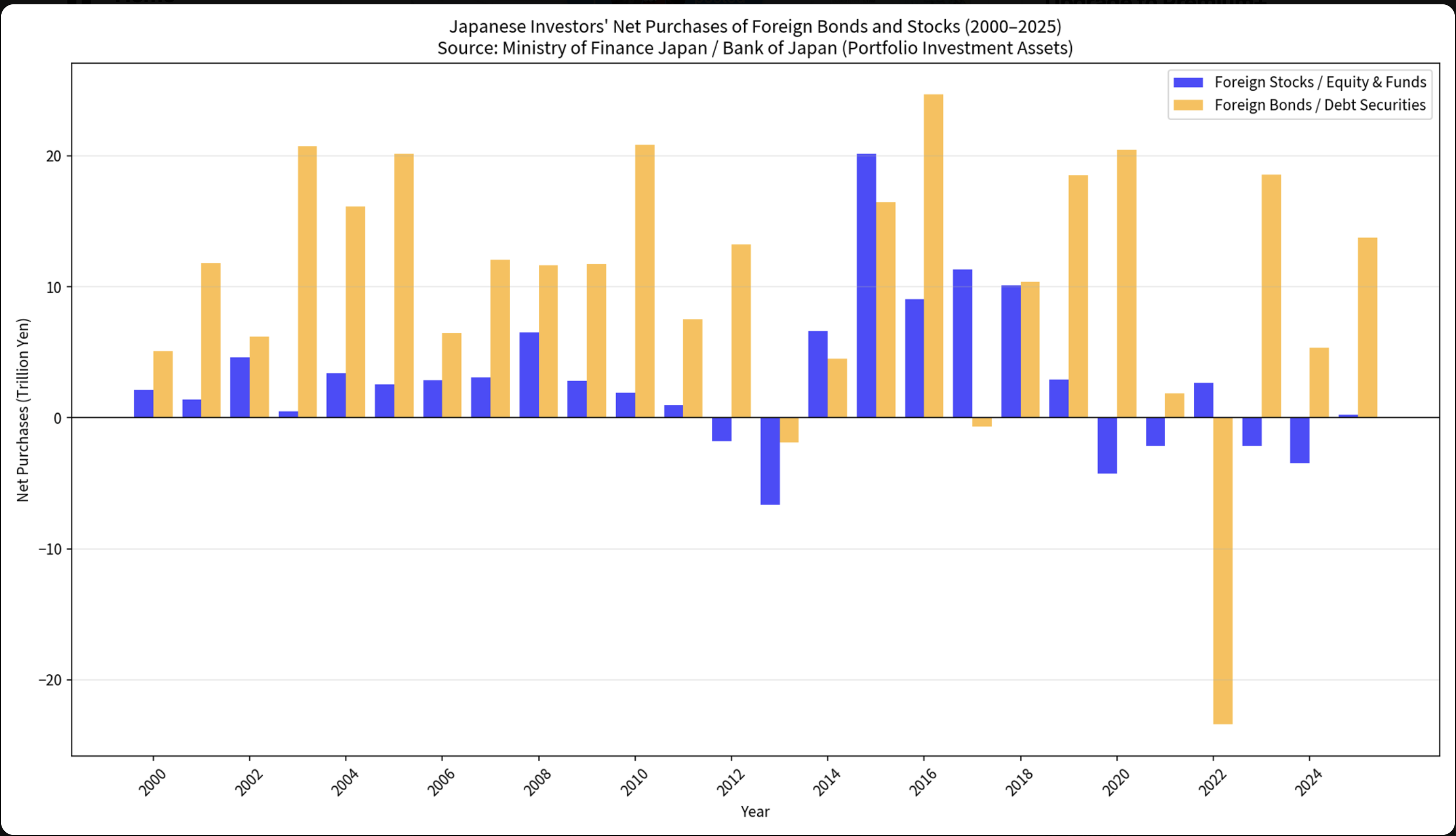

Estimates of its size run from $500 billion to $1.5 trillion, although nobody really knows. I would err on the high side. But there is another piece that is rarely discussed but I think must be considered in this conversation, and that is the outward investment flows from Japanese investors around the world, again largely to the US, but elsewhere as well. I asked Grok to create a chart of net investment outflows from Japan from 2000 to present and got this:

Other than 2022, when the Fed started hiking rates aggressively and bond prices fell sharply, it has been pretty consistent. The net amount of outflow over this time period is approximately ¥347.5 Trillion (again according to Grok) which at the average FX rate over the period of 112.40 works out to about $3.1 Trillion, arguably much more than the ‘pure’ carry trade. But I don’t believe you can ignore that as if the Japanese are going to bring money home, it will be there as well.

Of course, there is no indication that is what they are doing at this point, despite all the hypotheticals about that being the major risk. The Fiscal situation in both the US and Japan is awful, with both nations running huge budget deficits and showing no signs of changing that. Inflation has been rising in both nations and a key prescription by many is that both central banks should be raising interest rates. Of course, if the Fed raises and the BOJ waits, that widens the differential and will theoretically put more pressure on the yen.

The key concern and the favored story as to why the US helped Japan is that they didn’t want the BOJ to have to sell Treasuries to fund their USD sales. Much has been made of the fact that the US sold EUR, not USD, but that is because the Treasury doesn’t keep USD in the Exchange Stabilization Fund, just EUR and JPY and a bit of some others like GBP, so they sold what they had.

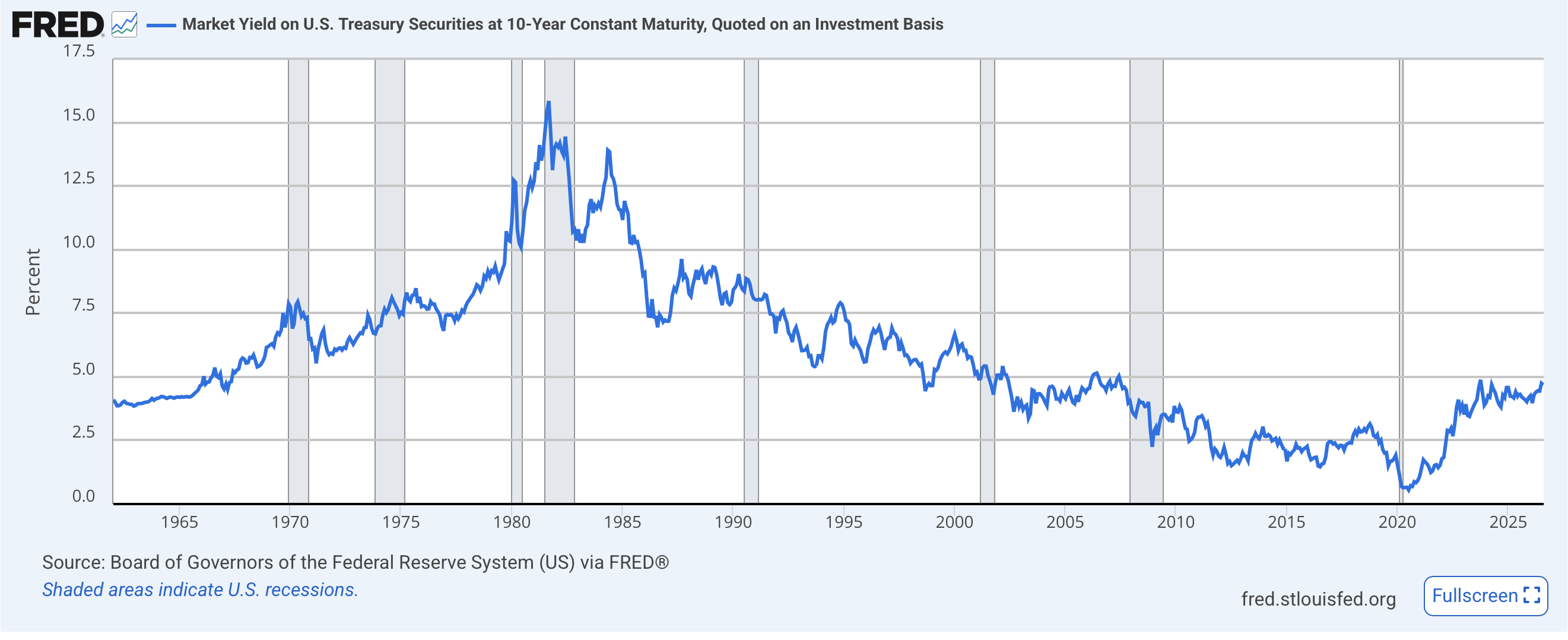

The big fear is that the US cannot afford for Treasury yields to go higher (although it seems these same folks are clamoring for the Fed to hike rates) and so will do all they can to prevent that. Now, the funny thing is that if you are Japanese and you own USD assets, you are thrilled with the weak yen as it enhances your return. While Takaichi-san doesn’t like the weak yen as it exacerbates inflation, I don’t think Japan’s asset holders are clamoring for a strong yen. Remember this, too, that the long-term average yield on US 10-year Treasuries is 5.81%, more than 100bps above where we are today. It is fair to say that recent lower yields are the exception, not the rule.

To my eye, the harder needle to thread in this process is for Japan, which really doesn’t want to see its massive foreign investment decline in value, although they are concerned about inflation. For the US, while the fiscal situation is a major problem, it remains a problem for the future. I’m pretty confident everybody in the world will still accept dollars for payment if they are offered. The dollar is not going to collapse, nor is the bond market. While pressure continues to build over time, it is going to take a LONG time. Mark my words. The end is not nigh!

In the meantime, JPY (-0.7%) looks like it is repeating the pattern after the last intervention attempts as per the below chart. As I have maintained, unless there are policy changes, a strong yen is not coming soon.

Source: tradingeconomics.com

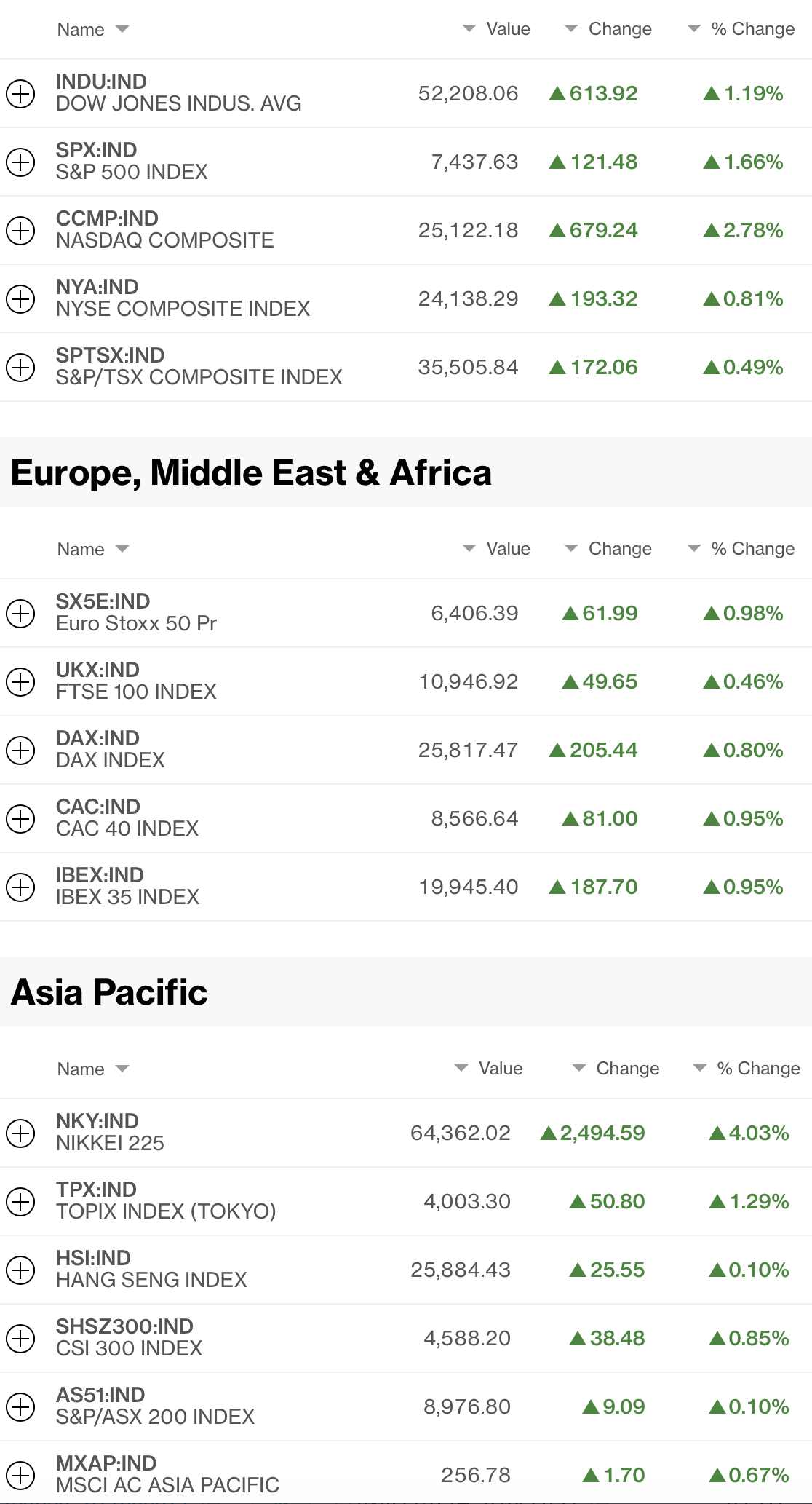

Speaking of the FX market writ large, this morning has seen very little net movement across almost all counterparts with KRW (-0.7%) the only other currency moving more than 0.1% in either direction. We have discussed the won several times recently and while the alleged proximate cause for this decline is increased uncertainty over the Strait of Hormuz, given the huge gains seen in the past 6 weeks, this is nothing more than a blip in a strong trend.

In fact, lack of movement aptly describes the bond market as well with yields on Treasuries and across all European sovereigns within 1bp of Friday’s closing levels. Apparently, fears of the apocalypse have been put on hold for the moment.

In the equity market, Friday’s US rally has seen a general follow-on by both Asia and Europe. Overnight saw modest gains in almost every Asian market (Tokyo +2.1%, China +0.2%, HK +1.1%, Korea +0.7%, Taiwan +1.6%, etc.) although Australia (-0.3%) managed to buck the trend. Given the resource focus of the Australian economy, and the recent gains in metals prices, that is a bit of a surprise. As to Europe, Germany (+0.4%) is the leader of the pack with both France and Spain basically unchanged while the UK (-0.3%) lags slightly, albeit lacking any new news. US futures are essentially unchanged at this hour (6:45).

Finally, oil prices (+1.4%) are firmer this morning as the ongoing saga over the Strait remains cluttered with confusion as to if a deal is coming close, or not and what role, if any, the US is going to play. Personally, I’m ready for the US to exit the area, but they don’t ask me. As to the metals markets, gold (-0.1%) is consolidating after a very strong performance last week, rising 7%, and silver (+0.8%) is continuing last week’s gains. But to me, copper (+0.5%) is the metal with the most upside as the supply/demand characteristics of the market, (not enough is mined to satisfy annual needs and the timeline to bring a new mine up to speed exceeds a decade), imply higher prices still despite the fact we are already at record levels.

And that’s all. We have no data today although CPI comes Wednesday. I will look at data tomorrow as I have already gone too long this morning.

Good luck

Adf