At first, it was open then not

As small boats attacked and were shot

But now, all eyes turn

To what we will learn

From Payrolls and if things are hot

While yesterday saw risk reduced

This morning stock futures are juiced

So, as we await

More news from the Strait

We’re hoping Jobs give things a boost

The top story was the minor skirmish in the Strait of Hormuz when three US destroyers transited the Strait and escorted one or two ships trapped in the Persian Gulf out. Iranian small boats attacked and were sunk, but missiles were fired and it seems they hit a Chinese tanker. I’m guessing President Xi is none too pleased with that outcome. In the end though, while oil (-0.2%) traded higher through most of yesterday, as you can see in the chart below, it subsequently faded back from its highest levels of the day and remains well below $100/bbl as I type.

Source: tradingeconomics.com

In the end, the major market themes and correlations continue to play out with oil the primary driver and other markets responding either in sync (the dollar and bond yields) or in opposition (stocks and precious metals). I imagine we are going to see this continue to play out until such time as an agreement is definitively reached to end all the hostilities there, whether that is by signing an accord or the complete destruction of the IRGC leadership.

Which means, we need to turn elsewhere for our news and happily, we have the payroll report to observe this morning. Leading into this report, we saw the ADP number on Wednesday print at a better-than-expected 109K, while Initial and Continuing Claims yesterday both printed at lower than forecast numbers, indicating that the labor market is in pretty good shape. With that in mind, here are this morning’s expectations:

| Nonfarm Payrolls | 62K |

| Private payrolls | 75K |

| Manufacturing Payrolls | 5K |

| Unemployment Rate | 4.3% |

| Average Hourly Earnings | 0.3% (3.8% Y/Y) |

| Average Weekly Hours | 34.2 |

| Participation Rate | 61.7% |

| Michigan Sentiment | 49.5 |

Source: tradingeconomics.com

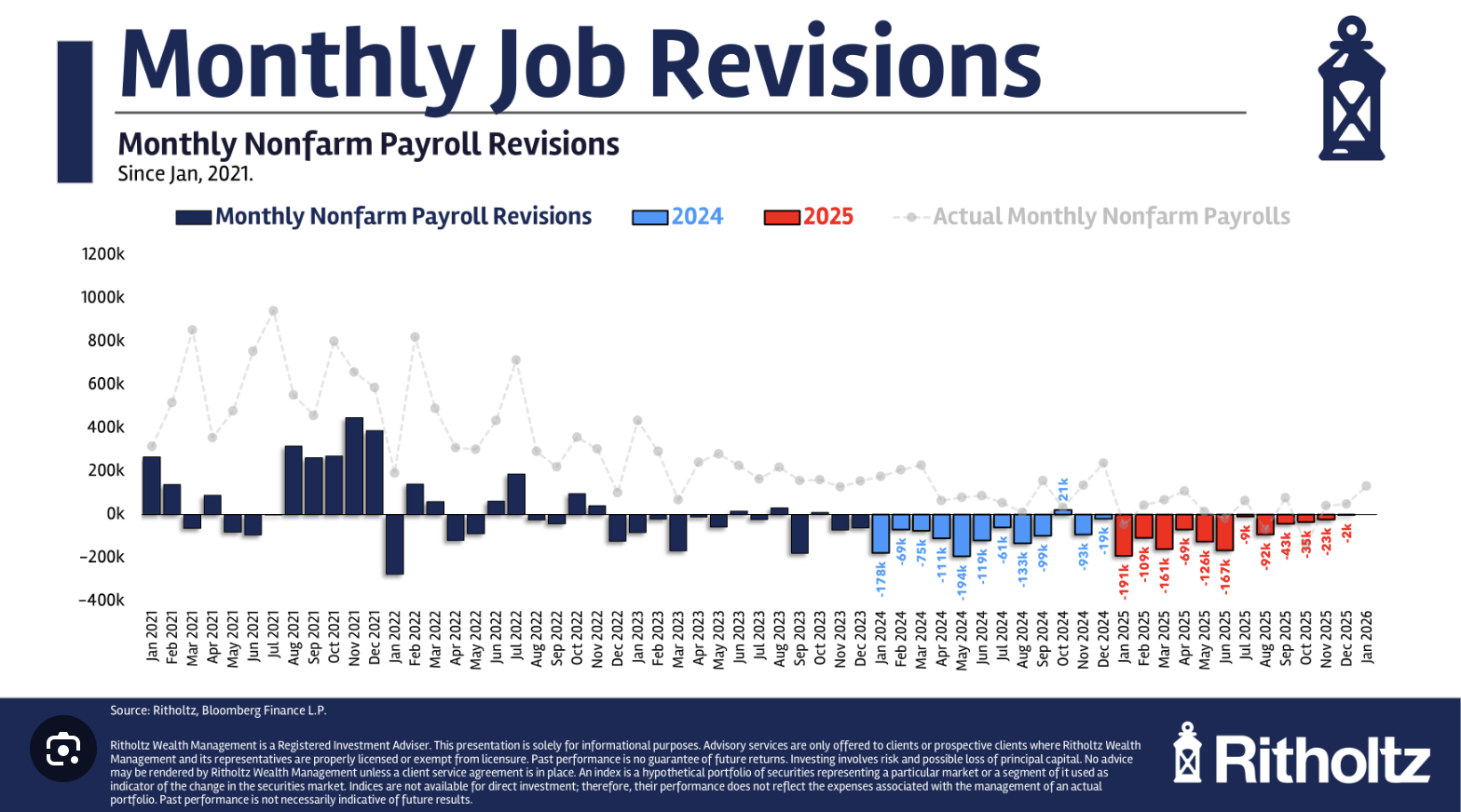

Of course, it is key to remember that revisions to this report have been consistently lower over the past several years as per the below chart. Of course, headlines are everything in today’s world, and while there are many economists and analysts who try to explain the revisions matter and offer a much dimmer view of the labor market, as we all know, the correction to a misleading story published on page 24 never impacts the narrative.

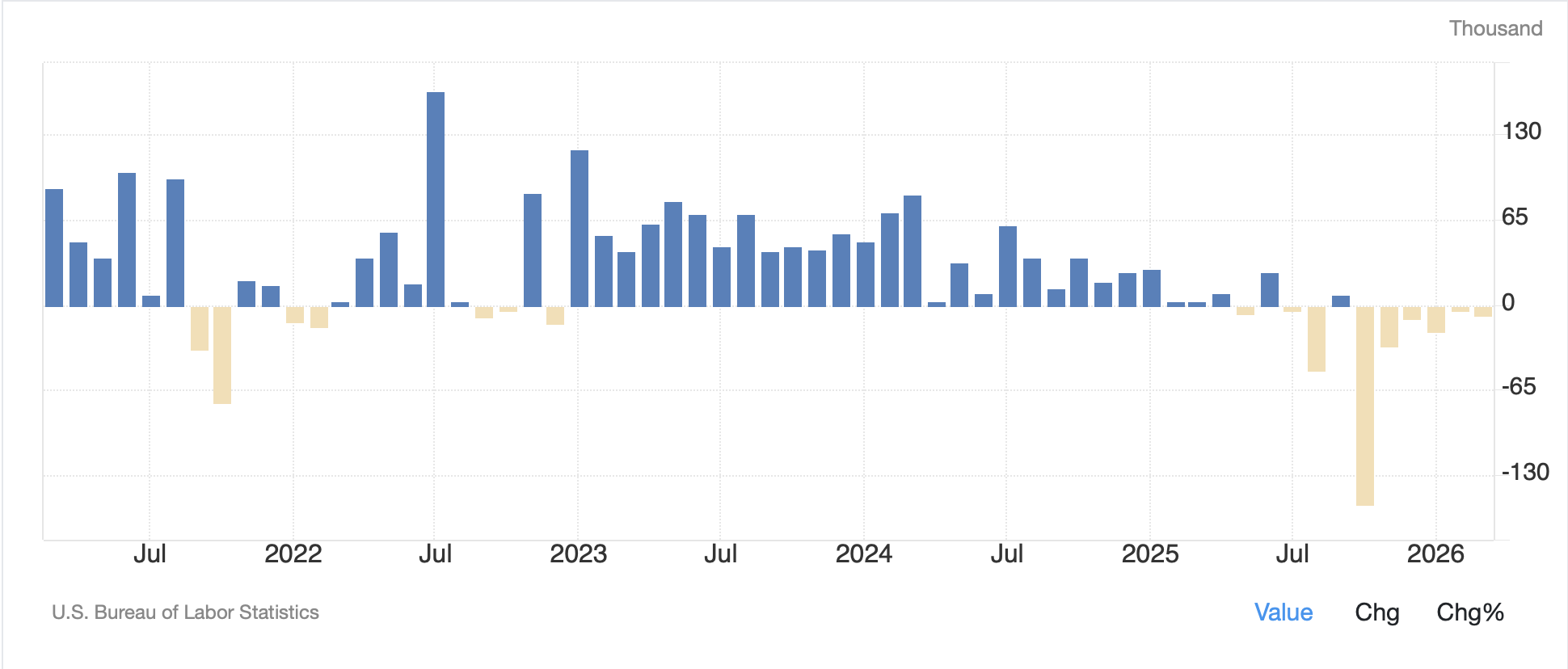

In fact, based on this, and what is apparently a fatally flawed birth/death model at the BLS, and based on the stronger performance in the ADP data as well as the continued low readings from Initial Claims, I anticipate a better than expected number and would not be surprised to see something on the order of 100K. There is one other thing worth noting that I believe is a major positive, and that is that government payrolls continue to shrink, something that can only help the overall fiscal position in the US.

We can only hope that the recent trend, as seen below, continues. As I have written in the past, given the remarkable lack of productivity in the government, if these people become baristas at Starbucks, it would add more to economic prosperity for the nation than their current role.

Source: tradingeconomics.com

And with that as preamble, let’s visit the overnight market results in the wake of the little skirmish and President Trump’s comments that the cease fire was still in effect.

Yesterday’s US weakness has been followed around the world, pretty much, with declines in Asia (Japan -0.2%, HK -0.9%, China -0.6%) and the regional exchanges there as well (India -0.7%, Taiwan -0.8%, Australia -1.5%, Indonesia -2.9%) with only Korea (+0.1%) managing to hold its ground during the session. There is much discussion regarding the upcoming Summit between Presidents Trump and Xi, and the other stories of note are yet another Chinese plan to support domestic consumption. (It strikes me that these plans are akin to European sanctions on Russia, full of fanfare and producing zero results).

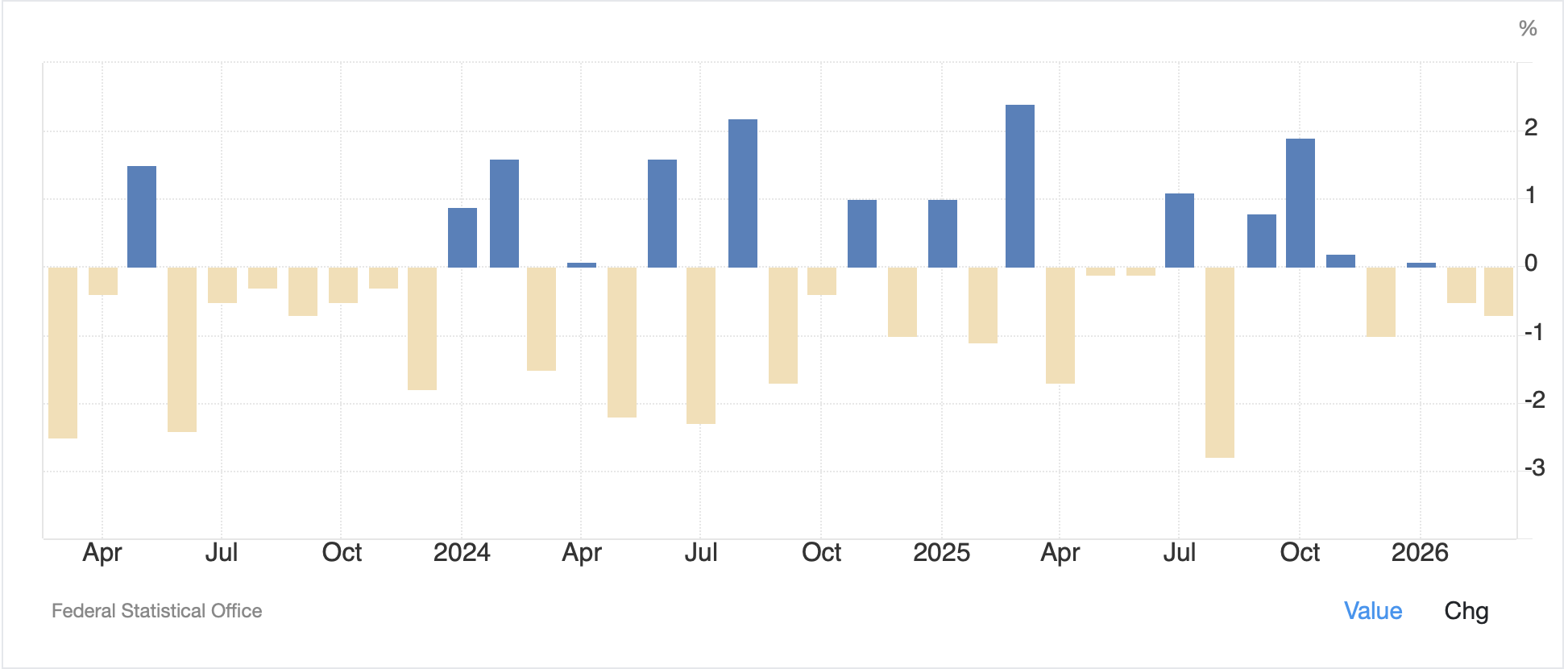

Speaking of Europe, equity markets are weaker there as well with the DAX (-0.7%) leading the way lower after IP was released at a much worse than expected -0.7% in March along with a smaller than forecast trade surplus. A quick look at the last 3 years of German IP and you can see that Energiewende, their insane energy policy, is effectively deindustrializing the nation, once the heartbeat of Europe.

Source: tradingeconomics.com

As to the rest of the continent, red is today’s color with France (0.7%), Spain (-0.3%) and the UK (-0.1%) all under water. However, US futures are higher by about 0.5% across the board ahead of NFP.

In the bond market, Treasury yields (-1bp) are reversing part of yesterday’s climb, but are still higher than yesterday morning. Most of Europe is little changed although UK gilts (-5bps) have performed best after (despite?) local elections where the ruling Labour Party lost half the seats they were defending with the MAGA-like (MUKGA? MEGA?) Reform Party of Nigel Farage and the Green party the big beneficiaries. Pressure is increasing on PM Starmer to step aside as his favorability plummets, but like most politicians, he is clinging to power with a death grip. I’m not really sure I understand the mechanics of why gilts would rally, although perhaps as Reform’s power increases, investors believe there will be more fiscal rectitude.

Precious metals, which rallied yesterday again, are continuing higher this morning (Au +0.8%, Ag +2.8%) with Silver back above $80/oz. I have not mentioned copper (+1.7%) lately, but it is worth noting that the red metal has been powering higher and is approaching the spike high seen in late January, which is the all-time high in the market there. While there are clearly market internals regarding positioning that are helping the move here, it does portend a positive outlook for the economy given its importance in virtually all manufacturing these days.

Source: tradingeconomics.com

Finally, the dollar is under pressure again this morning with the DXY (-0.1%) back below 98.00, but just barely. Again, the collapsing dollar narrative makes no sense to me and if I look at the DXY over the last year, 96.50 – 100.00 does a pretty good job of containing the entire range as per below. If the dollar gets down to that lower level and breaks it convincingly, we can discuss the merits of a short-term vs. long-term view on the dollar’s future.

Source: tradingeconomics.com

And it is important to note that the long-term future, at least compared to other fiat currencies, remains positive in my view. Looking at specific movers, both the euro and pound are higher by 0.35% while the yen (+0.1%) remains caught between its negative fundamentals and fears of another round of BOJ intervention. NOK (+1.3%) is kind of surprising given the lack of impetus in the oil market, but it is no surprise to see ZAR (+0.6%) and CE4 currencies benefit alongside the euro. LATAM currencies are also doing well although CLP (0.0%) is somewhat surprising given copper’s strong move higher.

And that’s really it today. We see payrolls in a bit and that should drive the discussion unless there is some other breakthrough in Iran and the ongoing conflict.

Good luck and good weekend

Adf