This weekend both wars got much hotter

Iran attacked ships on the water

Ukraine sent its drones

Across three time zones

And struck inside Vlad’s magna mater

Thus, oil has risen a bit

While gold and stocks both trade like sh*t

And soon, CPI

Will prove or deny

That views at the Fed are now split

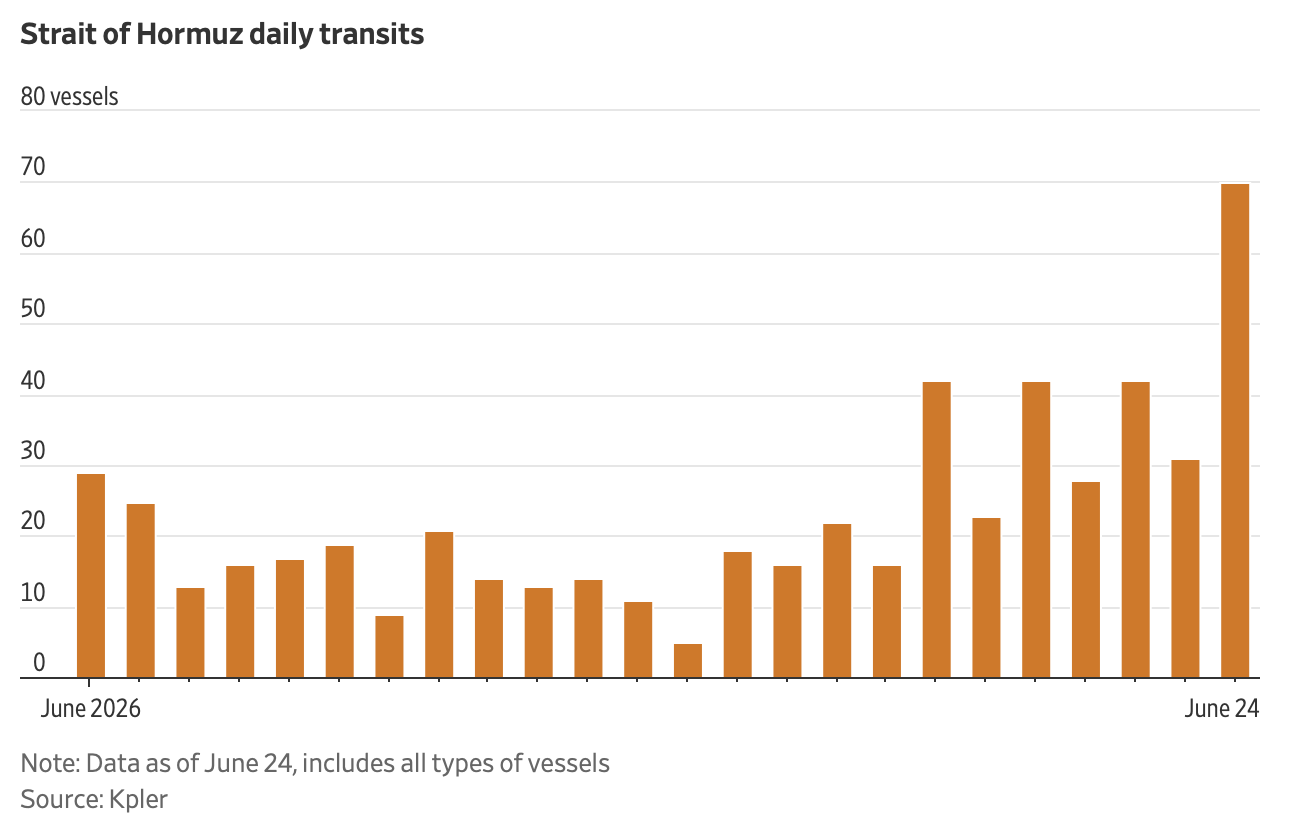

By now, of course, you know that there has been more military activity in the Strait of Hormuz with the IRGC attacking commercial ships and the US retaliating with significant strikes of military sites along the Strait. From what I can see, there are factions within the IRGC that do not want to end the conflict and whatever government exists within Iran has no control over them. As such, it is no surprise that the price of oil (+3.5%) has risen, but even in this scenario, it is well off its overnight highs.

Source: tradingeconomics.com

At this point, I believe the trading community will need far greater proof that there is a shortage of oil before responding with significantly higher prices. Of course, one way that could come about is if Ukraine continues its success with attacks on Russian oil infrastructure as there has been an uptick in that activity with several refineries having been hit in the past several days and Russia imposing an export ban on diesel. Net, things in the oil space remain precarious, but for all the analysts who continue to promulgate the idea that the end is nigh, markets continue to disagree. As always, I vote with markets here.

And, not surprisingly, other markets have responded in a similar fashion to their recent trends with higher oil prices leading to pressure on both stocks and bonds, as well as precious metals while the dollar finds some support. The thing is, my take is the strength of these correlations has been waning somewhat. Frankly, and remarkably, it appears as though an increase in military activity in the Strait of Hormuz has become somewhat normalized to traders and they are looking for other, fresher signals as to their next move.

What might those other signals be? Well, much was made of SK Hynix’s IPO in the US on Friday, which many pundits are now calling the top as the stock fell sharply in Korea overnight, down -15.4% dragging the KOSPI down -9.0% and tech stocks, in general much lower. Of course, the KOSPI had risen dramatically over the past year, as you can see below, and is still higher by more than 100% in the past year despite the recent decline of more than 25% since its peak on June 22.

Source: finance.yahoo.com

The problem with calling the top in stocks is that the earnings data, which starts in earnest this week, has been pretty good so far. If companies continue to earn real profits, investors will continue to purchase stocks.

So, where else can we turn for new information? Tomorrow brings the latest CPI report (exp 3.8% headline, 2.9% core), and you know that will be heavily scrutinized as the punditry tries to determine the FOMC’s reaction function and if it has changed with the new Chairman. At this point, I do believe the Fed’s reaction function has changed, and more importantly, I don’t think anybody knows what it will be like, the Fed included. The previous Fed whisperer, Nick Timiraos at the WSJ put out an article overnight discussing the idea that Chairman Warsh needs to decide whether to undo the most recent rate cuts. However, there is no evidence that Warsh speaks to Timiraos and based on everything Warsh has said, he is not likely to tip his hand. Chairman Warsh does testify to Congress this week, but I expect he will deflect all questions about the future path of monetary policy, and let’s face it, with the likes of Maxine Waters on the House committee, they won’t understand anything he says anyway.

And really, those are the only things that I think matter for now, so let’s review the overnight activity in markets. As mentioned above, stocks are generally under pressure, but not universally so. For instance, in Asia, Tokyo (-1.9%), China (-1.8%) and the aforementioned South Korea all had rough sessions, but HK, Taiwan, India and Australia were all basically flat on the day. The big surprise is Taiwan as given the semiconductor weakness; I would have thought that market would have been significantly impacted. But I guess not. Meanwhile, European investors appear to be completely focused on tomorrow’s France-Spain World Cup semifinal as equity indices there are virtually unchanged this morning. As to US futures, at this hour (7:30) NASDAQ futures are weaker by -1.2%, but the other markets are little changed.

Bond yields are higher this morning, but not hugely so. Treasury yields have edged up by 1bp, and European sovereign yields are higher by 2bps across the board with UK Gilts (+4bps) the real laggard there. Overnight, JGB yields backed up 4bps as well, but that story has more to do with the GPIF than anything else.

Remember Friday?

Japan was bringing home yen

They were just kidding

Think back to Friday. Japanese FinMin Katayama mentioned that the GPIF and other Japanese pension funds ought to consider investing more money in Japan and less abroad. That got tongues wagging about a major policy change coming that would serve to support the yen, and the JGB market while undermining Treasuries as the idea was the GPIF would sell their US Treasuries and buy JGBs instead. Well, it turns out that is not actually the case. The GPIF reevaluates its policy annually but has expressed no urgency to change things now despite the FinMin’s comments, at least according to Reuters. The upshot is that JGBs sold off as did the yen (-0.3%) as per the below chart.

Source: tradingeconomics.com

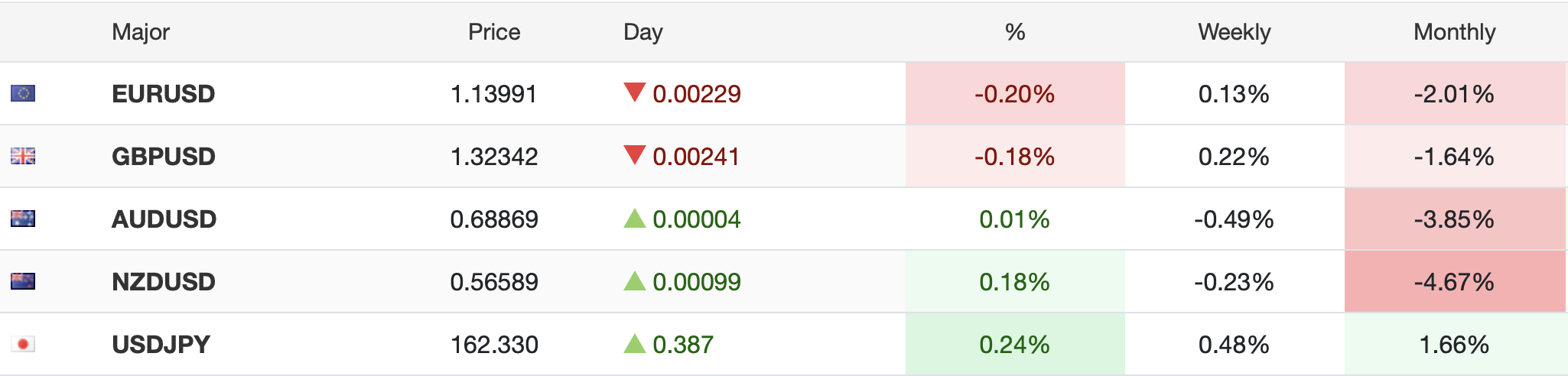

Perhaps more surprisingly, though, the dollar is mixed on the day, not higher across the board as might have been expected given the uptick in oil and military activity. So, we have seen weakness in GBP (-0.1%), AUD (-0.2%) and INR (-0.5%) while EUR (+0.1%), NZD (+0.2%), NOK (+0.3%) and KRW (+0.4%) have all had decent sessions. Net, the DXY is essentially unchanged this morning.

Finally, and quickly, both gold (-1.5%) and silver (-2.0%) are under pressure with the higher oil price although copper (+0.6%) continues to find support and remains well above $6.00/lb.

In addition to the CPI data, it is a pretty busy week as follows:

| Tuesday | NFIB Small Biz Optimism | 95.6 |

| CPI | -0.1% (3.8% y/Y) | |

| -ex food & energy | 0.2% (2.9% Y/Y) | |

| Warsh Testimony | ||

| Wednesday | PPI | -0.1% (6.2% Y/Y) |

| -ex food & energy | 0.3% (5.2% Y/Y) | |

| Empire State Mfg | 8.9 | |

| Warsh Testimony | ||

| Fed’s Beige Book | ||

| Thursday | Initial Claims | 218K |

| Continuing Claims | 1811K | |

| Retail Sales | 0.2% | |

| -ex Autos | -0.1% | |

| Philly Fed | 13.5 | |

| Friday | Housing Starts | 1.30M |

| Building Permits | 1.40M | |

| IP | 0.2% | |

| Capacity Utilization | 76.2% | |

| Michigan Sentiment | 51.5 |

Source: tradingeconomics.com

We also hear from 9 other Fed speakers (it almost seems like they didn’t get the memo about reducing communication) but with Warsh on the stand both Tuesday and Wednesday, I don’t think the others will matter that much. Of course, it will be interesting to hear the other speeches if CPI comes in softer than expected as it may put a crimp in the hawks’ views.

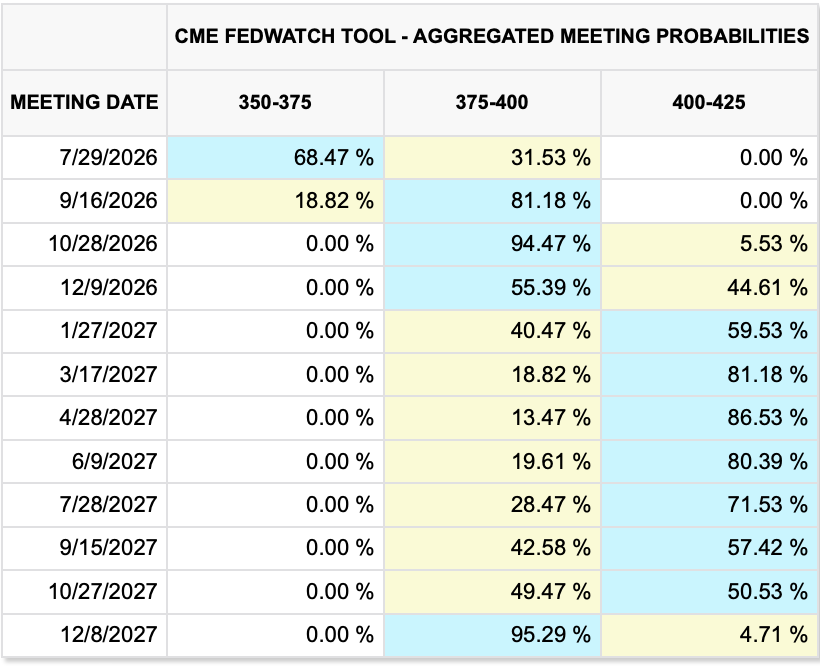

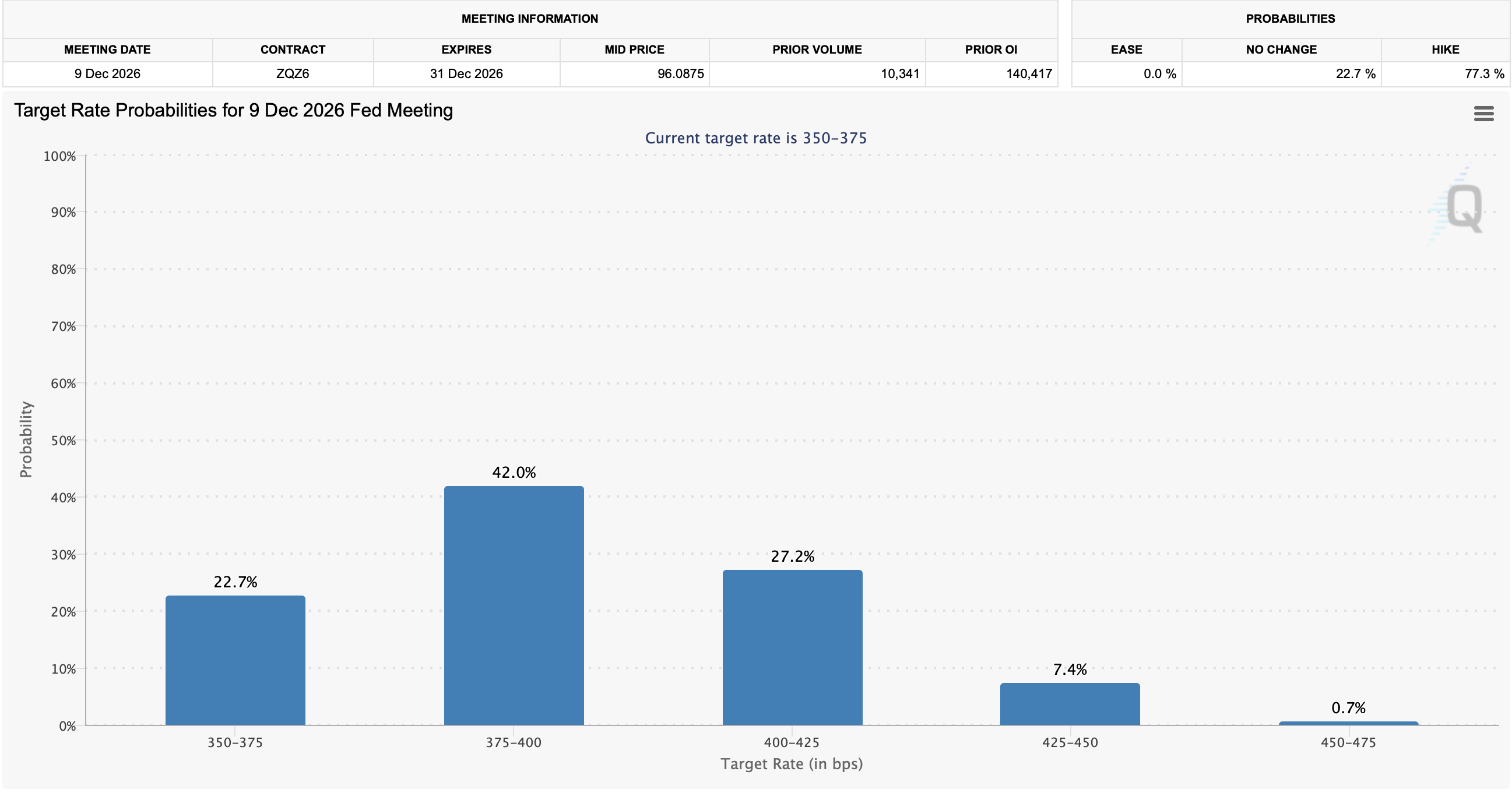

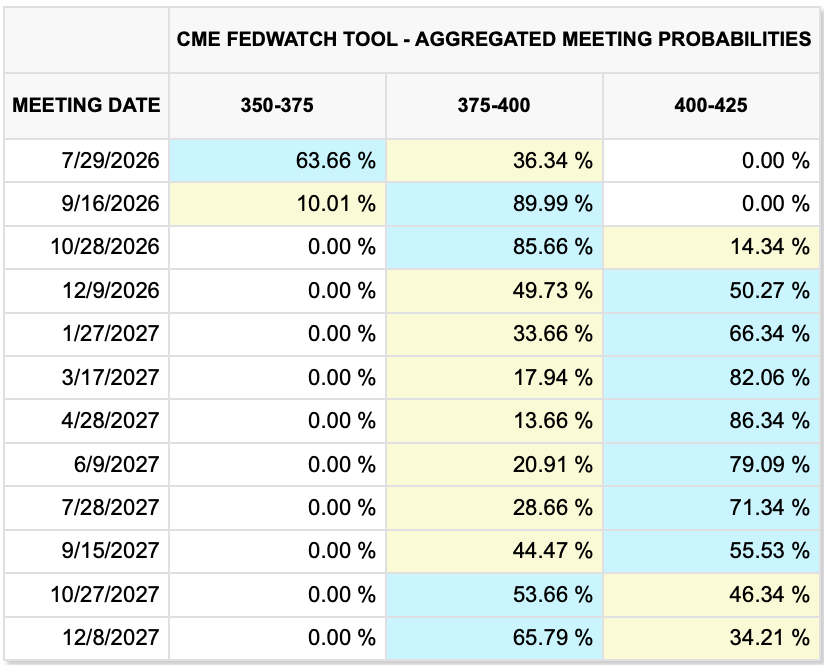

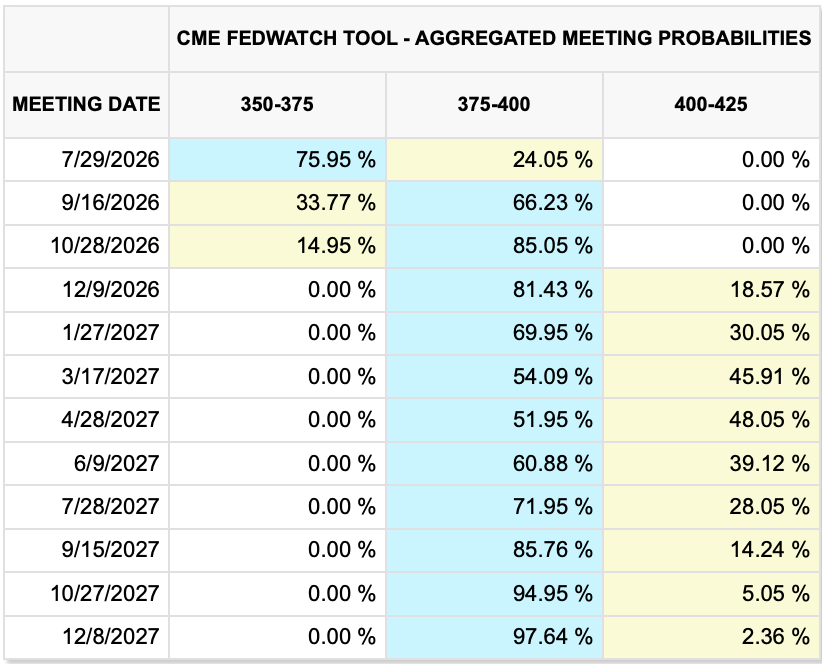

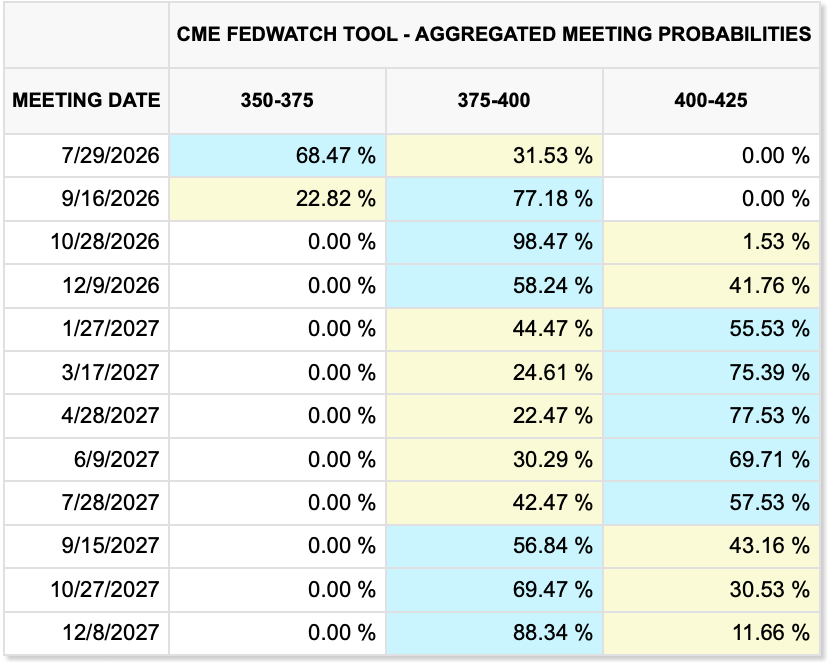

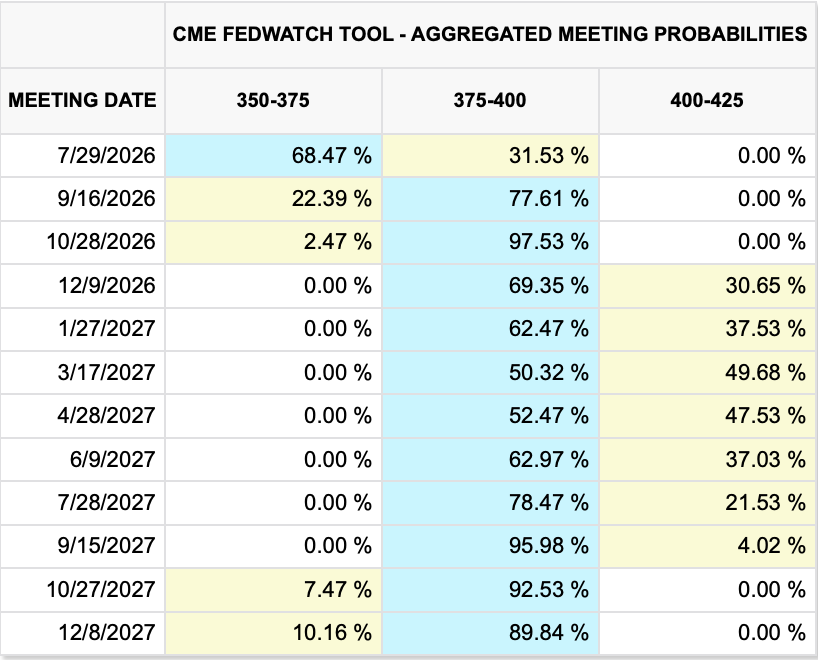

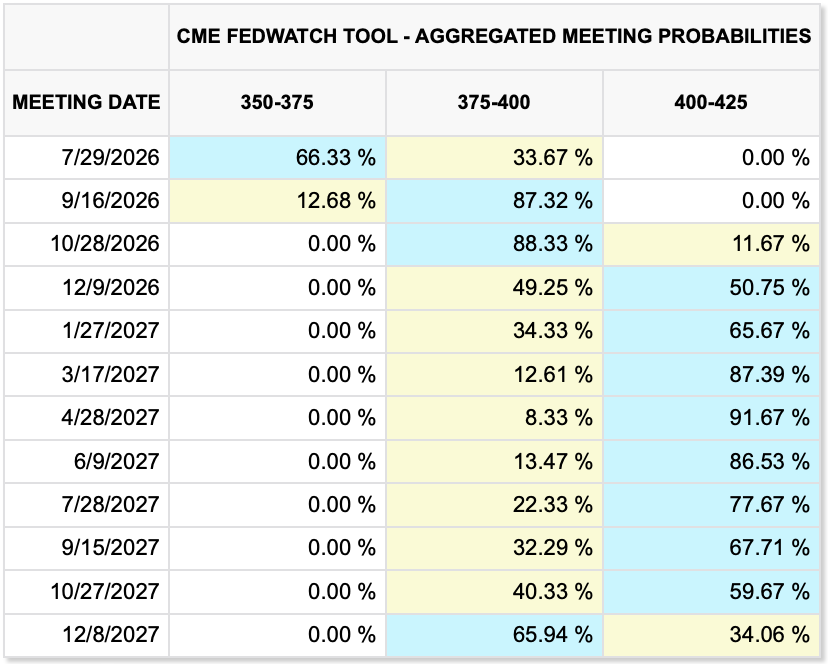

In the end, not that much has really changed I would argue. The war is an exogenous variable, and the market has learned to largely ignore it. The Fed is still too uncertain in its new construction for many views to have changed, but I think the one thing we can conclude is that the old models of their reaction function are no longer viable. My take is the beauty of the task forces for Chairman Warsh is they won’t report for at least 3 months, and probably more like 6 months, so until they report, absent a massive spike in measured inflation, the Fed is not going to do anything. The Fed funds futures market is now pricing a one-third probability of a hike at the end of this month and certainty of one and 50% probability of two by the end of the year. I would fade those trades.

Good luck

Adf