It’s true that I may seem passe

But when I heard words people say

I truly expected

The words I detected

To mean what they did yesterday

So, words like cease-fire depict

A time when two sides don’t inflict

The other with fighting

Or, likewise, inciting

An outcome the words contradict

I have always been a plain meaning of the words sort of fellow, using words in their most common form unless there is some extraordinary opportunity for a pun. And I don’t get many of those. But these days, government spokespeople sound more like Humpty Dumpty than Walter Cronkite, that’s for sure.

“When I use a word,’ Humpty Dumpty said in rather a scornful tone, ‘it means just what I choose it to mean — neither more nor less.’

’The question is,’ said Alice, ‘whether you can make words mean so many different things.’

’The question is,’ said Humpty Dumpty, ‘which is to be master — that’s all.”

Lewis Carroll, Through the Looking Glass

Frankly, Humpty Dumpty had nothing on either the Iranians or the US in this regard. After all, ostensibly there is a cease-fire underway, and yet two days in a row we have had Iran attack ships in the Strait of Hormuz and the US respond. I’m sorry, that doesn’t sound much like a cease-fire to me, but then, I’m just a poet.

While Tuesday’s activities had virtually no impact on the oil markets, with crude slipping further, and equities continuing their ride higher, last night, there was a modest bounce although so far, WTI is still trading around $90/bbl, hardly a signal that the end is nigh. But net, risk aversion is more evident this morning. I guess one day’s worth of skirmishes were believed to be limited, but now, two days in a row, people have concerns.

And that’s where things stand this morning, uncertainty over whether the cease-fire is going to remain in place and uncertainty as to whether talks are going to continue. My take is that, like every conflict, whether military or commercial or even governmental, the question is which side is feeling the pain more deeply such that they must alter their strategies. There was an interesting article in the WSJ describing that exact tradeoff as the blockade is successfully hurting the Iranian economy more than the closure of Hormuz is hurting the US economy. But given the lack of coherent leadership in Iran, with both IRGC hardliners and elected officials tending to be more pragmatic, it remains unclear who blinks first.

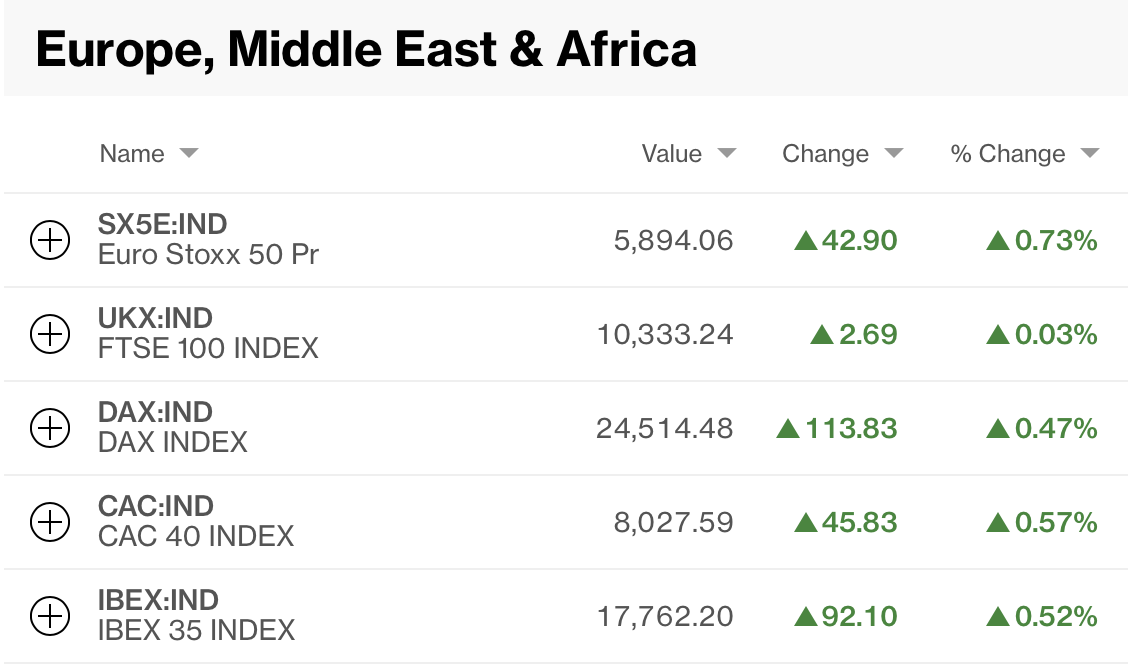

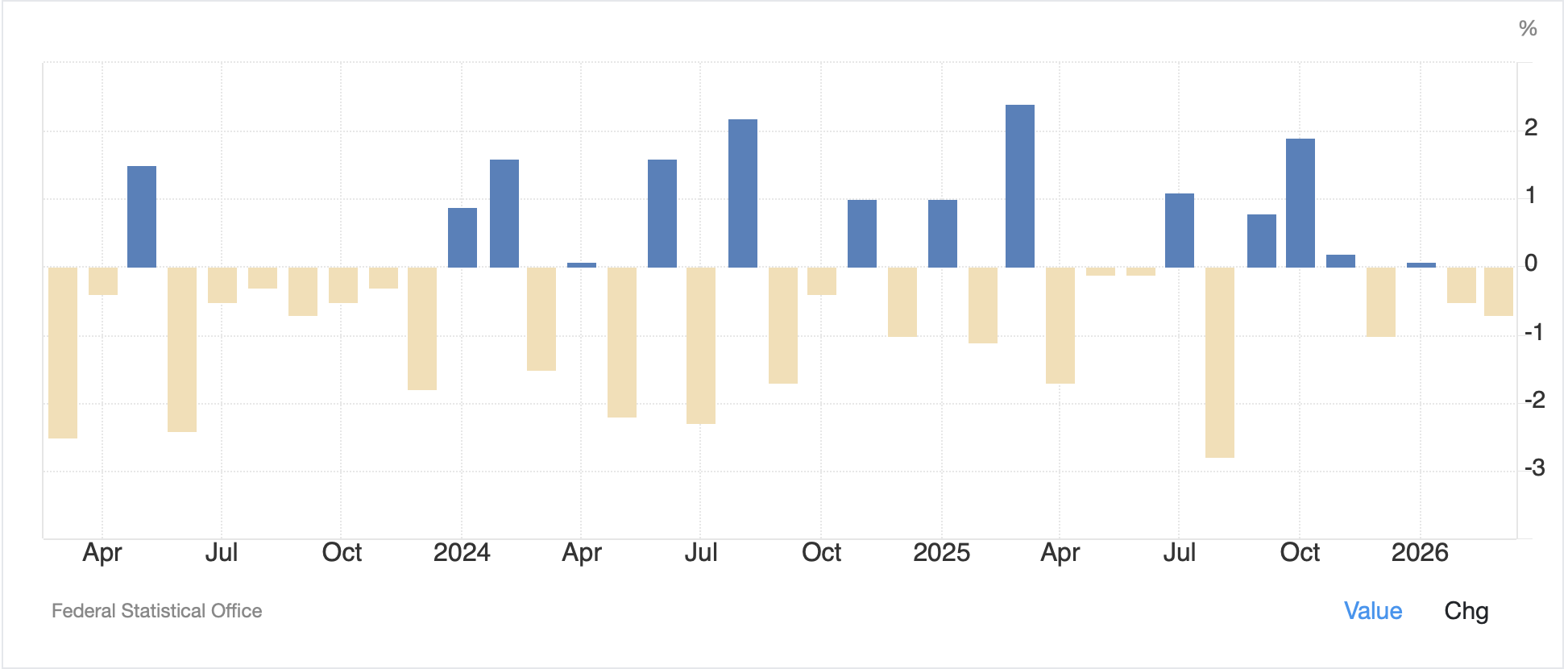

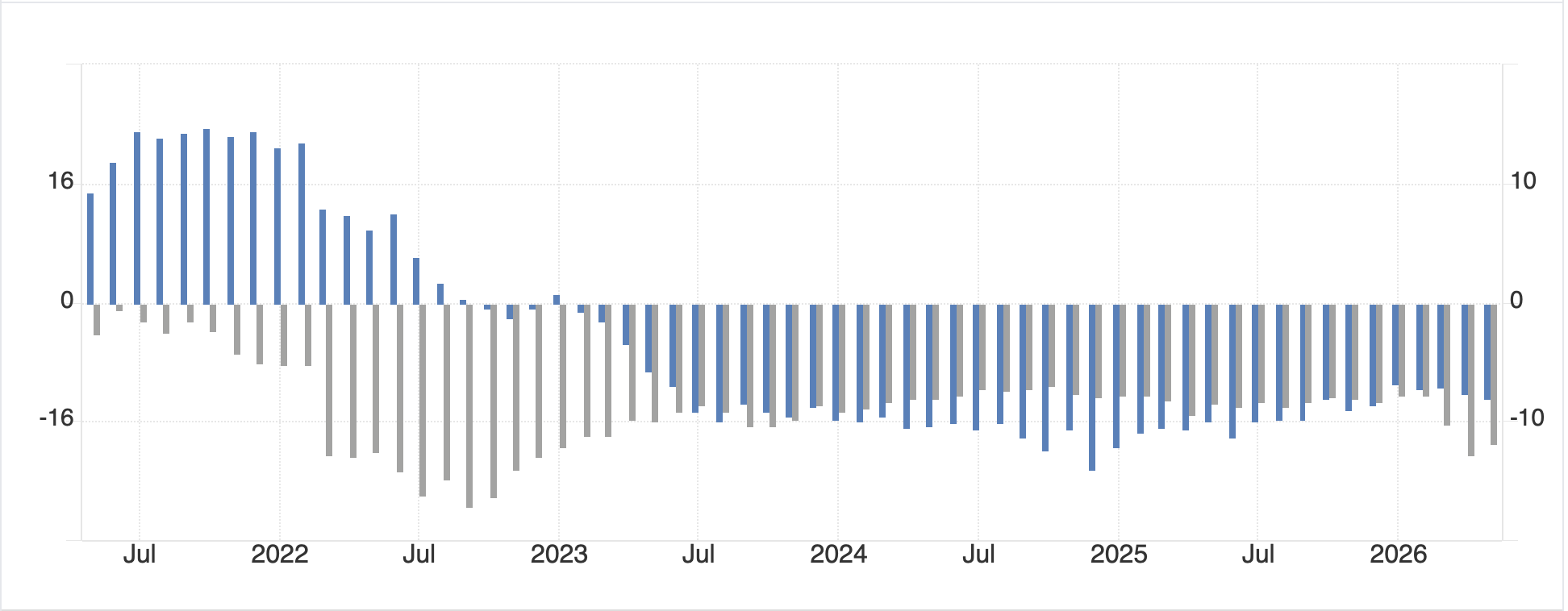

So, let’s see how markets are responding this morning. Yesterday’s lackluster US equity session, where miniscule gains were seen was followed by a somewhat negative picture in Asia as the second attacks made headlines. Tokyo (-0.5%) and HK (-1.3%) were under pressure as were Korea (-0.5%), Taiwan (-1.4%) and Australia (-1.4%). In fact, almost every market in the region was lower except China (+0.1%) which managed a tiny gain. European bourses are all lower this morning as well, with the UK (-0.8%) leading the way down while Spain (-0.4%), France (-0.3%) and Germany (-0.2%) slip less dramatically. The little data we saw showed weak Spanish Retail Sales and negative Eurozone Confidence indicators (Consumer (gray bars) -19, Industrial (blue bars) -8).

Source: tradingeconomics.com

But let’s face it, looking at this chart, things have been pretty dire in Europe for a while now. One wonders how long they can continue their current path of energy insanity and over regulation, although the current crop of leaders is clearly committed! As to US futures, at this hour (6:30) they, too, are pointing lower led by the NASDAQ (-0.8%) with the other indices just barely down in the session.

In the bond market, the fears of runaway inflation and yields from earlier this month have clearly abated and the 10-year is back around 4.50%. I am sure Secretary Bessent would like to see it somewhat lower, but this is hardly an apocalyptic level. One of the things that appears to be underlying the recent rise in yields has been foreign central bank sales since the beginning of the war. Not surprisingly, as the dollar rallied on its haven status, as well as the need for dollars to pay higher prices for oil, nations around the world needed to dip into their reserves to support their own currencies (recall, we have seen intervention from Japan, India and Indonesia for certain) and they sell Treasuries as part of that process. Bloomberg had a nice explanation this morning. But that takes me back to the idea that US yields are not running away, and if the Iran conflict ends soon, we will see yields head lower again. As to today’s price action, most markets have seen yields edge higher by 1bp or 2bps, not really demonstrating much.

In the commodity space, oil (+2.5%) has rebounded from the lows yesterday, but as you can see in the chart below, remains right in the middle of its wartime trading range.

Source: tradingeconomics.com

However, something that hits much closer to home, I would suggest, is gasoline, and you can see how that has behaved over the past month. While it has tracked oil higher today, we have seen a dramatic decline in the price there in the past week as you can see below. I imagine that will begin to filter through to your local gas station pretty soon.

Source: tradingeconomics.com

Turning to the precious metals, they have been absolute dogs of late with both gold (-1.5%) and silver (-1.5%) finding no traction whatsoever. One of the theories has been higher yields are weighing on them, and there is certainly truth there, but I must admit, there seems to be a glitch in the long-term story, a story I have long believed, regarding their ultimate value. Now, remember, markets have a habit of finding the most painful outcome for the most participants, and long gold and silver has been a favorite trade for a while, so perhaps we are simply watching the weakest hands get forced out. But whatever the case, it is certainly uncomfortable if you are long.

Finally, the dollar is modestly firmer again this morning, but looking at the DXY (+0.2%), it remains well within its trading range of 96.50 – 100.00, this morning trading at 99.38. It is very difficult to get too excited about very much here as all the major currencies in both the G10 and EMG blocs are trading in lockstep this morning with one exception, BRL (+0.3%) which has managed a modest gain although it is hard to find a direct rationale for that movement. After all, interest rates haven’t moved enough to change the carry characteristics. My best bet is that this is simply a reflexive move after several days of weakness.

On the data front, it is a busy morning with Personal Income (exp 0.4%), Personal Spending (0.5%), Q2 GDP (2.0%), PCE (0.5%, 3.8% Y/Y), Core PCE (0.3%, 3.3% Y/Y), Initial Claims (211K), Continuing Claims (1780K) all at 8:30 and then New Home Sales (670K) at 10:00. We also get the EIA oil inventory data today, with more draws expected. Adding to that we get NY Fed president Williams speaking this morning. Yesterday, Governor Cook explained that she was very focused on inflation and thought rate hikes may be needed if things don’t change. However, that has been the basic understanding since the last FOMC meeting. I don’t believe they will be hiking rates anytime soon, personally, although cuts are unlikely as well.

And that’s what we have today. The war and oil remain the key drivers, but there will be keen interest in today’s PCE data to see if there need to be further worries about the Fed moving. It is difficult to look at the current situation and think the dollar is going to decline soon, and frankly, my take is we are not going to see much movement at all with price consolidation the theme for the next several weeks.

Good luck

Adf