Said Warsh, when I think of what’s next

For prices, I’m not really vexed

The narrative’s starting,

A new view, imparting

That lower, is what it expects

While futures have yet to adjust

The more this idea gets discussed

The more it’s presumed

The hike story’s doomed

While negative vibes turn to dust

Fed Chair Warsh was in Sintra, Portugal yesterday on a panel with Madame Lagarde, BOE Governor Bailey and BOC Governor Macklem answering questions about monetary policy, forward guidance, and the future of economies as they are impacted by AI. Now, despite Mr Warsh’s adamant explanation at the last FOMC presser that forward guidance was dead, that didn’t stop the interviewer from asking about the Fed’s likely future moves repeatedly. This is getting tiresome.

Nonetheless, here is the comment I believe was most important. “Expectations of future inflation [over the last four weeks] have come down. Inflation risks have come down,” and anyone expecting the Fed would tolerate inflation running above its 2% goal “would be disappointed,” he added.

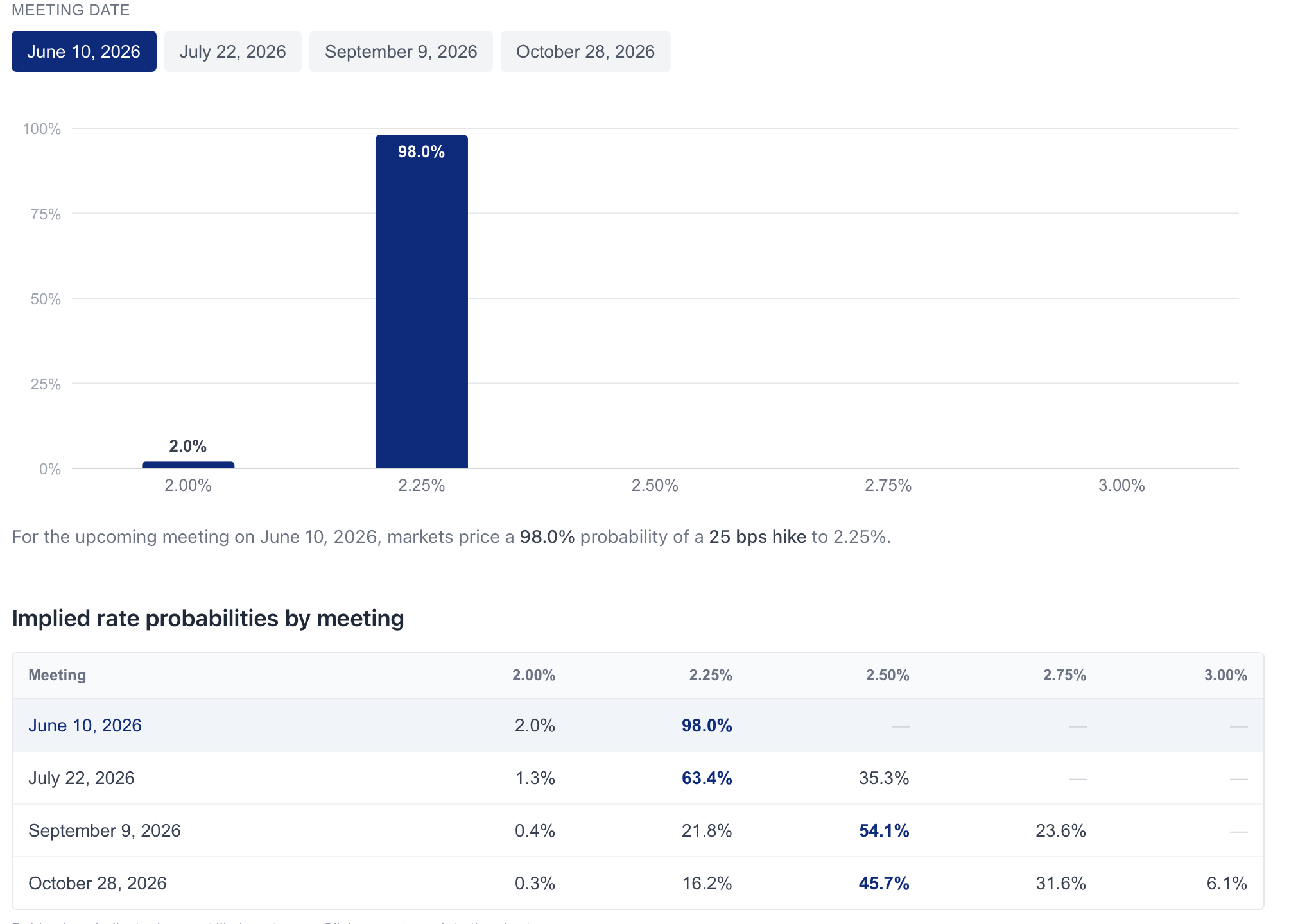

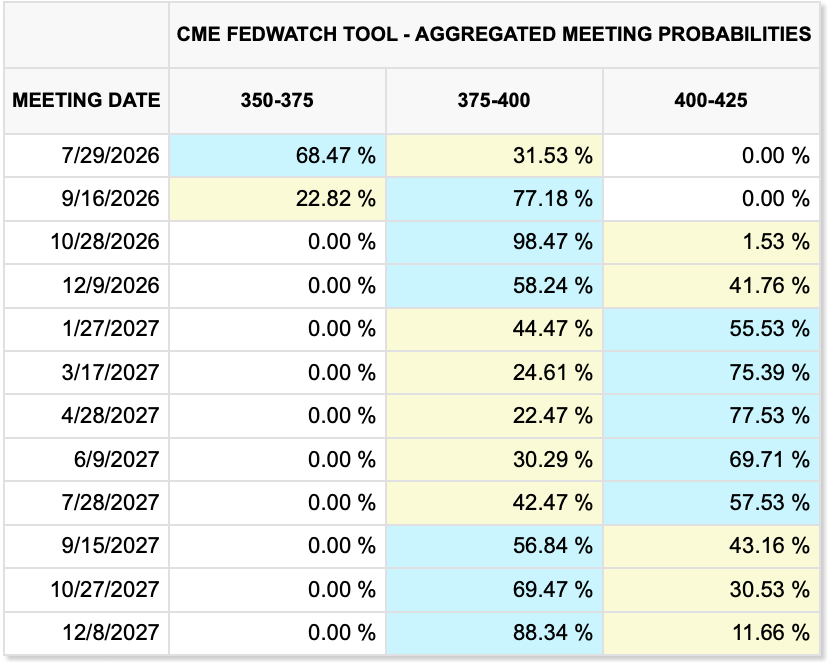

So, the first thing I did was look at the CME’s probability matrix based on its Fed funds futures contract, and there is no evidence to support Warsh’s comments there. As you can see from the below table, it looks virtually identical to what we have seen over the past week, a hike in October and a 40% chance of a second one in December.

Now, I will cut him some slack because, while I agree with him and expect that we will see lower inflation readings this month, simply on the back of the decline in energy prices, the rate hike narrative has been building for a while and has many adherents. My take is that the above table will not change very much until we have seen the two key data points this month, today’s NFP and CPI which is due to be released on Bastille Day.

While I’m on the subject, here is the current view of today’s median expectations according to tradingeconomics.com

| Nonfarm Payrolls | 110K |

| Private Payrolls | 110K |

| Manufacturing Payrolls | 3K |

| Unemployment Rate | 4.3% |

| Average Hourly Earnings | 0.3% (3.5% Y/Y) |

| Average Weekly Hours | 34.3 |

| Participation Rate | 61.7% |

| Initial Claims | 220K |

| Continuing Claims | 1810K |

| Factory Orders | -1.8% |

| -ex Transport | 0.4% |

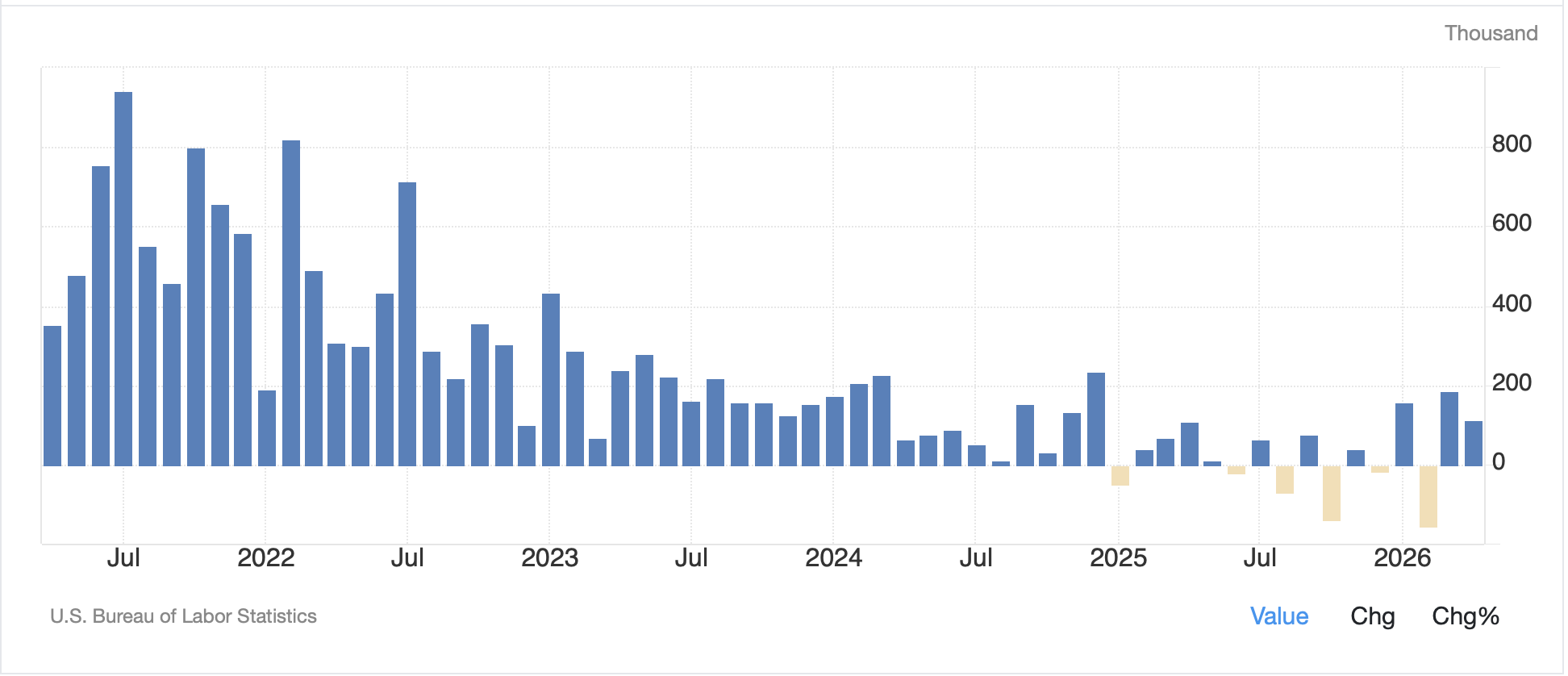

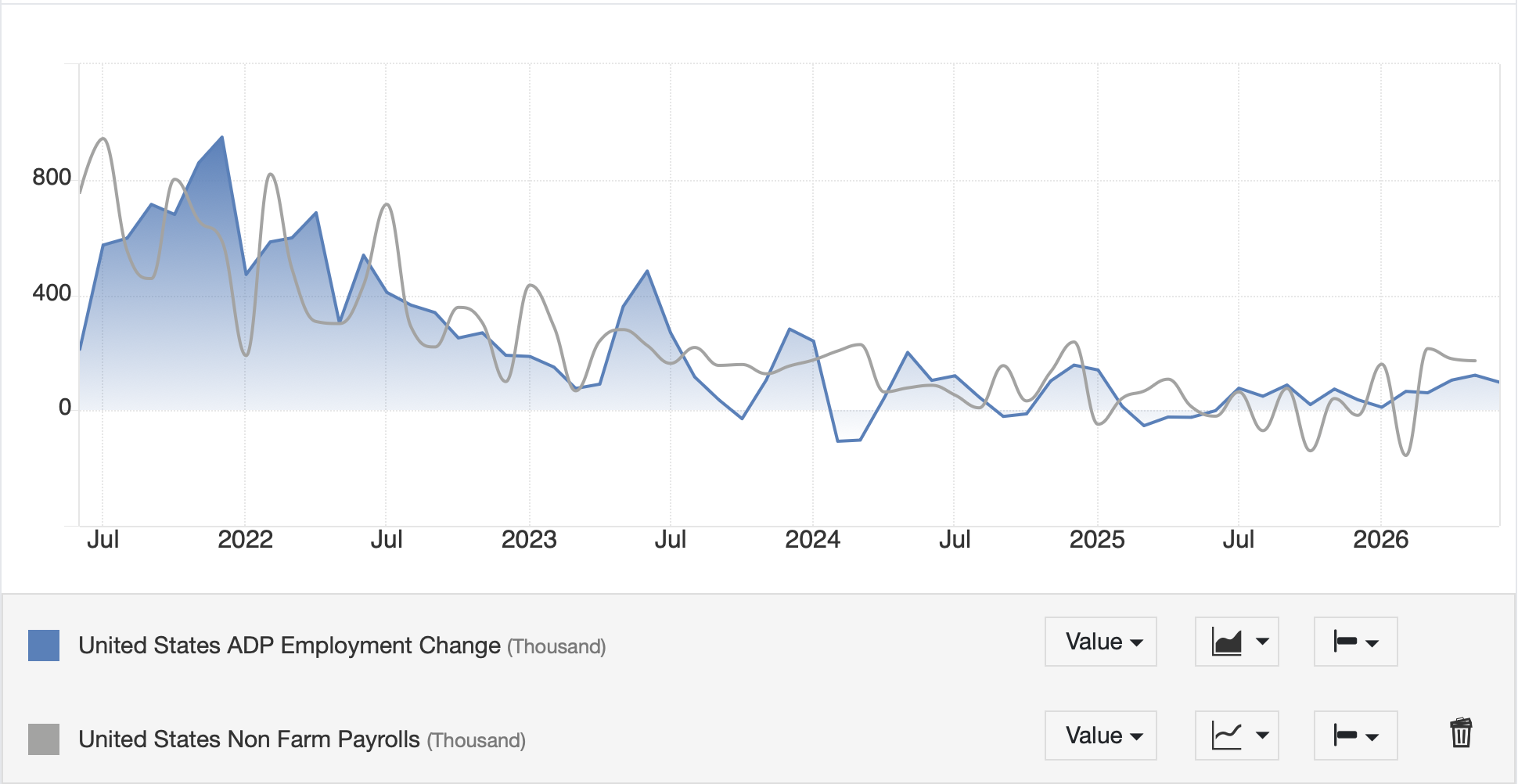

Yesterday saw a slightly softer than expected ADP employment number, 98K vs. the 113K expected and 122K last month, but as you can see from the chart below, comparing ADP to NFP, while the trend remains similar in both, there are an awful lot of wiggles in any given month.

Source: tradingeconomics.com

As things currently stand, the market’s strong Keynesian belief is if NFP is strong, that will be inflationary although it is quite clear that Chairman Warsh does not adhere strictly to that viewpoint (another reason I like him) as he anticipates significant productivity enhancements going forward on the back of AI adoption. But my point is, if we see a strong print this morning, I would look for the market to price more aggressively for a rate hike. I guess we’ll find out shortly.

In the meantime, let’s see what happened overnight. Starting with commodity markets, oil (-1.5%) continues to slide regardless of the group of doomporners who insist that we are about to run out of oil, or that Iran now controls the Strait of Hormuz and will kill the global economy. In fact, from a technical perspective, we have filled the gap that opened back on March 2nd, the first day markets were open after the conflict began.

Source: tradingeconomics.com

My question for all those who remain certain that we have merely delayed oilmageddon is, how low will prices need to fall before they are willing to admit they misread the reality of the global oil market? And, with oil sliding, precious metals (Au +0.8%, Ag +1.1%) are finding support. It seems to me there is a lot of wood left to chop in the PM market, but I maintain my longer-term bullish outlook.

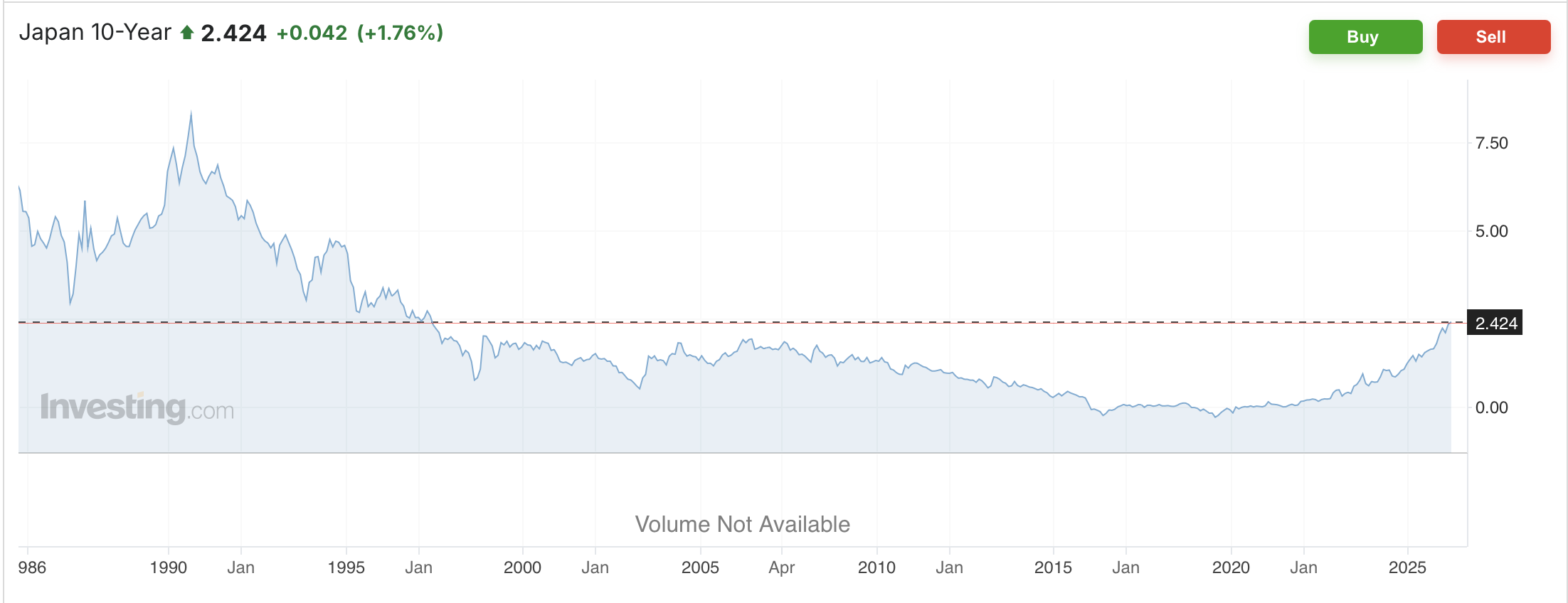

Turning to the bond market, yields rose again yesterday in the US (10-year +6bps) and have edged higher again this morning by 1bp. My sense is this is based on the idea that Warsh’s final comment from above about tolerating above-target inflation has the hawks all bulled up. Perhaps, Sintra helped the hawkish case elsewhere as well as European sovereign yields are all higher this morning by between 4bps and 5bps and JGB yields overnight jumped 8bps.

But there is a kink in the narrative now as despite this perceived hawkishness in the bond market, the FX market clearly heard a different tune. This is clearest in USDJPY, my favorite recent discussion, as you can see in the chart below. The yen jumped 0.7% ostensibly on the idea that Warsh’s comments about reduced inflation expectations implied a less hawkish Fed, despite the bond market reading the comment about unwillingness to tolerate inflation as a more hawkish Fed.

Source: tradingeconomics.com

But it’s not just the yen. The dollar is lower vs. virtually all its counterparts in both G10 and EMG spaces. So, the question you need to ask yourself is, who do you believe? Bond traders or FX traders? Historically, observers call bond investors/traders the ‘smart’ money, but they have made plenty of mistakes in the past. And the thing about FX traders is they seem to be far nimbler. Of course, you know I am an FX guy, and as it happens, I think this is the market that has it right.

Finally, equity markets had a mixed performance in Asia (Japan -2.5%, China -3.0%, Korea -7.9%) as tech stocks have been feeling some pain, but we did see gains in HK (+0.8%), India (+0.8%) and Singapore (+1.1%) as a counterbalance. That Korean number was impressive, but mostly what we are seeing there is serious volatility as the KOSPI is even more concentrated than the NASDAQ with just two companies, Samsung and SK Hynix, representing about 40% of the index. If they have a bad day, the index does as well.

In Europe, though, things are brighter this morning with gains across the board (Germany +0.9%, Spain +0.9%, France +0.8%, UK +0.5%) although there is no obvious catalyst for the move. There was no data of note (Eurozone Unemployment fell to 6.2% but that seems unlikely to be the driver) so perhaps the very fact there are no tech companies in Europe and tech is what is currently under pressure makes Europe seem a bargain. As to US futures, ahead of all the data this morning, they are little changed.

And that’s really it for today. As tomorrow is a holiday, there will be no poetry, so I wish you all a wonderful holiday weekend. 3 Cheers for the USMNT after their Round of 32 victory last night (alas it was on way too late for me to watch, but we will all be cheering on Monday night.

Good luck and good weekend

Adf