Said Roberts and five more Supremes

Those tariffs, are far too extreme

They don’t pass the test

And so, we request

You find a new revenue scheme

Said Trump, while I think you are wrong

Your actions won’t stop me for long

We have many laws

That give me good cause

For tariffs, that help make us strong

For whatever reason, this is what first popped into my head upon hearing the tariff ruling on Friday. I guess I confused love for law, but whatever. At any rate, I’m sure you have seen far too much on this subject already so I will be brief. The Supreme Court ruled against President Trump’s use of the IEEEA law to enable the imposition of tariffs on foreign nations. They did not discuss what to do about the ~$200 billion that has already been collected under that law. The companies that sued want the money rebated, but that was not part of the decision, and of course, the logistics of that would be extraordinarily complex.

But in the end, President Trump simply imposed a sweeping 15% tariff across the board under a different law, which to my understanding can remain in place for 150 days. The equity market shook off the news, rallying across the board on Friday (DJIA +0.5%, S&P 500 +0.7%, NASDAQ +0.9%), so it didn’t seem to be that big a deal. But then when Asia opened Sunday night, risk was in a much less desired state. Early returns show equities softer across the board (-0.75% at 10:00pm), the dollar (DXY -0.4%) under pressure and gold (+1.25%) and silver (6.25%) seeing significant haven demand.

One of the things that appeared to be in question was whether countries that had signed trade deals accepting tariffs and promising investments as part of the deal, would renege, but thus far, that has not happened.

My take is the tariff discussion is no longer a concern to investors. Playing the lead role once again is Iran, as concerns over a potential US military strike rise, with a new actor joining the cast, Mexico, which appears to be suffering significant chaos after the elimination of a cartel leader, “El Mencho” has resulted in fire fights throughout the country there. Obviously, given the proximity to the US, this has the potential to be quite significant, although since the border with Mexico has been effectively sealed, my take is all the action will stay in country there.

Historically, when there’s a war

The first move is stocks to the floor

But generally speaking

Post first mover freaking

The buyers step up to the fore

So, if tariffs are not going to be the primary topic of discussion, and I sincerely hope that is the case, after we finish congratulating the US men’s ice hockey team for the thrilling Olympic victory this weekend, what’s next on the agenda? Iran.

The US continues to amass forces in the Middle East and from various sources, including MSM and X and Substack, the growing consensus is that some type of military action is going to occur. The question now seems to be whether it will be an attempt to decapitate the regime, or just to impede its ongoing buildup of armaments, notably ballistic missiles.

Negotiations are set to resume this week in Geneva and given the stakes, especially for the Ayatollah, it remains unclear as to his willingness to cede to American demands of essential disarmament and the end of terrorist support. For President Trump, the risk is that any military action does not work as quickly and smoothly as either the first attacks on the nuclear sites, or the exfiltration of erstwhile Venezuelan president Maduro. If there is something quick and relatively clean that achieves a clear objective, I think it can be a huge boon for the President, but if anything drags on, it will have numerous ramifications for both the mid-term election and the markets. Let’s focus on the latter.

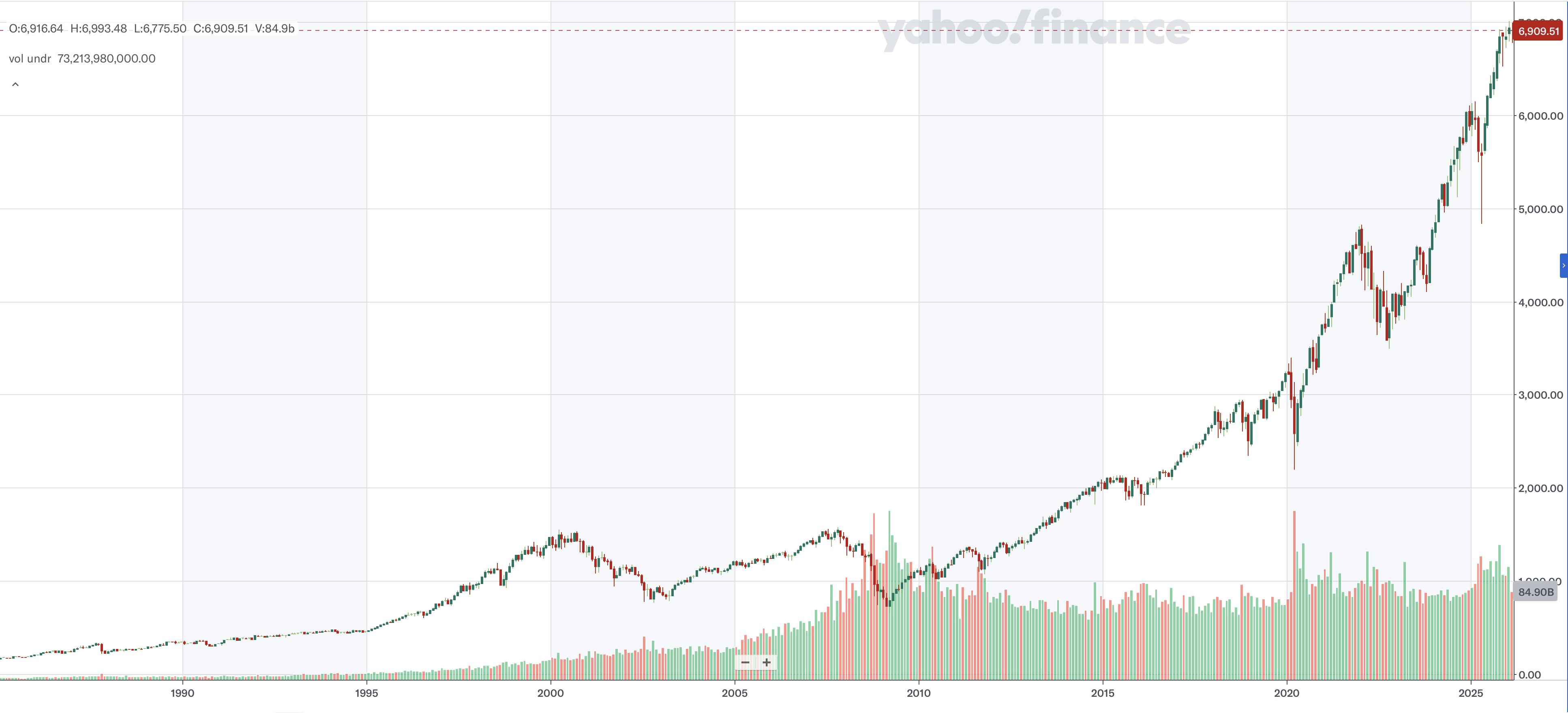

Below is a long-term chart of the S&P 500 which shows both the extraordinary recent performance relative to its previous history, as well as helps highlight some of the downturns seen during that time. Of course, the noteworthy feature is that the downturns don’t last very long.

Source: finance.yahoo.com

If we move from right to left on the chart (these are monthly candles), the first spike down is Liberation Day in April 2025, when President Trump first announced his tariff plans. Obviously, that is long past investors’ concerns now, especially given the events on Friday. The next major decline took place in February 2022, when Russia invaded Ukraine. But remember what also happened around that time, the Fed began its aggressive rate hiking when it figured out that inflation may not be transitory after all. You probably remember that 2022 was one of the worst market performances for both stocks and bonds. It is a worthwhile question to ask how much of that was the Russia/Ukraine situation and how much was the Fed. My money is on the Fed. Moving left, we see the Covid spike lower in Q1 2020 and then a baby dip during the repo shock of late 2018, when the Fed lost control of the Fed funds rate. After that, we go back to the GFC in 2008-09 and the bursting of the dot com bubble in 2000 – 2003. Sure, in 2003, the US invaded Iraq, but I don’t think that was the market driver.

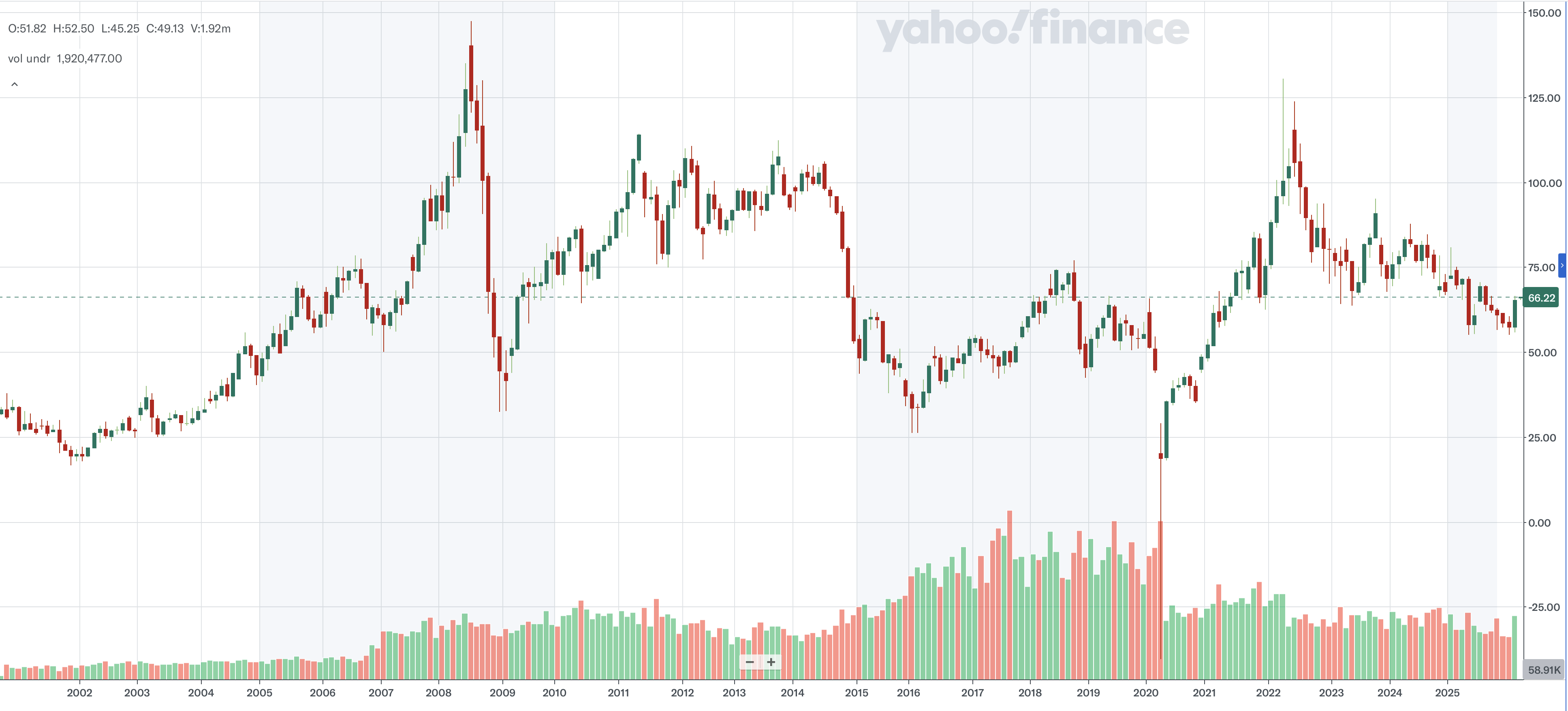

My point here is that any impact from military action is likely to be very short-lived in equity markets. The other market that will certainly be impacted is the oil market. A look at the long-term story there shows that, here too, there are many things that have a major impact on oil other than war.

Source: finance.yahoo.com

The huge decline on the left was the GFC and ensuing recession. The drop in 2014 was the realization that shale oil was going to add an enormous amount of supply to the market. You can see the Covid spike to negative prices and then the run up in prices in the wake of the Russian invasion in 2022, which was relatively short-lived, and we have been declining ever since.

Much of the commentary regarding Iran right now revolves around their ability to close the Strait of Hormuz and how that would cut 20% of the world’s oil supply from reaching the market. (It would cut almost all of Iran’s oil off from the market as they have virtually no pipeline network). But even here, the evidence is that a price spike will be relatively short-lived.

I raise these issues because while war is inflationary, that is generally not because of the impact on oil prices, but rather because of the increased government spending that accompanies war (remember LBJ’s guns AND butter policies leading to the inflation of the 1960’s and 70’s.).

Summing the discussion up, while in the immediacy, there will be market responses to military actions, I do not believe they will have long-term impacts.

Ok, I went on way too long, so let’s do a hyper quick tour of markets this morning and I will leave the weekly data until tomorrow.

Equities – mainland China is still closed, (they open tomorrow) but the rest of Asia mostly ignored the war drums. HK (+2.5%), Korea (+0.65%), India (+0.6%) and Taiwan (+0.5%) all showed strength although Australia (-0.6%) seems to have suffered on the tariff story. Tokyo, too, was closed last night. In Europe, despite slightly better than expected German Ifo data, the DAX (-0.45%) is today’s laggard while the IBEX (+1.0%) and FTSE MIB (+1.0%) both have seen strong support, ignoring any uncertainty regarding the US tariff situation and benefitting from positive earnings results. The UK and France have done little. As to the US futures market, at this hour (7:15) they have risen from their early evening lows but are still softer by -0.35% across the board.

Bonds – the bond market remains the enigma, in my mind, as it is basically locked in place and has been for months. Treasury yields (-1bp) have edged lower and European sovereign yields are essentially unchanged, as are JGB yields. It continues to baffle me that bond markets, which typically sense fear first, do not seem to care about all that is ongoing in the world right now, whether war, government spending, or commodity prices.

Commodities – this morning, oil (0.0%) is ignoring Iran, which is maybe the most surprising thing of all. Perhaps this is telling us that concerns over a closure of the Strait of Hormuz are overblown, or perhaps if that does happen, we will see a dramatic spike higher. Again, like the bond market, something feels amiss. In the metals markets, while both gold (+0.8%) and silver (+2.25%) are higher than Friday’s closing levels, they are well below last night’s opening levels. I guess fear is abating, at least for now.

FX – As to the dollar, it’s early decline has largely been erased with both the euro and pound unchanged, AUD (-0.4%) sliding and the rest of the G10 under pressure. In the EMG space, MXN (-0.5%) is feeling a little stress from the increased violence that has begun and there seems to be some sympathy in that move with CLP (-0.3%) and BRL (-0.2%). On the flip side, CZK (+0.5%) is the biggest gainer as the market continues to respond to recent central bank hawkishness.

In the US today we see the Chicago Fed National Activity Index (exp 0.3 in January) and Factory Orders (-0.5% from Dec). But remember this, as per the below, don’t look for that much activity in NY as this is the picture out my backyard this morning, I’m estimating 10” of snow, so skeleton staffs will be the rule.

Good luck

Adf