The asymptote nears

Will they act at One Sixty?

Can they afford to?

Yesterday saw the yen edge ever closer to the 160 level, the point at which the MOF/BOJ acted in April. Frankly, looking at the chart, it reminds me of an asymptotic limit from calculus, but the one thing we know is there is no natural limit, only whatever artificial one is imposed (or tried to be imposed) by the Japanese government.

Source: tradingeconomics.com

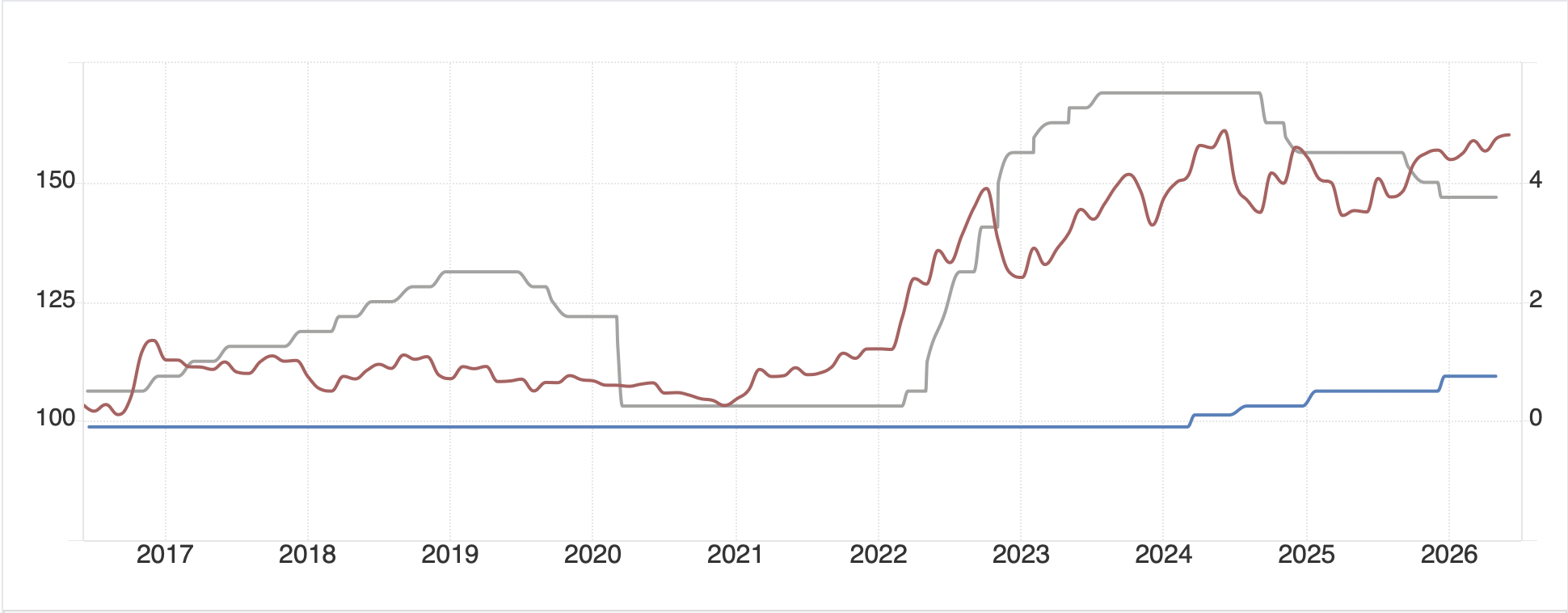

The market continues to price a high probability, ~86% according to the OIS market, of a 25bp hike by the BOJ next week, and I’m confident they will do that. But to me, the question is, will it matter to the FX markets? Here’s the thing about FX, typically there are two separate, but related, drivers of the relative value of one currency vs. another. The most common discussion is about short-term interest rate differentials, typically proxied by central bank base rates. Below is a chart of the past ten years of data for Fed funds (grey line), BOJ base rate (blue line) and USDJPY (brown line).

Source: tradingeconomics.com

It is abundantly clear that there is a strong relationship here, as US rates shot higher in the post-Covid inflation bout and USDJPY shot higher as well. Now, since the Fed started cutting rates back in September 2024, while Japanese rates have edged higher over the same time frame, it would be reasonable to assume that USDJPY should retreat somewhat. However, as you can see in the first chart, that is just not happening. In fact, the pressures are the other way, with far more weakness than strength.

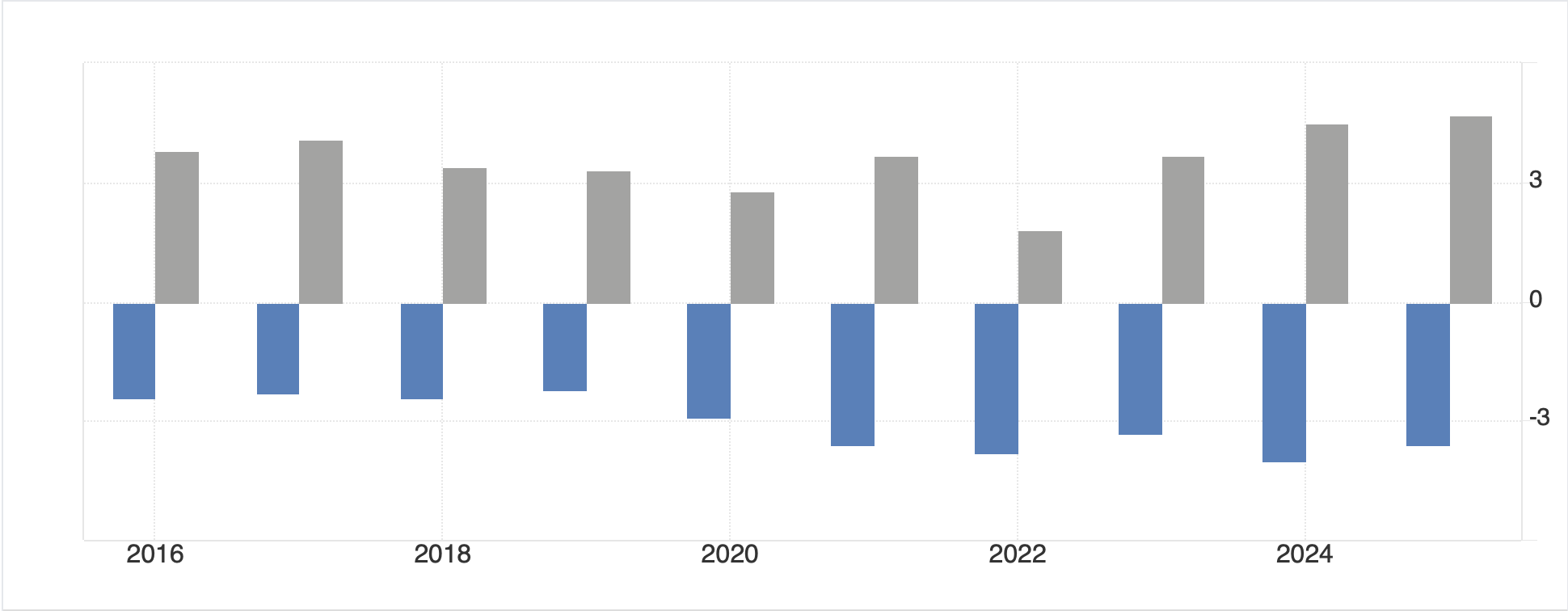

Why, one might ask, is this the case? This takes us to the other major factor in FX rates, relative capital flows. Nations that see substantial inflows in capital will typically see their currencies appreciate. Now, ask yourself, which nation sees the biggest inflows of capital in the world? Yes, the US, as the capital account surplus is the mirror image of the massive current account deficit that we run. In fact, if you look at the below chart, it shows the relative current accounts of Japan (grey bars) and the US (blue bars) in percentage of GDP which most recently showed -3.6% for the US and +4.7% for Japan.

Source: tradingeconomics.com

Now, let’s do the math. US GDP is ~$28.8 trillion while Japanese GDP is ~$4.4 trillion. 3.6% of $28.8 trillion = ~$1.037 trillion of capital inflows. 4.7% of $4.4 trillion = $202 billion of capital outflows. Of course, we know that everybody in the world is piling into US technology stocks, and that is where the capital is mostly flowing, but in order to do so, they are buying USD. This is true of Japanese investors as well as others around the world.

There is a narrative that is developing that claims as the Japanese raise interest rates, the massive, short yen positions that exist to fund many speculative trades will unwind, and with that, the yen will strengthen dramatically as well as we will see many other markets sell off sharply as those positions unwind. But the NASDAQ is up 21% YTD and 40% in the past year. If you are an investor and you are funding a speculative position at 0.75% annually that rises to 1.00% while you are returning 40% on the other side, do you really care?

To my eye, for the yen to change course, intervention is irrelevant, and so is a 25bp rate hike. We need to see a wholesale change in the combination of Japanese fiscal and monetary policies as well as changes in those policies in the US. Historically, a tight monetary and loose fiscal policy combination will strengthen a currency (something that the US currently has), but can Japan afford to tighten monetary policy that much? My money is on no, and while 25bps seems pretty certain next week, I would not be looking for USDJPY fall very far, if at all. And remember, the market is pricing a 50% chance of a Fed hike by the end of the year. Don’t be taken in by this story in my view.

Away from this issue, it is difficult to find other critical news. Yes, there was another skirmish in Iran straining the concept of a ceasefire, but all-out war has not resumed. The elections in California and LA will take several weeks to determine who will be on the ballot in November, which, when you think about it, sums up the incompetence of California governance writ large.

So, oil is higher along with the dollar and yields, but so are stocks, while metals slip. Let’s look at the overnight activity. Another set of equity records in the US was followed in Asia by broad based strength as Tokyo (+2.5%), China (+0.5%), Korea (+0.2%) and Taiwan (+2.0%) all continued to climb. Both HK (-1.6%) and India (-0.4%) were not as robust with the former seeing profit taking after a few strong sessions while the latter felt pressure from those rising oil prices. One outlier here was Indonesia (-4.5%) which suffered after weaker than expected trade data, higher than expected inflation data, and a weakening rupiah which set another record low (dollar high), touching 18,000.

European bourses, meanwhile, are mostly under pressure after President Trump has devised a new way to impose tariffs on nations that allow “forced labor” which is defined as “all work or service which is exacted from any person under the menace of any penalty for its nonperformance and for which the worker does not offer himself voluntarily.” One must give the president props for his continuous efforts to impose tariffs, if nothing else. At any rate, Germany (-0.9%) is leading the way lower, followed by Italy (-0.3%), France (-0.2%) and the UK (-0.2%) although Spain (+0.5%) is bucking that trend on the strength of the earnings for Inditex (Zara clothing parent) which is one of the largest companies in the nation. US futures, at this hour (6:40) are mixed.

In the bond market, yields are rising again on the back of the oil price rise with Treasury yields (+4bps) gaining alongside the entire European sovereign market, all of which have risen a similar amount. Last night, JGB yields also rose 6bps, as they respond to the oil market as well as pending rate hikes by the BOJ.

In the commodity market, if you think back to late May, you may recall an announcement that a deal with Iran was close which prompted a gap lower in oil prices as you can see in the chart below. Well, that gap has now been filled.

Source: tradingeconomics.com

Just as nature abhors a vacuum, markets abhor a gap and seek to fill it whenever possible. My take here, though, is now that the gap is filled, there is less reason to see oil rally much further and a consolidation before a slow decline is in the cards. As to metals markets, gold (-0.8%), silver (-1.2%) and copper (-1.1%) are all softer on the day, with their negative correlation to oil intact.

Finally, the dollar is firmer this morning, keeping in line with its recent relationship with other markets. However, the movement remains relatively muted with most G10 currencies softer by -0.2% or so as only SEK (-0.6%) and NOK (+0.1%) really buck that trend. NOK is clearly benefitting from the oil price rise while SEK seems to be suffering from a slightly higher beta to the broad dollar move. In the EMG bloc, KRW (-0.9%) is the laggard as it continues under pressure and trading to its lowest levels (highest dollar) since 2009.

Source: tradingeconomics.com

But otherwise, most of these currencies are slipping a similar amount to the G10 bloc, on the order of -0.2% or so.

On the data front, this morning brings ISM Services (exp 53.8) as well as Factory Orders (4.6%, 0.8% ex-Transport) and then the EIA crude oil inventories with another sizable draw anticipated. At 2:00, the Fed’s Beige Book is released which should make for some interesting reading. Yesterday’s JOLTs data was surprising in that it showed a significant jump in job openings, 700K more than expected which does not portray a weakening labor market.

Overall, equity markets seem to be disconnected from the impact of oil prices, something that very few analysts would have forecast in February. But the dollar remains closely linked to those prices for now. As we all sit here, waiting for the next headline, I cannot help but look at the US data and consider that the economy continues to tick over pretty well. Ultimately, I believe that bodes well for the dollar over time, or at least until some other major economy shows it can perform well.

Good luck

Adf