The fallout from Warsh’s decision

To leave rates without a revision

Has opened the doors

For pundits and bores

With hawks and doves set for collision

For some, Warsh has failed from the start

As they felt a rate hike was smart

But others explain

That under his reign

It’s markets that play the main part

For a no action outcome by the Fed last week, it certainly is interesting how much digital ink has been spilled discussing the outcome of that meeting and, depending on which side of the argument you fall, whether it was the right move or an error. You know I have been of the belief that there will be zero rate hikes this year and nothing has changed that opinion yet.

There is a great deal of conversation regarding the Fed’s credibility and how despite Warsh’s tough talk about achieving their 2% inflation goal at his first meeting, by doing nothing last week, he has trashed that credibility. My first thought here is, given the Fed has failed in its key objective for more than 5 straight years on its own terms, it is difficult for me to accept they had a lot of credibility left to trash. But my second thought is to listen to the Chairman’s words about allowing the market to do its job, and not simply watch the Fed, and I realize there are an awful lot of analysts and pundits who don’t know how to do that and therefore are extremely uncomfortable now. As I wrote last week, these folks get paid a lot of money by Wall Street and now they have to earn it. So perhaps that explains the ongoing diatribes.

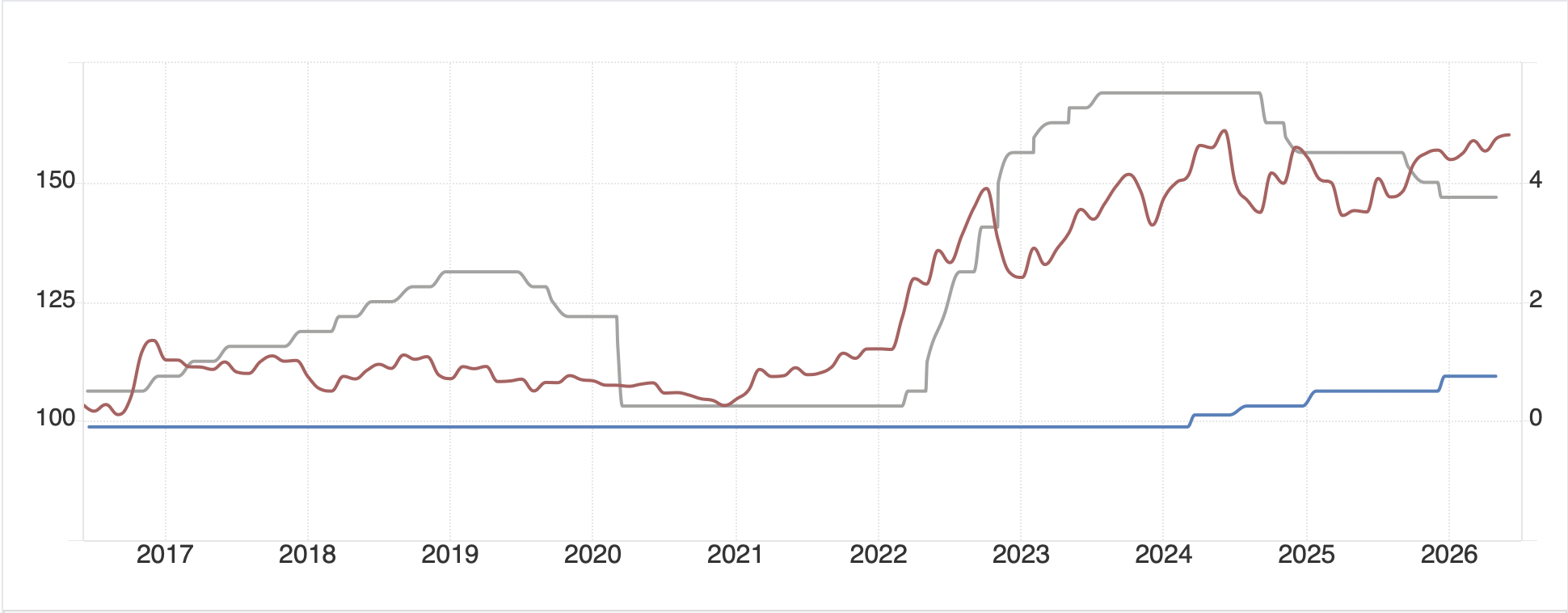

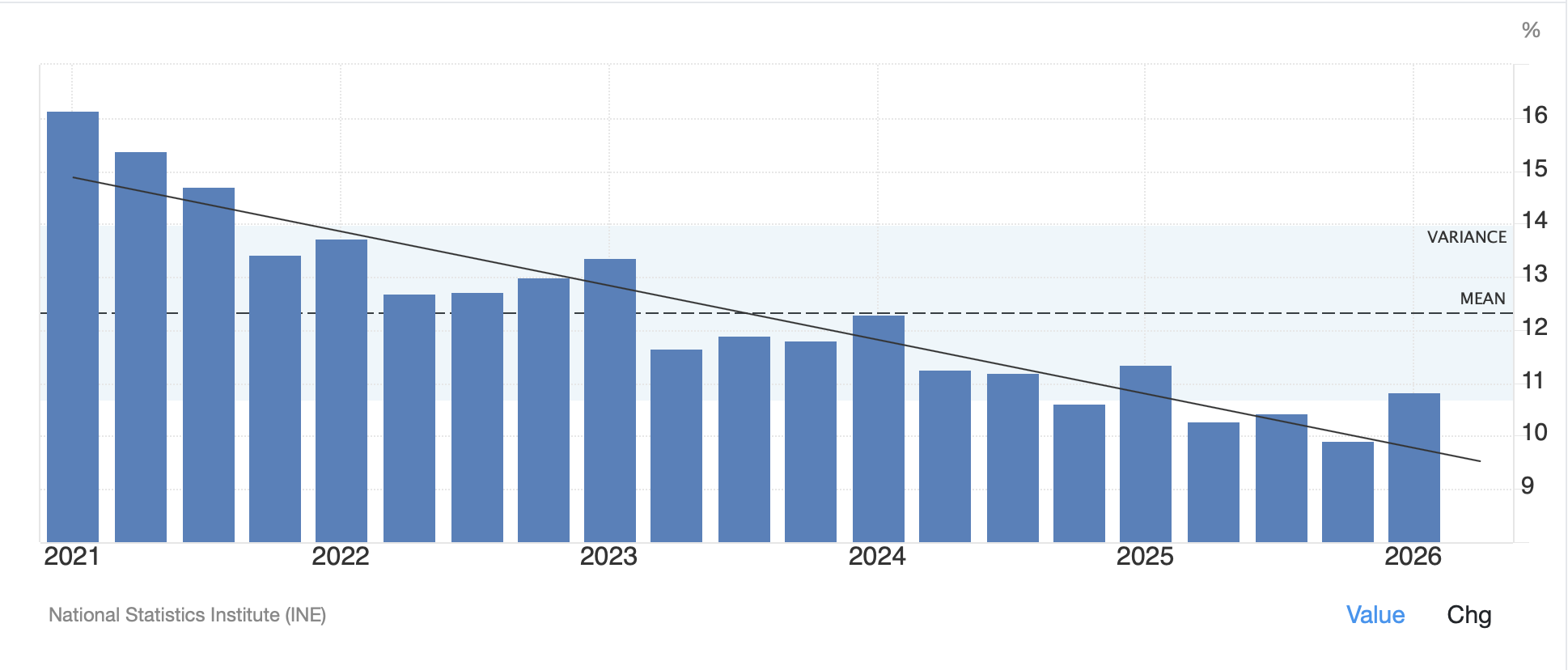

Much has been made of the fact that between the June and July FOMC meetings, US Treasury yields rose substantially as you can see from the below chart.

Source” tradingeconomics.com

At the close on Friday, they had risen 34bps in the 30-year and 28bps in the 10-year), although this morning, with oil prices (-5.6%) falling on the back of a renewed diplomatic initiative in Iran, both of those bonds have seen yields back off by 5bps.

Now, one of the things that Warsh specifically explained in the press conference was that the market had raised rates already, effectively doing the Fed’s job for them. And here is the point of departure, I believe, regarding the punditry viewpoint and the Warsh viewpoint. Warsh has been explicit in saying he wants the Fed’s footprint in the markets to shrink. He wants market participants to, “play the ball, not the referee”. However, the pundits claim that the only reason rates rose was in anticipation of the Fed hiking rates.

So, let’s try a little thought experiment. Assume there was no Fed, instead that money supply was mechanically increased by 2% per year and that all interest rates were determined by the market. Do you believe that in this scenario, a government running consistent extremely large deficits would not drive interest rates higher than they otherwise would be, without a central bank to officially do so? I know I do. Is that any different than the market pushing yields higher because they are concerned with excess supply of Treasuries and other inflation concerns?

The Fed has had a major, and in Warsh’s (and my) view, too large impact on markets for a long time, since Black Monday in 1987. Change is hard and the punditry does not like the fact that they are going to have to actually think and pay attention to many variables in order to have a viable view on things, so they are all crying and claiming Warsh is making a huge mistake. While not surprising, I think they are completely wrong.

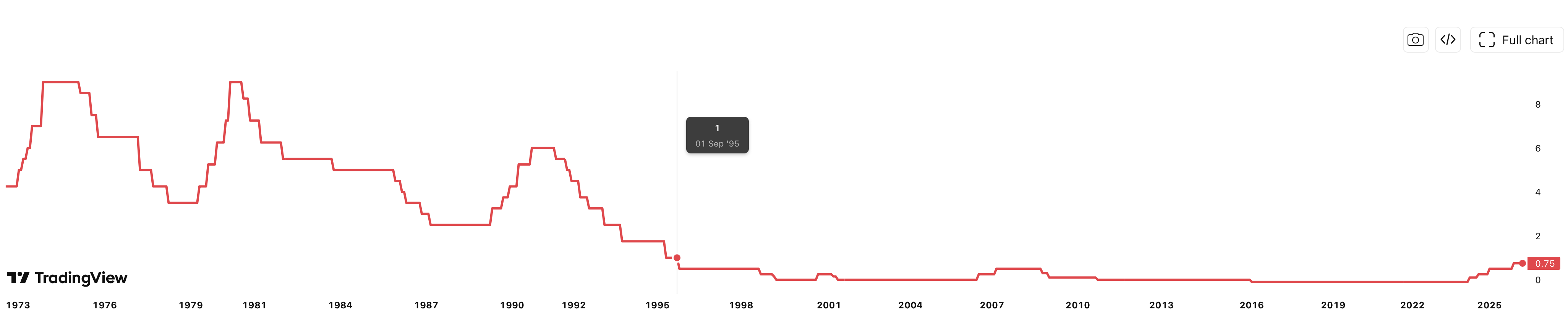

It is also important to understand that the current yields in the bond market are anything but ordinary. Below is a chart I created with FRED data and included the long-term average 10-year yield since 1962, which happens to be 5.81%, more than 100bps above current levels. For a very long time, a good rule of thumb for the 10-year yield was it should be approximate the nominal GDP growth rate, but we have gone through such a long period of financial repression, that idea faded away. Perhaps that is coming back into vogue, so at the long-term average, we could see 3.8% GDP growth and 2.0% inflation. And even today, it could represent 2.7% GDP growth and 2.0% inflation. I don’t think anybody would be unhappy with that outcome.

My understanding is the task forces will not be reporting until early next year. At the same time, I am convinced that Mr Warsh is very serious about making significant changes at the Fed going forward, and I applaud that. But it is going to require him to convince 18 other people who have been inculcated in a process that has proven to be a failure but offers comfort to those people because they know how it works. Change is very hard, and this will be harder than most. One last thing, the biggest change is going to be the balance sheet. The Fed continues to buy T-bills and expand the balance sheet as they continue to seek to maintain “ample” reserves, so banks have liquidity. I would not be surprised if when we hear from Chairman Warsh at the Jackson Hole meeting at the end of the month, he indicates the Fed will stop buying bills at the next meeting moving further down the path of change.

Surprising comments

Bessent admitted the Fed

Joined the Japanese

The following statement released by Japan’s MOF is quite a surprise, at least the fact that they admitted to the action, something that has rarely been the case in the past.

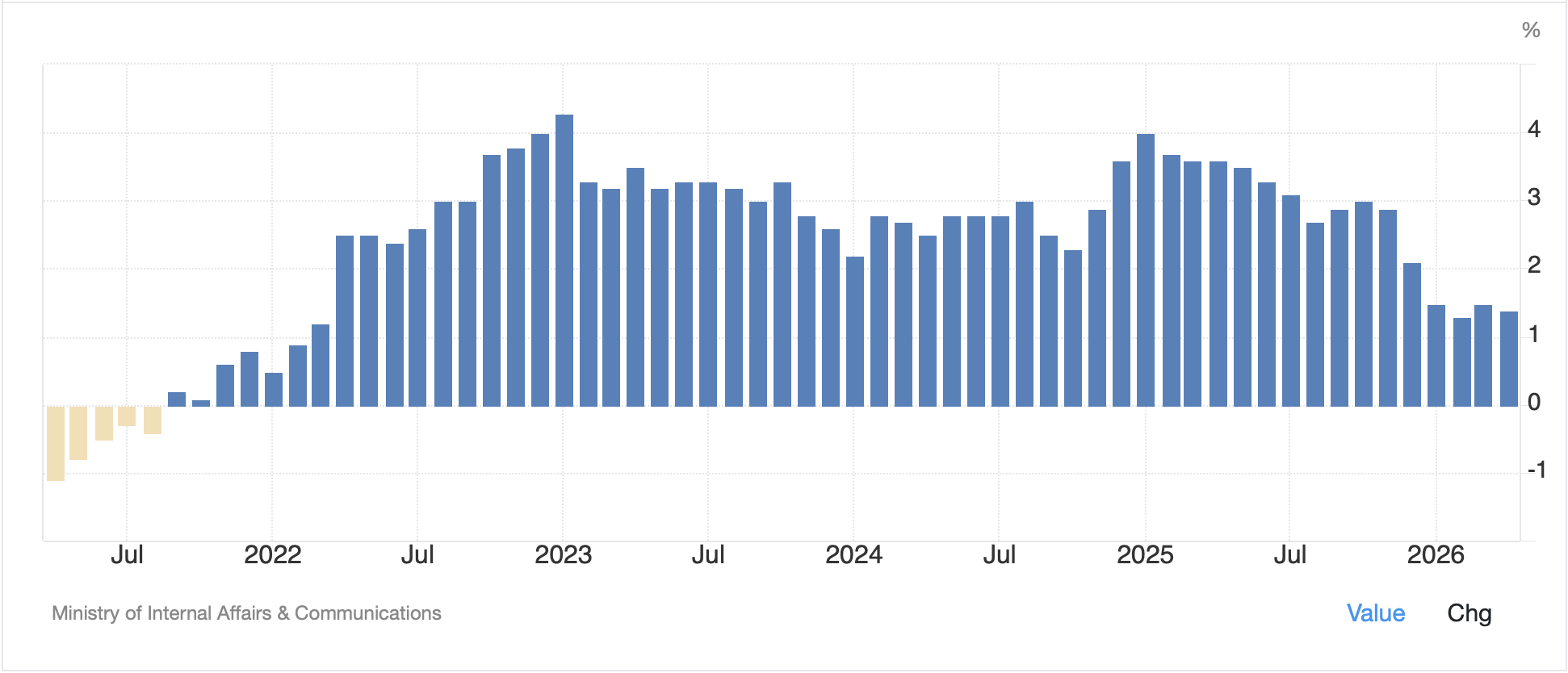

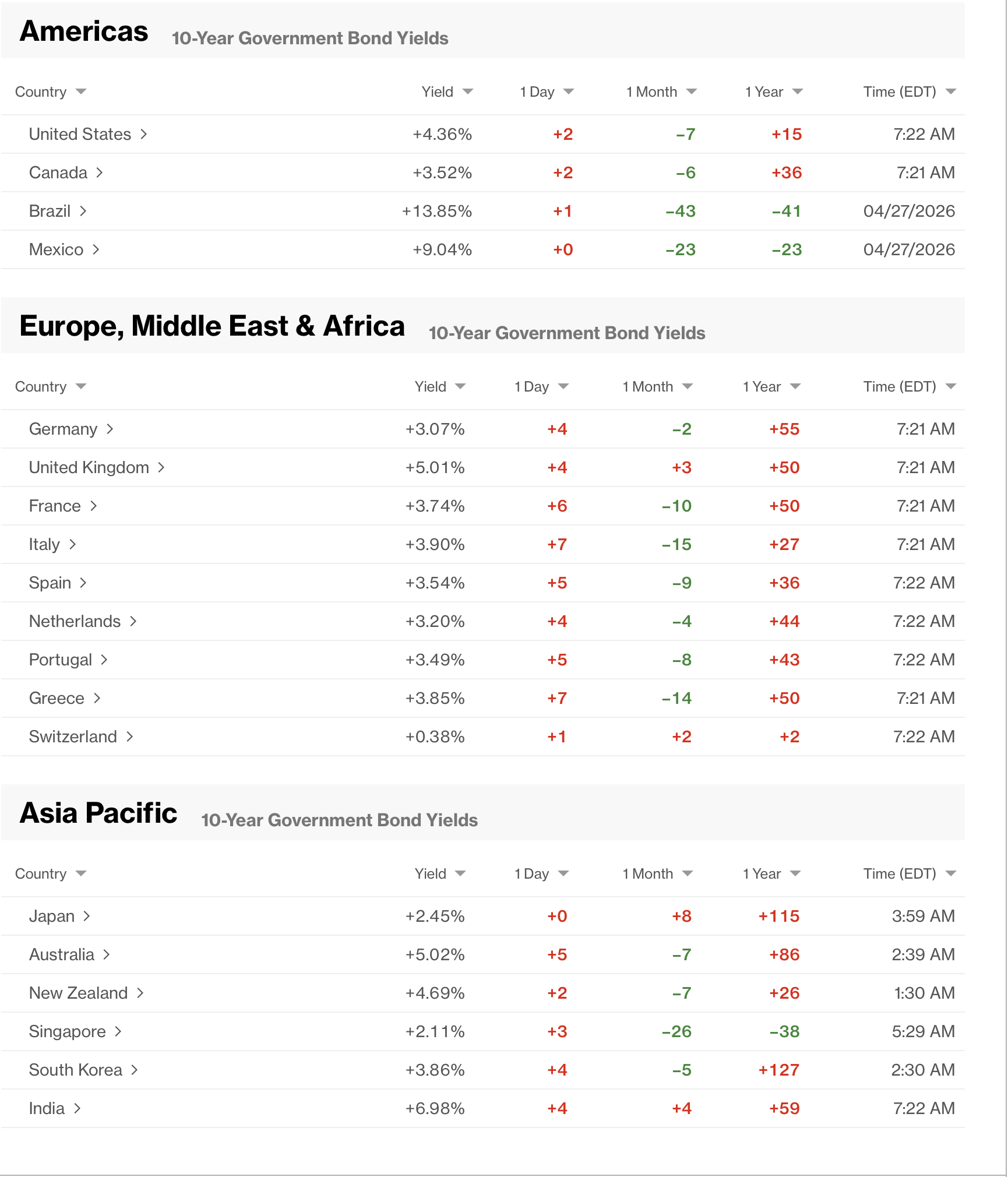

Some have made the point that given Japan is the largest holder of Treasury securities in the world (other than the Fed) and that they would need to sell their Treasuries to fund intervention, this was the driving force. Certainly, the US is not keen to have holders sell their bonds at this point. As you can see in the chart below, this intervention has had a larger impact than the previous bouts which were solo Japanese efforts.

Source: tradingeconomics.com

At the dollar’s low, the yen appreciated about 5% in the past two sessions, certainly a very large move. One of the other things that was interesting was that ostensibly, the Treasury sold EURJPY, not USDJPY. Perhaps they had extra euros lying around they no longer wanted. According to BOJ data, it appears the Japanese spent something like $33 billion on the intervention, but I have no indication as to the US effort.

Joint intervention is pretty rare, with the last time being in the wake of the earthquake/tsunami at Fukushima in 2011 when the yen strengthened dramatically. But it also has a better track record than solo intervention, although absent significant fiscal changes, on both sides of this equation, I suspect that within a few months, the yen will weaken again.

Ok, I feel like that’s enough for one morning. The oil story, as I mentioned, is that the President has called off the mooted weekend attacks and diplomacy is back on the table. Interestingly, the metals markets are not as excited by that with gold (+0.15%), silver (+0.6%) and copper (+0.75%) all higher, but not by very much, especially given the size of the decline in crude prices. And product prices (gasoline -3.4%, heating oil -3.0%) are also sharply lower.

As also mentioned above, bond yields have backed off with European sovereigns sliding far more than Treasuries, between -6bps (Germany, Netherlands) and -9bps (UK, Italy, Greece). However, JGB yields (+3bps) did not get the memo although I suppose that has more to do with the belief that the BOJ is going to be forced to hike rates as part of the joint US-Japanese currency efforts.

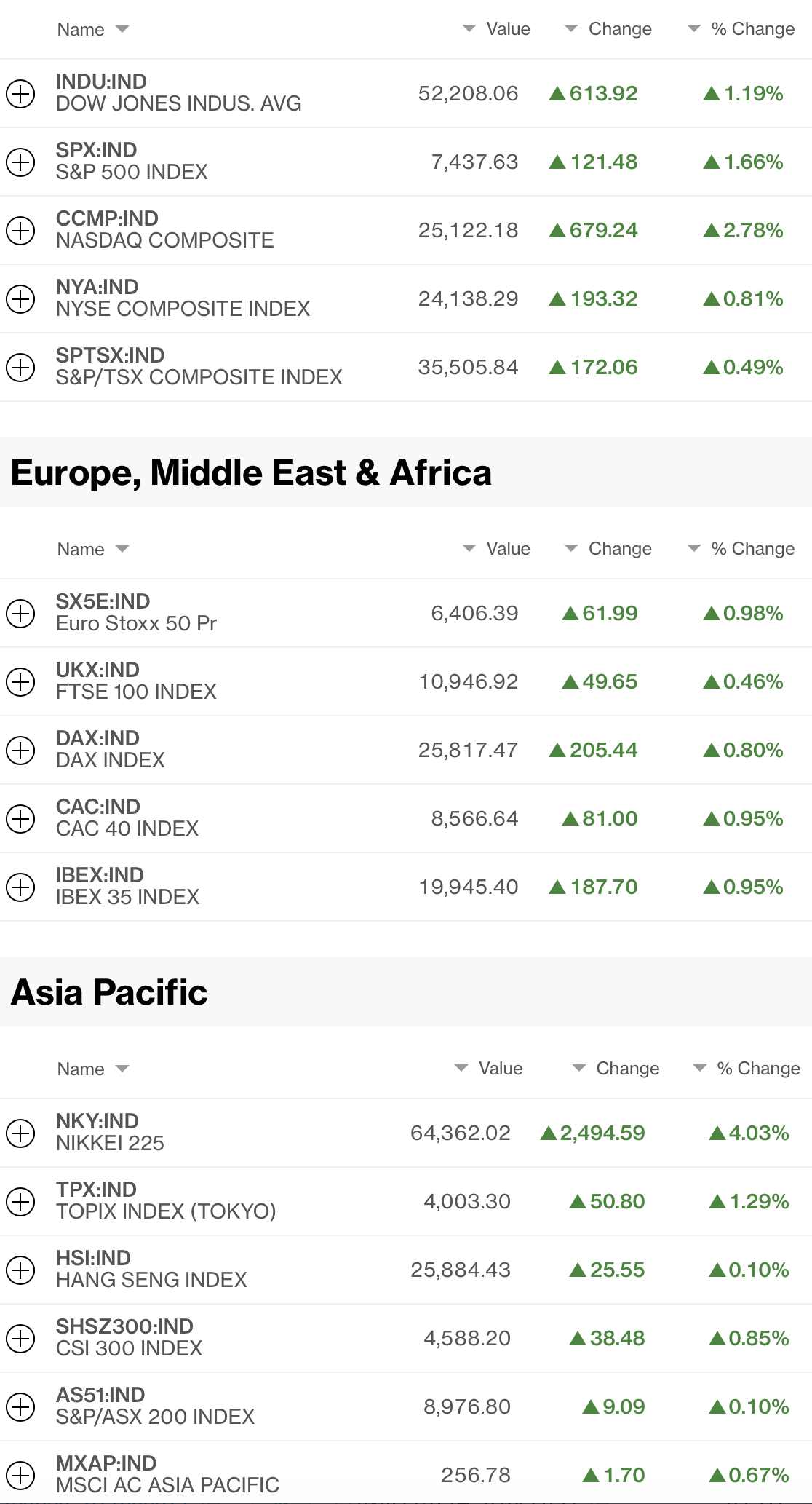

As to the equity markets, after Friday’s US rally, the picture in Asia was mixed, despite the oil price decline, although for Japan, a stronger yen is often a problem for Japanese equities. The worst performers were Korea (-5.1%), Tokyo (-0.9%) and China (-1.0%) while much of the rest of the region followed the US higher (HK +0.5%, India +0.7%, Taiwan +0.6%, Australia +0.5%) with the smaller exchanges mostly higher as well.

In Europe, things are generally bright with Germany (+1.4%), France (+1.3%) and Spain (+0.75%) all nicely higher despite (because of) modestly weaker PMI data although the UK (0.0%) has not been able to overcome its PMI weakness. Now, in fairness to the UK, its 51.9 reading, while weaker than last month and forecast, is still about the best in Europe. As to US futures, they are all in the green, led by the DJIA (+0.8%) at this hour (7:00).

Finally, the dollar is kind of confused overall. The big winner today is KRW (+1.0%) although that trade has been ongoing for more than a month and is approaching an 8% gain over that period. The yen (+0.4%) continues to climb, albeit less aggressively, although the other G10 currencies are generally under pressure (GBP -0.15%, AUD -0.3%, CAD -0.2%, NOK -0.6%).

However, I must mention something that Alyosha wrote this morning in Market Vibes that is worth considering; two of the major positions in markets were short bonds and short yen. Joint intervention by the US and Japan to sell EURJPY has likely forced a lot of covering in both of those markets and it would not be surprising to see more activity like that and further short covering. Japan is the largest holder of French bonds as well as Treasuries and could easily sell those without a peep from the US.

Ok, I have gone way over my daily quota this morning, although there were a couple of really big, and complex stories to discuss. On the data front, today brings ISM Manufacturing (exp 54.0) and I will delve into the rest of the week’s data, including Friday’s payroll report tomorrow.

Good luck

Adf