Some mornings the quiet is real

With limited news of appeal

But traders still need

Their families, to feed,

A story far less than ideal

Yes, oil prices have traded a bit higher overnight and this morning, albeit amid extremely low volumes. In fact, it is the volumes that speak to how little people seem to care about markets right now. We are seeing extremely low volumes across oil, gold, stocks, bonds and even FX markets are quiet. It’s not that they haven’t moved a bit, it’s just that there is no conviction amongst the trading community as to where things should be heading.

Of course, this is never true of the narrative community, who will spin up something to get clicks, but frankly their stuff, which is often the thinnest of gruel, has even less traction now. Arguably, reading through as much as I could this morning, the most noteworthy thing was the following clip I saw on X (and it is a worthwhile use of 13 seconds, I assure you) showing Representative Ilhan Omar discussing World War Eleven. I wish there was more to say, but since there is not, let’s head to the markets.

The most relevant argument in markets right now is how long can Iran hold out while their revenue stream is stopped by the US naval blockade and correspondingly, how long before they have to start shutting in production? How full is their storage? I have seen estimates from what I believe are credible sources of between half full and 80% full which would mean, even in the best case for them, they have about another 2 weeks before shut-ins begin. And if that happens, they are looking at the permanent destruction of upwards of half their current output. In other words, this war is not merely existential for the IRGC and their grip on power, but potentially for Iran’s longer-term future as an economy.

In the meantime, oil prices (+3.3%) continue to grind higher on limited volumes as you can see in the chart below with the lower bars indicating volumes.

Source: finance.yahoo.com

As consumers, we are all feeling the pain of this price action, but BP just reported record profits, and we can expect similar outcomes from all the oil majors, making hay while the sun shines as all corporates do. At the same time, gold (-1.6%) and silver (-3.2%) continue their direct negative correlation to oil. This relationship seems quite robust at this point. It appears that the ongoing dollar strength on the back of the rise in oil prices is undermining the status of gold as a haven asset. I continue to believe this is a temporary phenomenon, but for those long gold, it is nonetheless a painful reminder of how markets can remain perverse.

Speaking of the dollar, yesterday’s modest declines have been reversed this morning with the greenback gaining on the order of 0.25% this morning across the board. The biggest news here was the BOJ meeting last night where, as expected, Ueda-san left policy unchanged, although the vote was 6-3, with the three dissents seeking a rate hike. From what I can tell, Ueda-san prattled on for an hour in his press conference without giving any clear direction as to the future, confusing one and all by explaining they may not reach their objectives but may raise rates anyway. You can see in the chart below when Ueda started speaking as it initially sounded hawkish, but here we are, 7 hours later and it was as though he never opened his mouth.

Source: tradingeconomics.com

The overriding concern in the yen is whether it will weaken through (dollar above) the 160 level, which it briefly touched back in late March, but has since been trading just below. That is perceived by many as the ‘line in the sand’ regarding intervention. However, if we go back to the summer of 2024, when the BOJ last intervened, USDJPY was pushing 162 before they pulled the trigger as you can see below. It certainly suits them that the market is afraid of pushing this envelope, but my take is it will happen before too long.

Source: tradingeconmics.com

As to the rest of the FX space, zzzzz is the story. Perhaps the other interesting thing is that NOK (-0.15%) is weaker despite oil’s climb. Everything else is softer vs. the dollar by -0.2% and -0.4% with no real outliers. FX is just not that interesting, like most markets these days.

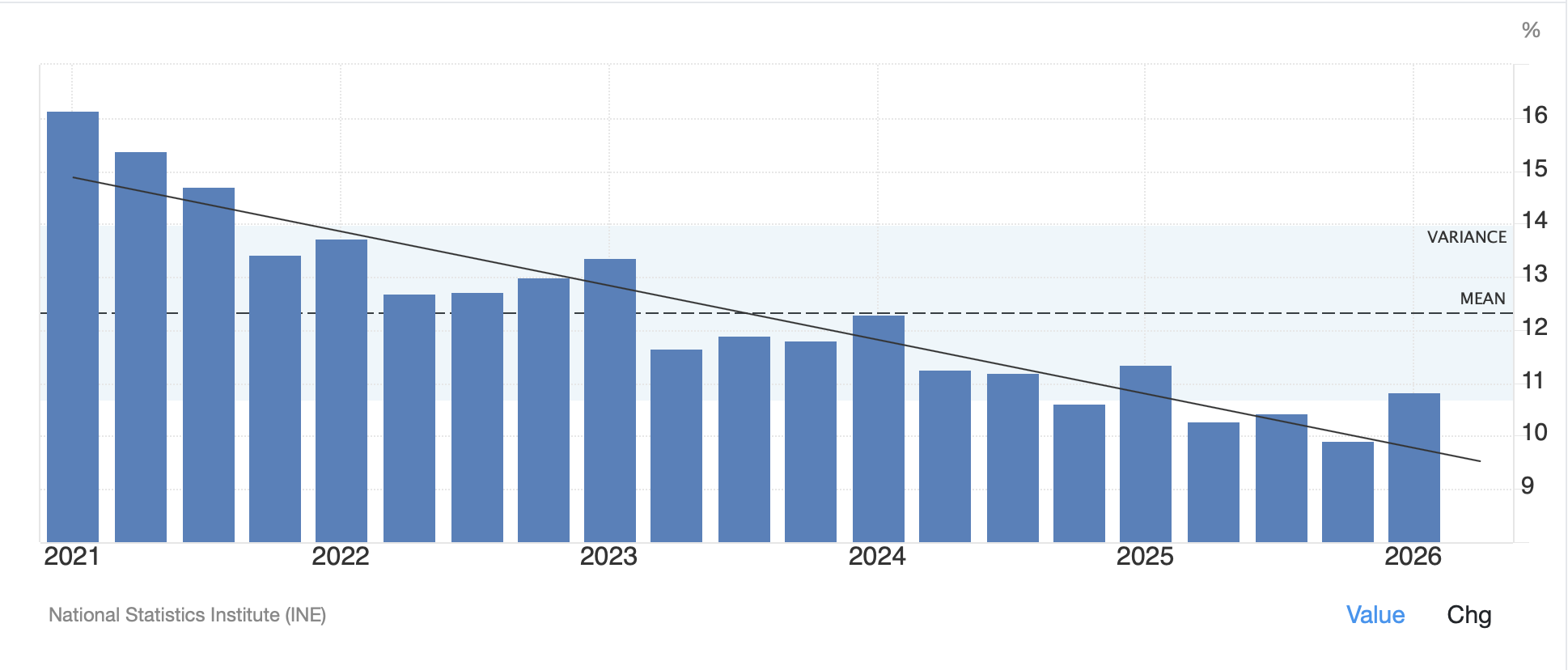

In the equity space, yesterday’s US performance was uninspiring, but we saw more weakness (Tokyo -1.0%, HK -1.0%, China -0.3%, India -0.5%, Australia -0.6%) than strength (Korea +0.4%, Malaysia +0.7%) across Asia. However, there are no new stories to drive things here with the Iran war and energy prices the only topic of note. In Europe, markets are feeling better this morning with gains across the board led by Spain (+1.0%) and the UK (+0.6%). I must admit I am confused by the Spanish performance as the only data point of note released this morning was Spanish Unemployment which jumped to 10.83% (such precision), far above last month’s 9.93% and a full point above economists’ forecasts. But I guess if you look at the longer-term history of Spanish Unemployment, this is still far better than it has been in the past and the trend remains intact.

Source: tradingeconomics.com

Meanwhile, US futures are pointing lower at this hour (7:25) with OpenAI having missed its own targets for user acquisition undermining the overall AI thesis thus far this morning. Plenty of time for that to change though, at least based on how buying remains the default position.

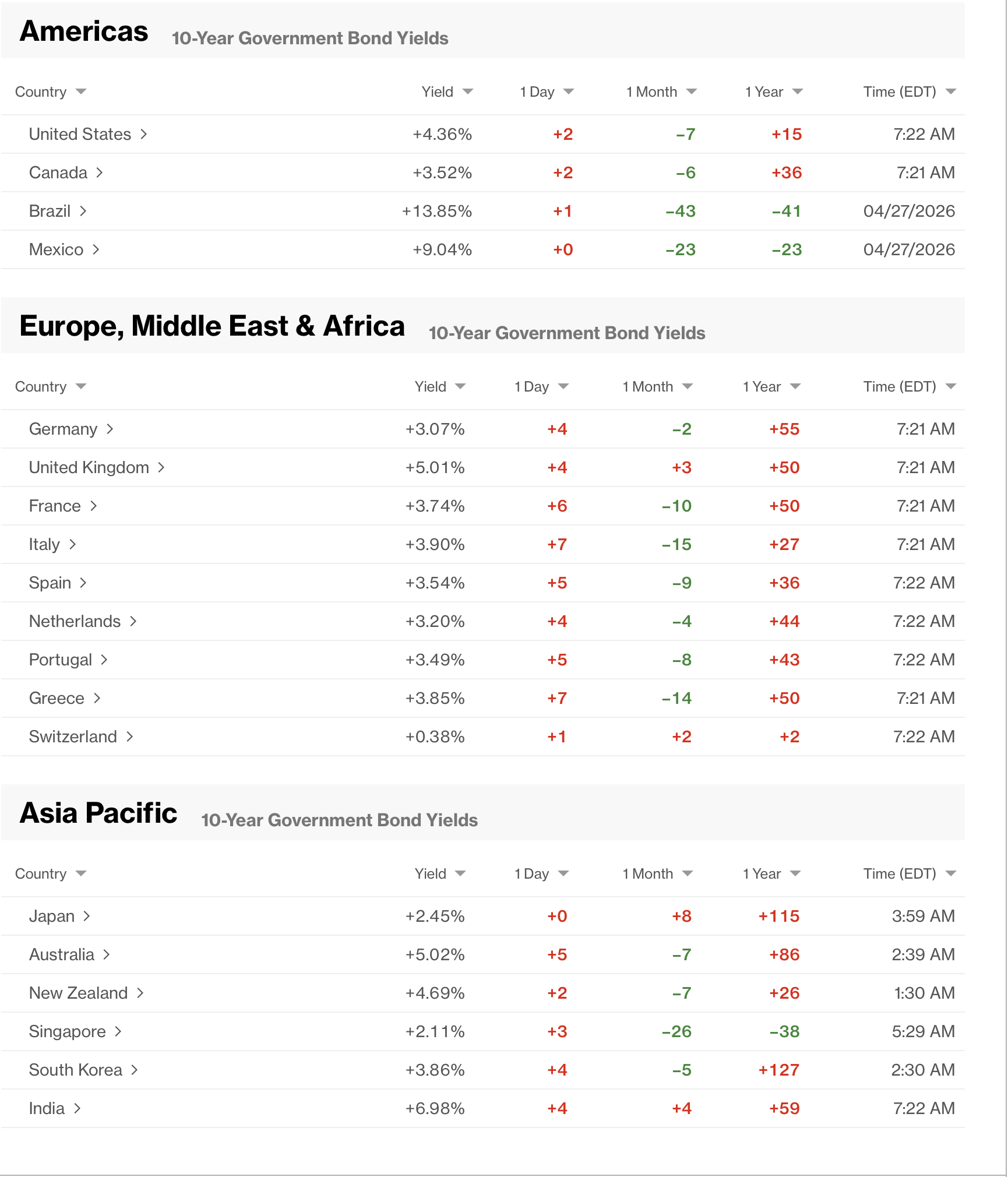

Finally, bond markets have sold off with yields continuing to edge higher across the board. While it’s not really a rout, as you can see from the Bloomberg screenshot below, every European sovereign yield is higher along with treasuries, although JGB’s managed to remain unchanged overnight.

Certainly, there is nothing new in the bond market right now, although I imagine as the Iran war drags on, we will see increased government borrowing across the board which ought to pressure yields higher.

And that’s it, really, for this morning. We see the Case-Shiller Home Price Index (exp 1.1%) at 9:00 this morning and Consumer Confidence (89.0) at 10:00. Neither of these is going to matter to traders anywhere, not even algos.

Until there is a change in the situation in Iran, it is hard to see more than lackluster interest across most markets. I imagine that if this extends for weeks, the offsetting forces of reduced supply and demand destruction will find an equilibrium point, which may well have already been found around $100/bbl. Remember this with respect to the dollar, since oil is priced in dollars almost universally, there is going to continue to be demand for the greenback everywhere in the world. It is hard for me to make a significant bearish case for the dollar right now, at least in the medium or long-term. In the short term, who knows?

Good luck

Adf