While pundits all like to complain

About everything, smart or insane

When stock markets rise

It’s no real surprise

That few people care what they’re sayin’

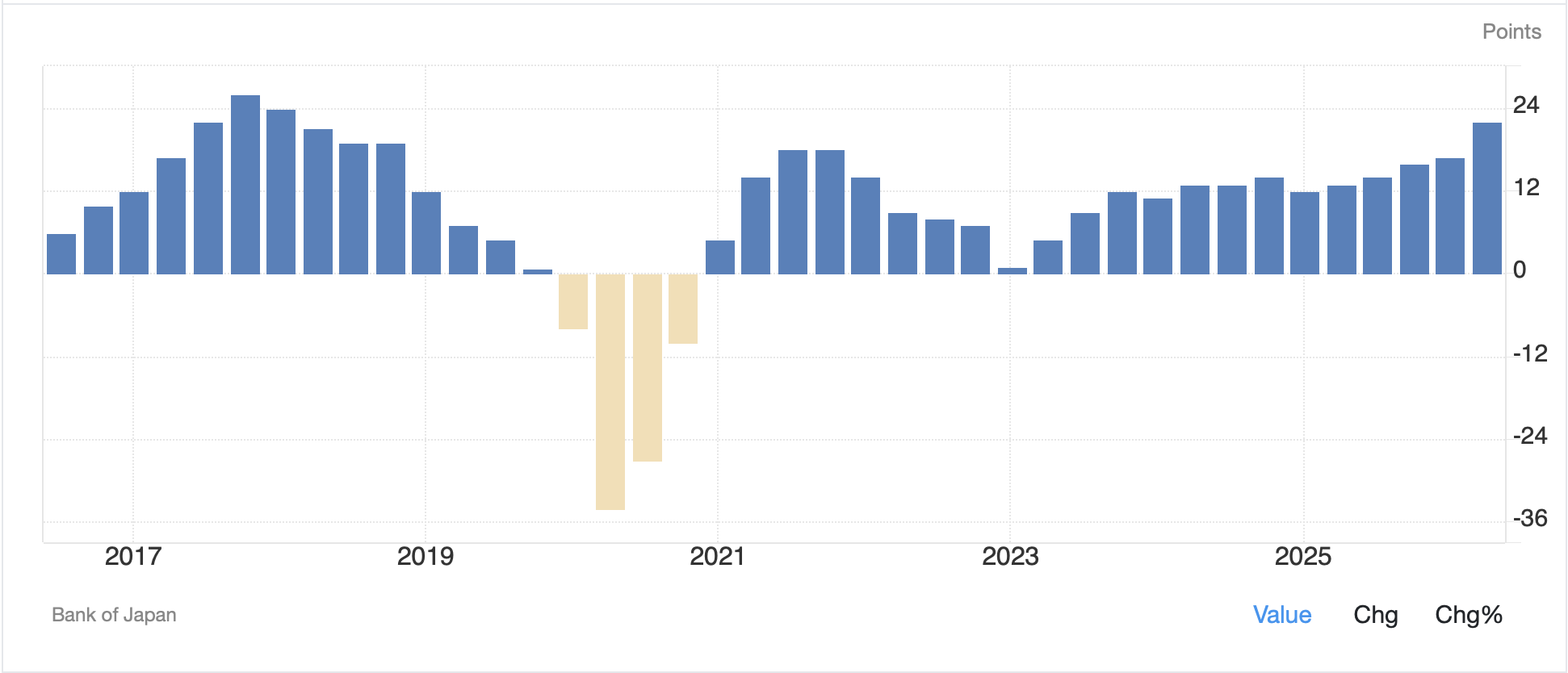

As penance for yesterday’s overly long diatribe, I will keep this morning’s much shorter, especially since there is not nearly so much interesting to discuss. There are still many discussions on the whys and wherefores of the US joining with Japan in intervening in the FX markets, with a pretty even mix of those saying it won’t matter and those saying it is a game changer. As you can see from the chart below, this morning the beleaguered JPY (-0.45%) is slipping a little, but hardly enough to matter in the context of last week’s gains.

Source: tradingeconomics.com

Of course, we won’t really know how effective this bout of intervention has been for at least a few weeks/months, as the history, clearly shown on the chart is a big move higher followed by a gradual depreciation in the yen. Will that play out again? My suspicion is that absent a policy change by the BOJ (i.e. a more aggressive rate hike schedule) or the Japanese government (i.e. less fiscal stimulus) the answer is no. This is especially true if the Fed raises rates, although I still do not believe that is coming soon.

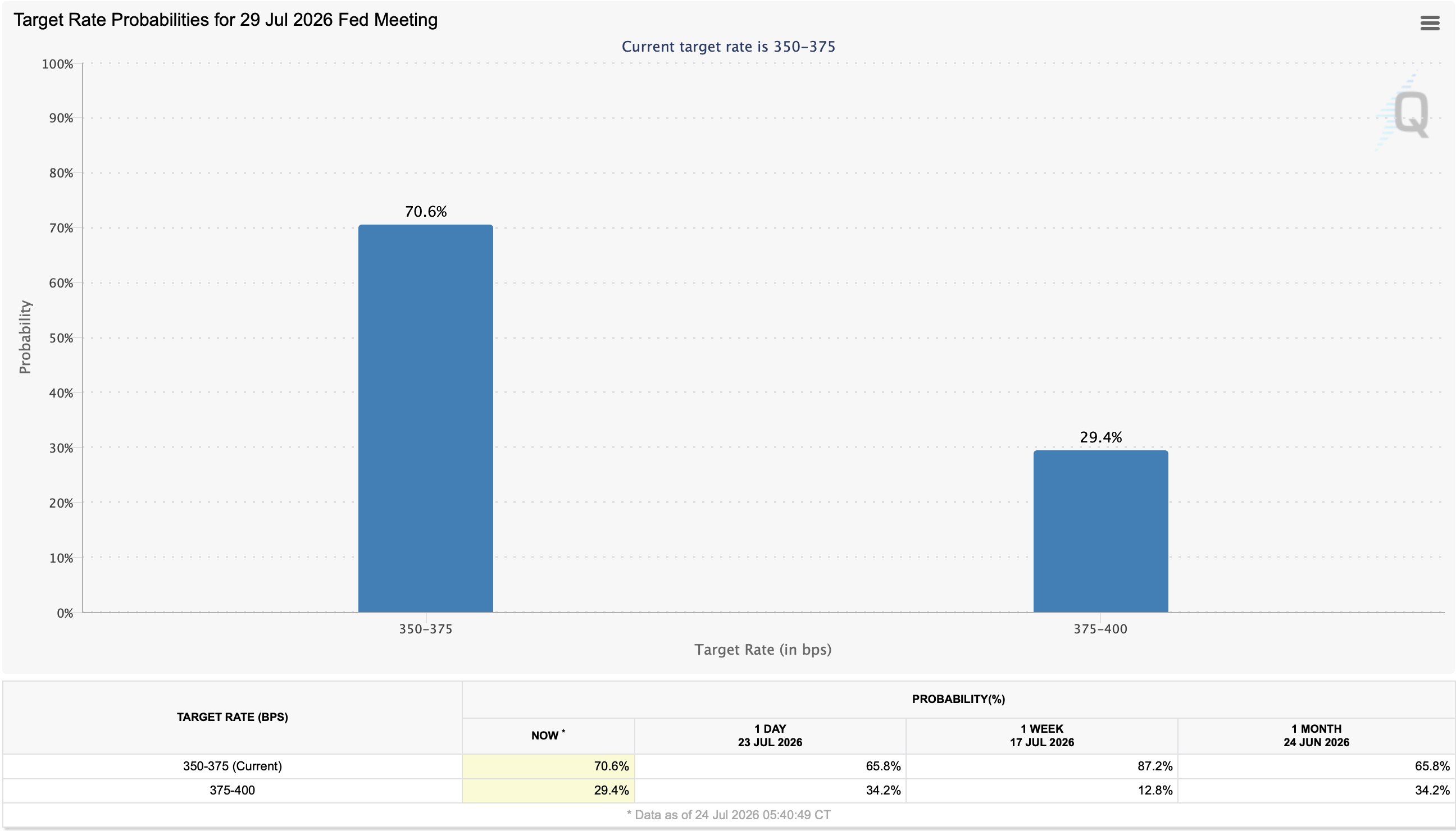

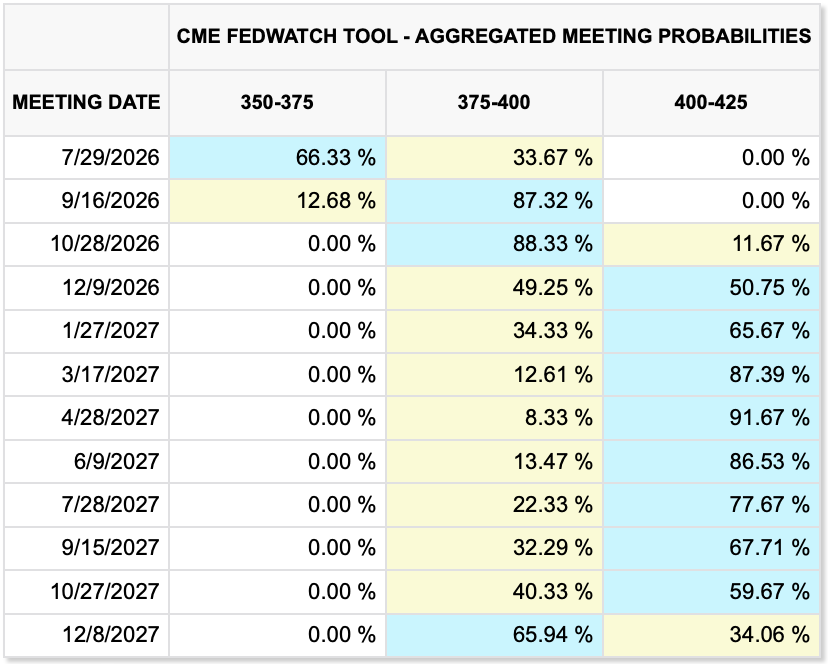

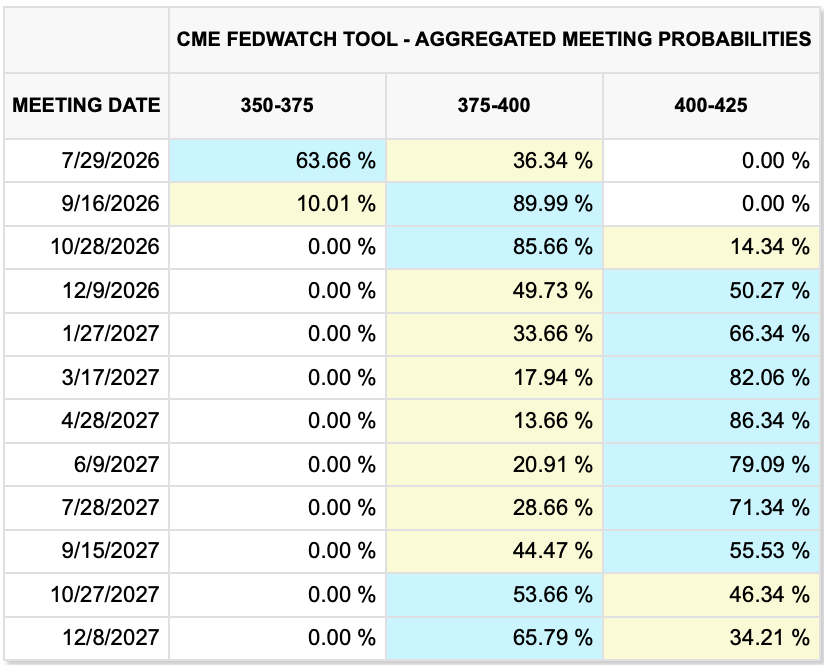

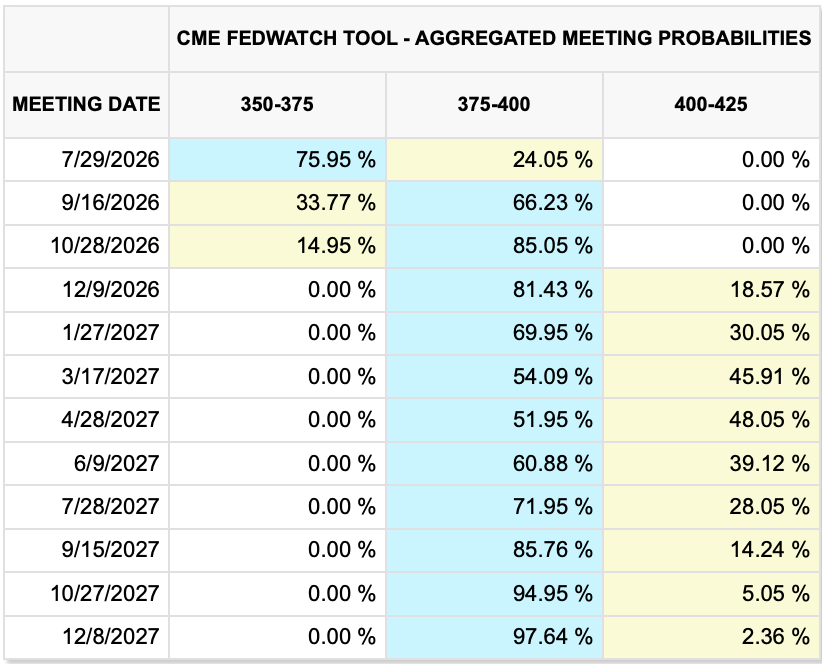

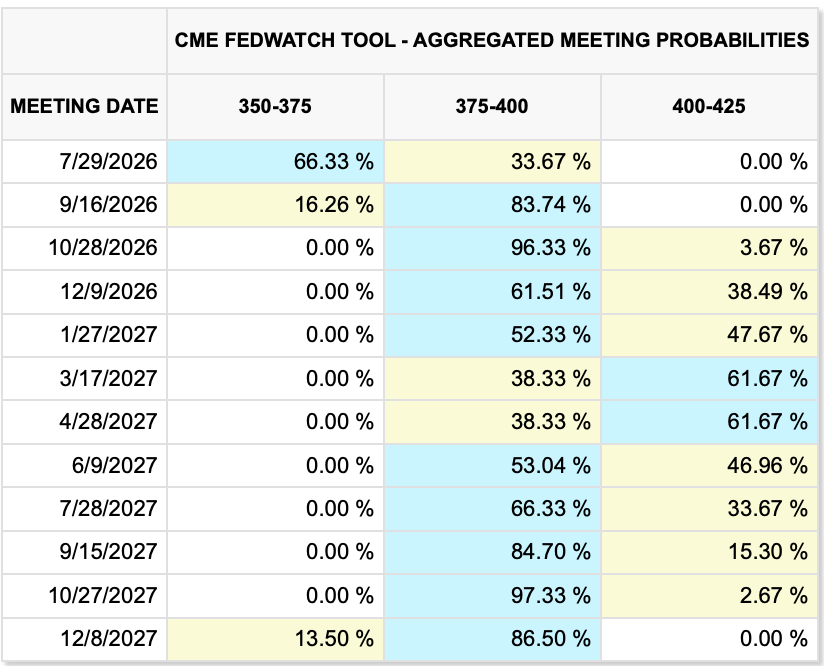

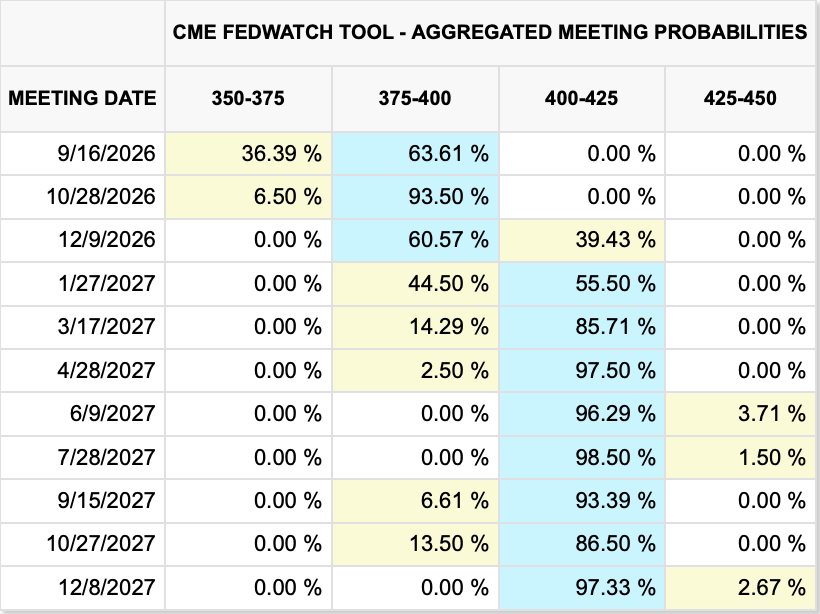

However, it is important to remember that the Fed funds futures market is confident of a hike by October, with a two-thirds probability of one next month as per the below cmegroup.com table.

Turning to the other major discussion from yesterday, the ongoing feedback/blowback from the Fed’s no movement, and more importantly from Warsh’s behavior during the press conference, that too remains a topic of discussion with pundits on both sides adamant that he was either right or wrong on both measures. The only thing I am sure about is that he doesn’t care much about what the pundits are saying. Rather, he is very likely focusing on getting his points across to the rest of the committee, and that will be a tough job.

In 2025, FOMC members gave, on average, one speech a day which added to the forward guidance which was a key tool in their toolbox. You know I often railed against the ongoing verbal diarrhea from these folks as from the best I could tell, nothing said was ever designed to sway opinion, merely to burnish each speaker’s credentials. And they clearly loved the quasi fame that came with it. In fact, I suspect it is that very quasi fame the committee is most reluctant to cede. Chairman Warsh has his work cut out for him.

As to today’s new stories, there are none, at least none of note. There are more conflicting comments from President Trump and the Iranians about negotiations or not. Yesterday’s ISM data was quite positive, coming in at 55.6 vs 54.0 expected, just another indication that the US economy continues to tick along quite nicely. After that, the news heads towards the political with several key primary elections to be held today with DSA candidates picked to win and run in the general elections in November.

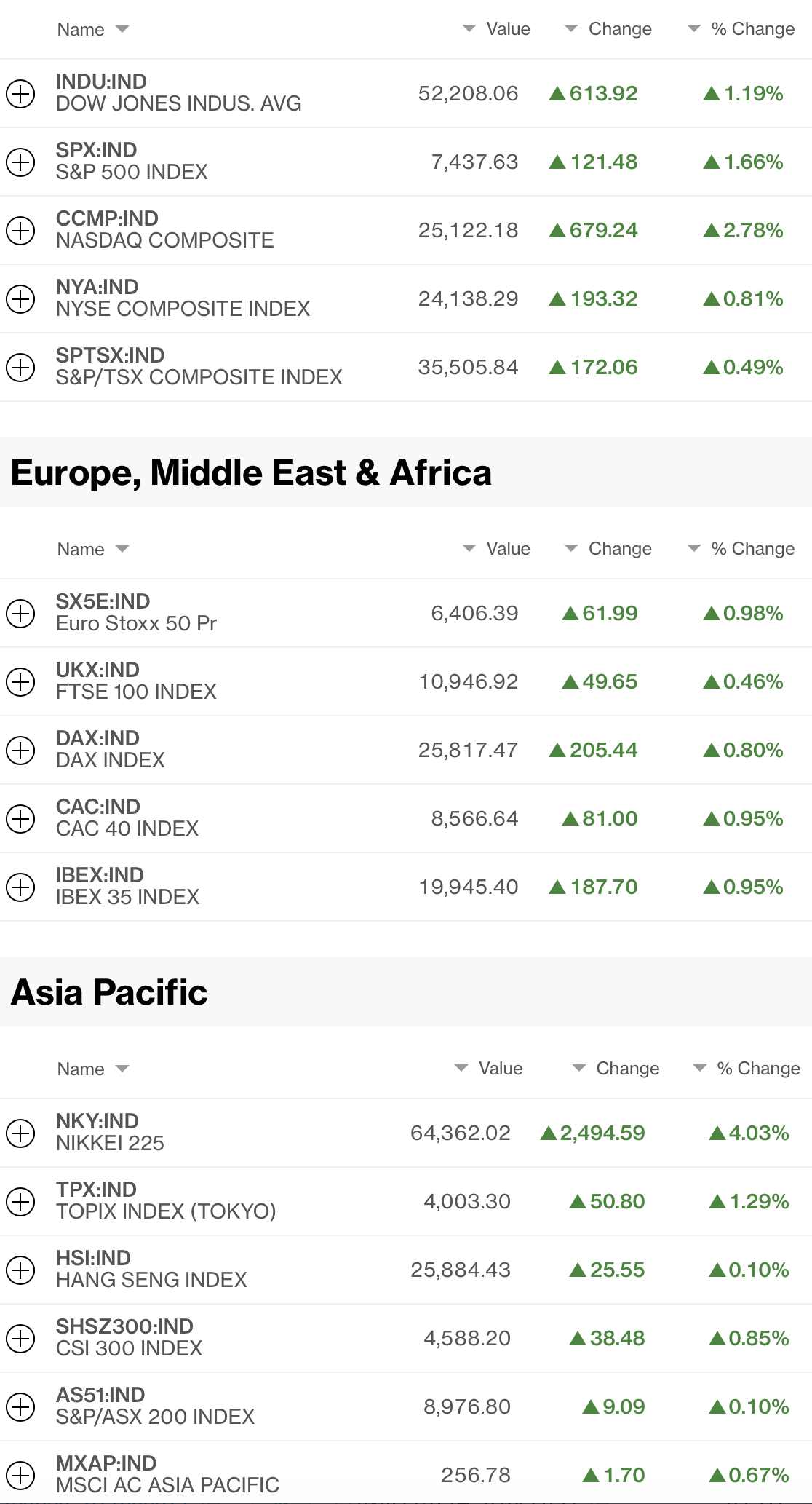

But what has everybody happy is the fact that equity markets are showing strength once again. I read that of the S&P companies that have already reported, 85% have beaten estimates, a much higher than normal percentage (76% is the norm), and another positive for market bulls.

So, let’s take a look at how markets behaved overnight with that theme. The strong US performance was followed by a more mixed session in Asia, although there were more gainers (Tokyo, China, Korea, Australia, Indonesia, New Zealand) than laggards (HK, India, Philippines). The tech story remains the major story since the oil story has become so confusing on a daily basis, I feel like most investors have moved on. Meanwhile, in Europe, it is a broadly positive session as well led by Germany (+0.6%) and the UK (+0.35%) while France (+0.1%) and Spain (0.0%) are not quite as happy. Arguably, the biggest news in Europe continues to be the unprecedented flood of illegal immigrants into Ceuta, Spain and the punditocracy is actively expressing their opinions on the issue, although whether there is a direct impact on the equity market in Madrid is unclear. Lastly, US futures at this hour (7:20), are all pointing higher again as the market awaits earnings from SpaceX this afternoon after the close.

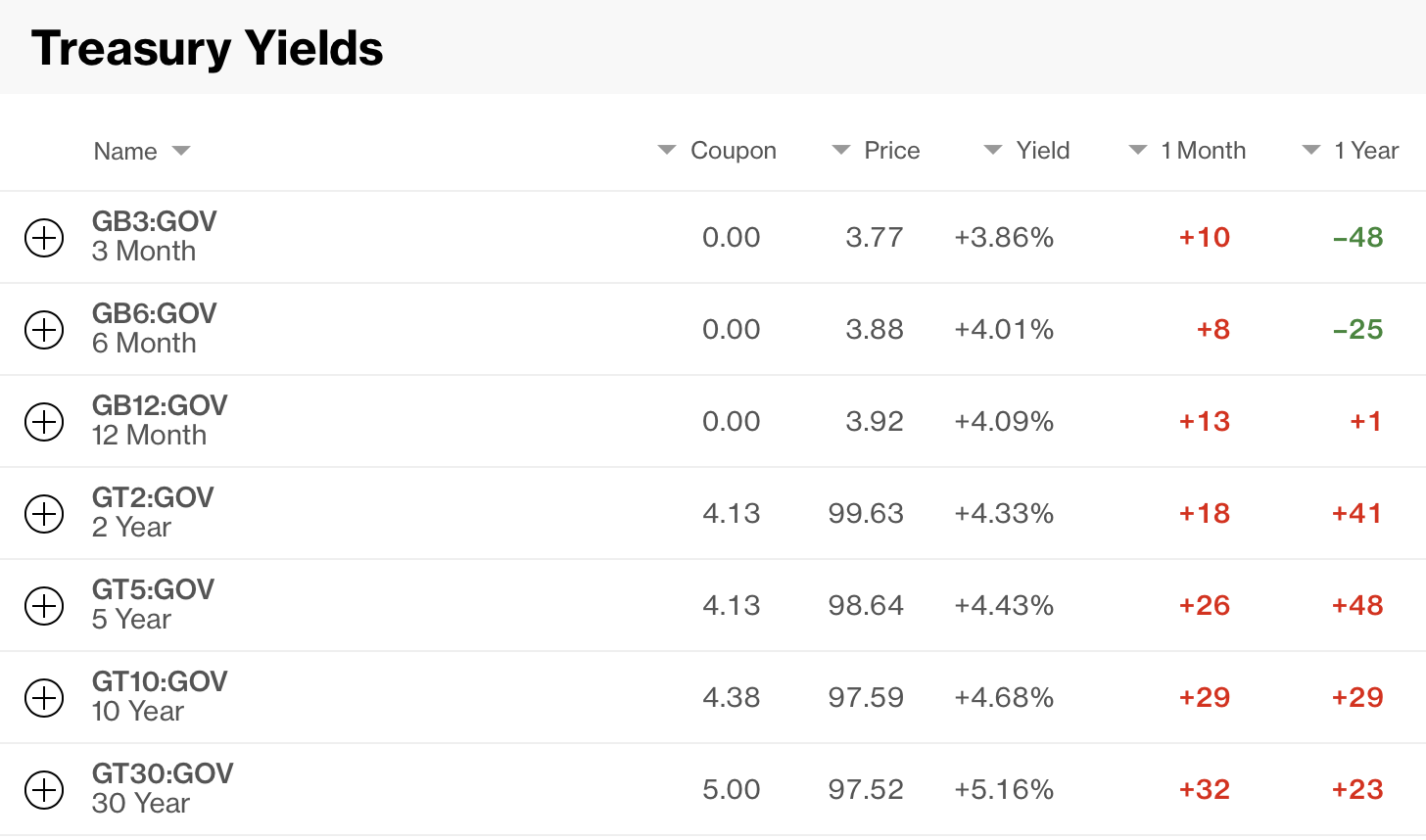

In the bond market, there continues to be a great deal of garment rending and teeth gnashing amongst the financial illuminati as yields hold the bulk of their recent gains. This morning Treasury yields have backed up 1bp after yesterday’s -5bp decline, although European sovereign yields are generally lower by -1bp this morning. As of now, there is no answer to the question of is the bond market focused on inflation or excess issuance although it could well be a little of both.

Remember when oil (-0.8%) was the only market that mattered, and all other trading looked there first. We heard stories about $200/bbl coming soon and tank bottoms as reserves emptied and a growing concern about future economic activity. Well, that never really happened. As I type, WTI is back below $80/bbl and I particularly like this chart that calculates the mean price over the past 6 months ($86/bbl) and shows no trend whatsoever.

Source: tradingeconomics.com

To me, this implies there is a new equilibrium although I suspect that when the hostilities cease, and I believe they will at some point this year, we will see sharply lower prices for crude and products. As to metals markets, they remain relatively uninteresting with modest gains today (Au +0.2%, Ag +2.4%, Cu +1.7%).

Finally, in the FX markets, away from the yen the dollar is under a bit of pressure this morning. First, for all of you who follow the DXY and were excited by the ostensible breakout above 100.50, as you can see in the below chart, that story appears to have ended for now.

Source: tradingeconomics.com

But away from the yen this morning, the rest of the G10 have all shown modest gains led by AUD (+0.5%) after some positive household spending data. Otherwise, 0.1% to 0.2% is the state of the day. In the EMG bloc, ZAR (+0.4%) is the leader of the pack on the combination of softer oil prices and stronger metals prices. Too, BRL (+0.25%) and MXN (+0.25%) seem to be benefitting on the same basis. Otherwise, it’s hard to get excited here. Perhaps another bout of intervention will perk things up, but I doubt that will happen soon.

On the data front, there’s quite a bit to be released this week culminating in the Friday NFP report.

| Today | Trade Balance | -$73.0B |

| JOLTs Job Openings | 7.4M | |

| Factory Orders | 0.2% | |

| -ex Transport | 0.5% | |

| Wednesday | ASP Employment | 70K |

| ISM Services | 54.5 | |

| Thursday | Initial Claims | 202K |

| Continuing Claims | 1790K | |

| Nonfarm Productivity | 0.6% | |

| Unit Labor Costs | 2.1% | |

| Friday | Nonfarm Payrolls | 80K |

| Private Payrolls | 79K | |

| Manufacturing Payrolls | 4K | |

| Unemployment Rate | 4.2% | |

| Average Hourly Earnings | 0.3% (3.5% Y/Y) | |

| Average Weekly Hours | 34.3 | |

| Participation Rate | 61.6% | |

| Consumer Credit | $10.85B |

Source: tradingeconomics.com

In addition, there are three Fed speakers, and I wonder (and am hopeful) that we hear less and less from them going forward. Obviously, all eyes will be on the payrolls on Friday, and we can dive into that later in the week. But today, it is hard to get excited about anything.

Good luck

Adf