Said Bessent, we’re close to a deal

Though not yet the President’s seal

Both sides have agreed

That two months they’ll need

To see if this outcome is real

It can, though, not be too surprising

That stock markets have resumed rising

While oil has slipped

And bond yields, down, dipped

All told, risk is quite appetizing

The major story, although it has been questioned by many, is that there is positive movement toward a deal to end the conflict in Iran. While I’m sure you will have seen the terms, a quick recap shows that there is to be a 60-day ceasefire to work out the final details. One of the things I saw this morning was that Iran would send its nuclear material to China, rather than the US, as a compromise, and frankly, that seems like a fine solution. After all, China enriches the stuff all the time, has many nukes and has never used one. While we may have disagreements with China on a geopolitical basis, Xi Jinping is not a religious fanatic. While Treasury Secretary Bessent made the announcement yesterday, he cautioned that President Trump has not yet agreed the details, but it is certainly a hopeful situation.

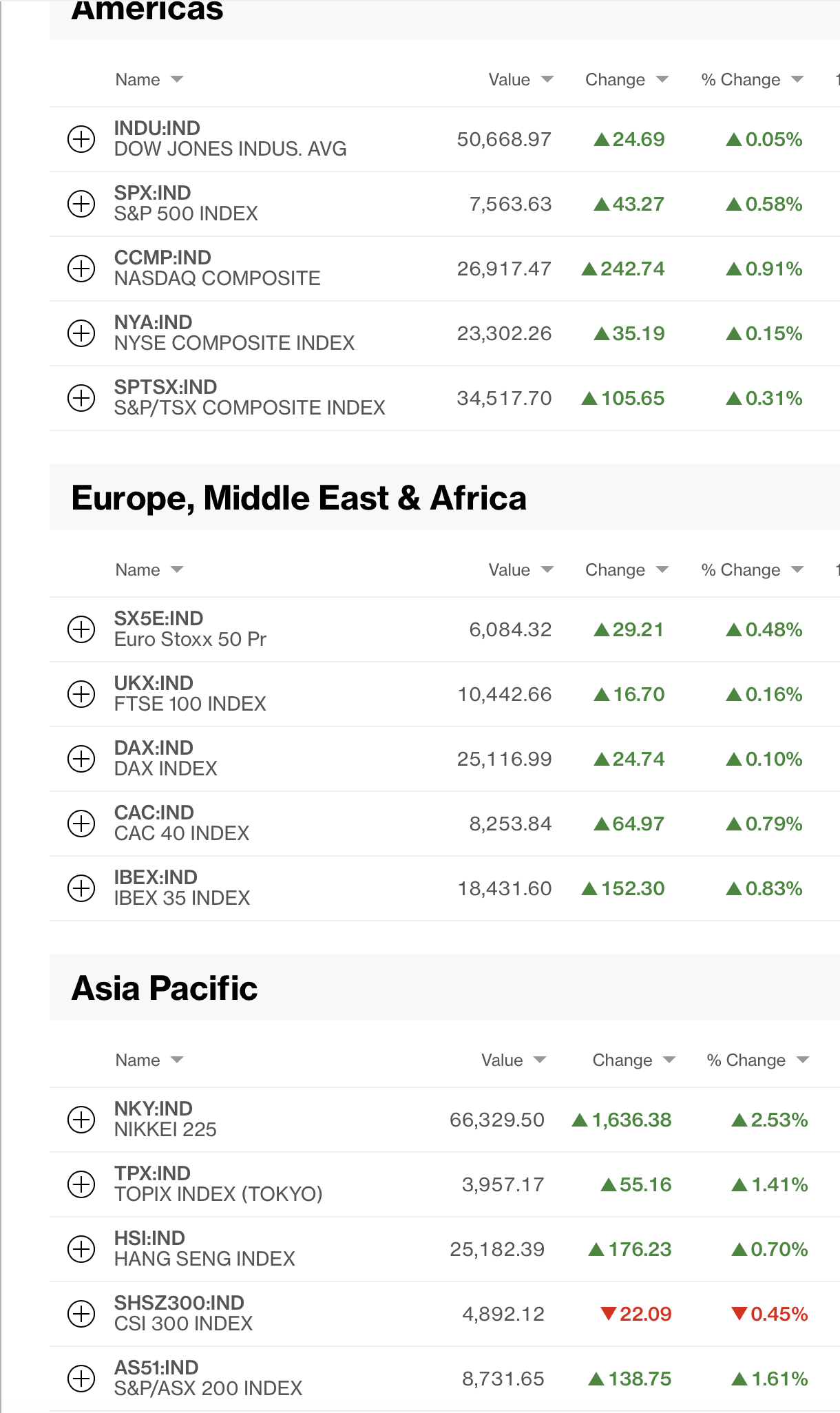

Of course, you know who saw it as a hopeful situation? Risk takers. The Bloomberg screenshot below is indicative of how things are going, with gains everywhere except China, where it appears that concerns over China-EU trade tensions are weighing on companies there. With the US having dramatically reduced its market for Chinese exports, Europe had effectively become the major dumping ground, and now that Europe is starting to push back, the question is what will become of all the stuff they continue to produce. Beggar thy neighbor policies are tougher to inflict on nations that also utilize those same policies. Just sayin’.

Of course, you won’t be surprised that oil prices have fallen further this morning on the news, down another -1.6% and firmly below $90/bbl, actually below $88/bbl as I type as per the chart below.

Source: tradingeconomics.com

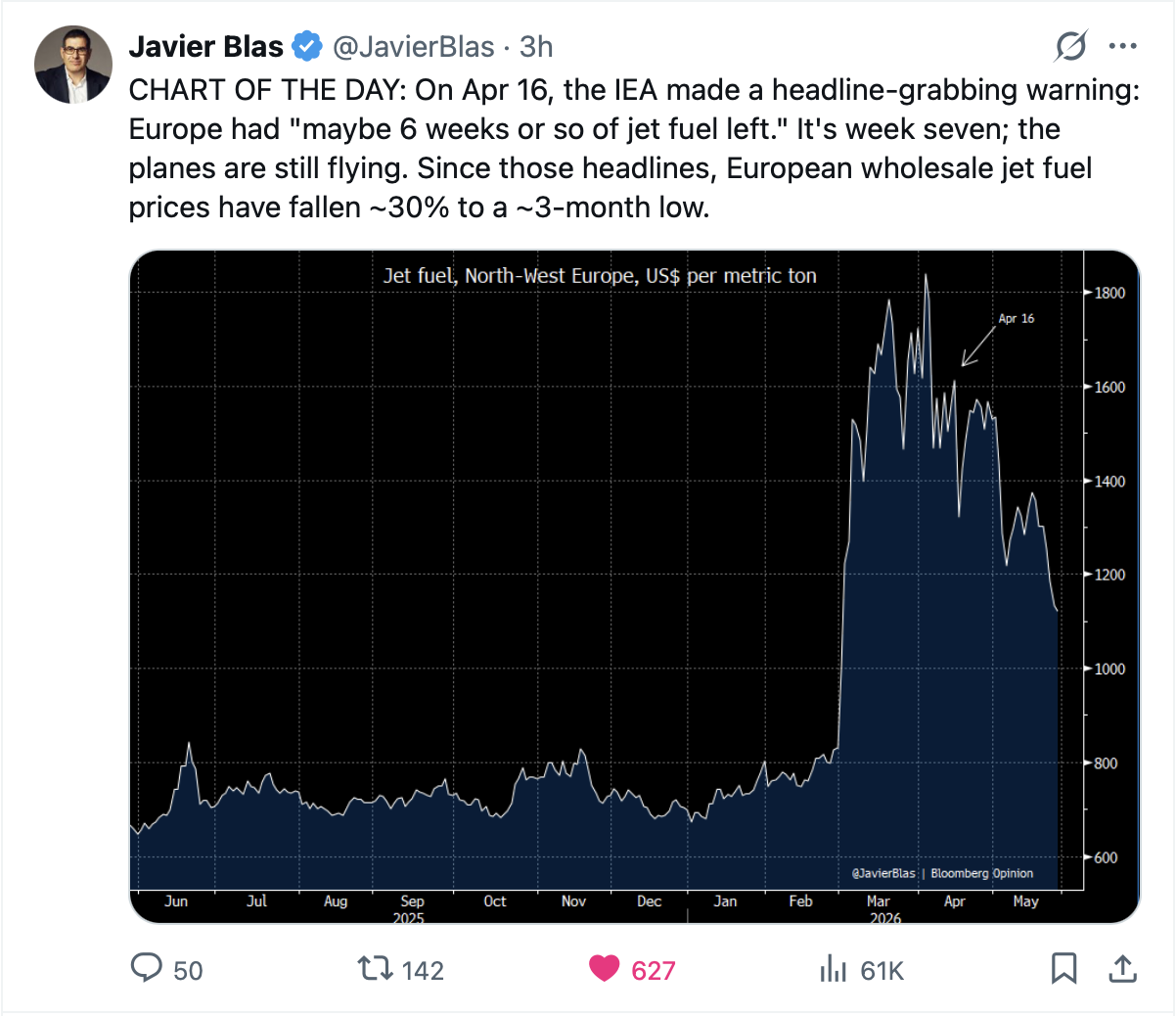

Now, clearly, prices are still substantially above levels seen prior to the Iran conflict, but as of now, the most apocalyptic predictions have simply not materialized. I saw two interesting comments on this subject this morning with very opposite takes. First, Javier Blas, the Bloomberg energy analyst/reporter, posted the following chart for jet fuel in Europe. You may recall that early on, there were many forecasting Europe would run out of fuel and planes would stop flying.

The price action does not indicate a market concerned by imminent shortages of the stuff. In fact, my understanding is that refineries are cracking so much oil to make jet fuel, that there is actually “excess” gasoline being produced, which would help explain my point yesterday about falling gasoline prices as you can see in the below chart. Since May 18, wholesale prices have slipped 19%.

Source: tradingeconomics.com

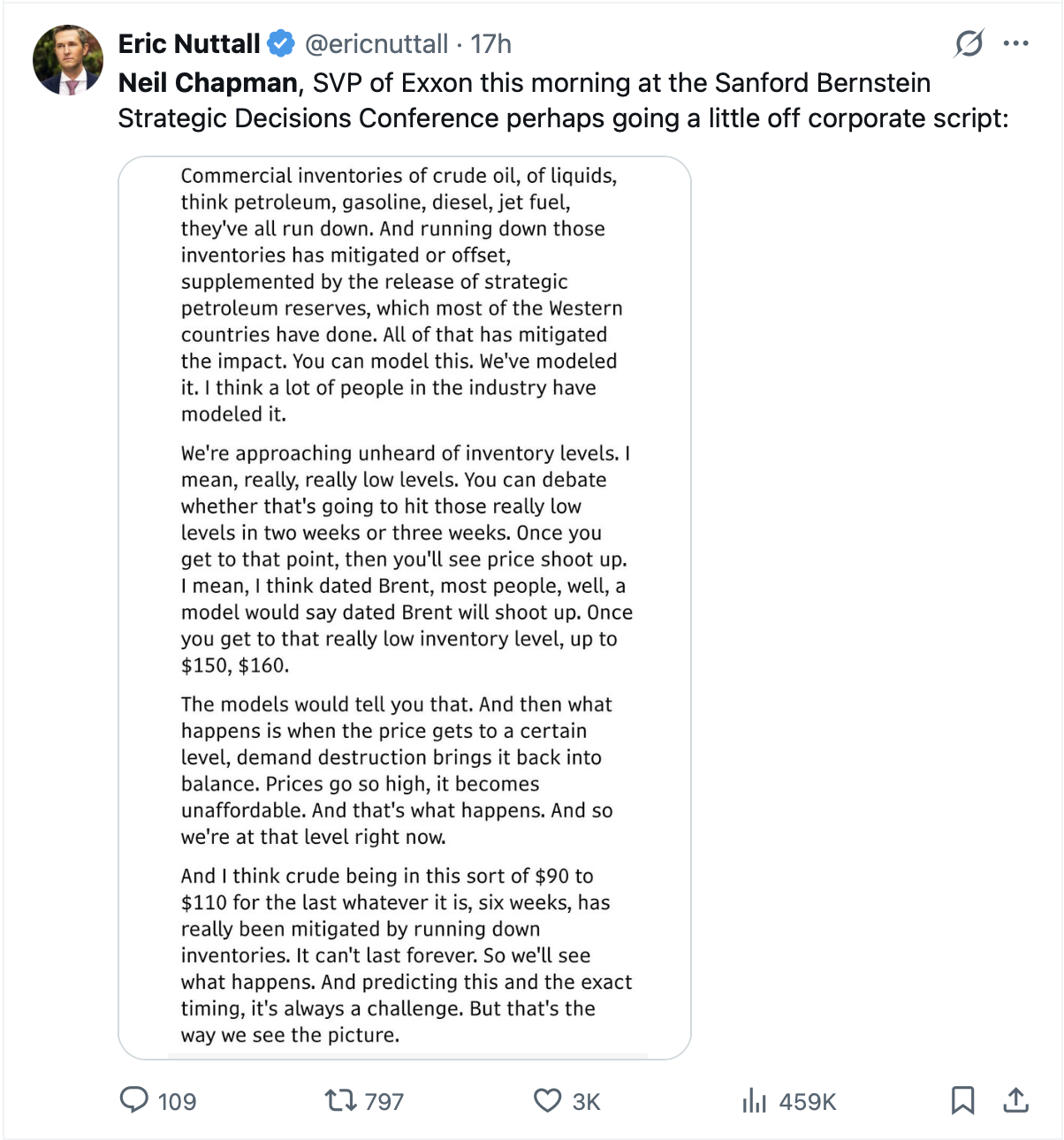

However, there is another side to the argument, the apocalyptic side, which was recently made by Neil Chapman, an Exxon SVP at a conference as per the below X post.

Here’s the thing about comments like this. First, I have no doubt that Mr Chapman is highly competent and explaining what he sees happening. I would never suggest he has any motive other than conveying information he believes is important. But I also have learned, over many years of experience, that arguing with the market is a very painful thing to do. As Mr Keynes reputedly said almost 100 years ago, “markets can remain irrational a lot longer than you and I can remain solvent.”

So, what to think? No matter the pedigree of the individual calling for a significantly different outcome than is current, it is very difficult for me to side with the apocalypse if the market disagrees. And clearly the market disagrees with this thesis. My understanding is refineries are running flat out right now, which means they have plenty of oil to process. If, and it’s a big if, the Iran conflict is truly coming to an end, $70/bbl oil and $3.50/gallon gasoline will be with us by Labor Day. At least that’s my view, and I’m pretty positive on it.

Looking elsewhere, it can be no surprise that bond yields around the world are slipping with Treasuries sliding -4bps yesterday, although they are unchanged this morning. European sovereign yields were also softer yesterday but are now struggling between the positive idea of the end of the Iran conflict and the negative reality that inflation in Europe continues to rise as reported this morning (Italy 3.3%, Germany 2.6%, Spain 3.6%, France 2.8%), which has the ECB set to hike rates at their meeting as per their own market watch tool.

The problem with this is that economic activity across the continent continues to slow (GDP in Italy 0.8% Y/Y, France 0.9% Y/Y), and hiking rates on the back of a supply shock, especially one that has a fair chance of ending soon, would seem to be a catastrophic error in the making. Of course, Madame Lagarde is no stranger to catastrophic errors, so, we should assume they will, indeed, hike rates in two weeks’ time. Even the Fed, no stranger to catastrophic errors, is not prepared to hike rates, although cuts appear to be off the table for now.

Elsewhere, precious metals (Au +0.8%, Ag +0.1%) appear to have put in a short-term bottom while copper (-0.5%) is consolidating after its continued remarkable run.

And finally, the dollar is stronger this morning, not aggressively so, and not universally, but on net I would say. NZD (+0.5%) is bucking that trend as further hawkish comments from the RBNZ Governor have traders looking for a rate hike there while INR (+0.9%) has been the biggest beneficiary from the decline in oil prices as India has been one of the most severely impacted nations from the conflict. Lastly, a note about the yen, where the MOF disclosed that they spent ¥11.73 trillion (~$73.6 billion) intervening in the FX markets last month, a larger amount than had been assumed by the market. Here’s the problem, as evidenced by the chart below, it didn’t do much good, from the peak print of 160.72 on April 30th(the wick of the huge red candle), the yen is not even 1% stronger as of this morning. As well, looking at the chart, you can see their subsequent minor interventions as the spikes down. As I have repeatedly said, if they don’t change policy, the currency will continue to weaken.

Source: tradingeconomics.com

Otherwise, FX is dull and boring today.

Turning to the data, this morning brings the Goods Trade Balance (exp -$86.5B) and then Chicago PMI (50.5). We also hear from 3 more Fed speakers, but it is hard to believe there is any change in viewpoint there. Yesterday’s data was, on the whole, better than expected, I would say. While GDP was a touch soft, Durable Goods was quite robust at 7.9% headline, 1.1% ex Transports. PCE was as expected to a tick softer, although remains well above 3%, let alone the Fed’s alleged 2% target. The biggest concern was Personal Income was flat, although Spending (+0.5%) continues apace. Much has been made by analysts about how the savings rate is collapsing and this presages an economic collapse. But these are the same folks who keep telling us that oil prices are going to explode as inventories collapse. Maybe they are right, but as of now, there is no evidence that is the case, at least based on the data.

What to make of it all? The idea that the Iran conflict is on course to end is clearly the top issue for the market and the economy. I expect that if this is the case, things will get back to “normal” far more quickly than the pessimists insist as the one thing we have learned is that the ability to resume economic activity is quite robust. If risk is warmly embraced, then one would assume that yields will decline and the dollar with them, at least for now. But that also implies that funds will continue to flow into the US markets, which will prevent any significant decline. And I cannot help but look at Europe with the prospect of hiking rates into an economic slowdown and wonder, again, why anybody wants to hold the euro.

Good luck and good weekend

Adf