The crude price continues to fall

But one thing that has us in thrall

Is narrative doom

Where pundits all fume

God dammit, we’ll soon hit the wall

But under the headlines we learn

It’s really not quite the concern

The major details

Of SPR sales

Are by next year all will return

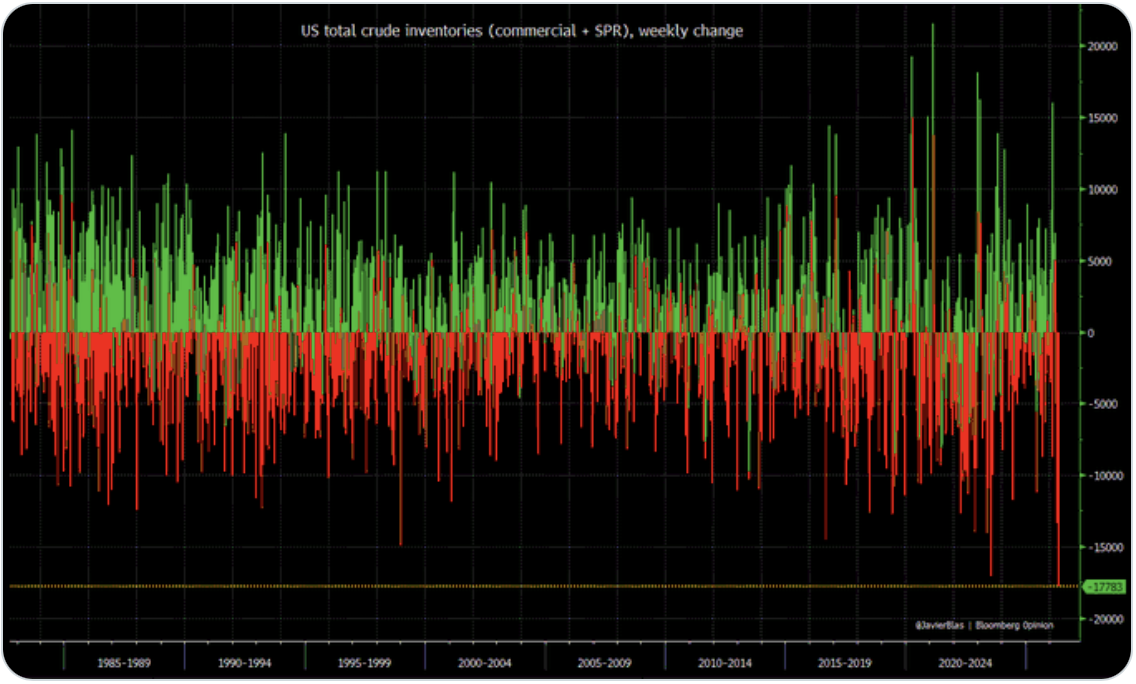

Oil puked yesterday, down nearly -6% despite the news that the EIA inventories fell dramatically as well. The total draw was just under 18 million barrels, which on the surface is a new record draw. Charts like the below were all over the place as the narrative writers were busy calling for the end of American Exceptionalism er.. the dollar, er.. US energy dominance.

However, I am not convinced that is the case. The first clue is that oil prices collapsed and if the doom porn was accurate, I don’t believe that would be happening. Instead, there is a far better explanation which I am lifting in its entirety from my friend JJ who writes market vibes and has been trading oil for as long as I have been trading FX. If you care about oil markets, you really need to be reading what he says.

The DOE is releasing 172 million barrels of SPR oil with swaps rather than outright sales. Companies borrow SPR crude now and they pay it back plus a premium in more barrels later which based on the curve could be as much as 25% more barrels. This is explicitly designed to grow the reserve by at least 200 million barrels “at no cost to the taxpayer” and it will.

These are not “draws.” They are loans. The swaps are repaid ratably from November 2026 through September 2028. Earlier return structures have lower premiums.

In other words, the administration is taking advantage of the major backwardation in the oil futures curve and selling prompt and buying forward, taking oil instead of cash at a discounted basis. If we understand this, it helps us understand why there is no panic in the oil markets, at least not in the US WTI market.

And, whether or not the IRGC is negotiating or getting ready to annihilate us all, my sense is this is a much bigger part of the picture than anyone is considering, except actual oil traders. But it is not nearly as sexy a narrative, especially if you hate President Trump and can try to tar him with yet another problem.

And as we have learned lately, as goes oil, so goes the entire market. So, it should be no surprise that equities and precious metals rallied as oil fell alongside Treasury yields and the dollar. Pretty ordinary actually.

For Jay in his last time as Chair

Where soon, Kevin Warsh we’ll compare

The Minutes revealed

That rises in yield

Would soon change to common from rare

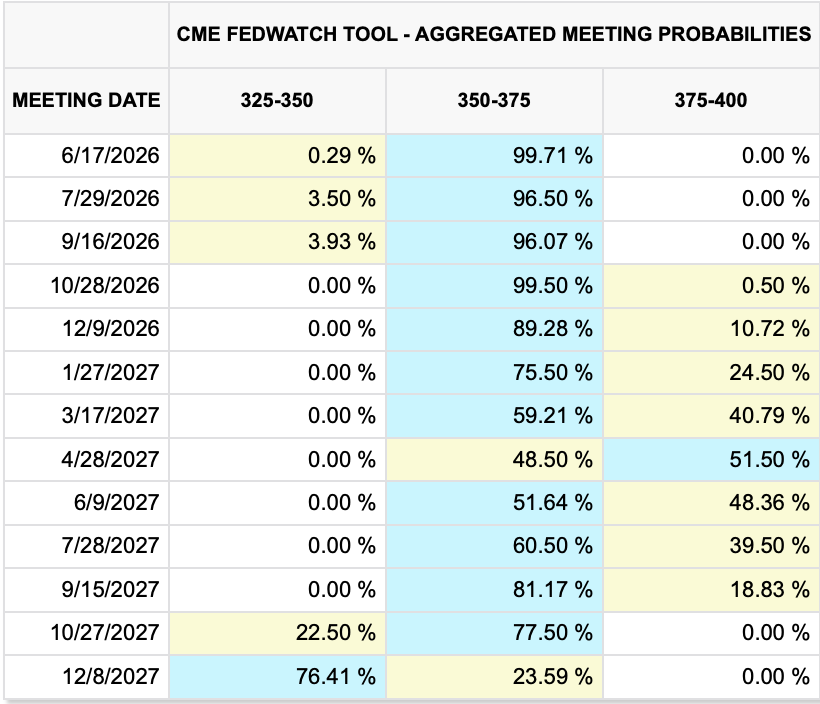

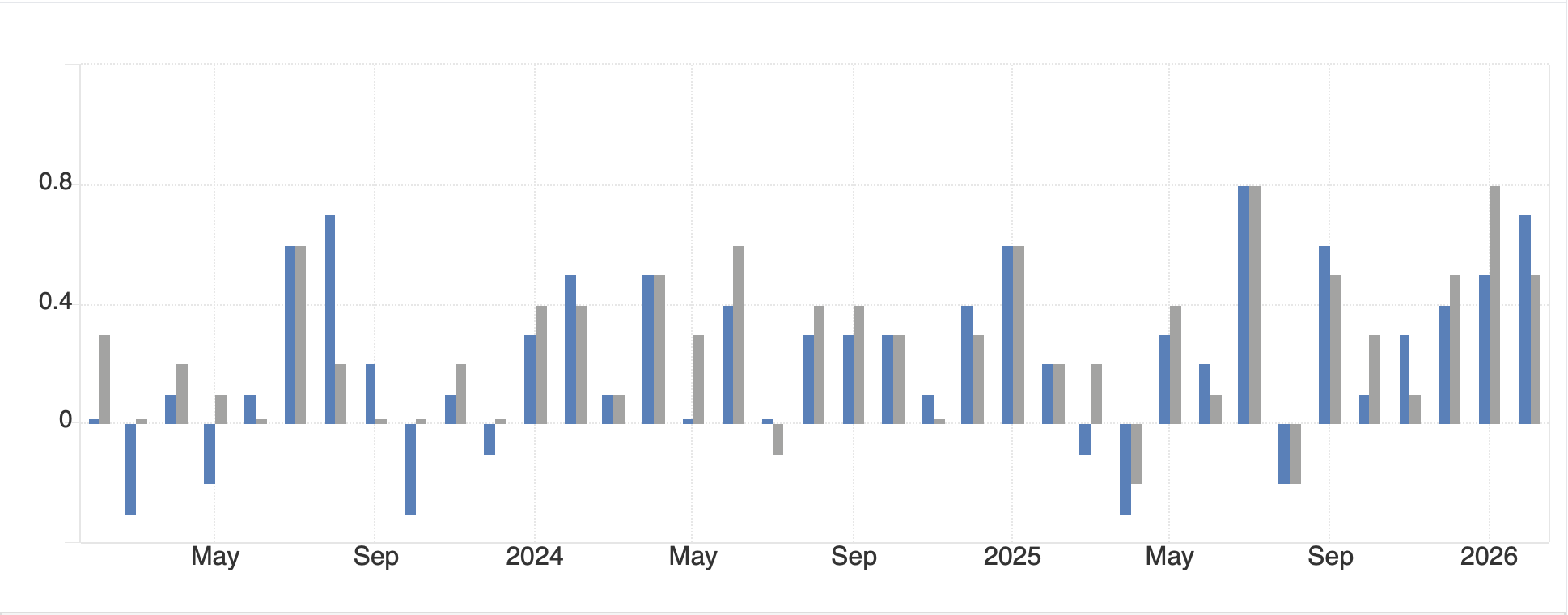

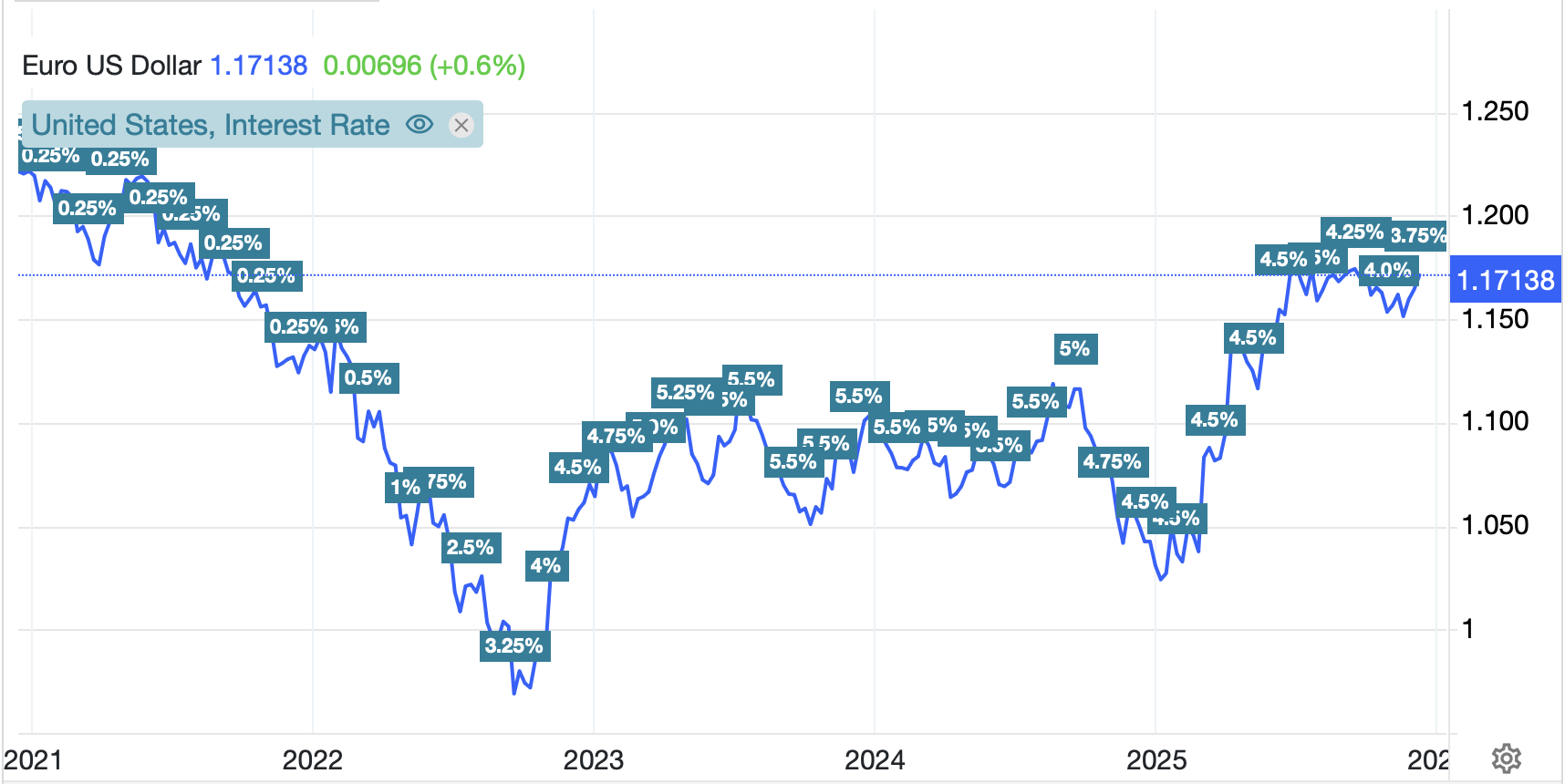

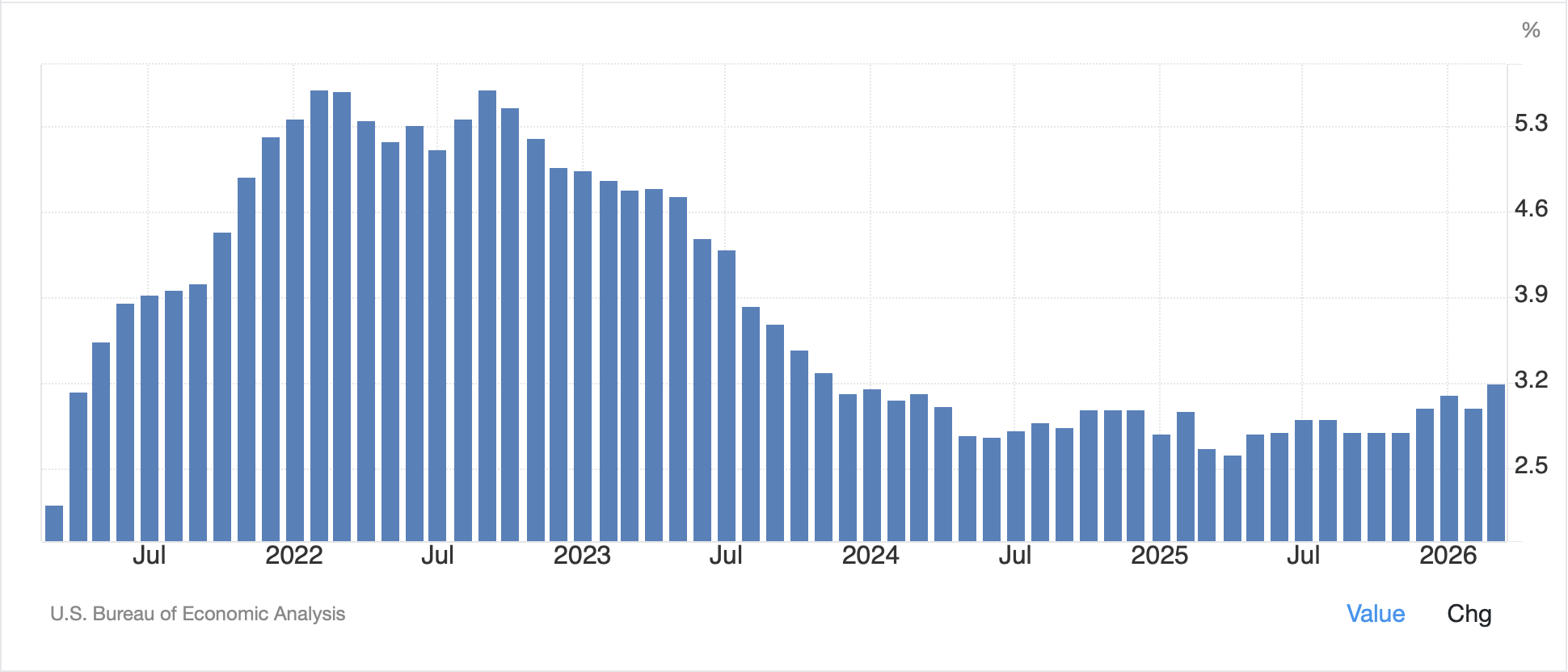

“A majority of participants highlighted…that some policy firming would likely become appropriate if inflation were to continue to run persistently above 2%.” This statement from the FOMC Minutes of the last meeting at the end of April is actually quite galling. Even though the FOMC has settled on the inflation reading that has historically run lower than all others, Core PCE, a metric, by the way, that doesn’t even try to represent a consumer’s experience, they have singularly failed to achieve their 2.0% target for more than five years running now. In the chart below from tradingeconomics.com, the leftmost bar is at 2.2% from March 2021, right as the Covid monetary insanity started to accelerate. This chart should be Jay Powell’s epitaph, a singular failure in the seat. After all, as awful as I thought Janet Yellen was in the role, her track record was not this bad!

Of course, now that Mr Warsh is due to be sworn in tomorrow, you can be certain that the punditry will lay the entirety of blame on the fact that inflation is running hot on him directly because, well, President Trump appointed him and they generally hate President Trump. Of course, I would contend this was not really a newsworthy release as we all already knew that the FOMC had turned more hawkish, and we have seen Fed funds futures begin to price in the probability of a rate hike by the end of the year.

In the end, though, the oil price remains the key driver of all market activity for the foreseeable future. So, let’s see how the rest of the markets behaved after yesterday’s sharp decline and given that the black, sticky stuff is sliding a little further this morning, currently down -0.75% at 6:00am. Remember, too, that Monday afternoon, WTI was more than $10/bbl higher than it is right now.

Source: tradingeconomics.com

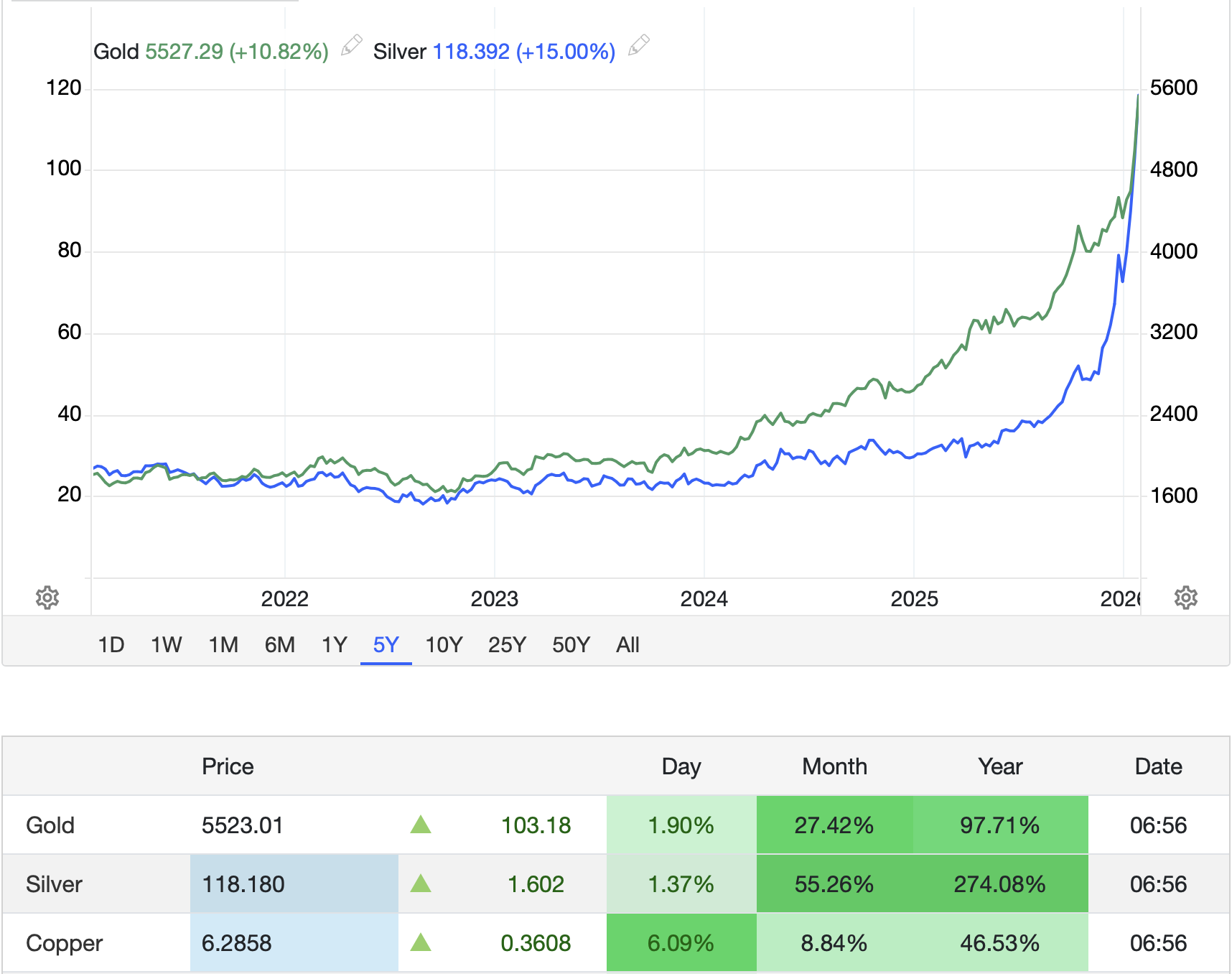

Finishing the commodity space, the metals, which all rallied yesterday, have slipped a bit despite oil’s slide this morning with gold (-0.3%), silver (-1.0%) and copper (-1.0%) all under modest pressure. I must admit that the price action in both gold and silver is starting to make me question the long-term case, let alone the short-term case, to hold them. Copper, however, seems like it will be in such demand as the electrification of everything increases, that any price declines should be snapped up.

In the equity markets, as mentioned above, yesterday saw gains in the US which were then followed up by what seemed to be a strong earnings report from Nvidia, although I read that there were those who were disappointed they didn’t guide things even higher. The follow through in Asia was mixed with Tokyo (+3.1%), Taiwan (+3.4%) and Korea (+8.4%) following the tech lead from the US. Interestingly, both China (-1.4%) and HK (-1.0%) did not follow along, but sold off, ostensibly on profit taking after their recent rallies. The other big laggard in this time zone was Indonesia (-3.5%) which reacted negatively to government export restrictions on key commodities like palm oil and metals as still-high oil prices take their toll on the economy.

As to Europe this morning, there is not much of which to speak with the major indices all +/- 0.2% or less after Flash PMI data showed weakening activity, notably in Services, although the market is still pricing two rate hikes this year by the ECB. US futures at this hour (6:35) are pointing slightly lower, with the NASDAQ (-0.6%) leading the way.

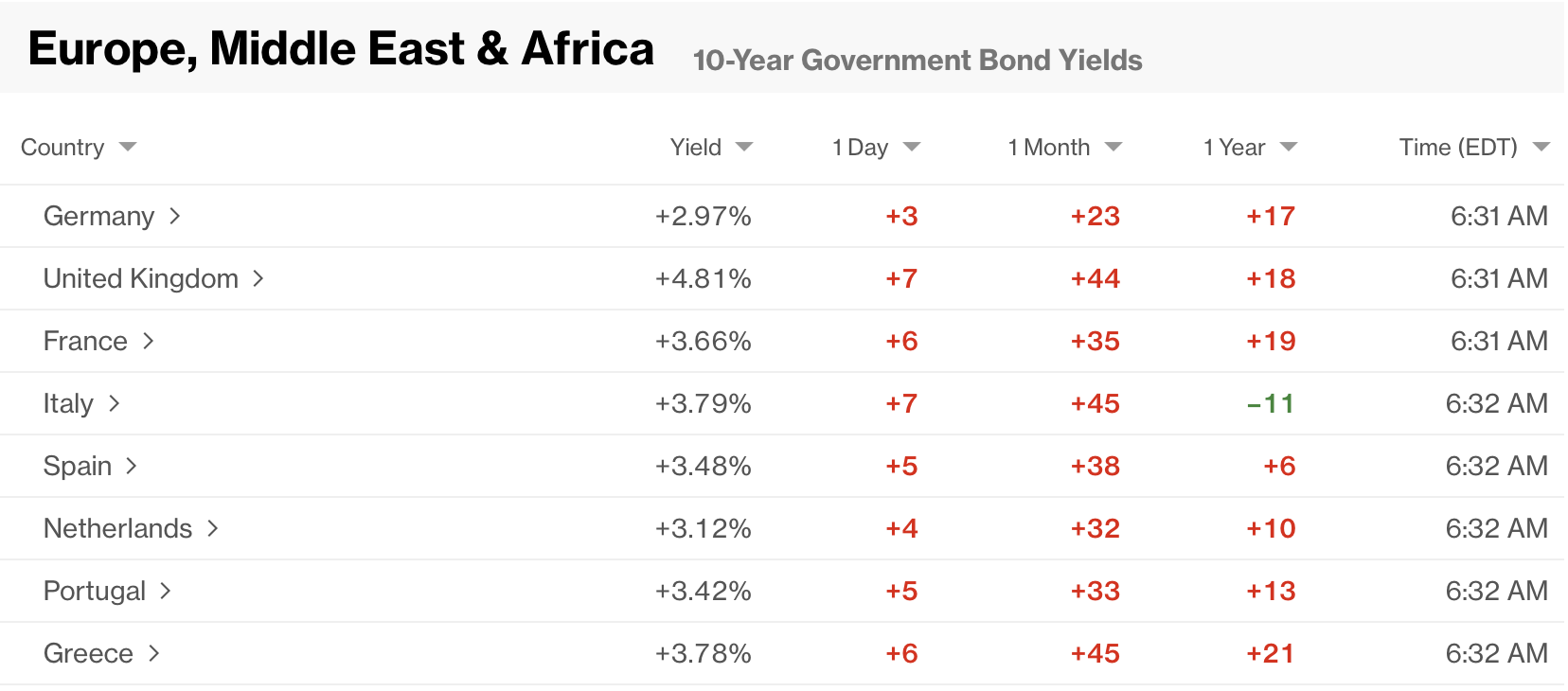

In the bond market, Treasury yields have backed up 3bps this morning after tumbling -8bps yesterday. Right now, they sit right at 4.60%. As it happens, yields fell everywhere yesterday alongside oil’s price decline, so it is no surprise that modest gains are the order of the day with German bunds (+1bp) outperforming the rest of the continent where yields are higher by 3bps to 4bps across the board.

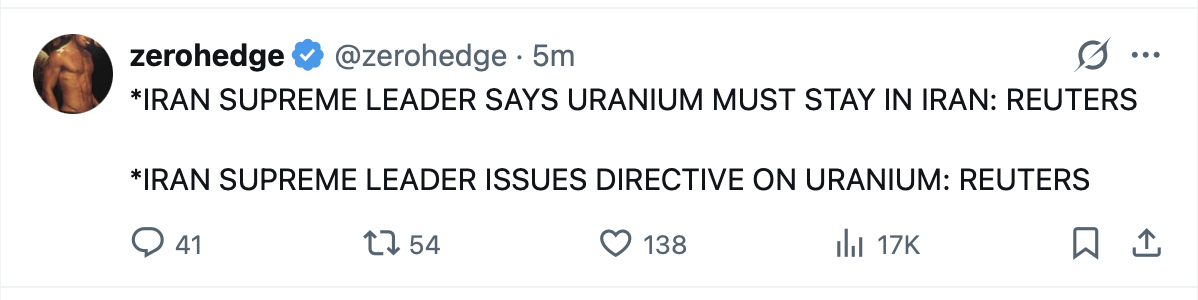

Finally, the dollar, which had been very quiet all evening, virtually unchanged when I sat down at my desk a 90 minutes ago, is starting to rally a bit here, which explains all the movements. Apparently, there was just an announcement by Iran regarding uranium, which not surprisingly, has changed the tone of the market.

This explains the dollar’s sudden revival, higher by 0.25% across the board, oil’s sudden rebound, it is now higher by 2.5% at 6:45, and the decline in metals prices. It also neatly matches bond yields higher. So, if negotiations are struggling, we should expect to see further risk-off behavior.

On the data front, this morning brings Initial (exp 210K) and Continuing (1790K) Claims, Housing Starts (1.41M), Building Permits (1.39M), Philly Fed (+18.0) and then a little later the Flash PMI readings (Mfg 53.8, Services 51.1). But as we have just seen in the past 45 minutes, everything is still attached to oil, so that is the key to watch. All the market correlations remain intact for now, and I suspect they will continue to do so until this conflict is well and truly over. In fact, it is situations like this, where news changes market pricing so dramatically in short order, that demands hedging programs to be maintained for everyone. Let’s face it, nobody is going to get it right all the time.

Good luck

Adf