Well, three little piggies said, whoa!

We think Fed funds rates are too low

But nine said, no way

We think they’re OK

And if hikes come, we should go slow

As well, pundit angst is exploding

Because they are now stuck decoding

The sparse words Warsh tenders

And so, story vendors

Now all have a sense of foreboding

It is truly remarkable to me how much angst was generated because Chairman Warsh refuses to offer any guidance whatsoever on what the Fed may do going forward. The same people who have railed at the Fed for being the underlying cause of economic problems, are now furious that he is trying to change their operating process. This tells me that much of that previous concern was theater as those same folks were either making a lot of money in the previous system or had a level of comfort that their positions were protected by the Fed put.

One of the biggest impacts the Fed has had in our society has been Ben Bernanke’s “portfolio-balance channel”, better known as trickle-down economics. His idea that buying Treasuries and forcing investors out the risk curve was a major driver of the current wealth and income inequalities that exist in today’s K-shaped economy. In fact, I would contend that we are seeing the results of that monetary experiment lately with the rise of the DSA in politics and the growing belief by many in the younger generations that they cannot get ahead regardless of their effort, so YOLO and socialism are a better fit.

The Fed is more than a century old and has had unchecked power during that entire period. Paul Volcker was the last Fed chair to be able to ignore (or withstand) the politics in order to do the right thing and address inflation. Everybody else has been captured by the organization. My take is currently the other 18 members of the FOMC all despise Warsh because they all hate President Trump, and Warsh is Trump’s man. Powell was Trump’s man too, but the Fed culture captured and converted him. Their biggest problem is Bessent and Warsh are besties and so Warsh has political cover. But they won’t go down without a fight.

My strong view is that ending the ample reserves framework and shrinking the balance sheet is the best thing the Fed can do for the economy and to fight inflation. It will take time, but that is clearly his goal. We shall see if he’s successful. But in the meantime, it appears that all the analysts who got paid a lot of money by Wall Street to do very little are now going to start having to earn their keep and think and figure out things on their own. And that is a really good outcome. As I continue to write, less certainty may bring more short-term volatility, but it will reduce the opportunity for excess leverage and reduce market fragility. And that is something to be sought.

So, how did the market respond? This chart from wolfstreet.com is annotated beautifully.

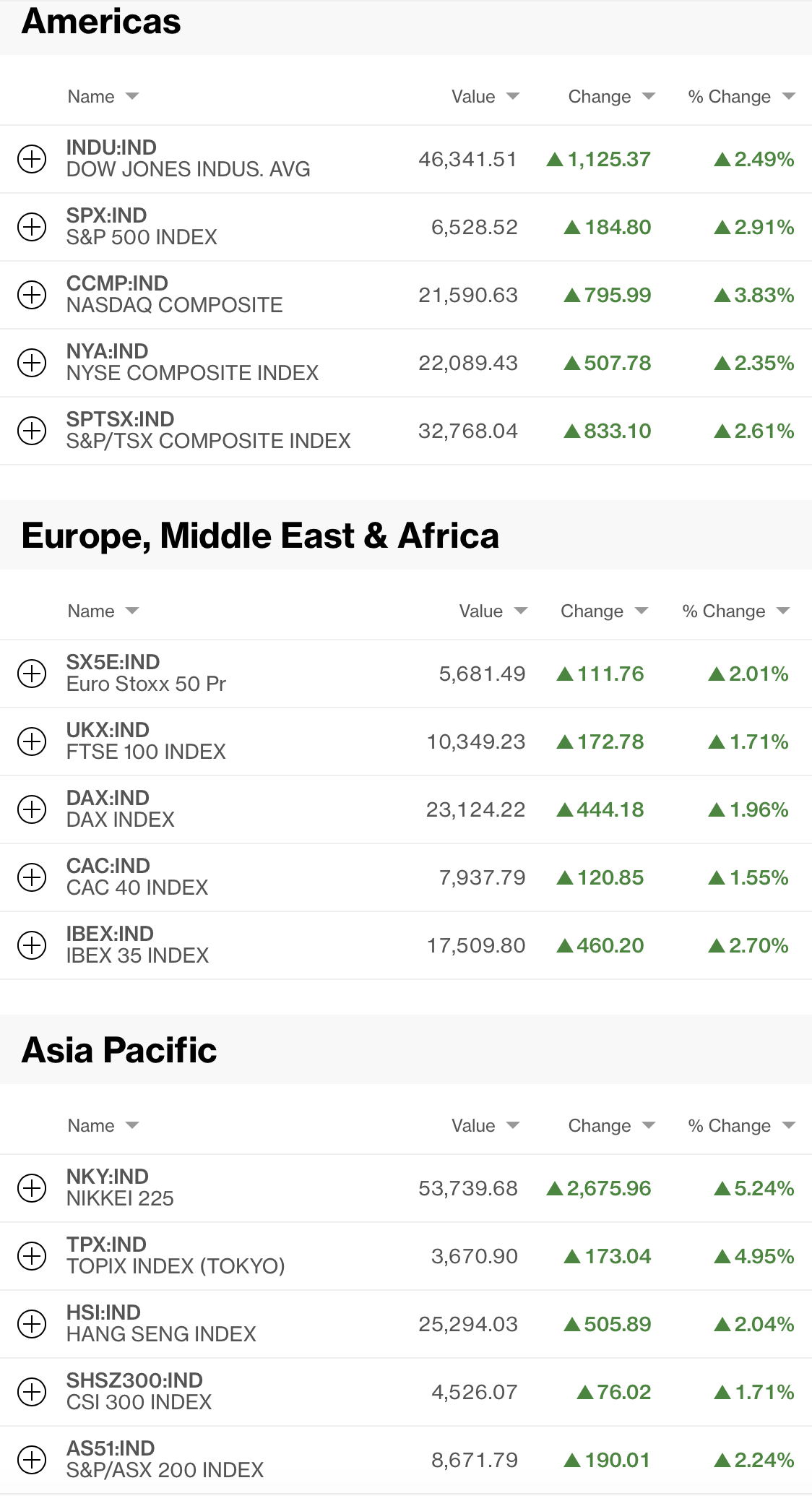

The equity market decided they didn’t like uncertainty and are growing increasingly scared there may not be a Fed put anymore. And so, we saw weakness across the Americas yesterday with US and Canadian indices falling sharply into the close. Is this the end of the world? I don’t think so although you might be confused by reading some of the commentary. Overnight, though, things were more mixed with some laggards (China -1.1%, Korea -1.2%, Australia -0.8%, New Zealand -1.5%) and some gainers (Tokyo +0.7%, HK +0.2%, India +0.3%, Indonesia +1.6%). The continued fighting in Iran (the US launched another series of strikes last night) as well as concerns over the tech sector valuation remains a generic equity market issue right now.

Europe, though, is in the green this morning (Spain +1.4%, France +0.9%) with Germany and the UK unchanged, as generally better than expected, albeit still soft, GDP data was released this morning as per below:

| Country | Actual | Previous | Expected |

| France Q/Q | 0.2% | -0.1% | 0.2% |

| France Y/Y | 0.7% | 0.8% | 0.8% |

| Spain Q/Q | 0.7% | 0.6% | 0.6% |

| Spain Y/Y | 2.7% | 2.7% | 2.5% |

| Netherlands Q/Q | 0.4% | 0.3% | 0.2% |

| Netherlands Y/Y | 1.3% | 1.4% | 1.2% |

| Germany Q/Q | 0.2% | 0.4% | 0.1% |

| Germany Y/Y | 0.9% | 0.7% | 0.6% |

| Italy Q/Q | 0.2% | 0.3% | 0.1% |

| Italy Y/Y | 1.0% | 0.8% | 0.7% |

| Eurozone Q/Q | 0.4% | 0.0% | 0.2% |

| Eurozone Y/Y | 1.0% | 0.5% | 0.5% |

Source: tradingeconomics.com

Hardly the stuff to quicken your pulse, but better than it could have been. As to US futures, at this hour (7:15), they are in the green with the NASDAQ (+1.25%) leading the way after MSFT reported excellent numbers last night which has been enough to offset META’s miss.

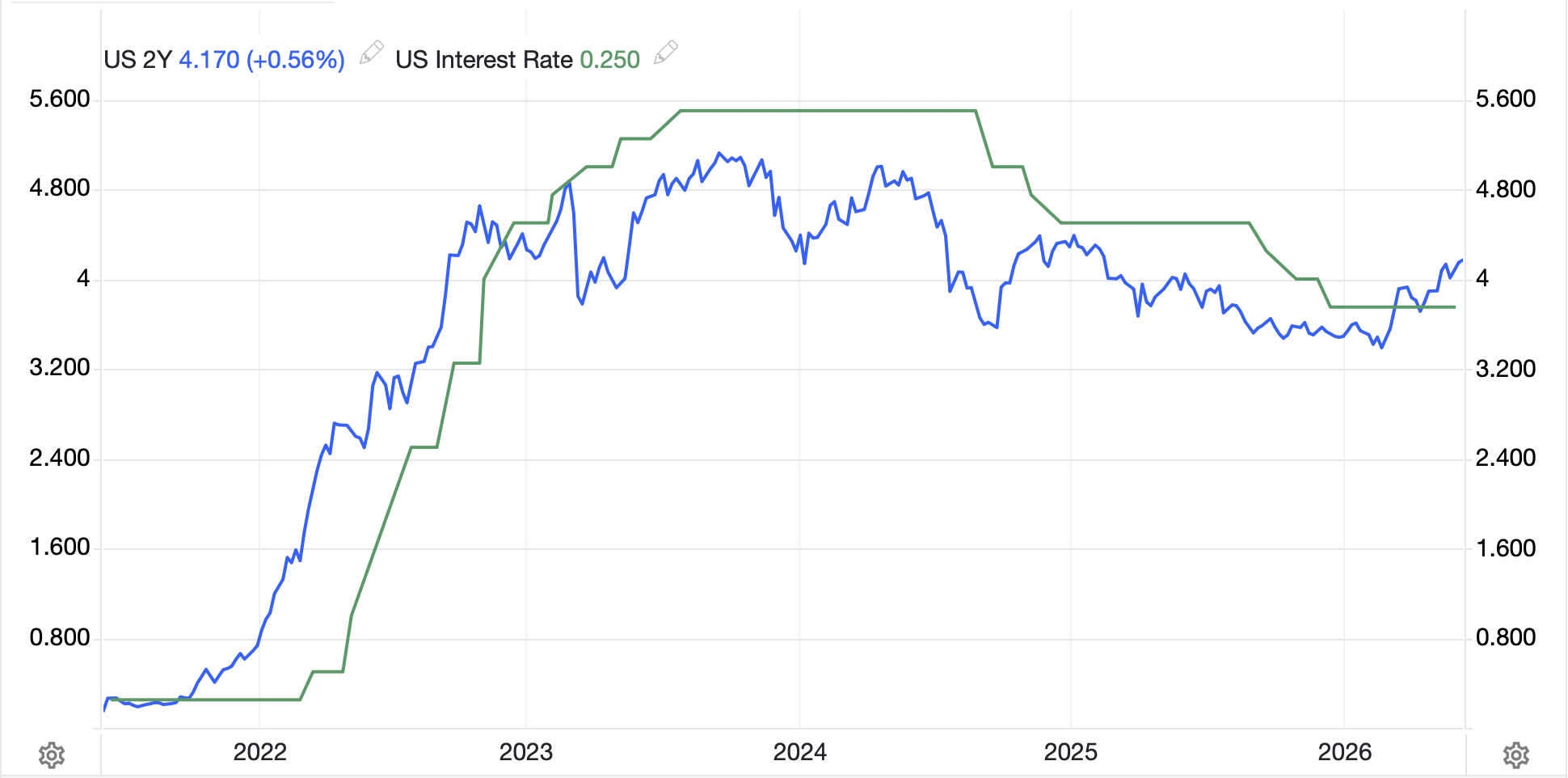

As to the bond market, after the FOMC, the yield curve steepened significantly with 10-year yields climbing 9bps and 30-year yields rising 11bps at their peak. the chart below of the 30-year shows it well. In addition, we continue to hear that the 30-year yield is now its highest since 2008. Again, I would ask all those complaining, you hated what the Fed did before, what did you expect would happen if it changed?

Source: tradingeconomics.com

European sovereign yields also rose yesterday, albeit not as far, more in the 5bp range, and JGB yields rose 6bps overnight. The BOE left rates on hold, as expected today with 3 votes to raise rates and 6 to stand pat. Overnight, JGB yields rose 6bps and other Asian yields rose further. As usual, the Treasury curve is the leader here.

However, it is interesting to note that 2yr Treasury notes actually fell -5bps yesterday as the market continues to adjust its views of what is going to happen going forward. Chairman Warsh was explicit in saying that he welcomed market movement doing the Fed’s work for them, and if inflation remains a concern, and it does, yields should rise. In fact, if the Fed starts to shrink its balance sheet (and remember it is still buying T-bills), I expect the curve to steepen and the front-end rates to decline.

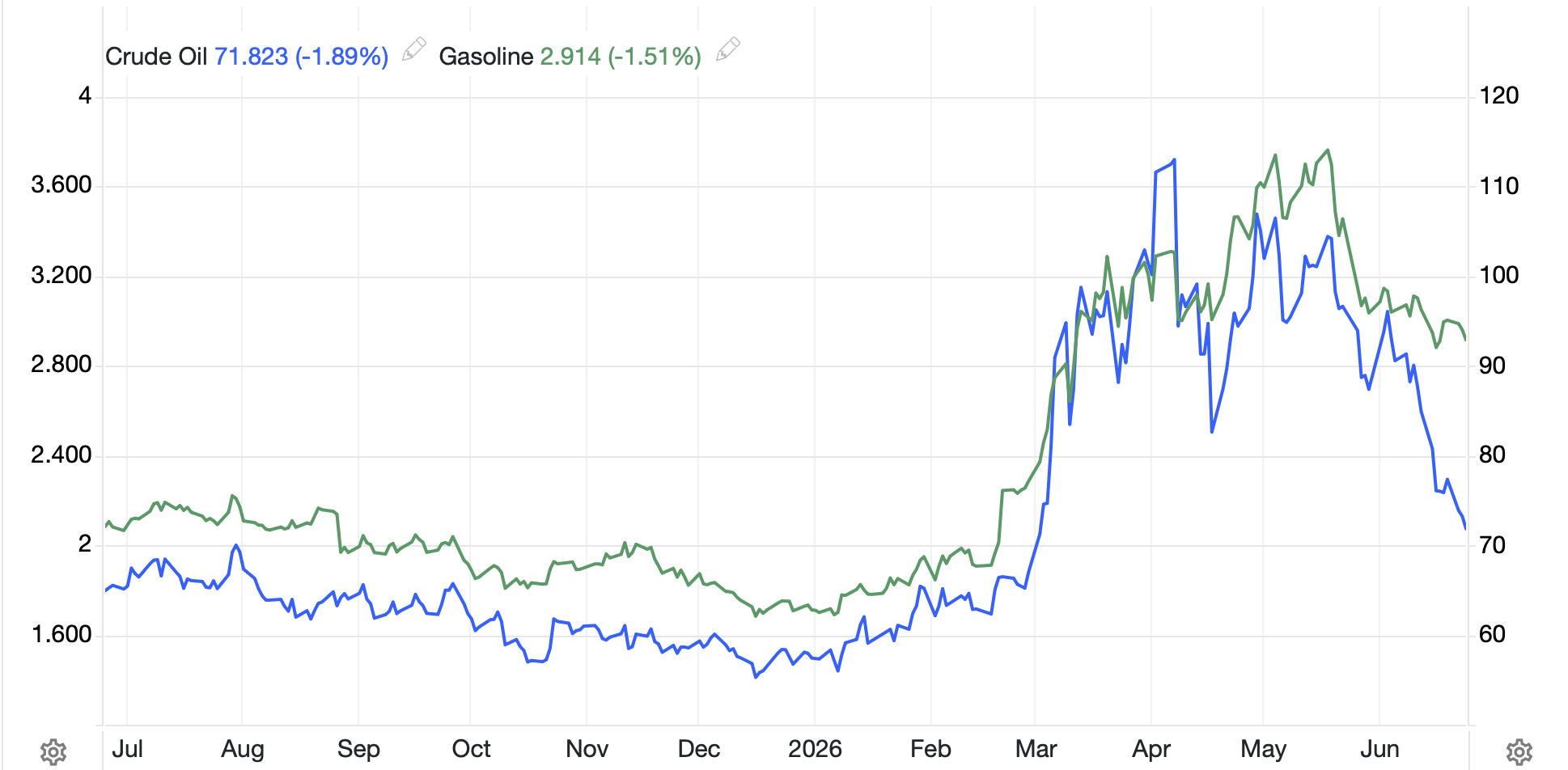

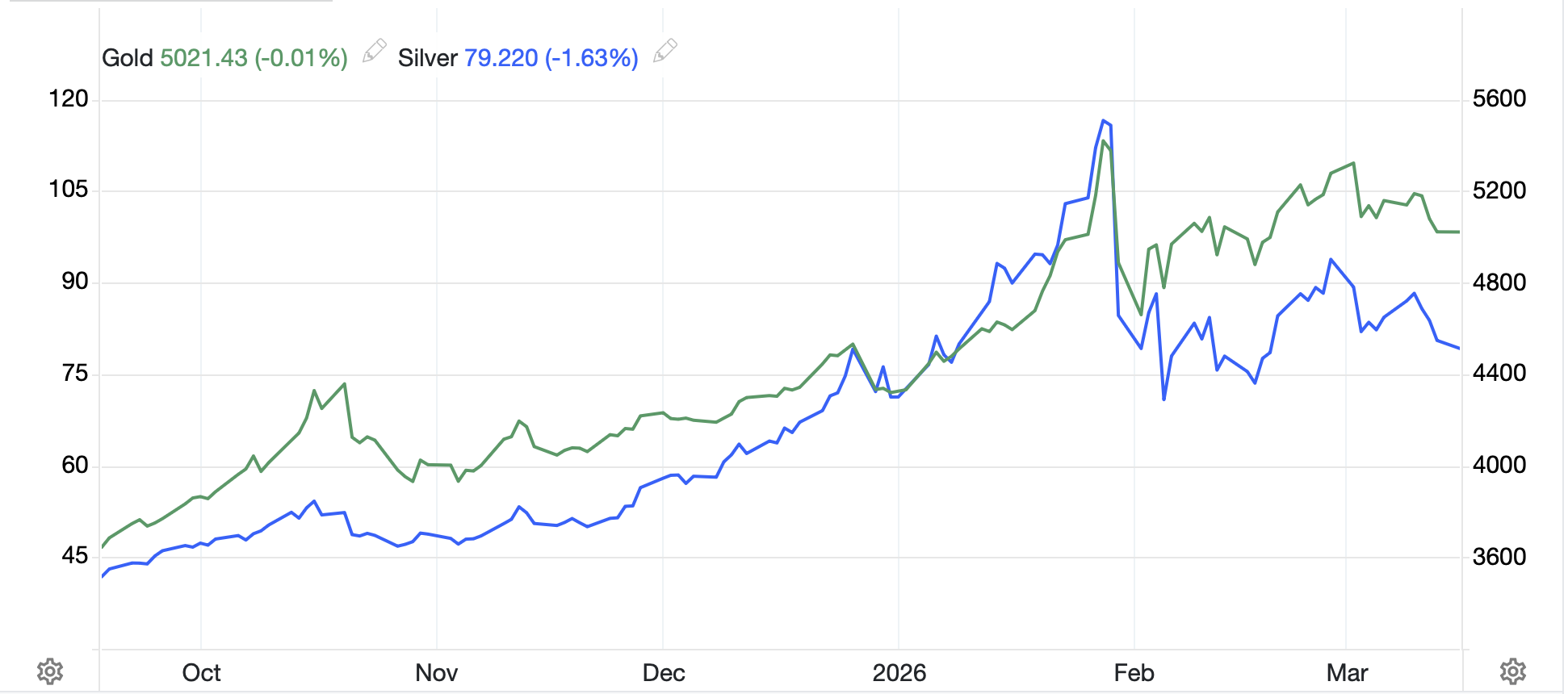

In the commodity market, remarkably despite further US attacks on IRGC military sites, oil (-1.3%) is slipping this morning. This is another market where things are not necessarily following the previous narrative. As to metals, they are firmer this morning with gold (+0.3%), silver (+0.9%) and copper (+2.2%) all starting the day in good shape.

Finally, the dollar is softer this morning as the DXY (-0.2%) slips back toward its breakout level of 100.50 once again.

Source: tradingeconomics.com

Somebody on Twitter made the point that if the dollar can’t rally amid rising yields, that is a problem. But my observation, and I believe the numbers back me up, is that the dollar tends to follow short-term yields, like the 2-year, rather than the 30-year bond. The yen (+0.3%) is having a good day and has backed below 163.00 for the moment taking some pressure off the MOF and the intervention watch. KRW (+0.6%) continues its remarkable rally which appears to be built on a combination of repatriation of earnings by SK Hynix and Samsung as well as the proceeds from the SK Hynix US IPO, and the strong economic activity plus the BOK’s efforts to internationalize the won.

Source: tradingeconomics.com

But overall, the dollar is under pressure this morning. and remember, this is not something that the Trump administration worries about, rather they embrace it for its trade benefits.

On the data front, we get a bunch of stuff today as follows:

| Initial Claims | 200K |

| Continuing Claims | 1800K |

| PCE | -0.1% (3.7% Y/Y) |

| Core PCE | 0.2% (3.3% y/Y) |

| Q2 GDP (second look) | 2.1% |

| Personal Income | 0.3% |

| Personal Spending | 0.3% |

Source: tradingeconomics.com

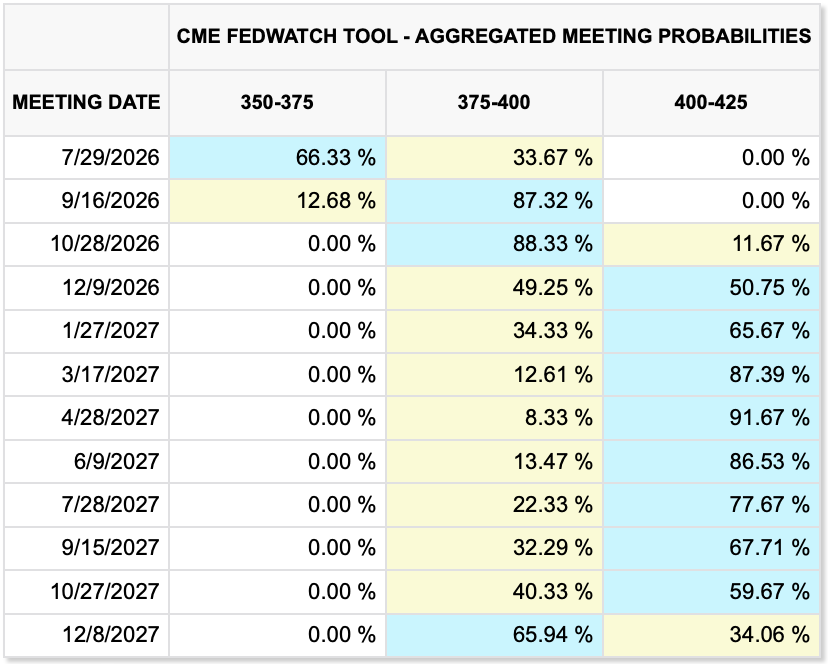

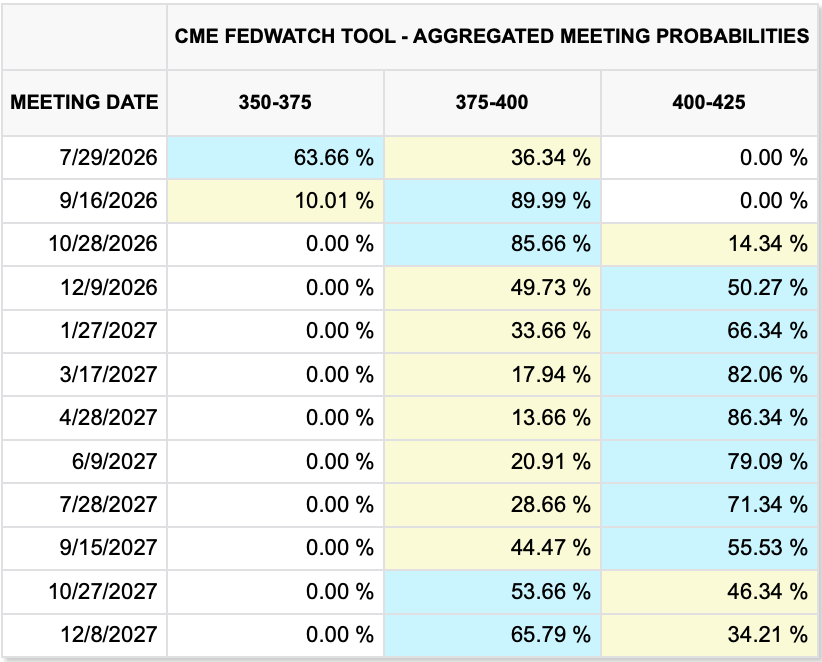

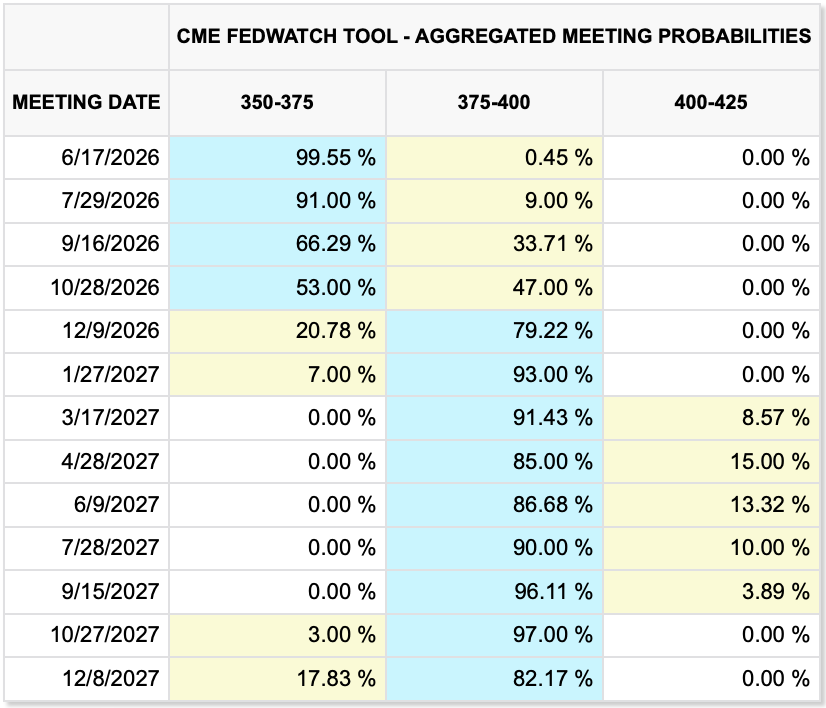

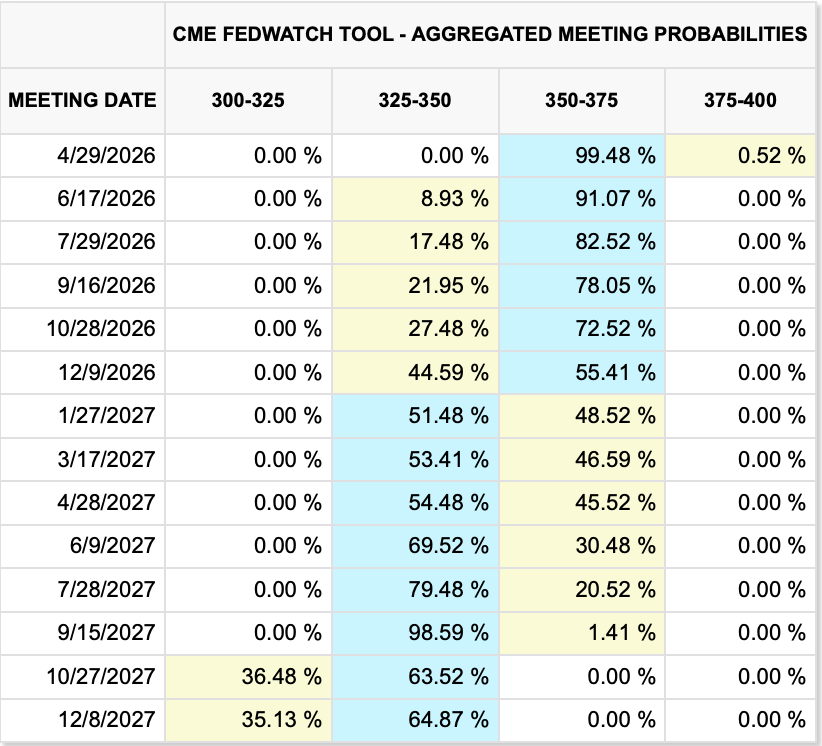

It’s funny, now that Chairman Warsh seems to be de-emphasizing PCE, will it be as important going forward? Probably still today where a hot number raises the probability of a September hike which currently sits at 63.4%.

Mercifully, there are no Fed speakers today or tomorrow so perhaps we can let the data guide the markets. Overall, oil still matters a lot, headlines still matter a lot, while the dollar could well slip back into its previous trading range, especially on a soft PCE reading.

Good luck

Adf