The third time, it wasn’t a charm

As thankfully, Trump saw no harm

But it’s disconcerting

The left keeps on flirting

With killing Trump by firearm

But absent more news on the war

Investors, most stocks, still adore

And there’s still a call

The dollar should fall

Though so far, they’re down on that score

It is certainly disconcerting that there have been three bona fide assassination attempts on President Trump in the past two years, something I fear speaks loudly about his opponents. Fortunately, this one also failed. Interestingly, as this occurred at the White House Correspondents Dinner, the entire Washington press corps, who largely detest the man, were there. I wonder if this experience will alter their rhetoric, which I would argue has been the key driving force behind these attempts. Alas, I fear that will not be the case, at least not for more than a few days at best.

But that was a far more exciting weekend than anybody imagined as there is no new news regarding the Iran war with potential talks never occurring over the weekend. Neither have the marines moved in on Kharg Island, so the status quo, a US naval blockade, remains the primary situation. This leads to two questions; first, how long can Iran withstand the lack of revenue with the government, or more accurately the military, still operating effectively? And second, how long before Iran’s oil wells need to be shut in, which is likely a death sentence on those wells, and by extension, on Iran’s long-term revenue stream?

Frankly, that’s what the weekend brought, so let’s turn to markets. While the DJIA lagged on Friday, both the NASDAQ and S&P 500 rallied to yet further new all-time highs as US corporate earnings remain robust and the market looks ahead to this week where 5 (MSFT, GOOG, AMZN, META, AAPL) of the Mag7 report earnings this week on Wednesday and Thursday. As well, Wednesday brings the FOMC decision, with no change expected. As to US futures this morning, as I type (6:50), they are essentially unchanged.

Overnight, Asia’s session was mixed with Japan (+1.4%) putting in a nice performance along with Korea (+2.15%), India (+0.8%) and Taiwan (+1.8%) although there were laggards (HK, Australia, Indonesia, Singapore) as well, with much smaller declines. China was basically unchanged. Perhaps the biggest news was that an oil tanker from the US arrived in Japan for the first time, although certainly not the last time. European bourses are all a bit firmer this morning, seemingly responding to decent earnings throughout many nations there. Thus, Germany (+0.6%) is leading while Spain, France and Italy (+0.5% each) lag slightly and the UK (+0.1%) brings up the rear as King Charles prepares to visit President Trump and the US starting today, ostensibly trying to resurrect the once special relationship that has deteriorated over time.

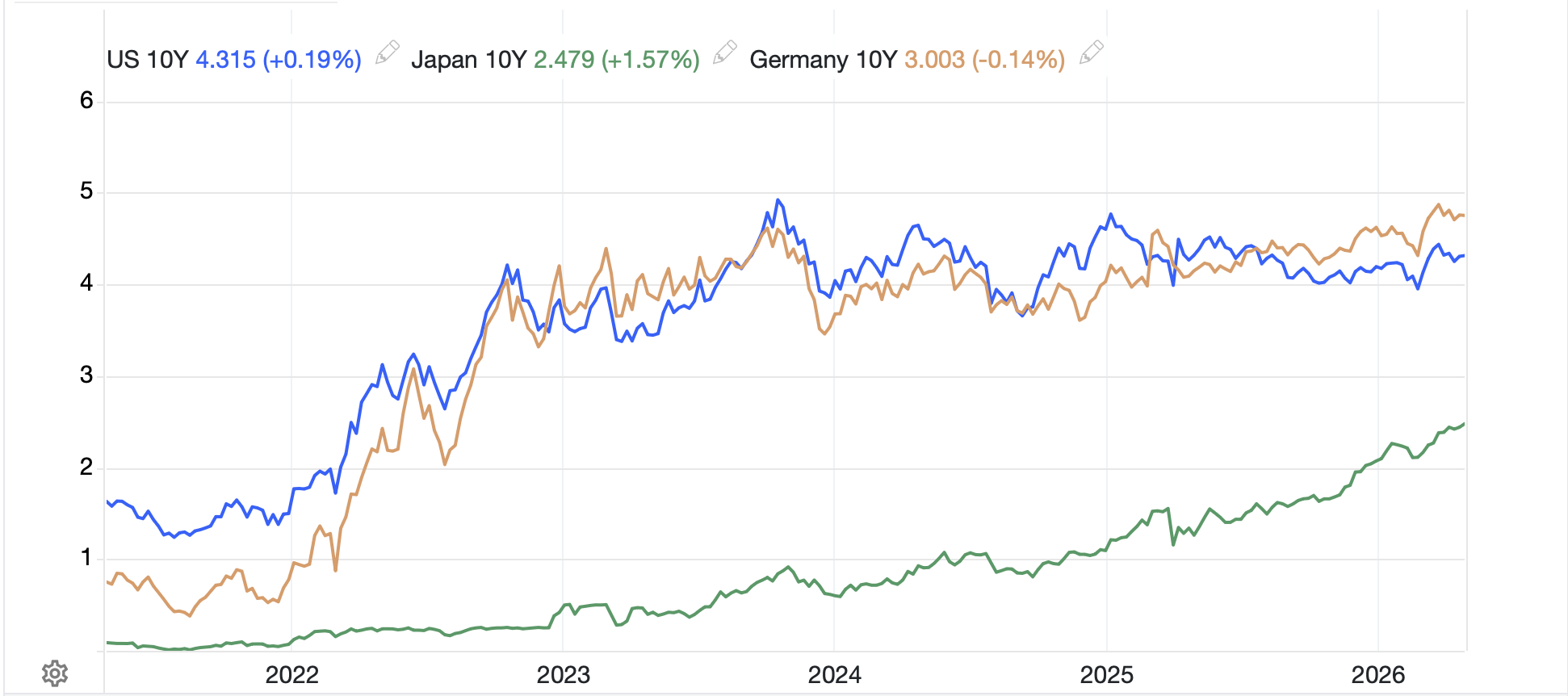

In the bond market, nothing continues to happen with Treasury yields higher by 1bp this morning and similar price action across all of Europe. JGB yields (+4bps) were the big mover as market participants await three key central bank meetings this week, the Fed, ECB and BOJ. But here’s the thing, of all the major economies around, Japan’s is the only one where the bond market is offering any real signal. The below chart from tradingeconomics.com shows US (blue line), German (tan line) and Japan (green line) 10-year yields over the past 5 years.

While we all remember the pain in markets when the Fed, and then all other central banks, figured out that the Covid policy inflation wasn’t going to be as transitory as they hoped and pushed rates up at a historically fast pace in 2022, since then, it is pretty easy to make the case that neither US nor Germany (and by extension the rest of Europe) have seen any substantive change in their bond markets. I am speaking in a big picture reference here, not the day-to-day noise that we see. Meanwhile, Japan has finally begun to feel the pressure of a massive debt/GDP ratio and rising inflation.

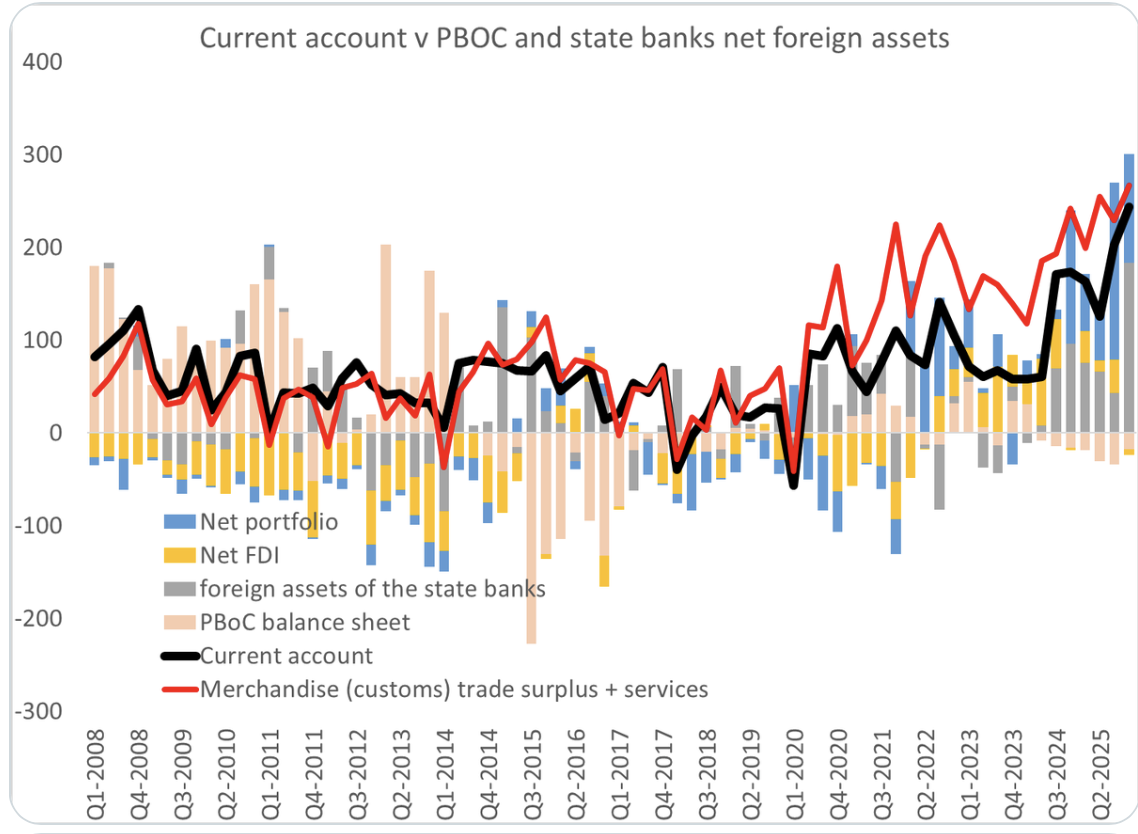

Contrary to popular belief, Treasury bonds remain the reserve asset of choice around the world as every nation needs to hold a certain amount of USD simply to function in the world today (which is why there is so much recent discussion regarding USD swap lines for numerous countries). While it sounds great for the panican set to discuss how Chinese “official” holdings of Treasuries have collapsed and that is a signal they are selling bonds, the reality is they have switched their custodians from the Fed to Clearstream and Euroclear in Brussels and Luxembourg while many of those assets are now held in large Chinese ‘private’ banks rather than on the PBOC’s balance sheet.

Source: @Brad_Setser

Notice the large grey bar at the right, foreign assets of the state banks. Which brings us to the central bank meetings this week where no major central bank is expected to change policy. Japan seems the diciest call, but the word was put out last week that June is the likely date. As well, the ECB’s own market watching website is now looking at June as a probable rate hike as per the below from ecb-watch.eu.

For the FOMC, no change today and now that the DOJ has referred the cost overrun investigation to the IG at the Fed, the hold on Kevin Warsh by Senator Tillis has been lifted. I expect he will be confirmed in time for Powell to leave on his scheduled date. It remains to be seen if Powell will stay on the FOMC (his term technically runs until January 2028), but historically, once a Fed chair leaves that role, they step away completely. Ultimately, until the markets begin to understand that inflation is going to be structurally higher than in the past, I suspect bond yields are going to remain range bound.

In the commodity space, oil (+0.7%) is a touch higher as the market seems to be becoming increasingly concerned that the impacts of the closure of the Strait of Hormuz are going to be longer lasting than previously assumed. However, the futures curve remains steeply backwardated as per the below chart form tradingview.com.

Personally, I see this as confirmation of my own view that oil prices are likely to decline over time as more and more supply becomes available with new projects. If anything, this war has accelerated that process. Meanwhile, metals prices are essentially unchanged this morning, biding their time for the next big piece of news.

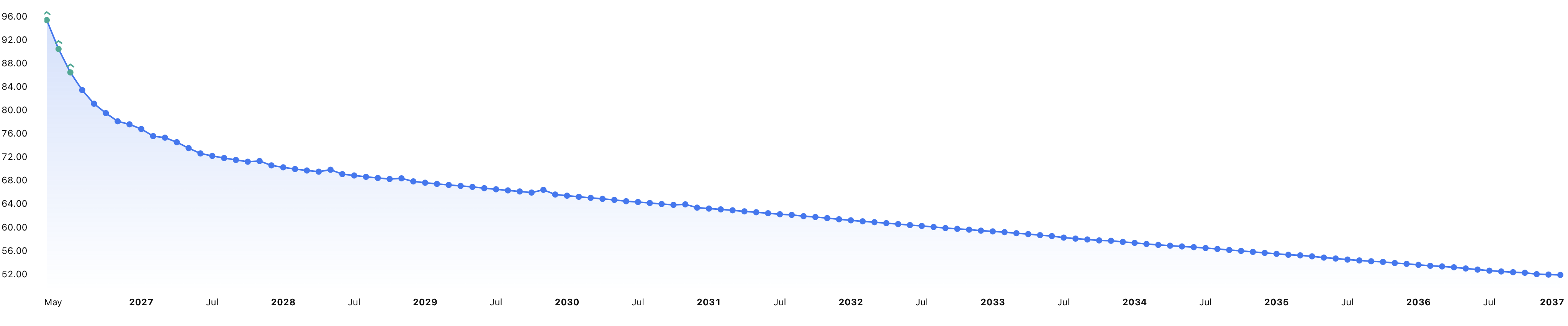

Finally, the dollar is under modest pressure this morning, down about -0.2% across the board as risk appetites continue to build with the war receding in traders’ collective mindset. But here, too, just like in the bond market, it is difficult to make the case that anything of note has happened to the dollar, writ large, over the past year. I know I show this chart frequently, but it is simply to hammer home the idea that the dollar is not collapsing. It has basically had a 3.5% range 96.50 – 100.00 for the past twelve months. I’m sorry, that is not a death omen!

Source: tradingeconomics.com

On the data front, there are a total of 5 central bank meetings with no changes expected anywhere, and then PCE data later on.

| Tonight | BOJ Rate Decision | 0.75% (unchanged) |

| Tuesday | Case-Shiller Home Prices | 1.1% |

| Consumer Confidence | 89.2 | |

| Wednesday | Housing Starts | 1.4M |

| Building Permits | 1.39M | |

| Durable Goods | 0.5% | |

| -ex Transport | 0.4% | |

| Goods Trade balance | -$86.0B | |

| BOC Rate Decision | 2.25% (unchanged) | |

| FOMC Rate Decision | 3.75% (unchanged) | |

| Thursday | BOE Rate Decision | 3.75% (unchanged) |

| ECB Rate Decision | 2.0% (unchanged) | |

| Q1 GDP | 2.2% | |

| Personal Income | 0.3% | |

| Personal Spending | 0.9% | |

| Initial Claims | 215K | |

| Continuing Claims | 1820K | |

| PCE | 0.7% (3.5% Y/Y) | |

| Core PCE | 0.3% (3.2% Y/Y) | |

| Chicago PMI | 53.0 | |

| Leading Indicators | -0.1% | |

| Friday | ISM Manufacturing | 53.0 |

| ISM Prices Paid | 80.0 |

Source: tradingeconomics.com

It remains difficult to get too excited about the data, though, as war stories remain top of mind. Until something changes there, I suspect we will see equities continue to rally on earnings data with the rest of the markets doing very little overall, data be damned.

Good luck

Adf