Now, all eyes will turn to the chat

When Warsh and his minions, they sat

Round oak polished bright

Discussing their plight

‘Bout prices and jobs and all that

But since they met three weeks ago

Chair Warsh very clearly did show

His view that inflation

Was short in duration

And rate hikes were not apropos

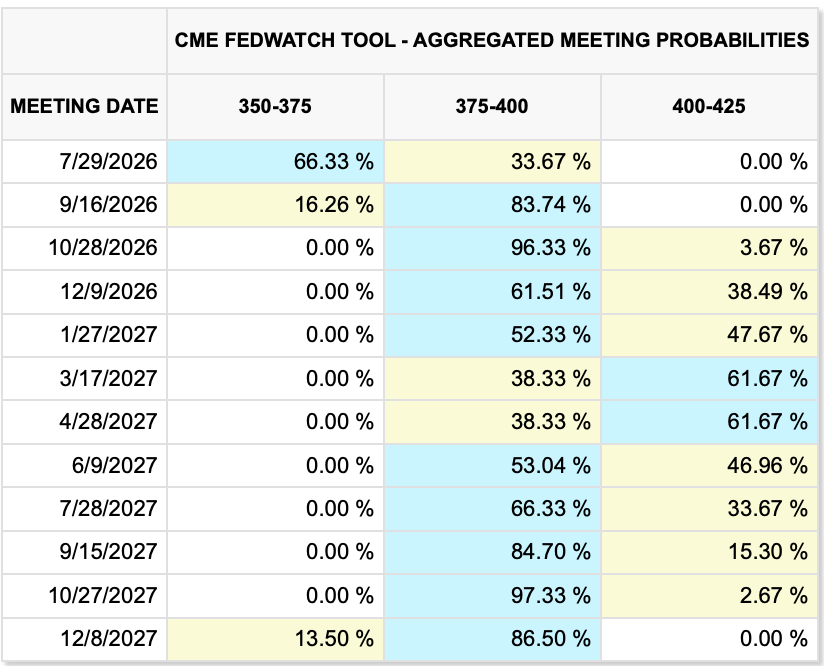

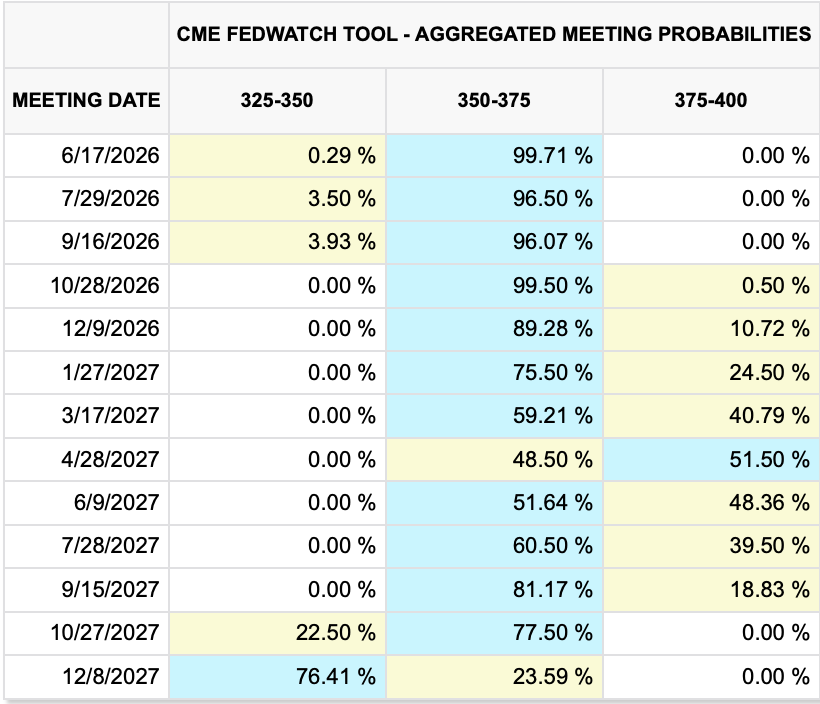

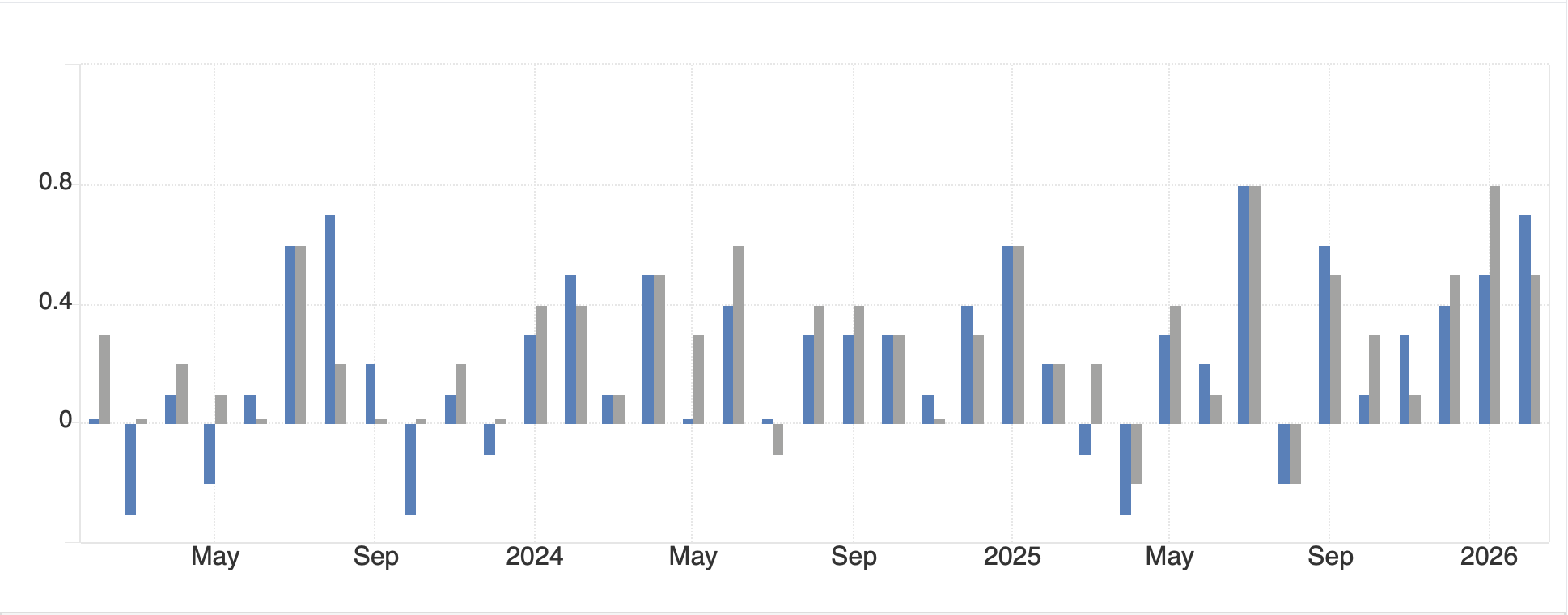

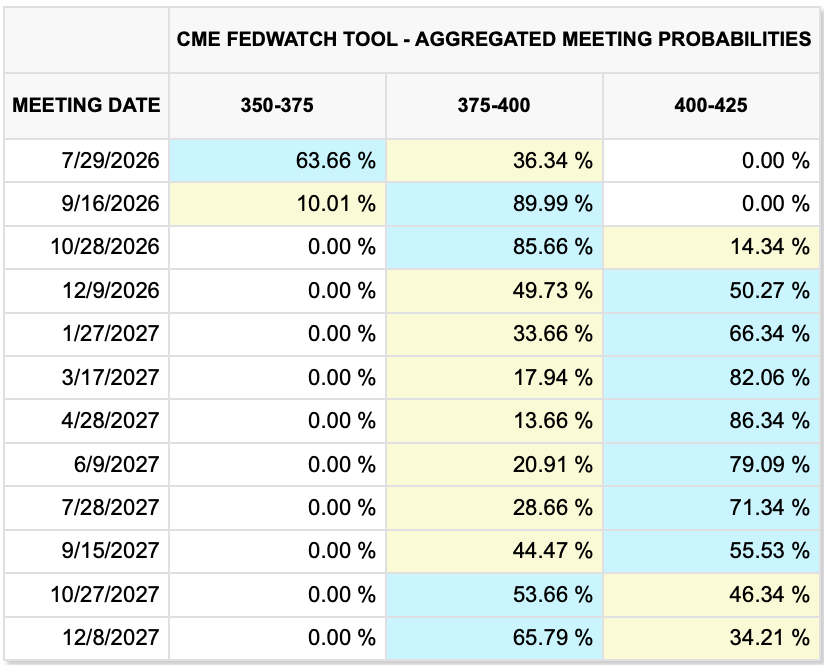

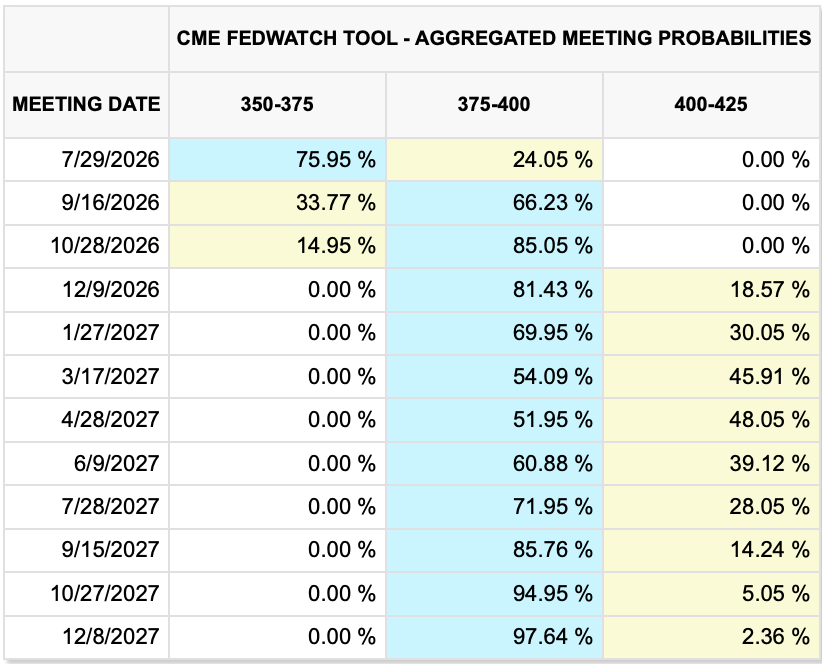

It is getting increasingly difficult to maintain a hawkish Fed view as both the data and the Chairman are working against you. While we all enjoy the World Cup this week, arguably the biggest market related news will be Wednesday’s release of the Minutes from the last FOMC meeting. You may recall that in the wake of that meeting, interest rate hawks were in the ascendancy with an October hike fully priced and odds for a second, December, hike priced as well as you can see in the below CME table from June 24th.

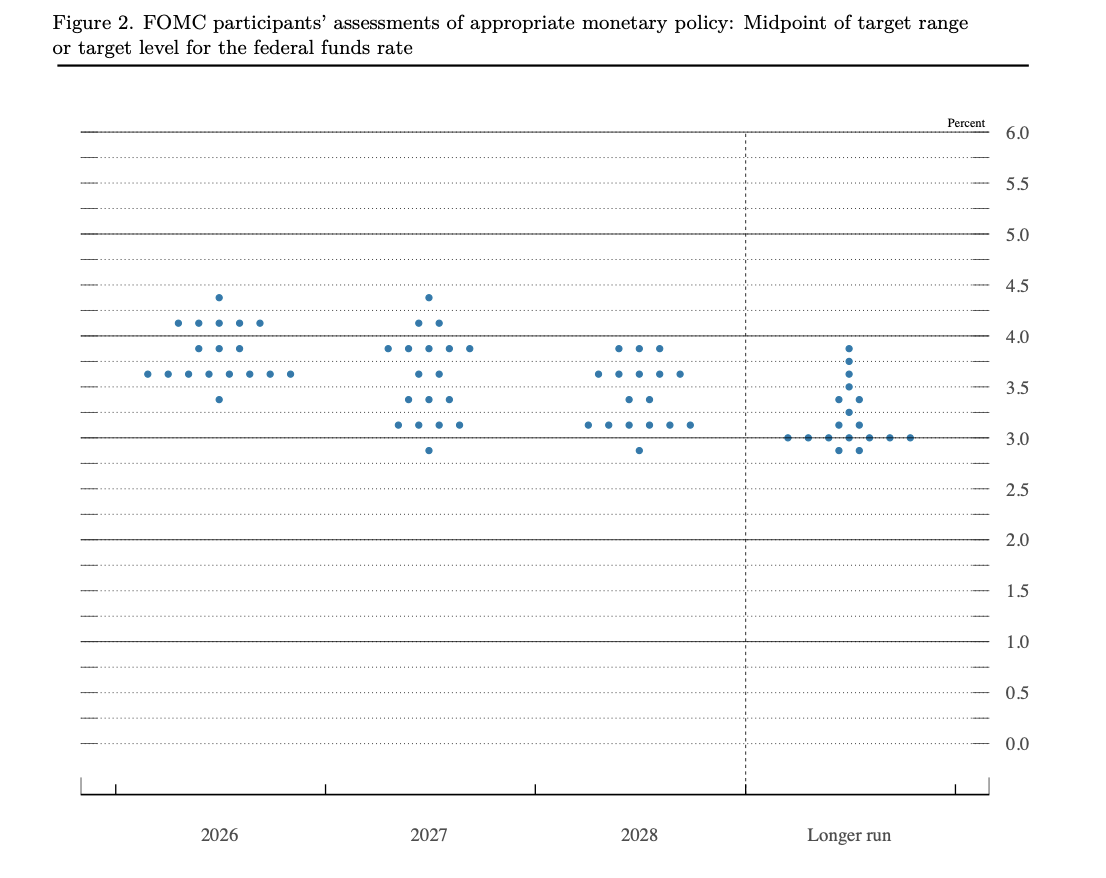

Now, in the wake of that meeting and the press conference, the combination of the dot plot showing half the committee expecting a hike this year and the lack of forward guidance along with the succinct statement explaining the Fed would achieve their 2.0% inflation mandate had many analysts expecting a serious tightening cycle upcoming.

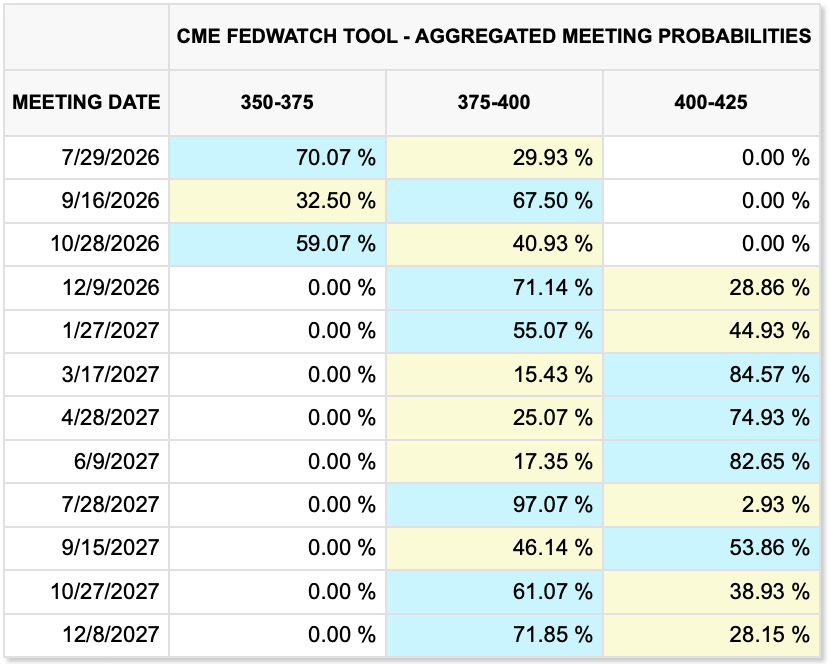

But a funny thing happened on the way to the next FOMC meeting, still three weeks hence, the price of oil, and energy in general, accelerated its decline. Given how much effort was made to explain that the core inflation readings were heading higher because of the impact that energy has on everything, hence the need to hike rates, this has been an inconvenient outcome for the hawks. Add to that Chairman Warsh’s comments at Sintra, Portugal last week, regarding the easing of inflationary pressures as energy prices decline (oil -0.9% this morning) and futures traders have been adjusting their views pretty steadily as per this morning’s CME table.

While a hike is still assumed by year end, the second one has fallen by the wayside. Personally, as we continue to see inflation pressures subside alongside energy prices, I expect that not only will we not see a hike this year at all, but a cut by December is viable.

Adding to the downward bias on Fed funds futures was Thursday’s payroll report, where the headline number was softer than expected, although the Unemployment Rate did slip another tick to 4.2%. I think a key problem with using the Unemployment report as such a critical signal is the fact that since President Trump’s inauguration and the actual closing of the Southern border, as well as the deportation (by both the government and on a self-basis) of somewhere between 2.5 million and 3.0 million according to Grok, the old econometric models of what type of job growth was necessary to maintain solid economic growth are no longer terribly useful. If we throw in the dramatic changes to the economy on the back of the increase in AI as a tool and infrastructure investment, it becomes increasingly difficult to utilize the old models. Too, one of the main themes from several months ago was that AI was going to replace hundreds of thousands of jobs and unemployment would skyrocket, while now, those ideas are being rethought with many analysts now expecting AI will support more jobs. Perhaps, the best thing that can come of this change is that markets will no longer radically adjust based on an outdated statistic.

There is still a long way to go before the next FOMC meeting and I doubt that the many task forces will have come to any conclusions yet, but if energy prices continue to decline, and I couldn’t help but notice this WSJ article discussing the sudden glut of oil driving prices lower, and I am growing increasingly confident in my views.

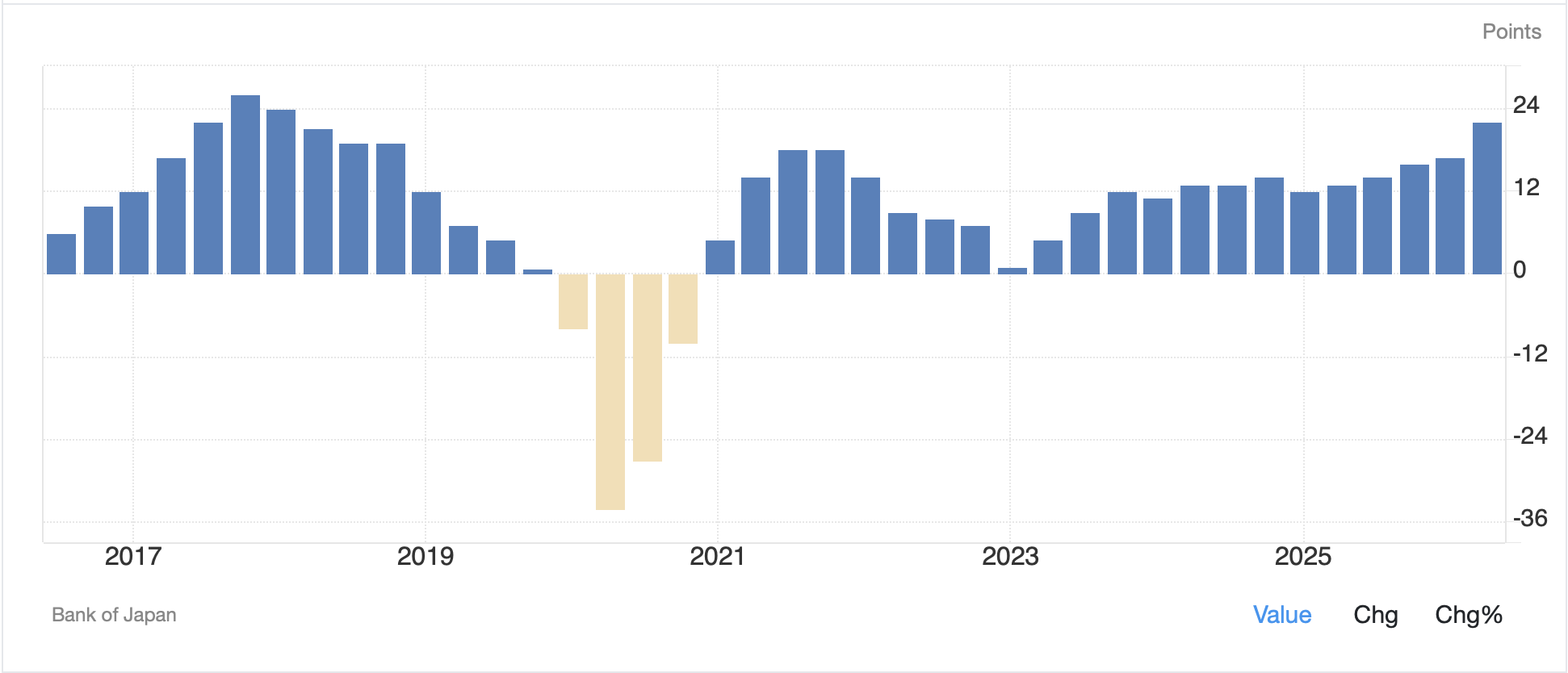

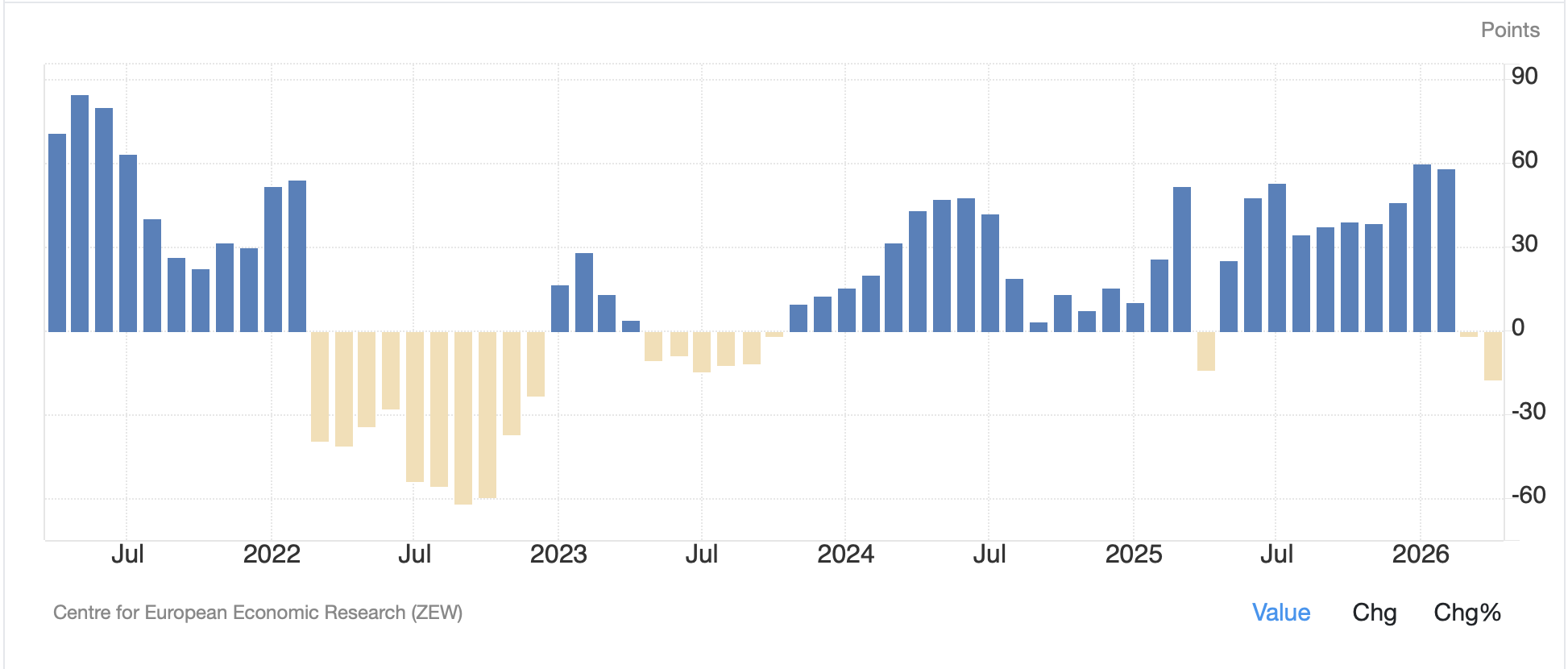

Which takes us to the currency that most needs to see a more dovish FOMC, the yen (-0.6%). You may remember last week when the yen, after making yet another new low for the move, suddenly reversed course ahead of the July 4thholiday. While there was no actual intervention, the discussion was that the MOF would no longer discuss their intentions ahead of any intervention and with a holiday weekend seeing reduced liquidity, many anticipated some action. Well, as you can see from the chart below, that idea has essentially been erased with the yen softening again and pushing back to those lows seen last week.

Source: tradingeconomics.com

Bloomberg ran an article this morning about a former Vice Minister from the MOF explaining his view that the yen was undervalued by 20% or so. If we look at the yen on a PPP basis, the IMF claims the value should be about 93-95 instead of the current 162+. The Economist’s Big Mac Index calls for 78.00, and by all accounts, visiting Japan is relatively inexpensive for most foreigners. In fact, I read that Japan was increasing the visa fees to try to discourage the massive amount of tourism as people around the world see it as a cheap destination.

Ultimately, the problem with the yen, in my view, remains that real interest rates remain deeply negative and the government’s spending plans continue to indicate massive deficits as far as the eye can see. While reduced energy prices are a boon, the yen was falling sharply long before the Iran conflict began. Policy changes of substance are required, and they are still uncomfortable for domestic politics. While the pace of the yen’s decline may slow, I still see it weakening going forward.

So, let’s briefly look at markets overnight before closing. Regarding the dollar, it is broadly stronger this morning with only BRL (+0.3%) finding any support despite their ignominious defeat to the Norwegians. But modest slippage across the G10 is the rule, -0.1% to -0.2%, while similar movement has been observed in the rest of the EMG space. For now, the yen remains the only interesting currency.

In the commodity markets, despite oil’s continuing slide, this morning the metals (Au -0.4%, Ag -0.6%, Cu -0.1%) are also under pressure, but that accords with the dollar’s strength. As long as the dollar remains bid, it appears the metals markets will have difficulty gaining traction. But if I am correct regarding the Fed and the market turning toward a more dovish view, I would look for the metals to head higher again.

In the bond market, Treasury yields (-3bps) are slipping as the market reopens after the holiday weekend, arguably following through on the softer payroll data. European sovereign yields are little changed to lower by -1bp amid a quiet market while JGB yields (+4bps) are the notable outlier, arguably as concerns rise over the weakening yen.

Finally, equity markets remain beholden to the semiconductor and AI trade and with the US having been closed on Friday, there was less information for the rest of the world. But this morning, NASDAQ futures (+0.9%) look like they are set to resume their march higher, dragging the S&P with them. But this follows a mixed to lower session in Asia (Tokyo 0.0%, China 0.0%, HK +1.1%, Korea -0.5%, India +0.7%, Taiwan -0.5%) as leadership was lacking. Not surprisingly, European bourses are also mixed this morning (Spain -0.7%, UK -0.2%), Germany and France both +0.1%) as the question of note is how much defense investment is going to be forthcoming from NATO and European nations and how much of that will be spent in Europe. Perhaps excitement in the US will help global risk appetite as the day wears on.

On the data front, it is a quiet week for numbers with just the below on the docket:

| Today | ISM Services | 54.0 |

| Tuesday | Trade Balance | -$78.0B |

| Wednesday | FOMC Minutes | |

| Thursday | Initial Claims | 220K |

| Continuing Claims | 1810K | |

| Existing Home Sales | 4.20M |

Source: tradingeconomics.com

As well, we hear from three Fed speakers, Waller, Williams and Logan. Now it will be interesting to see if any of them start to discuss the lower energy prices and how that is likely to moderate their inflation concerns. If we do hear something like that, I expect the Fed funds table above will reflect that quickly. We shall see.

It is summer, and there is not much new to discuss. With the US playing Belgium tonight, all eyes will be there, and my take is we are not looking forward to a terribly exciting session today.

Good luck

Adf