For OPEC, the times are a changin’

With membership now rearrangin’

Thus, looking ahead

They’ve nowhere to tread

With more nations set for estrangin’

The proximate cause is the war

Which Gulf members rightly deplore

Meanwhile the blockade

Will keep throwing shade

On all their decisions before

One of the key features of the Fourth Turning, as so ably described by Neil Howe and William Strauss in their 1997 book of the same name, is that it is a time when institutions that have been part of the global system are torn down as they are no longer fit for purpose. By the end of the turning, new institutions have arisen to take over those roles going into the future.

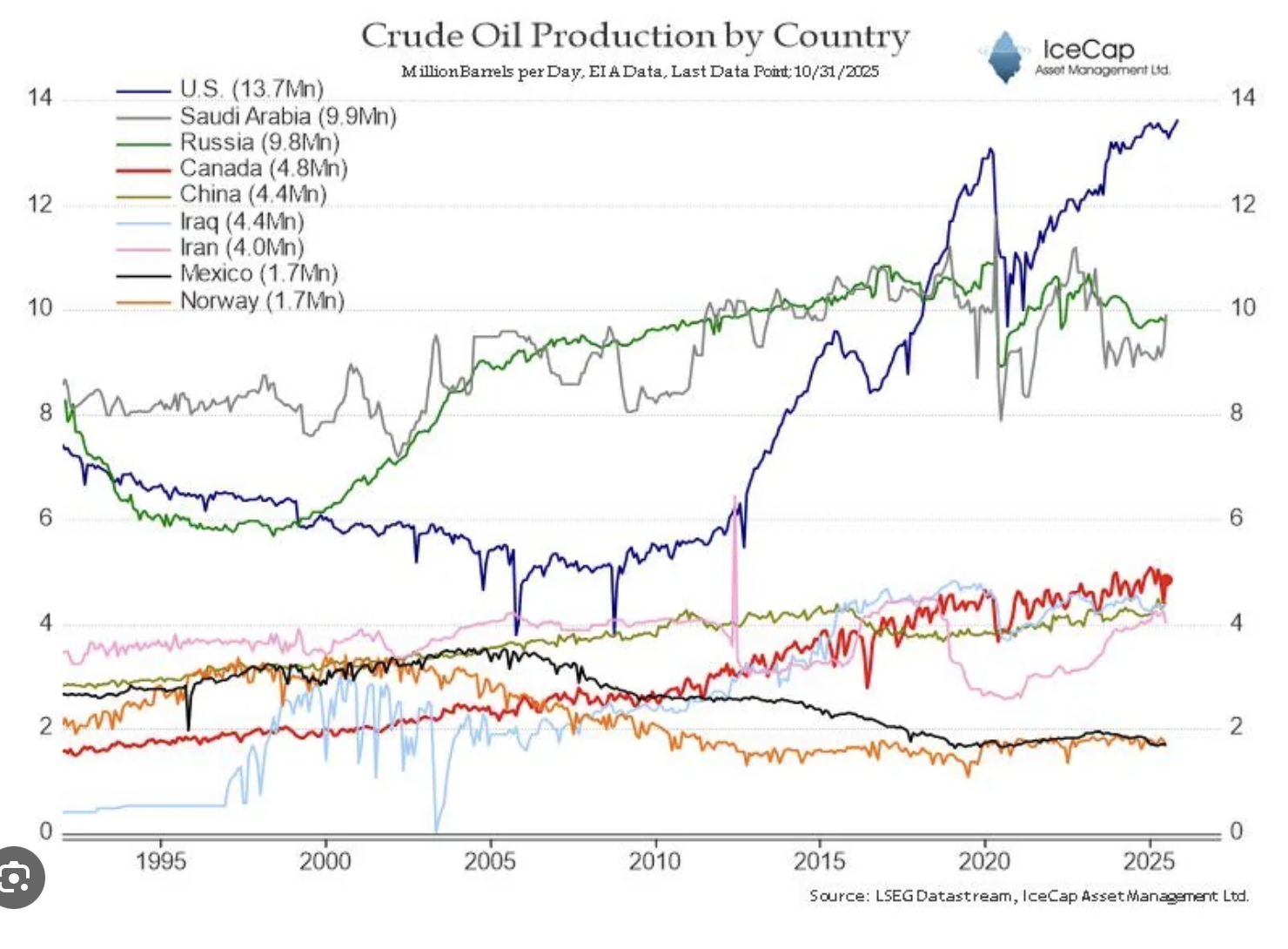

I will be the first to say that I don’t have any idea what may replace OPEC, but with the UAE’s announcement that they are exiting the group as of Friday, May 1st, OPEC is in a world of trouble. OPEC was founded in 1960 as Gulf states sought to establish control over oil markets that had been developed by the “Seven Sisters” major global (and notably foreign) oil companies. Of course, the 1973 oil embargo and the follow on in 1979 cemented their power for two generations. Thus, Saudi Arabia and friends punched far above their weight on the global stage because of their oil reserves.

But the fracking boom in the US in the 2010’s laid the groundwork for OPEC’s demise as suddenly, not only was there a major producer outside the group (there had always been a few like Norway and the UK), but there was a major producer that had power in its own right. Thus, the seeds were sown back in 2014 or so, as fracking in the US took off, for the end of this organization. And that’s where we stand today. The US is the largest producer of hydrocarbons in the world by a long shot these days, as not only do they dominate oil production, but, too, natural gas and associated liquids.

So, now the world’s last standing superpower is no longer reliant on imported energy, and in fact, is a major energy exporter. Remember, energy = life, or put another way, energy = economy. Arguably, this is the biggest geopolitical shift the world has seen in decades, since the end of the Cold War.

Returning to the thesis of institutions being torn down and rebuilt, I cannot foresee what type of institution is even necessary to replace OPEC. Arguably, it will slowly disintegrate as it has lost all its coercive power, and each nation will simply pump as much oil as they can going forward. For everyone who believes there is a long-term shortage of oil, and that oil prices are heading higher, I will take the other side of that bet. History has shown that every shortage is followed by a glut, and this one will be no different.

There are many commentaries that Iran can withstand the US naval blockade longer than President Trump can stand the political heat. I disagree with that on both sides of the equation. First, as a second term president, Trump is not seeking re-election and just doesn’t give a f*ck about a lot of things. Second, any stress Iran has felt in the past occurred while the government and infrastructure there were completely intact. Now, Ahmad Vahidi, the effective leader of the nation, lives in a series of holes in the ground with no electronic communications because he knows that his days are numbered if he becomes public, and that’s a hard way to govern. Second, the extraordinary damage that has been inflicted on the nation from the bombing campaigns has resulted in much less tolerance for additional stress. Add to that the blockade is starving Vahidi and the IRGC of money to pay their proxies and soldiers, and the fact that at some point soon, Iranian oil wells are going to start to be shut in risking permanent damage, and Iran’s options are few and shrinking.

Right now, oil prices (+3.3%) are continuing to trade higher, although have not yet returned to the initial spike levels from the opening night of the attacks and they could climb higher still in the short-term. But I am highly confident that by autumn, they will be much lower as the roughly 1 billion barrels that are around in floating storage and stuck in the Persian Gulf come back to the market.

Source: tradingeconomics.com

In the meantime, this will continue to lead the news, but my view is this is already a fait accompli. However, until such time as it ends, we must deal with the daily twists and turns. Personally, I think it is healthy that there is another topic of interest, AI and the associated companies and their stocks, which has captured a growing share of the market’s collective mindshare. We need more than one thing lest every X-pert who previously knew about Covid, Ukraine, Russia and now Iran, would suck up all the air in the room.

Touching quickly on AI, Torsten Slok, the Chief Economist at Apollo, posted an interesting, and I believe very useful, take on AI and its future impact on employment, calling it The Jevons Employment Effect. In essence, as William Stanley Jevons explained for coal in 1865, the more efficient use of a resource results in increased demand for that resource. So, Slok’s idea is that as workers become more efficient, there will be more demand for efficient workers which will expand economic output as productivity is enhanced. Worth a thought to counter the entire black pill view that AI is going to take all the jobs.

Ok, I’ve gone on too long, so let me quickly tour markets here. The inverse relationship between precious metals and oil remains in place with gold (-0.6%) and silver (-0.4%) both softer this morning. We did learn that central bank purchases of gold in Q1 rose to 244 tons as they took advantage of the decline in prices post the peak. Considering my view that oil’s price is going to fall sharply going forward, I think that may bode well for gold then.

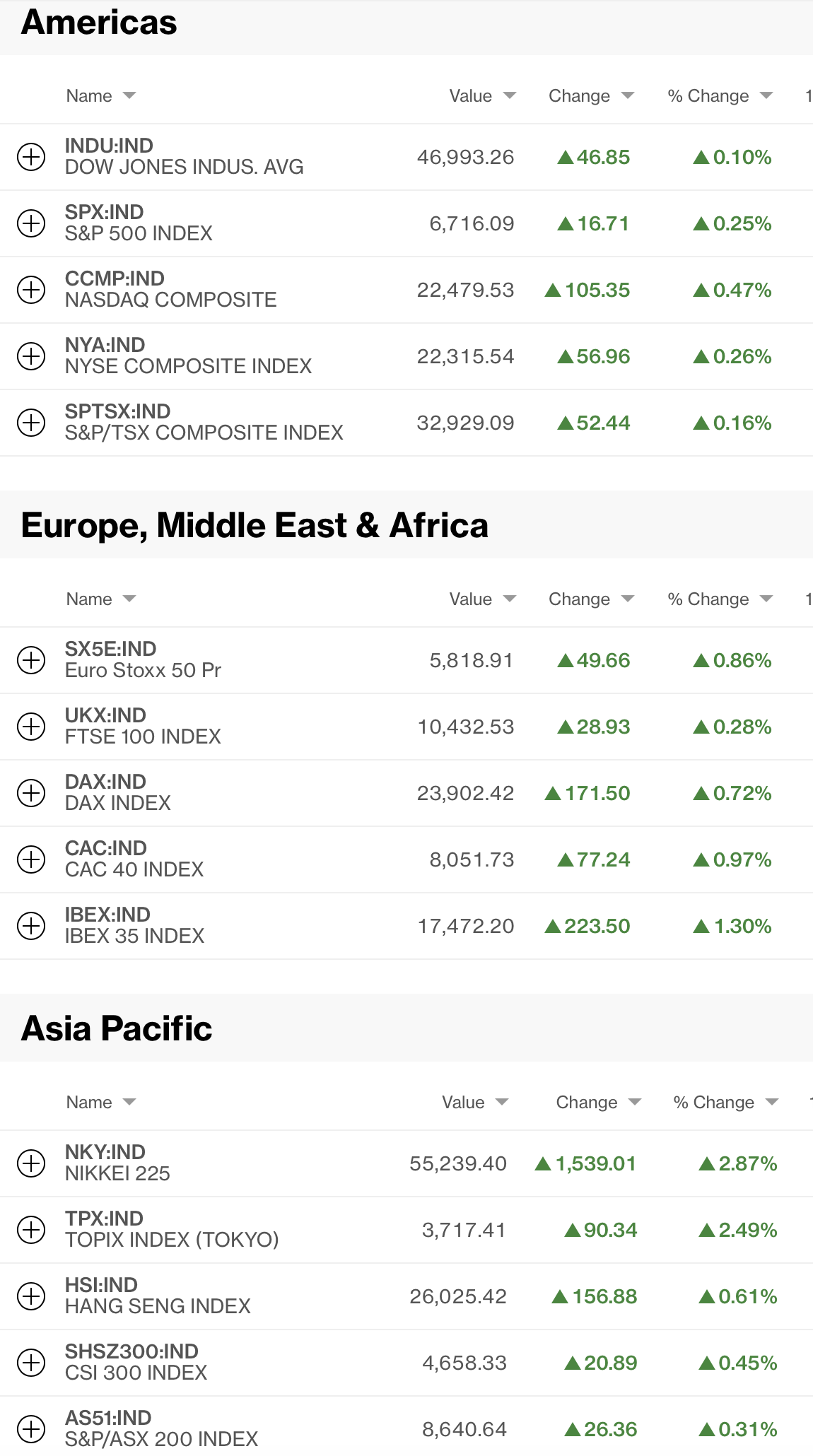

In equity markets, yesterday’s declines in the US were followed by a mixed session in Asia with Japan the perfect symbol as the Nikkei (-1.0%) fell while the TOPIX (+0.6%) rose along with most other Japanese indices. China (+1.1%), HK (+1.7%), Korea (+0.7%) and India (+0.8%) were all in fine fettle although other regional exchanges were less optimistic overall. Turning to Europe, though, red is today’s color, with the UK (-0.8%), Spain (-0.7%) and France (-0.6%) all under decent pressure after inflation data showed continued stickiness which will prevent any central bank easing tomorrow by either the BOE or ECB, although the idea that either will hike rates remains ludicrous in my eyes, but they are error-prone, I will give them that. As to US futures, at this hour (7:30) they are hanging around unchanged ahead of the FOMC meeting this afternoon.

In the bond market, yields are creeping higher across the board with virtually every market currently open in Europe and the US showing yields higher by 1 basis point. It is hard to get excited here.

The dollar, too, is dull and boring today with little movement broadly. NOK (+0.65%) is responding to the ongoing rise in oil prices, as is BRL (+0.4%) which is also benefitting from the idea that rising inflation will prevent the BCB from cutting rates much further. On the flip side, ZAR (-0.4%) is under pressure on the back of gold’s weakness and rising oil prices as they import the bulk of their energy. But the G10 is a bit boring with the exception of AUD (-0.3%) and NZD (-0.4%), both of whom released CPI data last night that while high, was not as high as forecast.

And that’s really it for today. I chuckled at an article in Bloomberg discussing Chinese companies and their needs in the FX market as they explained it could move the CNY between 6.80 and 6.85, which given the current rate is 6.836, means it’s not moving at all!

On the data front, before we hear from Powell at 2:00, hopefully for the last time, we get Housing Starts (exp 1.4M), Building Permits (1.39M), Durable Goods (0.5%, 0.4% ex Transport) and the Goods Trade Balance (-$87.0B), with the FOMC statement and comments clearly the most important thing. Then, this evening after the close we get earnings reports from MSFT, META, GOOG and AMZN, which has the market on tenterhooks.

The clock is ticking in Iran and that remains the biggest unknown, its timing, for the market and the world writ large. Let’s hope it ends soon.

Good luck

Adf