Chairman Warsh, to the House, testified

And explained that his tolerance died

For higher inflation

Throughout this great nation

And ‘bout this, he will not backslide

But prior to his starlike turn

Investors and markets did learn

That CPI fell,

Though not a death knell,

And caused, for rate hawks, some heartburn

It is better to remain silent and be thought a fool than to speak and remove all doubt. – Abraham Lincoln

The attributed saying above, while not certain that it was uttered by President Lincoln, still makes its point eloquently, as well as somewhat humorously. And I strongly believe that every member of the FOMC should take it to heart before they speak. In fact, they should be thanking Chairman Warsh for his efforts to shut them up, because then they won’t sound quite so foolish.

For instance, just Monday, Governor Waller, in a speech in New York, finished with the following line, “But I don’t take the inflationary signals I have discussed today lightly. If we get another hot reading on core inflation this week, then the FOMC will need to consider tightening monetary policy in the near term.” Oops!

And this is one of the issues because many believe that the FOMC gets the data earlier than the release date and so have inside information. Thus, when Waller talks about the risk of a hot print, many think he knows something. And this is yet another reason that ending forward guidance and reducing the commentary of the FOMC will be valuable.

By now, I am sure you are aware that yesterday’s CPI reading was the largest downside miss since Covid in 2020, with the headline number falling -0.4% on the month and the annual slipping back to 3.8% while the core number was flat with the annual falling to 2.6%. Now, as the Inflation Guy explains, this was the product of numerous subcomponents declining, not just the price of oil/gasoline and this is not the venue to discuss them (read the link).

But it certainly helped Chairman Warsh in the timing of his testimony as nobody there could ‘blame’ him for still rising prices, at least for now. As expected, several House members tried to get interest rate information from him, but he remains firm that the Fed’s mission is to drive inflation lower and this will be done through both interest rate and balance sheet policy changes, not through forward guidance.

It is not surprising that the market responded dramatically with the following chart from Polymarket (taken from Kobeissi on X) showing an impressive change of heart.

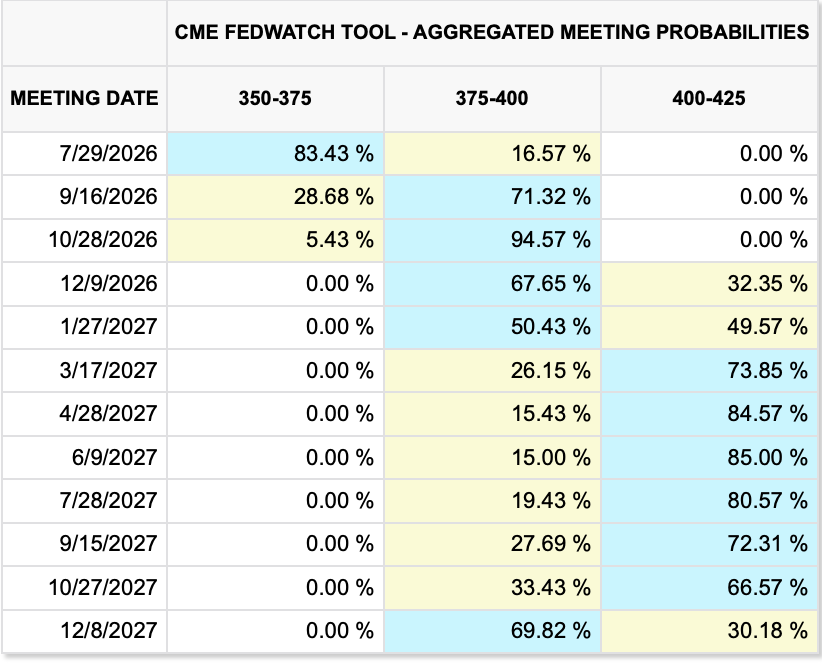

While I use the Fed funds futures chart from the CME as my guidepost, there is something to be said for the wisdom of crowds here. Remember, this is a binary call, not a gradient one. But even the futures markets adjusted significantly, and rightly so, with the probability of a July hike there falling to 16% from 40% when I wrote yesterday morning. As well, while there is still more than one rate hike priced for 2026, the calculated change has declined to 33bps from 43bps yesterday morning.

Source: cmegroup.com

Skepticism remains rife regarding Chairman Warsh and his attempt to change the way things are done at the Fed, but personally, I am quite optimistic that he is attacking the real problems. Remember, the Fed is a 114-year-old institution with an extremely long memory and a staff that, like most of government, believes they know what is best for others. I strongly subscribe to the monetarist view that printing more money leads to more inflation, but making a change that dramatic all at once is just not possible. Let us be thankful that Chairman Warsh appears to have a better understanding and is working to change things. And remember, he has only been in the Chair for two months, give him some time.

As I start to recap markets, it is quite interesting that the price of oil seems to have decoupled from the war in Iran. I say this because as I type at 7:15, a bit more than an hour after CentCom explained they had instituted another wave of military attacks on Iran, WTI is largely indifferent to the news. While it has edged higher by 0.7%, a look at the chart below of the past 24-hours shows essentially no response.

Source: tradingeconomics.com

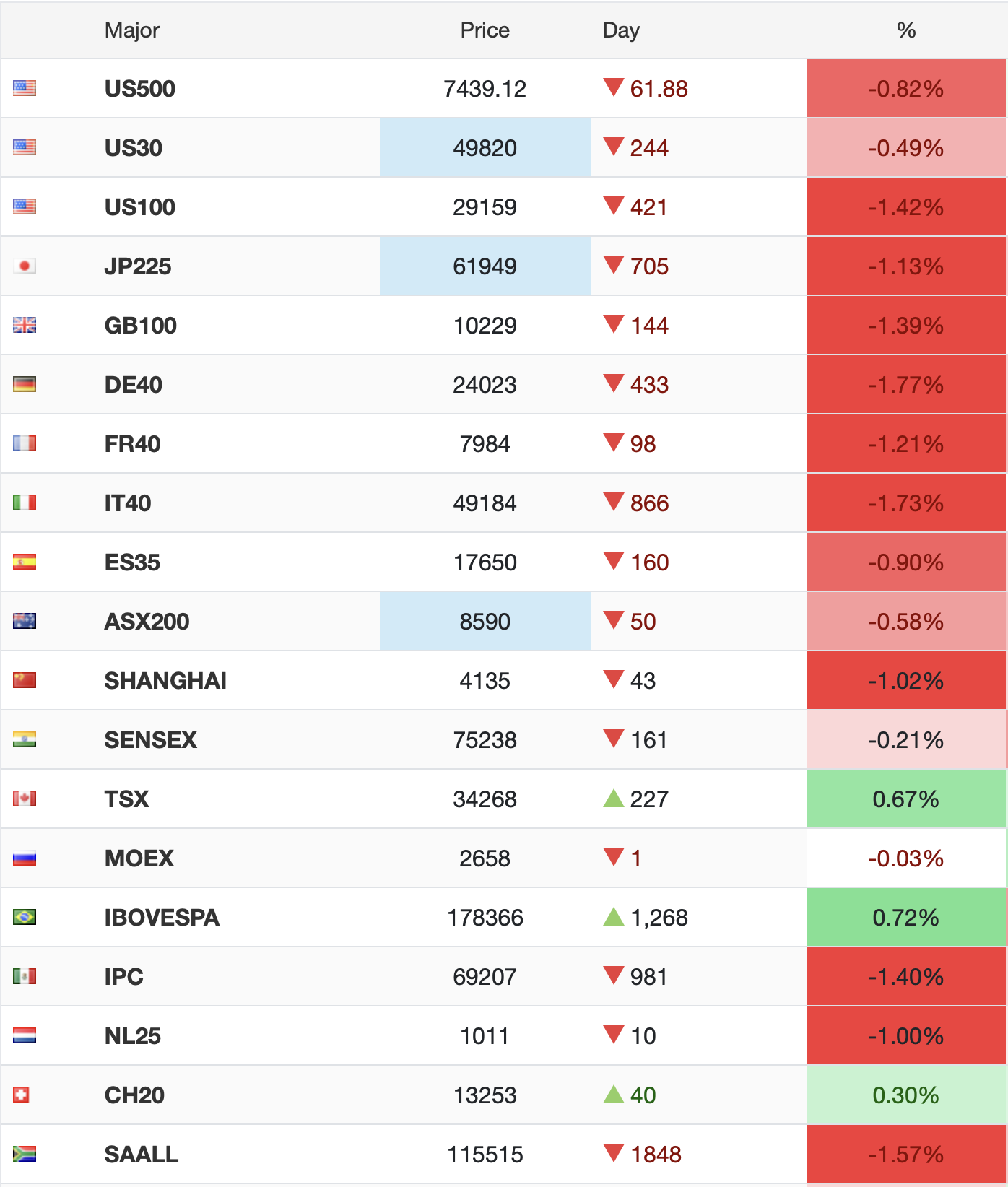

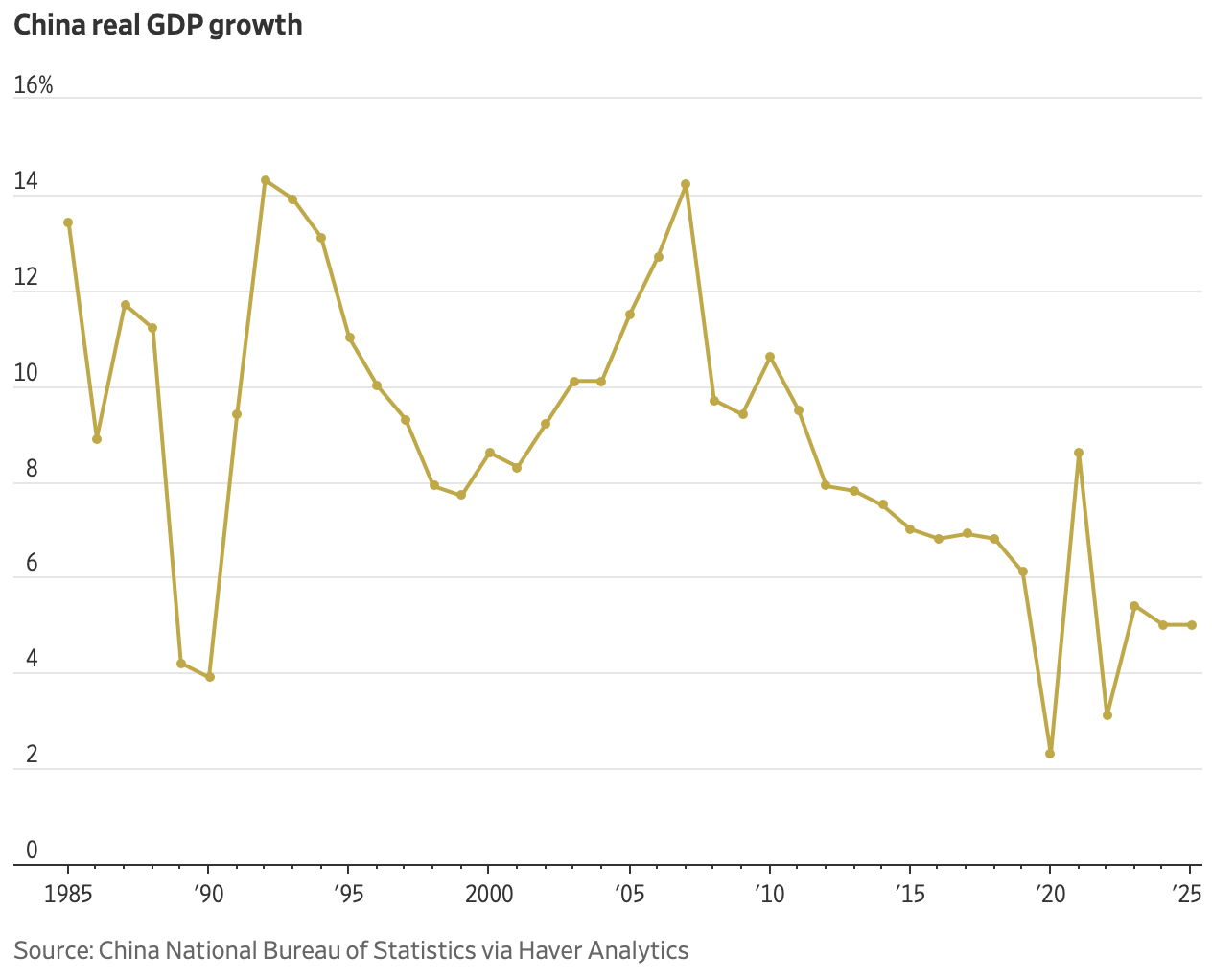

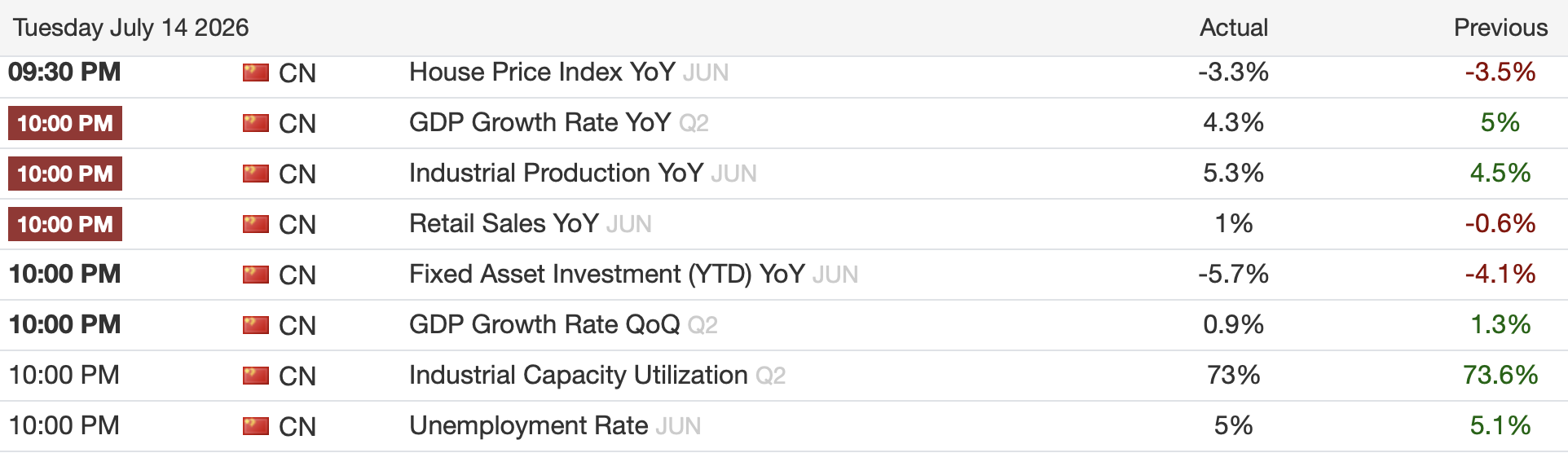

So, let’s turn to equities, which rallied on the CPI data in the US yesterday and saw follow through in Asia with Tokyo (+1.5%), HK (+1.4%) and Korea (+6.25%) all having strong sessions as did almost every market in the region. However, there was an exception, China (-0.2%) which while not disastrous, substantially lagged other markets. Arguably, the proximate cause of that disappointment was the disappointing data released last night as per the below:

Source: tradingeconomics.com

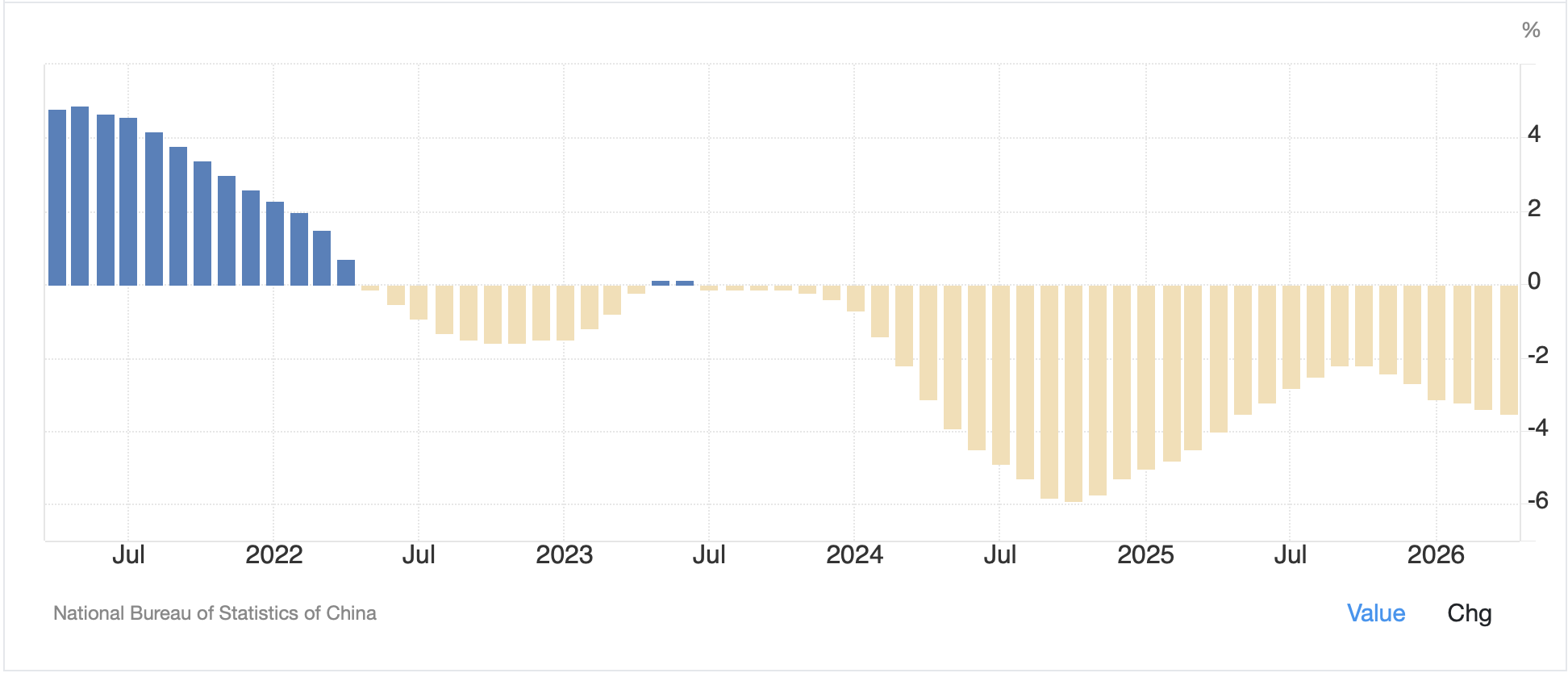

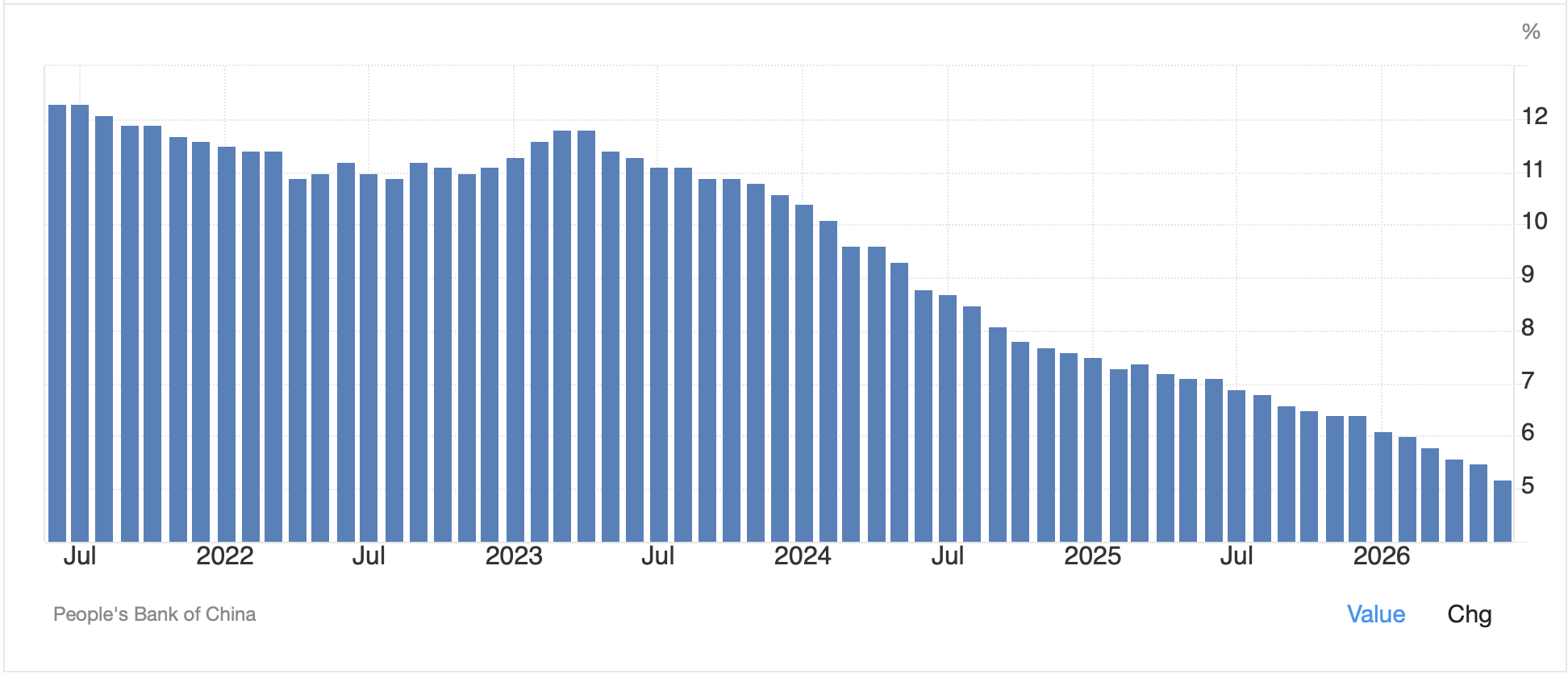

Certainly, GDP at 4.3%, below even Xi’s reduced target must be concerning and Fixed Asset Investment (housing) continues to crumble. It is very difficult to look at this data, as well as their monetary data which, for instance, shows loan growth not merely trending lower, but doing so at an accelerating rate as per the below chart and conclude things are going will there for the economy or the equity markets.

Source: tradingeconomics.com

Europe, though, continues to lag with all the major bourses lower as the DAX (-0.8%) leads the way followed by Spain (-0.6%) and then France and the UK both slipping -0.2%. (I guess World Cup results are not indicative of their equity markets!). As to US futures, at this hour (7:25) they are all up very slightly.

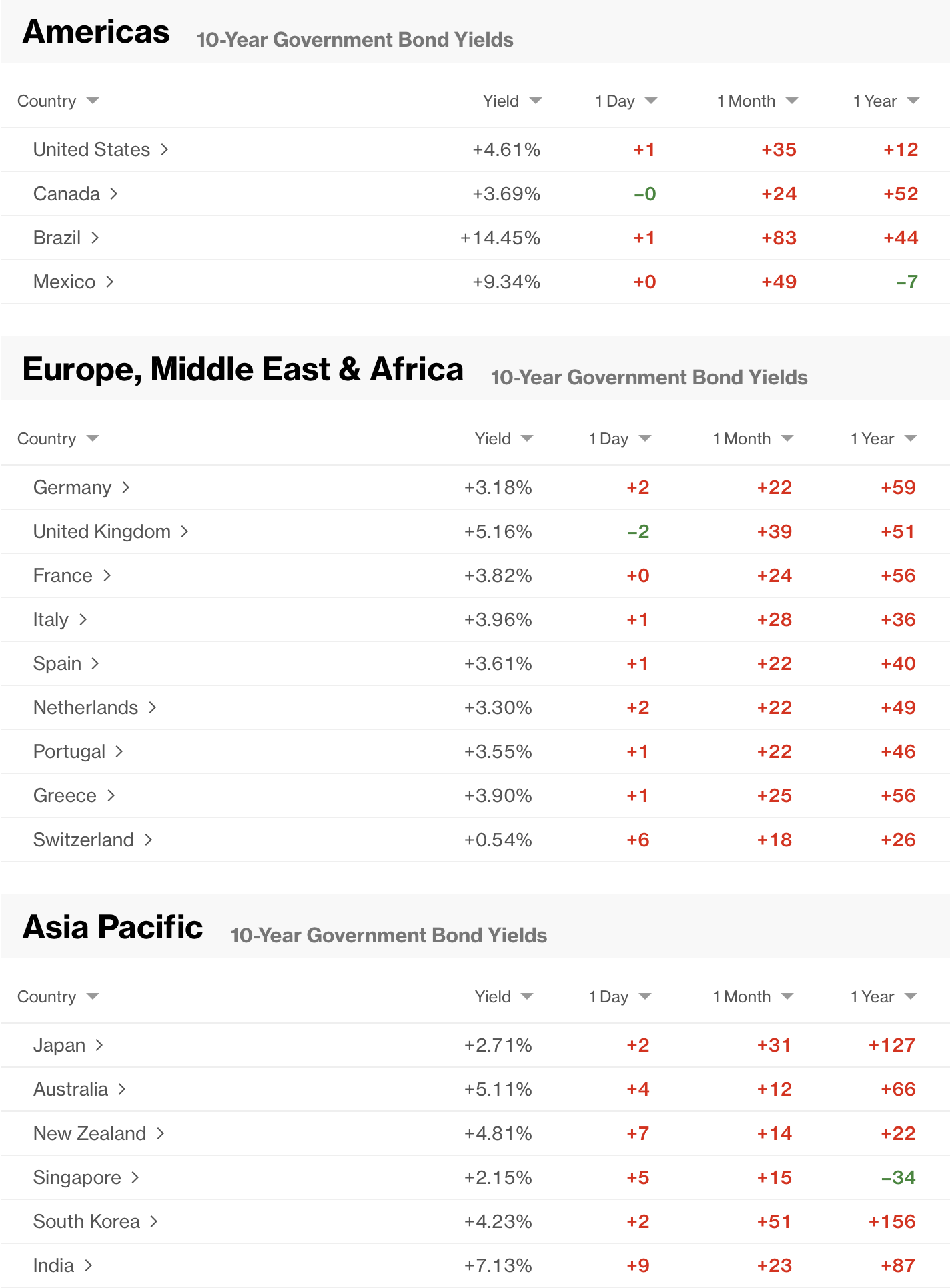

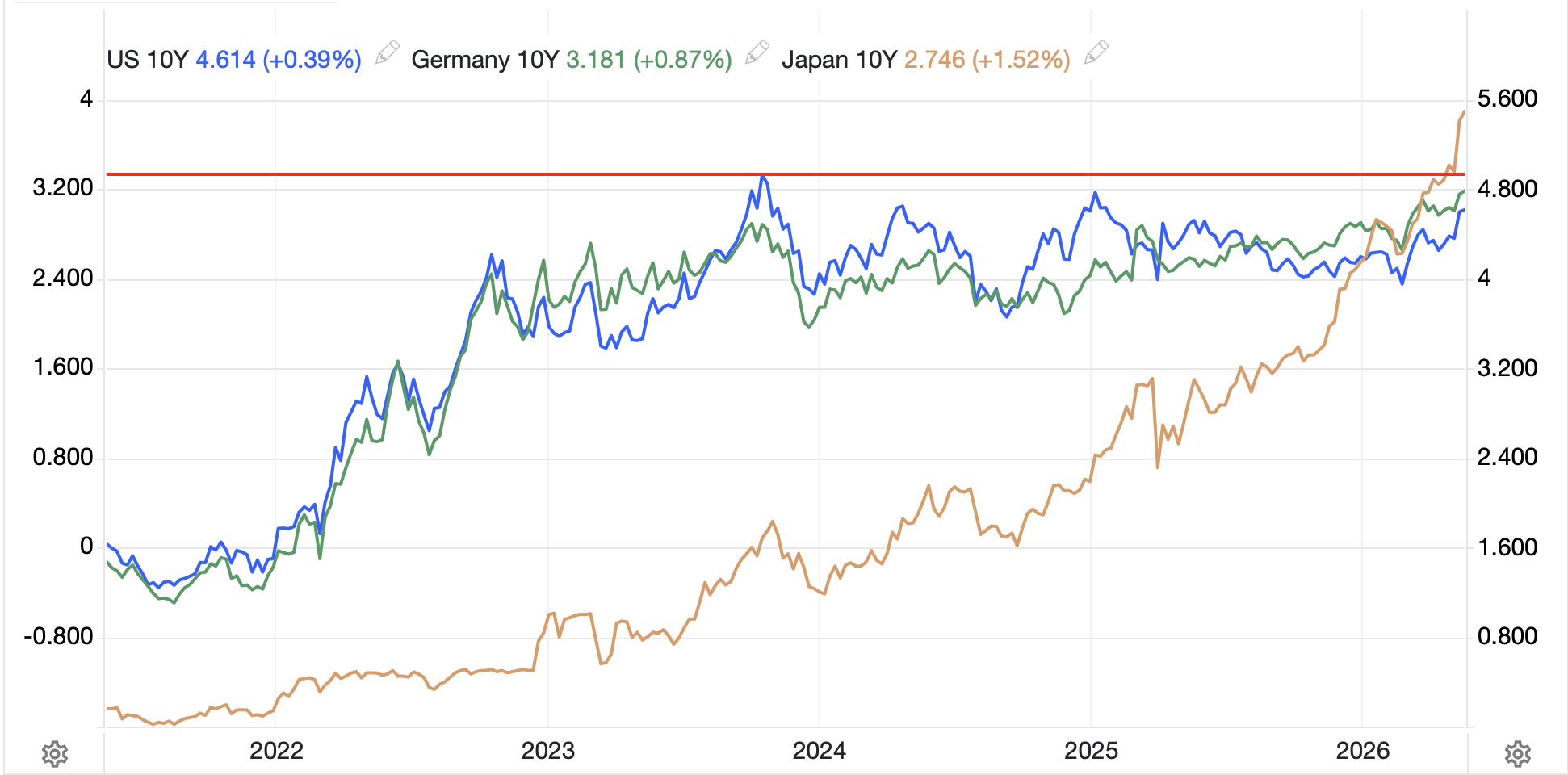

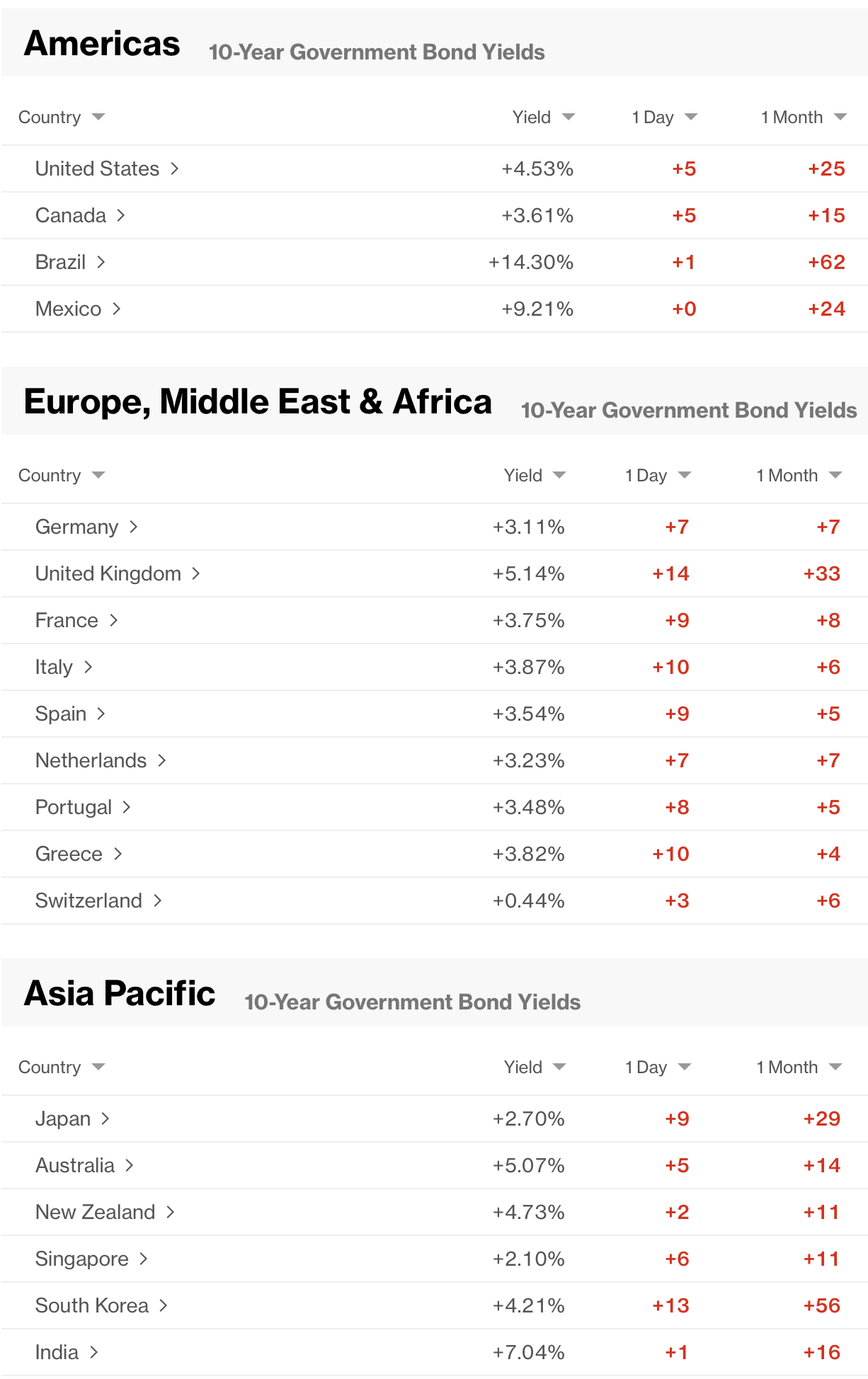

Bond yields fell yesterday, notably the 2yr slipping -6bps, while the 10yr only fell -3bps. This morning, though, yields are edging back higher with Treasury yields up 2bps and European sovereign yields higher by between 3bps and 4bps. While equity markets remain sanguine about Iran, it seems bond markets are having a tougher time. JGB yields (-2bps) are bucking the trend as there are still those who are looking for Japanese pension funds to start bringing more money home.

While the metals markets rallied yesterday, this morning they are under pressure again with gold (-0.6%) and silver (-1.2%) giving back yesterday’s gains while copper (-0.3%) is consolidating after jumping a dime yesterday.

Finally, the dollar is sidelined this morning with no notably large movements in either the G10 or EMG blocs. A brief word on the yen, which has certainly been the subject of much digital ink spillage lately, as it seems all those thoughts of the pension fund support for the yen are not part of the FX conversation. We remain less than 50 pips from the peak seen back on June 30 and I see very little reason for the broader trajectory to change. The BOJ is not going to waste its reserves in this process, and given the gradual movement, I don’t think they are that upset. As long as PM Takaichi is planning to spend more money, whether on infrastructure or investment, given they are borrowing all of it, a strong yen seems highly improbable.

On the data front, this morning brings PPI (exp 6.2% headline, 5.2% core) and the Empire State Manufacturing Index (8.8) at 8:30. Then, at 9:45 the BOC will most likely leave their base rate on hold at 2.25% and at 10:00, Chairman Warsh will testify to the Senate Banking Committee. We also get the Fed’s Beige Book this afternoon, EIA oil inventories and three more Fed speakers, although with Warsh speaking, will anybody care? Especially since they continue to make fools of themselves with their own forward guidance.

The most remarkable thing to me is how insouciant market participants have become despite increased hostilities in the Gulf. But both oil and equity traders have seemingly decided that other things matter more. With that in mind, it is hard to get excited about too much these days. Unless we see markets breaking their recent ranges, in either direction, I suspect that the weight of summer, and reduced liquidity is going to prevent anything substantial from happening anytime soon.

Good luck

Adf