The meeting between Trump and Xi

Had little but hyperbole

So, markets now turn

To their key concern

Inflation that’s grown one, two, three

While oil has garnered attention

Tis yields and their latest ascension

That’s starting to bite

And causing a flight

Of buyers, and lots of press mention

And one more thing that you should know

Is China continues to slow

Through all of Xi’s bluster

He simply can’t muster

His people to get-up-and-go

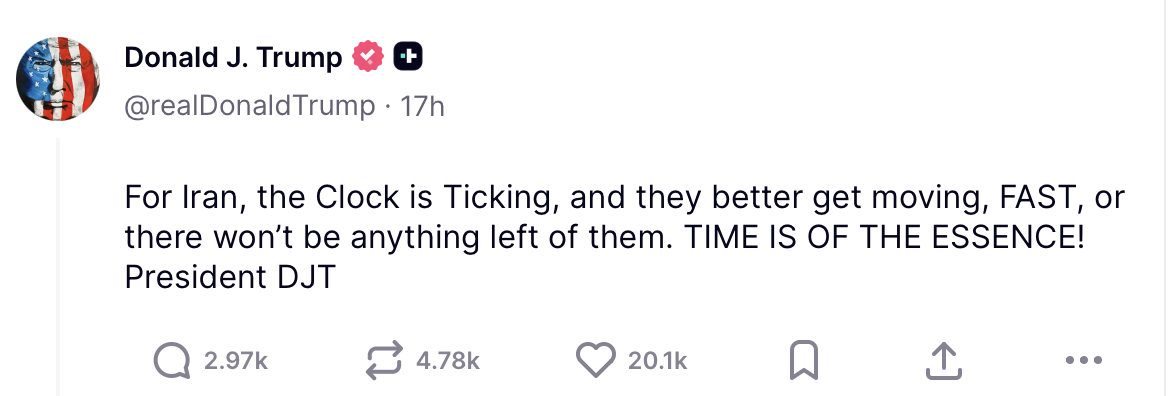

As we begin a new week, a quick review of the last one shows that the much-touted Trump-Xi summit didn’t seem to address any of the current problems, at least as defined by what financial markets deem problems. These are the lack of transit ability through the Strait of Hormuz, with the resultant limit on oil supplies and the resulting rise in prices and inflation as energy prices feed into the price of everything else. I guess it was always a great leap to believe that this summit was going to end the war, and depending on which side’s comments you read, China has either agreed, or not, to try to push Iran to reopening the Strait. Certainly, they would like that to be the case, but thus far, as I type Monday morning, there has been no further movement. In fact, last night, the President sent this message out.

I guess we cannot rule out a further escalation of military action in Iran at this point, and I imagine the oil market will not be pleased.

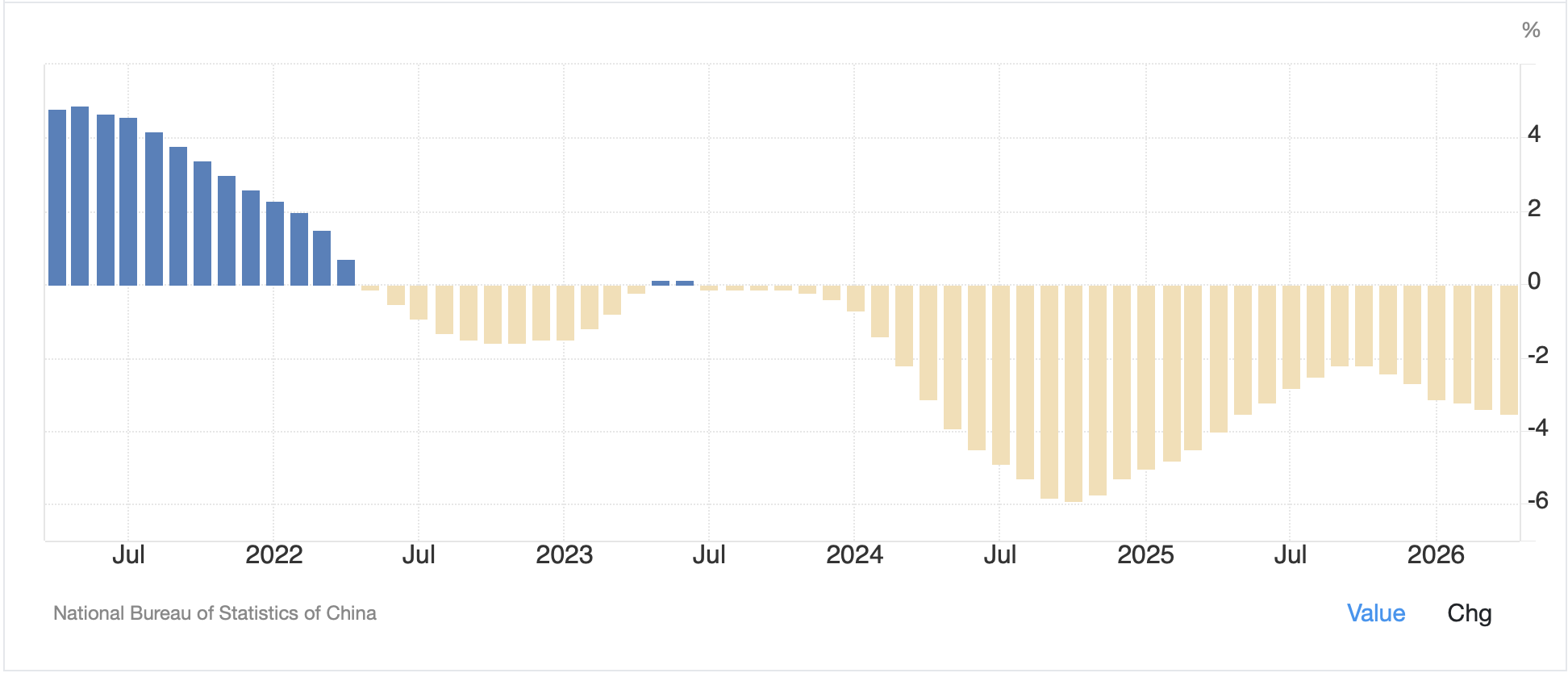

Speaking of China, though, while many want to continue telling the story that they are weathering the Iran conflict with limited impact because they had stockpiled so much stuff ahead of time, below are their latest economic data statistics, a grouping that does not shout, at least to me, of a nation hitting on all cylinders.

Source: tradingecomomics.com

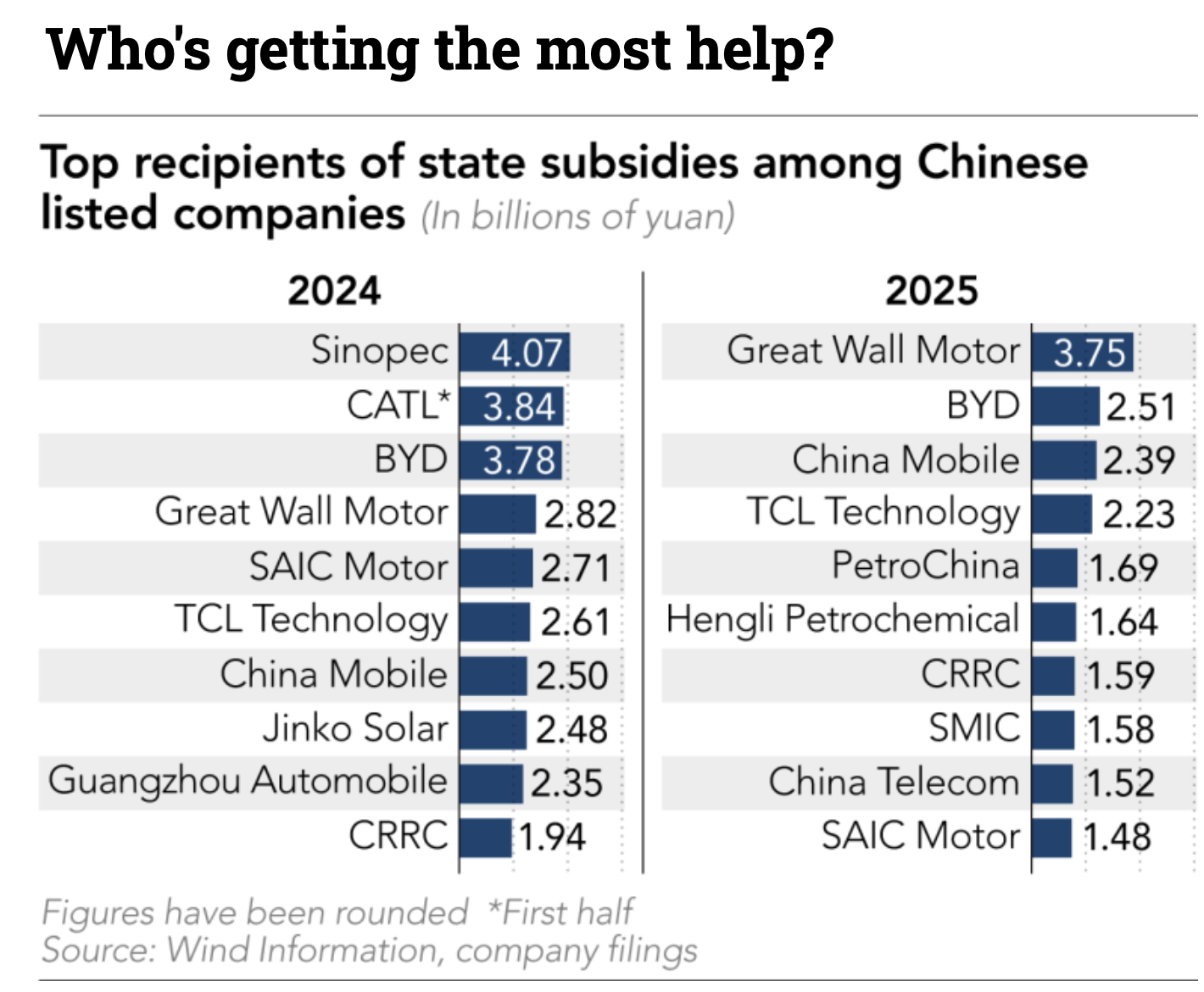

I am confident that we will once again hear about all the stimulus that President Xi will soon add to the Chinese domestic economy as they seek to increase the proportion of domestic activity compared to their export focus. But I would take the under there. First, if you thought that politicians in the US didn’t care about their constituents, compared to Xi, they wait on their constituents hand and foot. But history has shown that China’s model is to support chosen industries, as I showed on Friday, and subsidize them so they can learn to dominate all competitors.

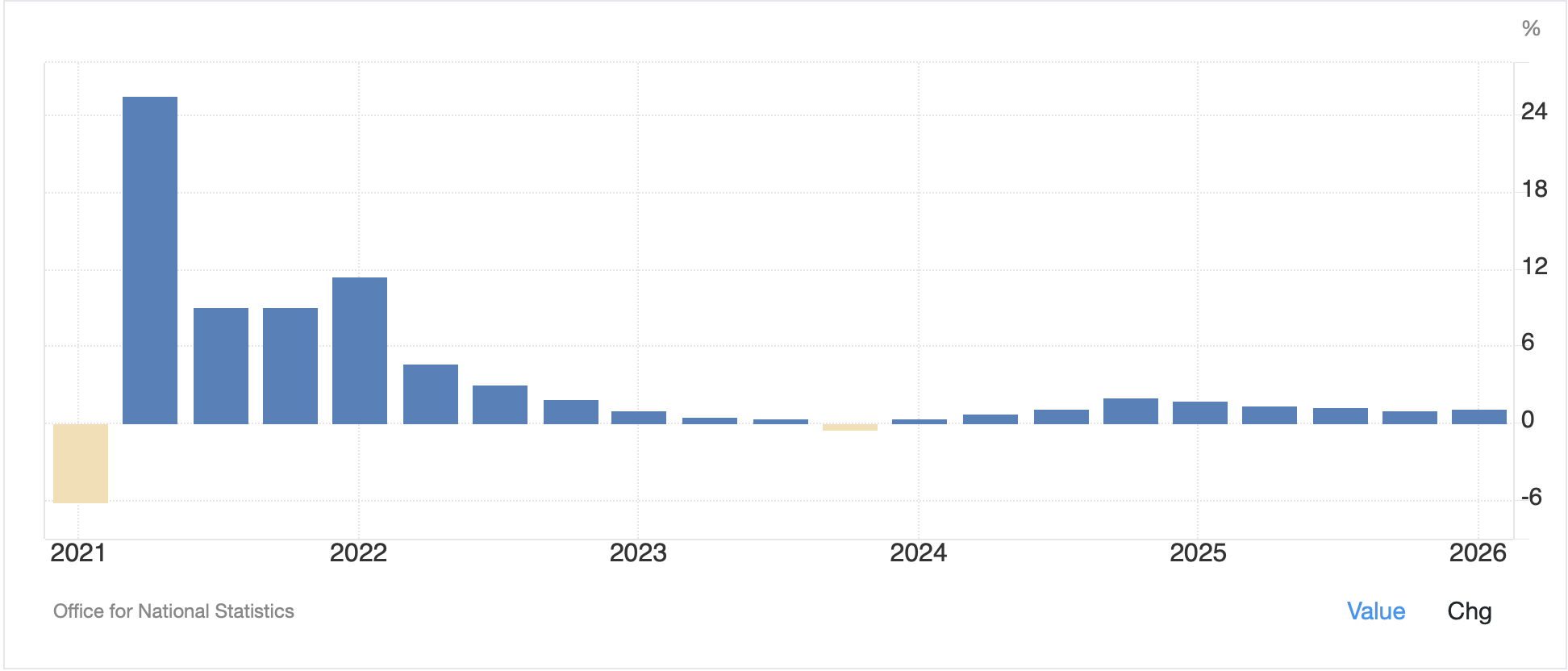

Arguably, the one time they were willing to subsidize the domestic economy was with the property market, although that simply led to the construction of the so-called “ghost” cities, where people invested in the property bubble, as they had few other outlets to save money, and enormous amounts of resources were consumed to build cities that never had any occupants. Alas, for all those investors, those cities still don’t have occupants, and with a shrinking population, never will. The property market has been shrinking in value for 4 years now and shows no signs of slowing as per the below chart of the House Price Index from above.

Source: tradingeconomics.com

While things are certainly not perfect here, China’s got problems as well, just remember that.

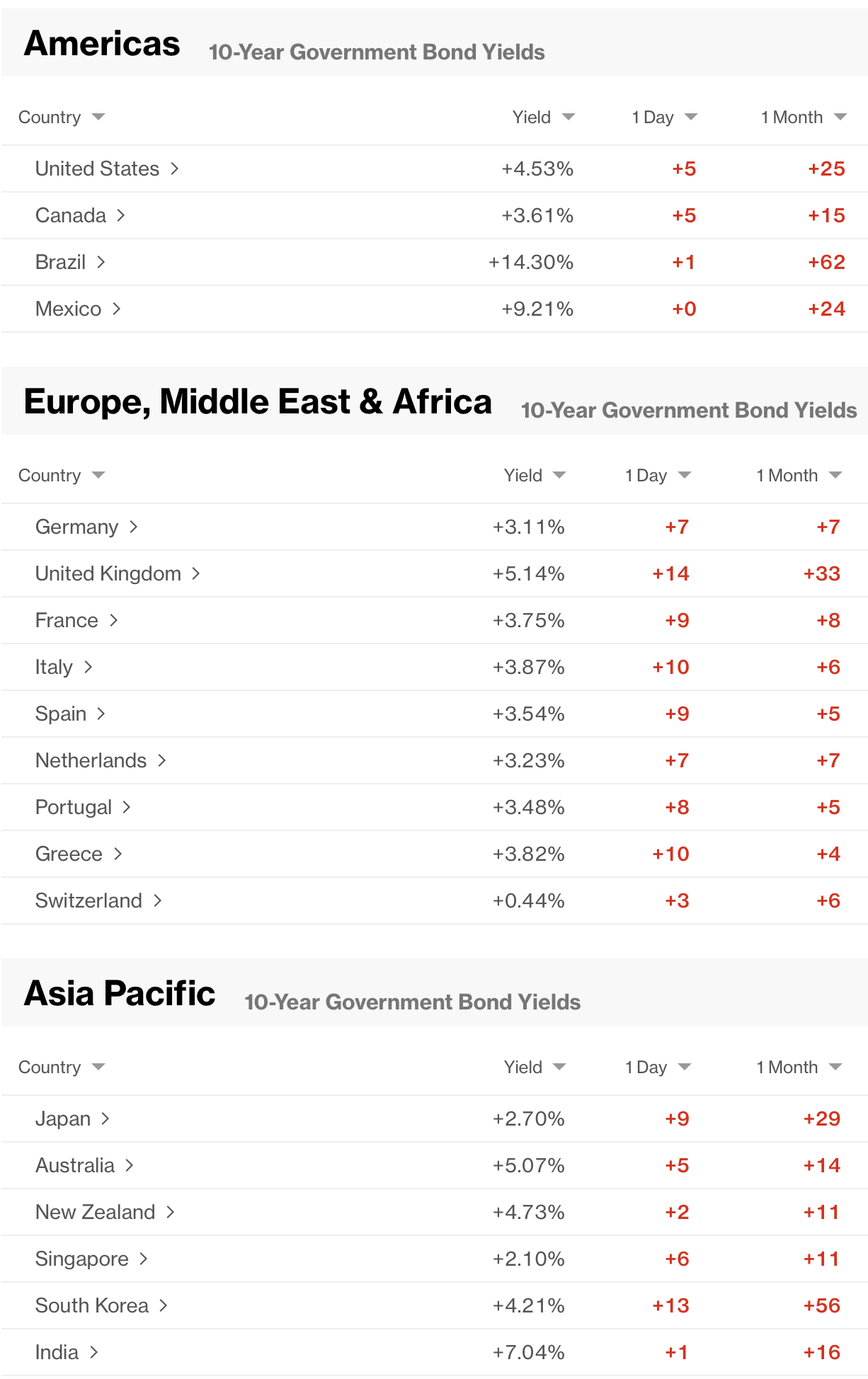

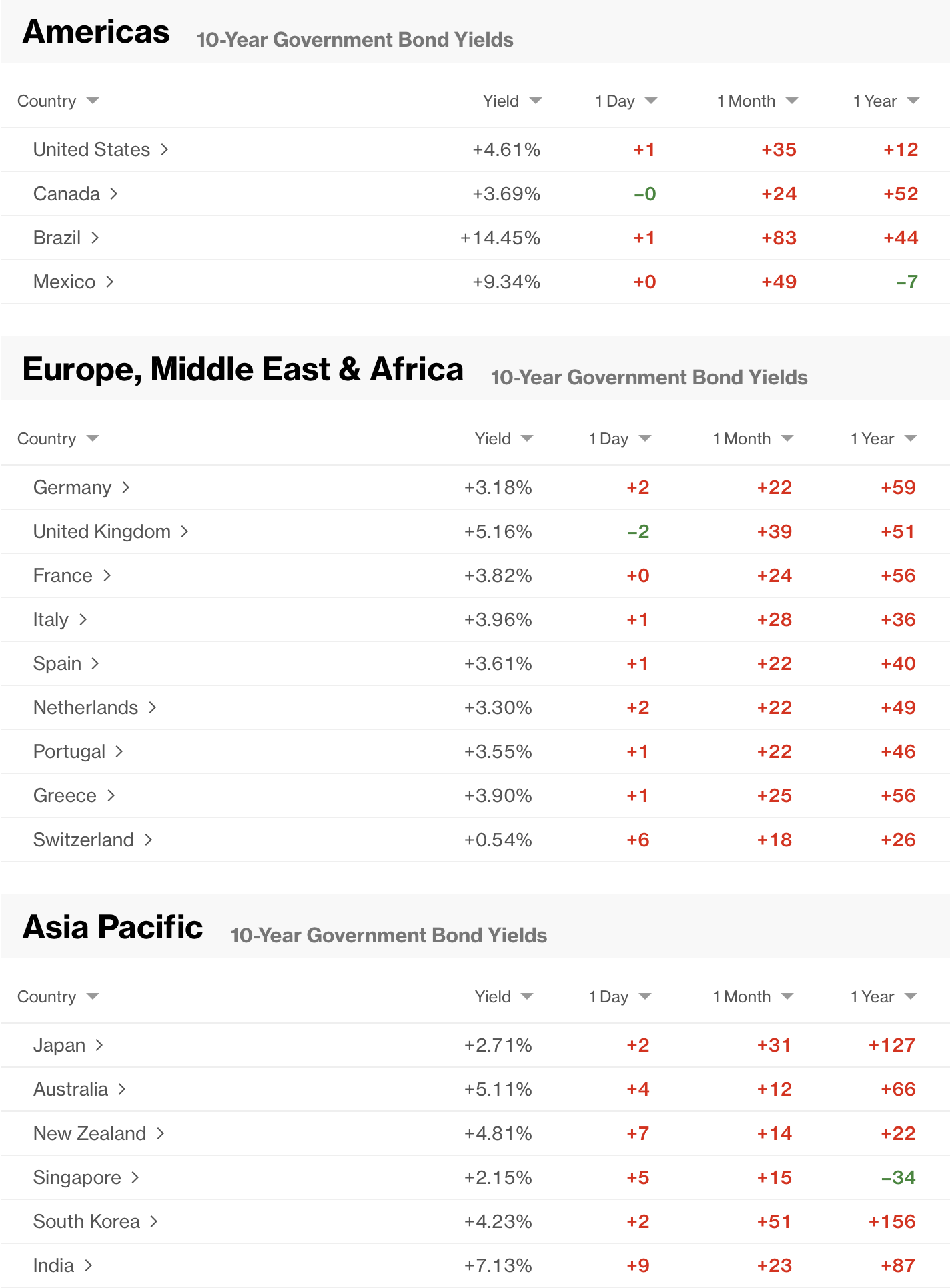

But arguably the real story right now is bond yields as Treasury yields, and those almost everywhere else in the world, continue to rise. As you can see from the Bloomberg screenshot below, while the overnight movement has not been excessive by any stretch, yields have now risen pretty aggressively over the past month, and year, and are trading at their highest levels since the 2022 inflation peaks.

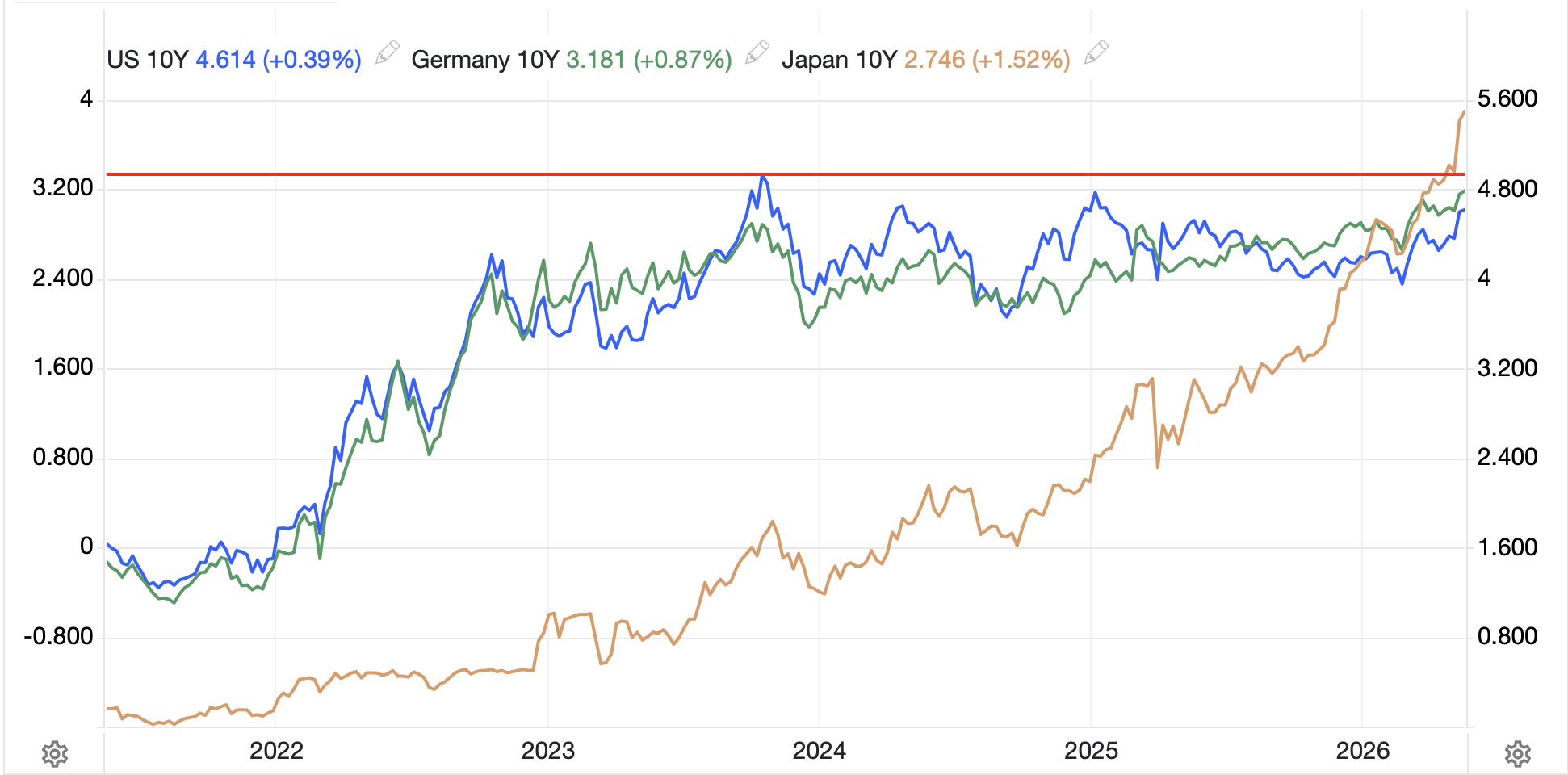

Now, if we look at the below chart from tradingeconomics.com, it shows 10-year yields over the past 5 years. You can see that US yields have not yet reached their October 2023 highs (driven then by the combination of strong economic growth and ongoing QT as inflation remained high from its Covid induced rise), but both Germany (green line) and Japan (brown line) are at their highest levels in quite a long time. We have discussed Japan numerous times over the past months, but not spent much time on Germany. However, the German story is one of stagflation. I have shown how poorly German economic output has grown over the past 5 years, as it has essentially stagnated over the entire timeframe. Now, add the self-inflicted energy policy insanity, that had already severely impacted Germany before the Iran conflict, and then the Iran conflict and $100/bbl oil prices, and the Germans have even more problems.

Here in the States, the recent inflation data has been consistently higher, and higher than expected and the great white hope of AI-induced deflation seems to always be a little further away than hoped/expected. It remains difficult for me to see a scenario where prices fall dramatically in the US anytime soon as there is too much economic stimulus to allow for a recession, let alone a depression, which is what I think would be needed to get prices to fall. In this world, yields will continue to creep higher, at least until such time as Iran is no longer an issue. One other thing to remember is that there is a massive short position in bond futures, upwards of $1 trillion across all maturities, although that is entirely driven by hedge funds in the basis trade, where they are long cash bonds and short futures as an interest rate hedge. But that only works as long as the math works (funding costs are less than the carry they earn). The point is, if short end rates start to rise such that funding is too expensive, we can see a massive unwind of that position, which would mean huge sales of cash bonds, and that will really drive yields higher. However, if that were to start to play out, even Mr Warsh, he of the shrinking balance sheet idea, will be out there buying bonds to prevent a collapse.

Ok, I’ve gone on too long, so a really quick tour of the markets overnight follows. Friday’s US equity selloff was followed by weakness across the board in Asia (Japan -1.0%, HK -1.1%, China -0.5%, Taiwan -0.7%, Australia -1.5%) although somehow Korea (+0.3%) managed to hold in there ok. In Europe, while the UK and Germany are essentially unchanged this morning, both France (-1.0%) and Spain (-0.7%) are under pressure, following the trend. US futures, at this hour (7:30) are also lower across the board, on the order of -0.6% or so.

Of course, underpinning all of this is oil (+1.2%) which continues to climb slowly higher as fears over an escalation in Iran have removed hope for a resolution. Oil is higher by nearly 9% in the past week and 22% since this time last month. In the metals markets, gold and silver, which both fell sharply on Friday into what appears to have been some major option expiration liquidation, are little changed this morning although copper (-0.8%) is still sliding from its highs amid overall market concerns about risk.

Finally, the dollar, which had a very strong week last week, is ever so slightly softer this morning, -0.1% on the DXY although there are two currencies with more substantive moves, NOK (+0.5%) on the back of the oil rally, and COP (+1.1%) which seems odd given copper’s performance today, but remember, copper is still within spitting distance of its all-time highs set last week and higher by 35% in the past year.

On the data front, it is extremely quiet this week with only a handful of meaningful numbers, although all eyes will be on NVDA’s earnings Wednesday after the close.

| Wednesday | FOMC Minutes | |

| Thursday | Initial Claims | 210K |

| Continuing Claims | 1790K | |

| Housing Starts | 1.41M | |

| Building Permits | 1.40M | |

| Philly Fed | 186 | |

| Flash Manufacturing PMI | 54.0 | |

| Flash Services PMI | 51.0 | |

| Friday | Michigan Sentiment | 48.2 |

| Leading Indicators | -0.3% |

Source: tradingeconomics.com

We also get 7 Fed speeches, although only four speakers in total. And remember, too, next weekend is the holiday weekend, so as summer approaches, trading desks will start to thin out.

My take is all eyes will be on the bond market for now, which will obviously be driven by oil prices, but also by the huge basis trade. As to the dollar, I see no reason to sell it with any force, that’s for sure.

Good luck

Adf