So, prices were all Hot, Hot, Hot

Resulting from Trump’s Iran shot

But do not forget

The government’s debt

And spending, with what that has wrought

Meanwhile, Trump, to Beijing, has flown

As both sides seek a temperate zone

Where it is agreed

To what both sides need

And neither, the outcome, bemoan

For a change, Iran is not the lead story today in markets. Instead, there is much angst over yesterday’s CPI reading, which was hotter than forecast, and much pontificating as to what will come from the summit between Presidents Trump and Xi that starts tonight in Beijing. Let’s take inflation first.

The results showed the month-on-month readings for headline (0.6%) and core (0.4%) which translated into annual readings of 3.8% and 2.8% respectively. I always turn to The Inflation Guy™, Mike Ashton, when trying to understand CPI readings and have linked here his description of the report and things driving it, which you should all read. However, I will offer his conclusion here:

“Wrapping this up, the read is actually pretty easy. Inflation is not just in energy, but right now is fairly wide as the diffusion index shows. Some of that is related to energy…the price of diesel fuel affects trucking costs, which affects other goods prices…and some of it is related to the fact that wage growth is no longer slowing. Any way you look at it, as I said the read is pretty easy: the Fed obviously isn’t going to be tightening into an oil shock. But there is nothing here that gives them cover to ease into an oil shock either. Warsh inherits a pickle.”

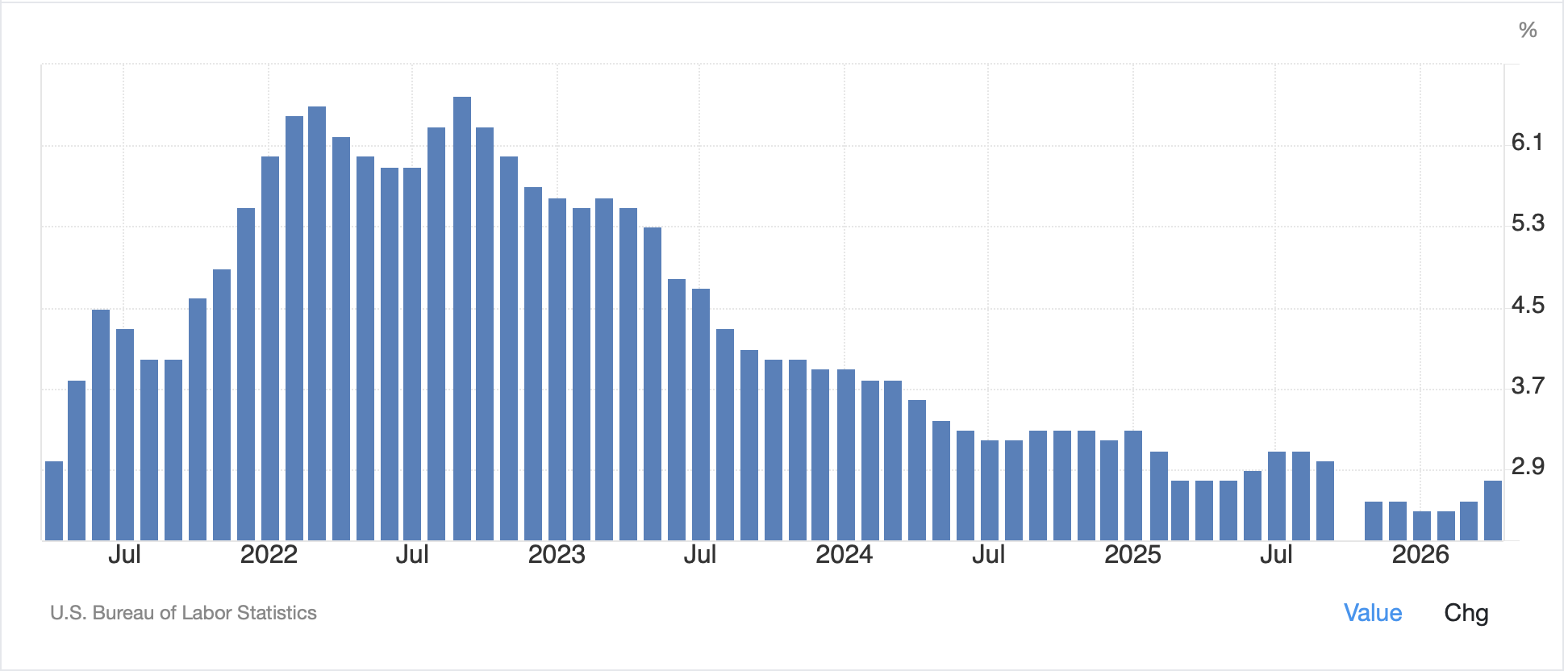

I know the Fed targets Core PCE, not Core CPI, but I include the below chart of the latter to remind us all of just how far from their target the Fed has been for the past 5+ years. Powell may have bitched about political pressure, but he received none during the Biden administration and he failed dismally then too. Just sayin’.

Source: tradingeconomics.com

(One last thing I will note is that USDi, which I mentioned yesterday, will return 10.2% annualized during the month of June, on top of this month’s 12.6% return. Folks, you really should own some. You can mint it at www.usdicoin.com ).

We cannot be surprised that yields rose yesterday on the back of the CPI result with the 10-year rising a further 3bps right after the number and 4bps on the day. This takes us to a 10bp rise in the past three sessions including this morning as per the below.

Source: tradingeconomics.com

It also is the highest yield since last summer and clearly is not moving in the direction the administration would like to see. The thing is, now that we are several months into the Iran war and oil prices have been elevated since the beginning of March, we are going to see more pass through of price increases due to energy costs, at least until demand starts being destroyed. That is always the market tension, rising prices force behavioral adjustment unless the central bank accommodates those prices by increasing money supply. It is, of course, that action which helps drive generalized inflation as opposed to specific price increases. Mr Warsh, who was confirmed as a Fed governor by the Senate yesterday and faces another vote today to become Fed Chair, although I expect that will be without fireworks either, will have has work cut out for him.

Moving on to the Beijing summit, the key to remember is that summits are where things are signed amid a ceremony, they are not events to negotiate details. Secretary Bessent has been in Asia all week and he has met with Chinese Premier Le Hifeng, clearly discussing terms of what can be agreed. One would expect that the focus will be on Iran and having China press Iran to come to an agreement, trade between the nations, especially in AI related technology and rare earth elements, and Taiwan. I have no way of knowing what will be announced, but I’m confident Mr Trump wouldn’t be going if there wasn’t a deal of some sort already agreed.

So, let’s see how markets have behaved overnight. Yesterday’s US session, which started out looking pretty awful, moderated throughout the day to wind up with fairly benign outcomes. Weirdly, this led to some dramatic differences in Asia with some strong gainers (Korea +2.6%, Japan +0.85%, China +1.0%, Singapore +1.2%) and some serious laggards (Indonesia -2.0%, Taiwan -1.25%) with some lesser weakness (Australia, New Zealand, Malaysia and HK). I might argue that most investors were excited about the potential results of the summit, but if so, perhaps it implies a change in the US position regarding Taiwan, and that could well be a negative there.

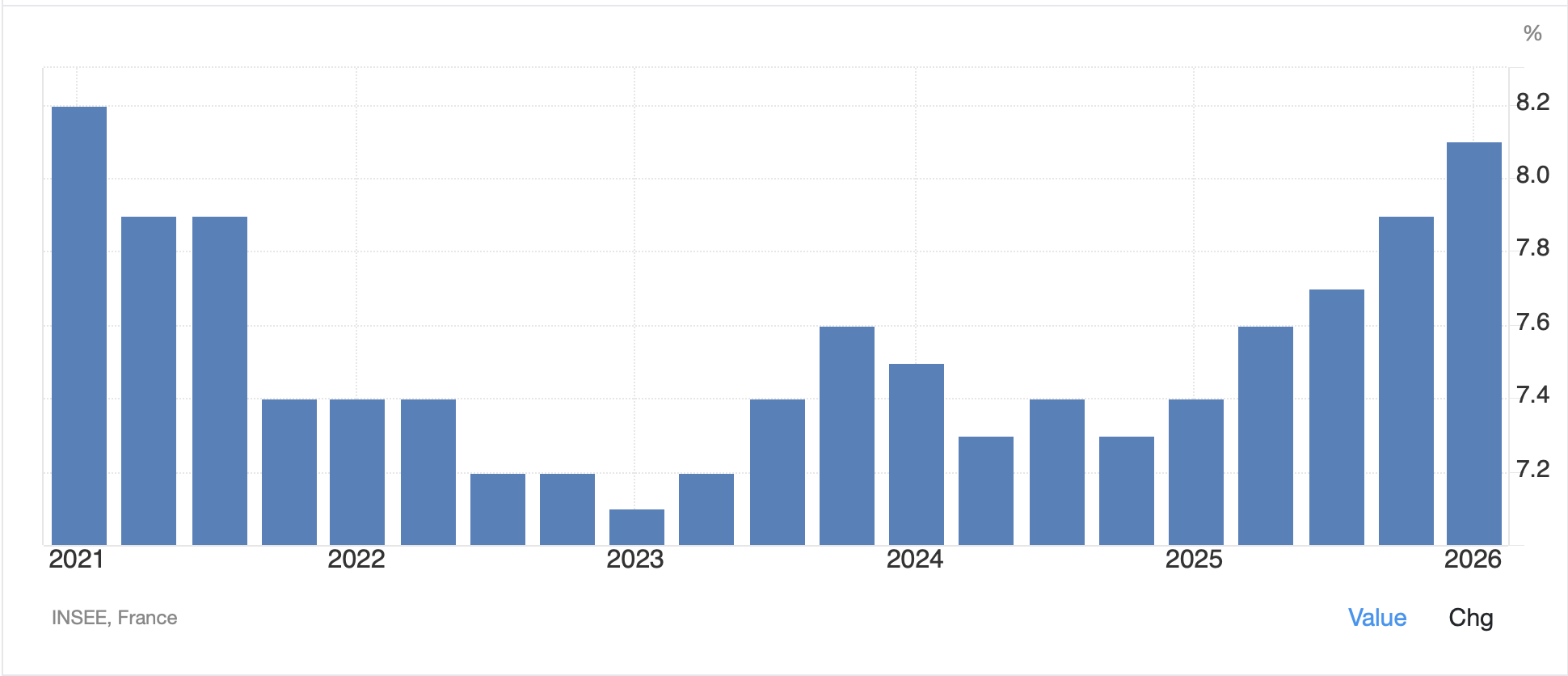

In Europe, the picture is also mixed as Germany (+0.7%) is having a solid session on some solid earnings reports from the pharma sector, although France (-0.4%) is under pressure after the Unemployment Rate there jumped to 8.1%, its highest print in five years.

Source: tradingeconomics.com

Otherwise, the rest of Europe is mixed with little of note. US futures at this hour (7:30) are also mixed with DJIA (-0.25%) lagging but the other two major indices showing gains of 0.25%.

While we discussed Treasuries above, looking elsewhere around the world, yields this morning in Europe are essentially unchanged, having risen on the back of the US CPI report yesterday. However, overnight, JGBs saw yields rise 4bps on that inflation fear, and they have made yet another new 19-year high as per the below chart (dates are in European terms).

In the commodity markets this morning, oil is essentially unchanged as it is clear nobody knows how things will play out in Iran. There have been numerous commentators competing to describe just how much oil has been missing from the market and how soon (June? July? September?) the infrastructure will crash and it will be a global depression. But they keep having to push their timeline further out as the combination of more production outside the gulf plus the ingenuity of getting production there to other markets via trucks and trains, has mitigated the overall price risk. Again, here in the US, there is no risk of a shortage of any type as we continue to export our net surplus of products. I have not read about the blockade lately, but I think that speaks to the fact it must be effective because most articles wanted to describe it as a failure and not doing its job. If Iranian oil is not getting to market, their financial troubles are growing apace which is the key pressure point.

As to the metals markets, given the lack of movement in oil, it should be no surprise that gold (-0.25%) is little changed as well. However, something is changing here and that is silver (+1.0%) and copper (+2.0%) are both starting to distance themselves from the gold trade as both remain critical inputs into the electrification story. A quick look at the chart below of the two elements shows how just in the past two days, silver has broken away from gold.

Source: tradingeconomics.com

Finally, the dollar is firmer again today, continuing to ignore the many calls for its demise. But as we have seen in most other markets today, the magnitude of the movement is unimpressive. So, DXY (+0.2%) is an excellent proxy for virtually the entire FX market this morning.

On the data front, today brings PPI (exp 0.5% M/M, 4.9% Y/Y) and core (0.3% M/m, 4.3% Y/Y) although with CPI already released, I doubt it will get much interest. We also get the EIA oil inventory data which is looking for continued draws of roughly 6 million barrels across crude and products. there are Fed speakers too, but when was the last time anyone listened to anything they had to say with interest? Exactly.

It is shaping up to be a quiet session (famous last words) and I suspect all the news of note will come from Beijing tonight.

Good luck

adf