The doom mongers are up in arms

As though they raise many alarms

Investors don’t care

And add risk with flair

Ignoring the much-mooted harms

So, war is no longer concerning

And though hyperscalers are burning

Through all of their cash

Amid much backlash

Investors, their shares, are still yearning

And what about data and growth?

Investors care naught about both

Concerns about yen?

Not that trope again!

To stocks most investors are troth

As I read through my X feeds in the morning, as well as the WSJ and Bloomberg, the overriding theme appears to be the end is nigh. Whether discussing Iran and the oil price and the future of the Strait of Hormuz, AI and the bubble or the potential for massive job losses and the creation of Skynet, the economic data and the incipient recession coming because people cannot afford to continue their consumption habits, or the idea that we are on the precipice of a Treasury bond market collapse because the Japanese yen is weak, the dominant theme is disaster is around the corner. It is really tiresome, I have to say.

Now, you might say that I simply follow the wrong people, and that may be true, but my feed hasn’t changed, and I never look at the algorithm’s selections for me, I only look at my followings. So, I cannot tell if people have become that much more bearish on the overall situation, or if they simply write these things because they believe they will get more engagement. I fear it is the latter, but that simply devalues anything useful they may have to say. Mostly, it’s frustrating to try to get an unbiased sense of what is happening in the world these days. After all, while I understand that governments put out propaganda constantly, I thought the idea behind X and Substack was you could avoid that. I think I am going to go back to reading books!

So, as we await this morning’s payroll report, I’ll try to touch on the key issues I believe matter. Starting with the yen, which continues to garner attention, or more accurately, the joint intervention garners attention, I first have to laugh at the following Bloomberg headline, “Yen Surrenders Nearly Half Its Gains From US-Japan Intervention”. This was written by Mia Glass, and I don’t know anything about her except her grasp of arithmetic is tenuous. Here is the chart of USDJPY and while the yen has been weakening steadily since the intervention last week, half? Even taking the spike low into account, we are nowhere near a 50% retracement and on a closing basis, it is a ridiculous claim.

Source: tradingeconomics.com

There continues to be much fodder made about Secretary Bessent trying to prevent a meltdown in the Treasury market but Occam’s Razor tells me that it is far more likely that a too-weak yen is bad for Japan because of its inflationary impact and the US because it impedes US exports so joint intervention made sense. And as I have maintained all along, unless underlying fiscal and monetary policies change, the yen is going to continue to weaken.

Turning to Hormuz, the press continues to write with glee about President Trump’s miscalculation and the US losing the war and whether Iran and Oman are going to come to some agreement on the Strait, but oil prices, while they rallied a bit yesterday, are lower this morning by -0.6% and -9.25% in the past week. Looking at the chart below, despite all the discussion of inventory depletion, which are real, but obviously not as important to the price as many previously believed, the trend remains downward and we are well below the trend. Frankly, at $75/bbl, it appears the world works fairly well.

Source: tradingeconomics.com

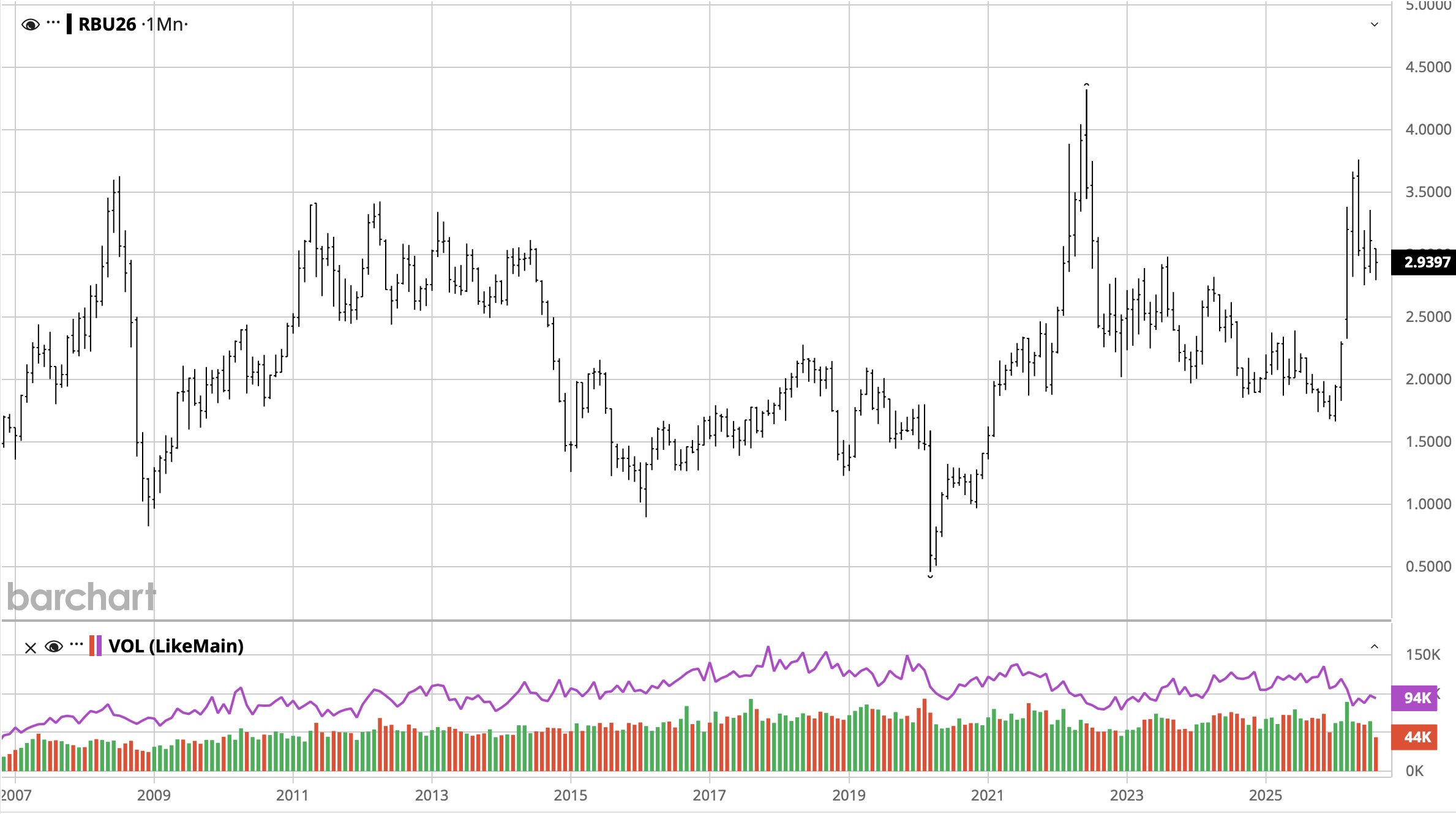

Look, I would rather pay less for my diesel, and I know you would all like to pay less for your gasoline, but here’s a 20-year history of the RBOB (NYMEX gasoline) contract. We are hardly in unprecedented territory having spent a lot of time around here from 2011 through 2015 as well as the beginning of the Russia/Ukraine war.

I have no idea how things will end up in Iran, nor does any other commentator. I know I am happier if Iran does not have a nuclear weapon and ballistic missiles that can reach Europe, let alone the US. But I would say the market has almost lost interest in the war.

As to the hyperscalers and the AI bubble, in truth, it seems much of the animosity has been turned toward SpaceX as everyone loves to hate Elon almost as much as they love to hate Trump. But it appears by many metrics that equity markets continue to benefit across the board from strong earnings results, with ~85% of companies (depending on your source) beating estimates which is well above the average of 77%. So, the economy continues to grow pretty strongly, and companies continue to make money, and investors continue to want to buy shares. The hyperscalers aren’t leading the pack anymore, but they have not collapsed either. There are many who continue to explain this cannot go on forever and there will be a reckoning, and they may well be correct, but in this case, being early and being wrong are the same thing.

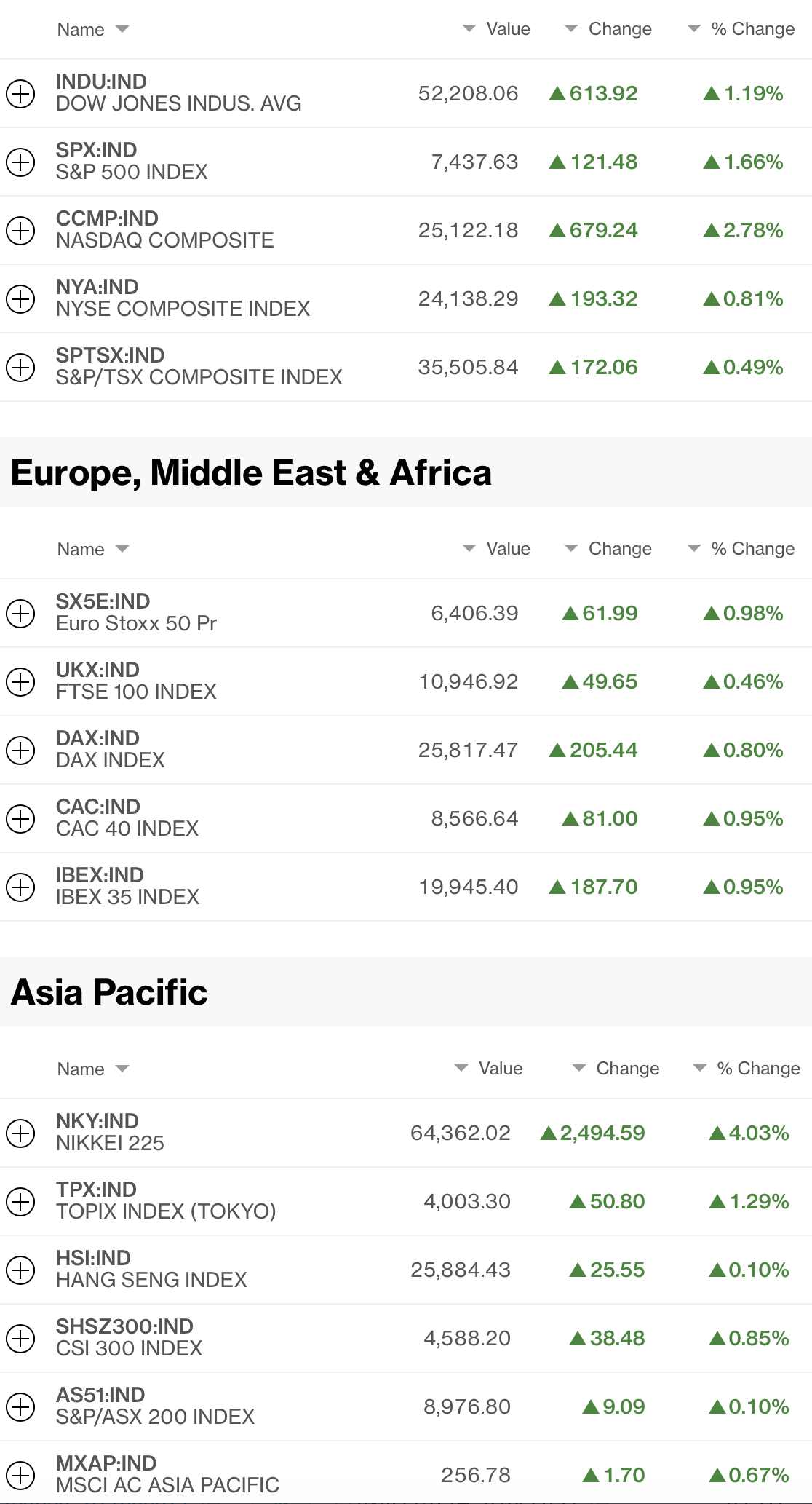

Ok, enough of that. Let’s see if anything noteworthy has happened overnight. The truth is, not especially. Asian shares were mixed with Chinese shares doing well after solid trade data, but the rest of the region drifted lower. European shares are firmer across the board after broadly positive data (German IP and Trade, French Trade) although the French Unemployment Rate ticked higher to 8.3%. And US futures are higher this morning as well ahead of the NFP report. Despite the doom and gloom, equity markets are doing fine.

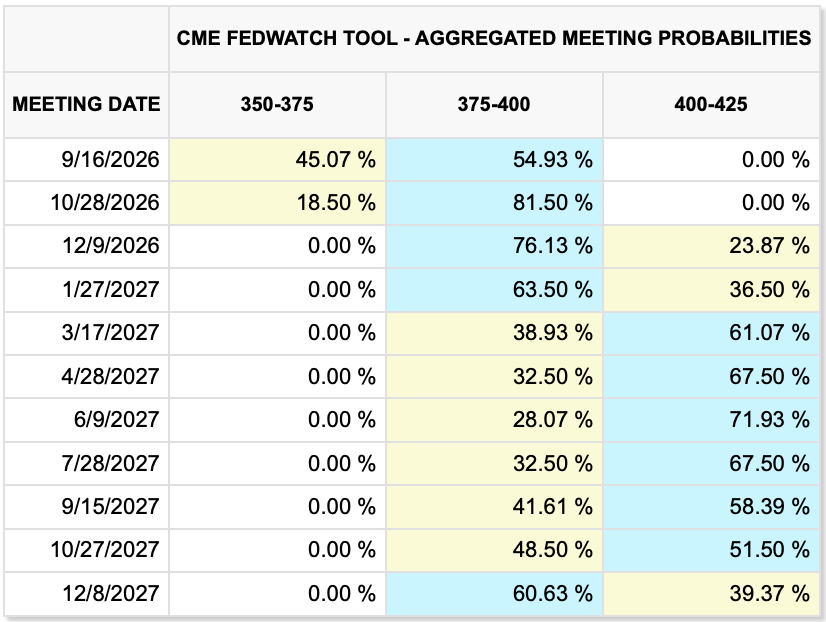

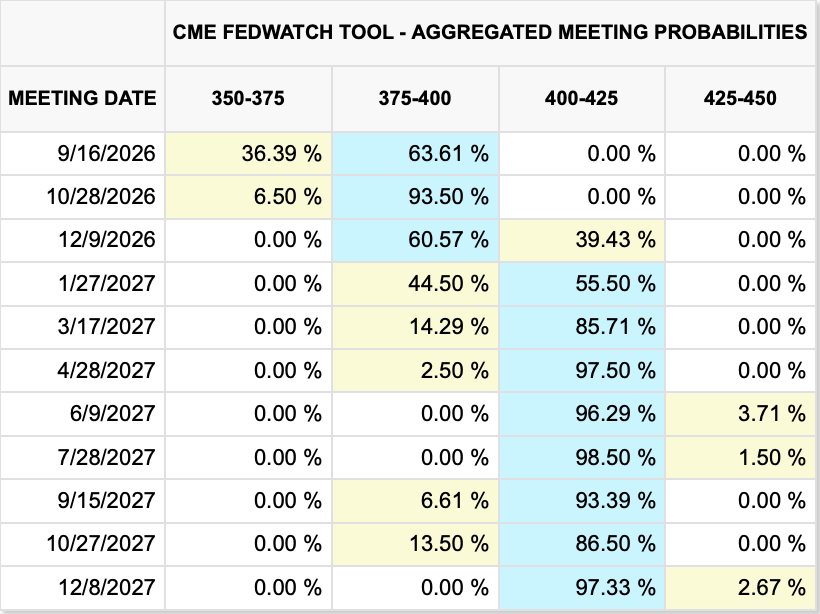

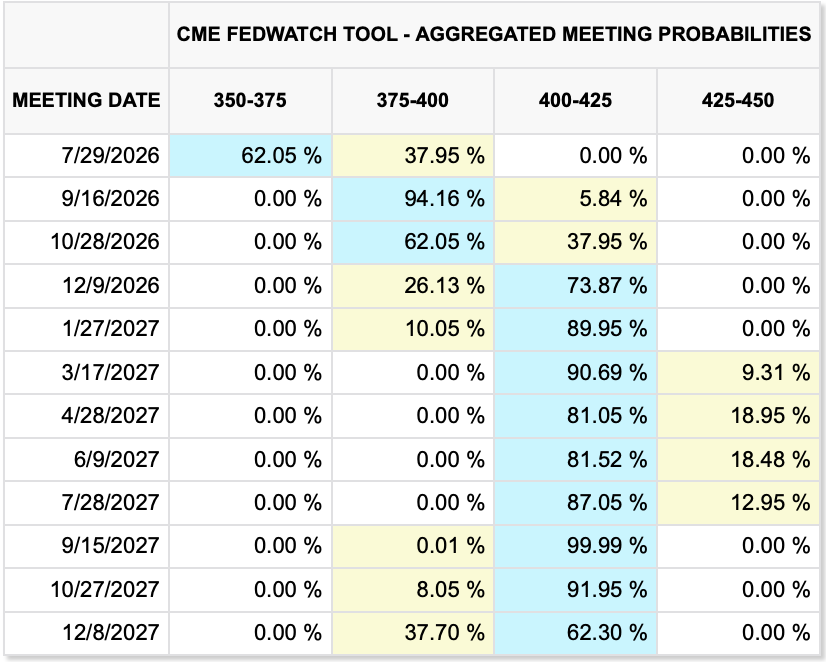

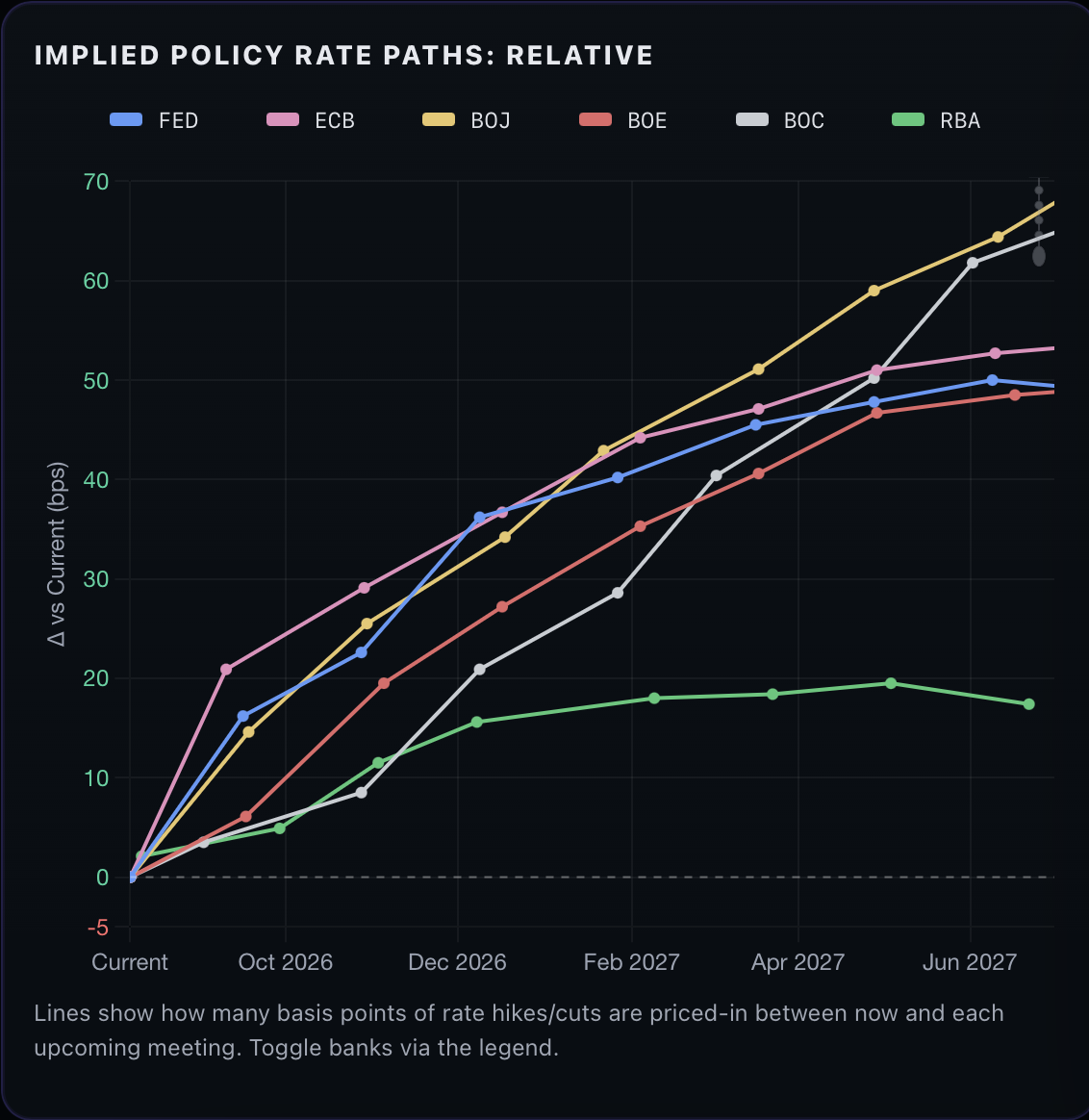

Bond markets have barely moved overnight, although we did see Treasury yields back up 5bps yesterday. That appears to have been on the back of the oil price rise, although as I look at probabilities of central bank rate hikes, there is a growing belief that the Fed, ECB and BOJ are all going to raise rates next month as hiking rates into an energy shock seems to be their MO.

Source: rateprobability.com

We discussed oil but gold (+2.0%) and silver (+4.1%) are the real story in commodities as both are extending their recent rallies from the consolidation lows. For instance, silver is higher by 11% this week and $9/oz since July 17th.

Source: tradingeconomics.com

Finally, the dollar, despite all the anxiety about the yen, remains quiet overall. The DXY is below 100, back in its range and showing no inclination to move in either direction. This morning ZAR (+0.7%) is the king of the hill on the rally in gold while MXN (+0.3%) is a touch higher after Banxico left rates on hold. But remember, peso rates are still high and economic growth continues apace so investment opportunities abound. The peso has strengthened more than 17% since the beginning of 2025, shaking off any tariff concerns easily.

Source: tradingeconomics.com

As to the data, here are consensus forecasts:

| Nonfarm Payrolls | 80K |

| Private Payrolls | 78K |

| Manufacturing Payrolls | 4K |

| Unemployment Rate | 4.2% |

| Average Hourly Earnings | 0.3% (3.5% Y/Y) |

| Average Weekly Hours | 34.3 |

| Participation Rate | 61.6% |

Source: tradingeconomics.com

We also see Canadian employment data (exp 6.5% Unemployment Rate) and hear from Thomas Barkin, the Richmond Fed president. But it is a summer Friday and typically, about an hour after the NFP release, traders are gone for the weekend so don’t expect too much today.

The world is not ending, the dollar is not collapsing, the Treasury market is not collapsing, and equity markets are not about to implode. My take is the big stories from the past months have lost their luster and I suspect after a lull, we are going to start to focus on the politics of the midterm elections in November. But until then, have a cold one and relax.

Good luck and good weekend

Adf