The weekend saw missiles in flight

As both sides continued the fight

But just ere the open

The market put hope in

The idea that peace was in sight

So, here we are first thing today

And focus has moved far away

We’re back to AI

And pie in the sky

As stocks, once again, make more hay

Much has been made of the fact that President Trump is hyper aware of financial markets and seeks to ensure that whatever is happening in the world, it happens on weekends so that by the time markets reopen, the situation appears far less dire, hence less need to sell stocks. This weekend is a perfect example as Friday after the close, it was announced that the US had responded to the several Iranian attacks on ships in the Strait of Hormuz last week with significant force. The early punditry on Friday night and Saturday was that when markets reopened, the recent decline in oil prices would reverse as that has been predicated on a more lasting peace. But then, last night shortly before futures markets opened, there were announcements that the US had finished its response and that the peace talks were back on under the guise of the 60-day ceasefire.

I have to say, though, it almost appears as if Iran is in on the joke. After all, if not, wouldn’t they try to force Trump’s hand during market hours? Just asking. Whatever the case, the situation as we wake up this morning is that oil (+0.8%) has edged back higher near $70/bbl but certainly doesn’t have the feel of breaking out higher. Meanwhile, equity markets are generally positive and have been overnight while bond yields and the dollar are little changed. in other words, there’s not much happening this morning.

In reality, it is not that surprising that things are quiet. It is summer and summer markets are typically somewhat less active. As well, away from the uncertainties of the Iran conflict, economic activity seems to be ticking along pretty well. Arguably, the biggest story remains AI and both its potential impact on workers and the economy as well as the questions about its ability to generate sufficient revenue to repay the hundreds of billions of dollars being spent on it. But those are longer-term stories, not day-to-day.

Which takes us to this morning. Frankly, I don’t think there is an interesting market related them right now. Instead, we have much time-biding until the next big thing.

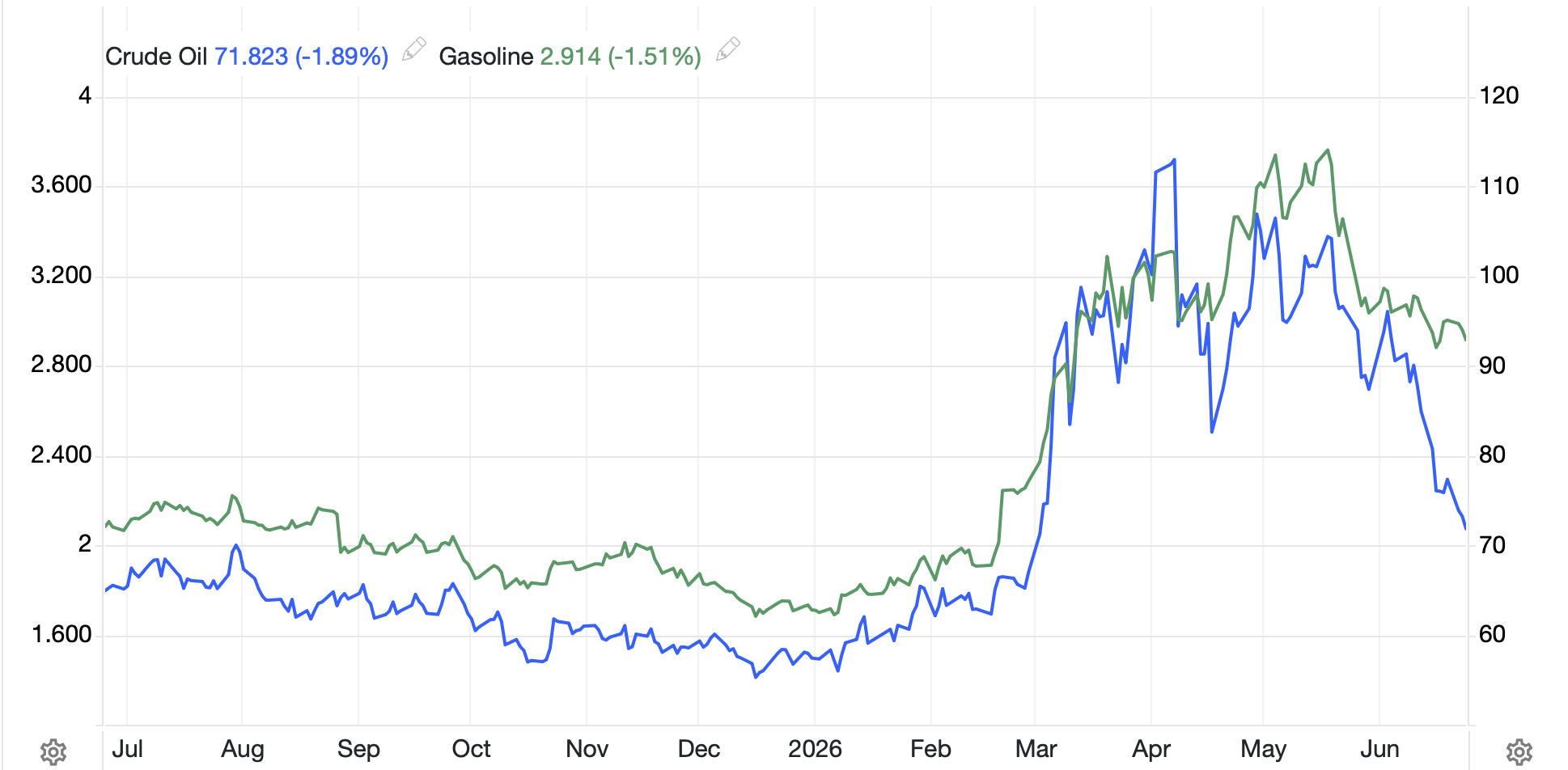

Let’s start with commodities as oil continues its multi-month decline from the early April peak. it remains very difficult to look at the below daily chart and think, damn, oil is about to run away higher. At least for me.

Source: tradingeconomics.com

There are still numerous analysts who maintain that the drawdown of reserves is going to come back and haunt the market, driving prices much higher as inventories fall and tank bottoms are reached. And I am sure they earnestly believe those outcomes are ordained. But the relative wisdom of market prices disagrees.

Remember back when this all started, there was another point that was made by these same analysts, that fertilizer shortages would be manifest and food prices would rise much higher. The story was that the closing of the Strait would reduce the ability of Qatar to produce and ship LNG and that was a critical input into the making of Urea. Let me show you the price chart for Urea.

Source: tradingeconomics.com

While it certainly rose initially, apparently there is sufficient urea around to continue with agriculture as we know it. Again, much of the initial fear seems to have been misplaced. I do not know if that is because analysts didn’t really understand the way these markets operated, or because they have models that they have used for years, and those models are no longer fit for purpose. My observation is that many analysts try to determine the price trends by looking at their understanding of both supply and demand of a given commodity. But I might argue that the price is what defines both supply and demand, and that at given prices, those two curves adjust to make the system work. Think of it as price is the independent variable, not supply/demand.

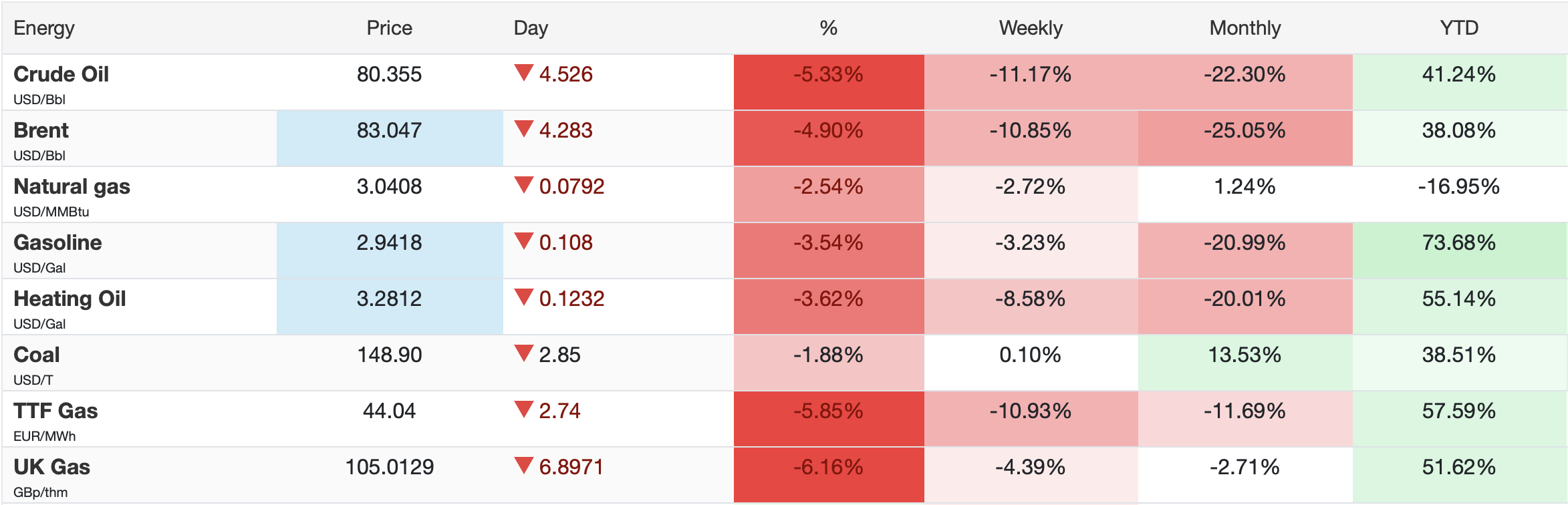

Moving on to the metals markets, they remain under pressure this morning with both gold (-1.3%) and silver (-1.9%) unable to find support, especially the latter. Copper (-0.3%) is holding up better and I continue to believe that all three will fare well over time, but not right now.

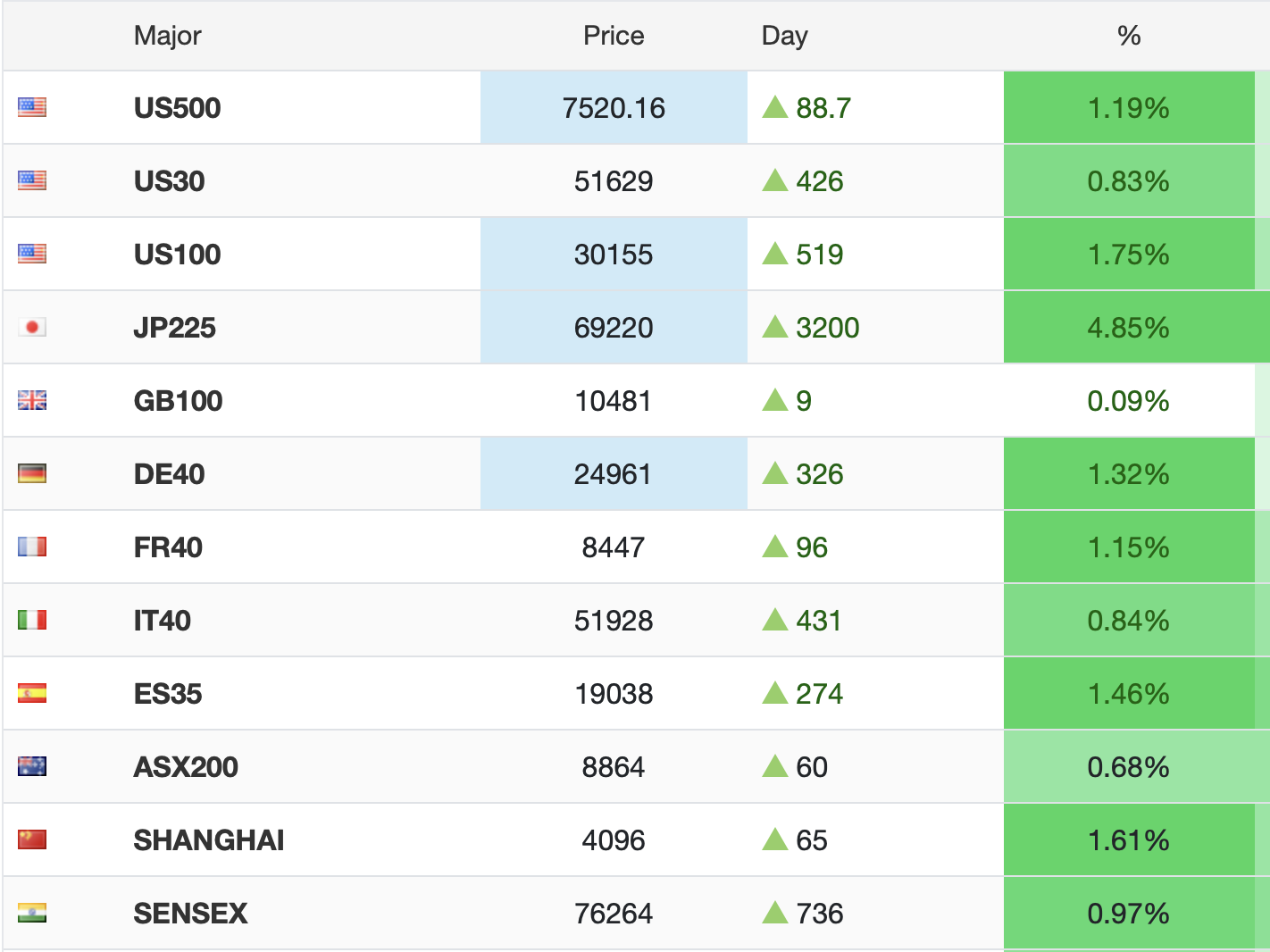

In the equity markets, Friday’s nondescript US markets were followed by more strength (Tokyo +0.15%, HK +1.6%, China +1.2%, Australia +0.7%, Taiwan +1.0%) than weakness (Korea -0.2%, India -0.5%, Indonesia -1.3%) in Asia. The big news overnight was the South Korean government supporting a massive semiconductor investment by the two big Korean firms, SK Hynix and Samsung, to build four more fabs. In Europe, though, things are less positive with Germany’s unchanged performance leading the way although the declines elsewhere (UK -0.2%, France -0.3%, Spain -0.4%) are hardly devastating. We ought not be surprised that US futures are higher this morning as I type (7:25) led by the NASDAQ (+0.9%) as the AI/semiconductor theme continues.

Bond markets continue to do very little with yields essentially unchanged on the day in Europe or the US. 10-year Treasury yields are currently 4.37%, well off the highs seem a month ago near 4.70% when there was much discussion about a breakout higher. But look at the below longer-term chart of the 10-year Treasury yield and tell me that anything substantive has happened in the past 3+ years. Since yields rise alongside the 2022 inflation surge, we have seen very little net movement.

Source: tradingeconomics.com

Finally, the dollar is a bit softer this morning but is clearly not the focus today. I continue to read analyses about Chairman Warsh and what he is going to do and why he will not be able to achieve his goals. The implication is that either he will need to be ultra hawkish, raise rates quickly and the dollar will soar, or he will wind up with QE 5 or 6 or whatever number we are on, and the dollar will collapse. My personal view is neither of those scenarios will play out. As I wrote in the wake of his first meeting, I expect inflation data will ease along with the recent decline in energy prices, and he will be able to do nothing without consequences as he works to change the way things work there. In the meantime, the dollar will remain supported by real investment flows.

On the data front, even though it is a holiday-shortened week with markets closed Friday for July 4th, we get a lot of data.

| Tuesday | Case-Shiller Home Prices | 0.8% |

| Chicago PMI | 60.0 | |

| JOLTS Job Openings | 7.28M | |

| Consumer Confidence | 94.2 | |

| Wednesday | ADP Employment | 113K |

| ISM Manufacturing | 54.0 | |

| ISM Prices Paid | 79.0 | |

| Thursday | Nonfarm Payrolls | 110K |

| Private Payrolls | 115K | |

| Manufacturing Payrolls | 3K | |

| Unemployment Rate | 4.3% | |

| Average Hourly Earnings | 0.3% (3.5% Y/Y) | |

| Average Weekly Hours | 34.3 | |

| Participation Rate | 61.7% | |

| Initial Claims | 220K | |

| Continuing Claims | 1825K | |

| Factory Orders | -2.1% | |

| -ex Transport | 0.4% |

Source: tradingeconomics.com

Obviously, all eyes will be on the payroll data on Thursday. But Chairman Warsh will be at Europe’s version of Jackson Hole, in Sintra Portugal and speaking at 9am Wednesday morning. It will certainly be interesting to hear what he has to say there.

It doesn’t seem like there is much about which to get excited today, or tomorrow frankly. So, Warsh and then NFP will be this week’s story absent another major flareup in the gulf.

Good luck

Adf