Iran has implied they will skip

The coming Islamabad trip

But if they don’t show

The risks of war grow

For them it’s high stakes gamesmanship

Meanwhile markets blithely ignore

The likely resumption of war

But can it be true

That conflict, part two

Will open the next rally’s door?

Ostensibly, a second round of peace talks are due to get underway today in Islamabad, Pakistan, but whether they will remains an open question, at least as of right now at 6:20am in NY. As always, it is difficult to know what comments are true or were even made by the players involved as propaganda remains Iran’s largest current export. I have seen comments allegedly from Iranian sources that claim they both will not attend, and that they will attend. I guess we will know before the day ends as none of the negotiators is named Schrödinger.

As well, President Trump has indicated he is uninterested in extending the cease-fire even one more day if they do not attend. At this point, it appears that the hardest line members of the IRGC that have survived are the ones in charge over there, and my take is they are not very interested in negotiating as any result would likely end their grip on power. After all, if they are prevented from having nuclear weapons capability to destroy their sworn enemies of Israel and the US, what exactly is their raison d’etre?

Thus, my fear is that fairly soon, the second stage of this conflict is going to ignite. If this is the case, the recent market insouciance over the situation seems likely to change dramatically, at least for a little while. This implies that oil prices will spike higher again along with the dollar, while equities and gold will slump. I assume bond yields, too, will rise somewhat. Looking at a chart of yields, though, the current level is right in line with where they were for much of 2025 and at the beginning of 2026, and I am left to wonder if the move lower in yields in January and February, was the anomaly, not the return to current levels.

Source: tradingeconomics.com

I remain suspect of the thesis that inflation is going to decline dramatically because of AI implementation and have felt that way since far before the war began. Over a long period of time, as AI utilization increases, I do believe it will improve productivity significantly (I see what it has done for me with just limited uses, none of which involve the wordsmithing this note!), but it is difficult for me to foresee a significant deflationary impulse absent a significant reduction of money in the system, and I don’t see that on the horizon any time soon. The point is, yields don’t seem to be wrong overall in my eyes.

Now, Kevin’s about to sit down

In front of each Senate assclown

They’ll ask him ‘bout rates

But whate’er he states

The Dems will vote no with a frown

The other noteworthy story is that Fed Chair nominee, Kevin Warsh, is having his hearings at the Senate Finance Committee today. There is a great deal of discussion in the press regarding whether he will simply be a Trump puppet, or become a Trump whisperer, or be an independent voice. As well, there has been a recent conversion from Fed chair worship amongst the mainstream media, to encouragement for FOMC dissent to anything he wants to do, simply because he was appointed by Trump, so they seek his failure. It is really quite tiresome. Frankly, whatever he says is likely to be irrelevant as we already know that every Senate democrat will vote against because…Trump, and most Senate republicans will vote for and when it comes to the floor, he will be confirmed.

That said, it is a tough job to take right now, regardless of the president, given the goals he has stated, the current situation with respect to the Fed’s monetary stance, and the potential for dramatic changes in economic outcomes because of the war. I know I wouldn’t want the job!

Ok, let’s analyze that insouciance from overnight. While yesterday started off with a negative tone, by the end of the day, US equity markets were little changed with the NASDAQ and S&P slipping just -0.25% while the DJIA was unchanged. Futures this morning are pointing higher by 0.5% at 7:20am. Overnight, Asian markets were mostly higher, some by a significant amount (Korea +2.7%, Taiwan +1.75%) which continues to baffle me given the impending energy crisis that is about to hit the region. The larger markets were also firmer (Tokyo +0.9%, HK +0.5%, China +0.2%) with the rest of the region +/- 0.3% or so. Fear is not evident here.

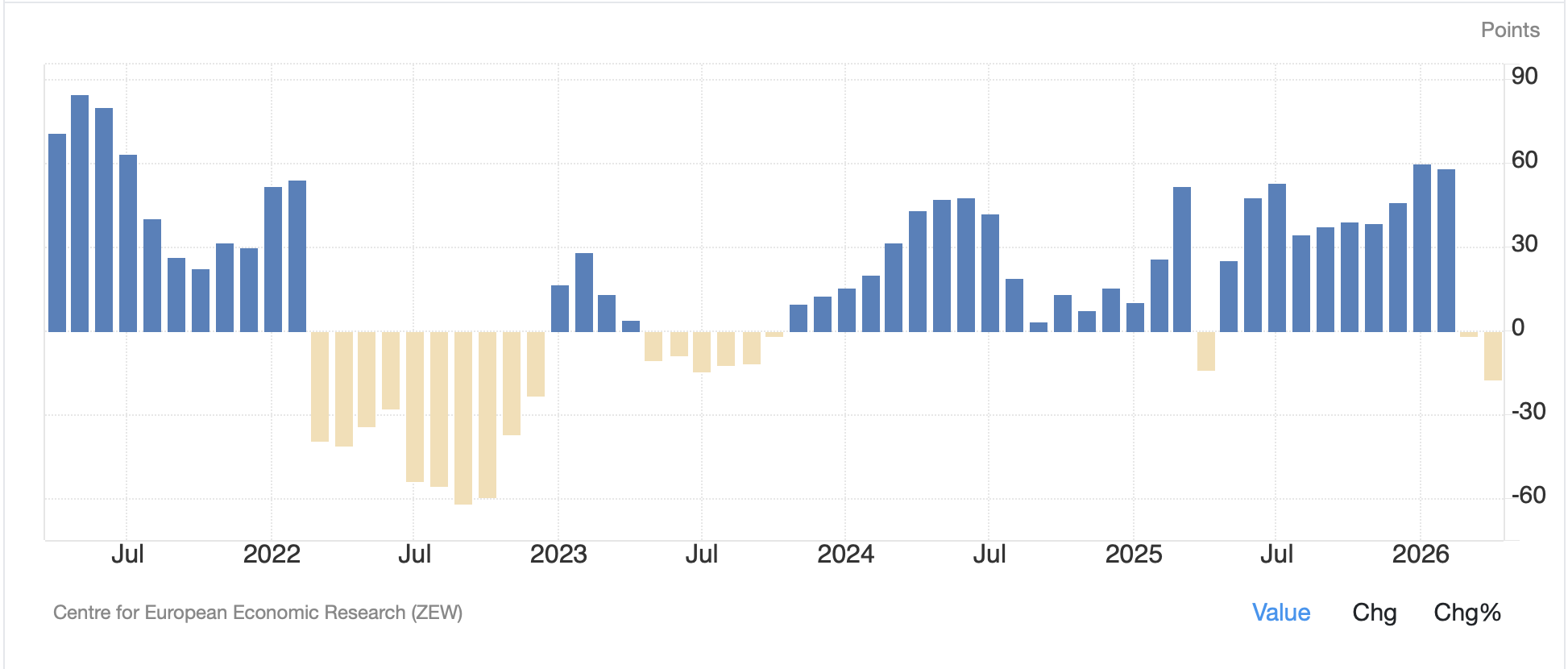

As to Europe, there is also no fear with Germany (+0.7%) leading the way higher despite the worst ZEW Expectations result since December 2022.

Source: tradingeconomics.com

But Spain (+0.6%), France (+0.3%) and the UK (+0.15%) are also higher this morning. Fear is not an option.

In the bond market, yields this morning are basically unchanged across the board and nobody is paying attention to this market right now. The only remotely interesting news is that Nikkei News reported the BOJ is not going to raise rates at their meeting next week, and they apparently have a 100% accurate track record in this situation. Nobody cares about this right now.

Oil (-0.2%) is hanging around awaiting the next story from the Persian Gulf and Strait of Hormuz, sitting between the level seen when it was declared the Strait was reopened and the level it touched when that was denied. As you can see from the chart below, not only has oil been hanging around, but trading volumes (the light grey bars below the price chart) also appear to be sinking. Everybody is holding their breath for the next thing here.

Source: finance.yahoo.com

Meanwhile, metals are under some pressure this morning (Au -0.7%, Ag -0.9%, Pt -0.2%, Cu 0.0%) but volumes here are also muted. It’s not just the oil market waiting for the next steps, that’s for sure.

Finally, the dollar is a bit firmer this morning, with DXY (+0.1%) pretty representative of the entire space. One outlier is NZD (+0.3%) after inflation data released last night was higher than expected and market participants started pricing in another rate hike there. But otherwise, this market is also bored and boring. There was a Bloomberg article this morning explaining that hedge funds are starting to layer in bets on a rising euro given how low implied volatility is in the options market, but the very fact that implied volatility is so low, around 6%, tells me that nobody really cares.

On the data front, Retail Sales (exp 1.4%, 1.4% ex-autos, 0.2% control group) is due. The big jump is because the data measured is nominal terms, so the dramatic jump in gasoline prices will have raised Retail Sales a lot, hence the focus on the control group that doesn’t include gas.

And that’s really it. The Warsh hearings will get headlines right up until something happens in either Pakistan from the talks, or Iran because there were no talks. There are many known unknowns right now, and that explains the lack of trading volume. But real price movement in every market will rely on unknown unknowns, which by definition are opaque, at best. Once again, my advice remains, play things close to the vest.

Good luck

Adf