For weeks it appeared that the war

Was something we all could ignore

As equities rallied

And most people tallied

Their gains as those prices did soar

But yesterday, things took a turn

And suddenly, stocks, folks, did spurn

While oil went higher

As missiles did fire

And UAE oil did burn

The question today is what’s next?

Will Hormuz soon wind up annexed?

Or will Iran’s forces

Back up their discourses

And keep Mr Trump greatly vexed?

For nearly two weeks, it appeared that the market was completely willing to accept the narrative that the Iranians were on their last legs and that the Strait would be reopened soon, thus relieving the pressure on the oil markets, and global markets in general. After all, US equity markets, as well as those in Korea and Taiwan, were making new all-time highs regularly despite the ongoing stress in Iran.

But yesterday, those happy thoughts were called into question as evidenced by the equity markets’ collective sharp decline throughout Europe and the US. Of course, most of Asia was closed on Monday, but the few markets that were open performed well then. Alas, last night was a different story with more losers (HK, India, Australia, New Zealan, Singapore) than gainers (Malaysia, Indonesia). Even if markets don’t decline much further, there has been a distinct change in sentiment about things, at least in my view.

The timing of the progress in potential negotiations and the question of potential escalation of fighting again are suddenly weighing more heavily on investor perceptions than they had for the last several weeks.

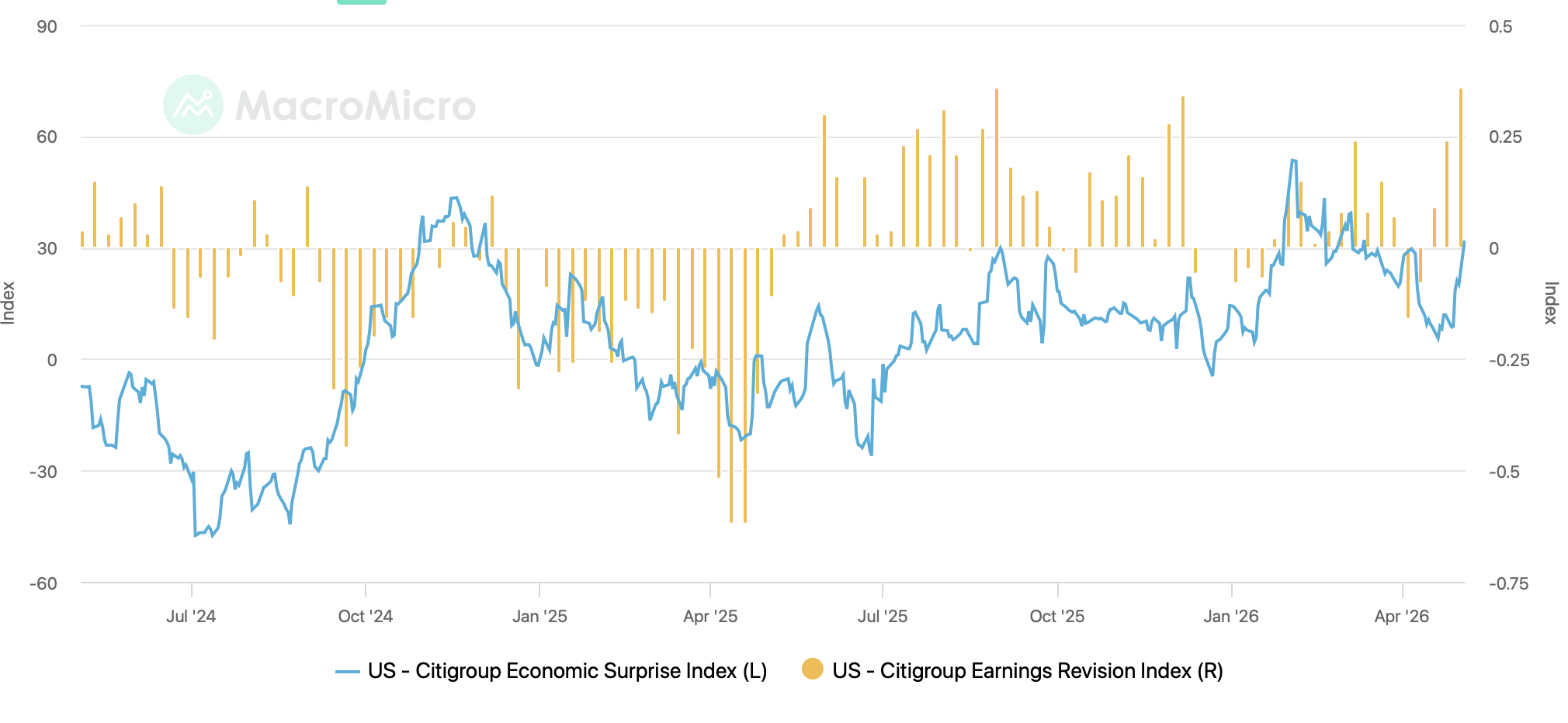

In the meantime, if we turn our attention to economic data, yesterday’s Factory Orders came in much stronger than expected, just the latest in a line of “surprisingly” strong data points from the US. If we look at the chart below from macromicro.me, showing the Citi Surprise Index and their earnings index, we can see that both the economic indicators and US corporate earnings results are moving higher. This seems at odds with the narrative of imminent collapse that is still making the rounds but is likely the cause of the equity market’s resilience.

In fact, this morning, markets are once again pointing in a more favorable direction as yesterday’s skirmishes in the Gulf have been quickly forgotten, it seems, and European bourses are all higher (Germany +1.0%, France + 0.6%, Spain +1.1%) recouping yesterday’s losses although UK equities (-1.0%) are suffering on a combination of yesterday’s concerns as well as a surprisingly negative HSBC earnings report. And US futures are also higher at this hour (5:45) by about 0.4% across the board. It is difficult to get markets downbeat for very long these days, which is remarkable given the sentiment indicators which have consistently been reading quite poorly.

This dichotomy is quite interesting to me as I am currently reading “Narrative Economics” by Robert Shiller, where he describes how social narratives have, throughout history, led to economic outcomes, whether positive or negative. His implication is that the data tends to follow the current zeitgeist, and then almost regardless of any government efforts to change that narrative, the zeitgeist is what drives the economy. For those of us who have been observing markets for any extended length of time, I don’t think this is a surprising revelation, although Shiller does a great job highlighting all the different times the narrative drove the bus.

And that is what makes the current situation so remarkable, the narrative is that things are terrible with the nation dramatically split politically while gasoline prices have risen so much and inflation is a major problem. You can see that in the Michigan Sentiment Survey and the political polls. Yet Retail Sales remain firm and we just saw those strong Factory Orders, two things which one would expect to soften given the current narrative.

Perhaps what we have seen is the impact of social media and ‘influencers’ whose goal is to show the good life and why/how you should live it. Given they only maintain their followers if they show an ideal situation, there will be no shaming for ostentatious consumption, that is their stock in trade. So, while during the Great Depression, social pressures were such that buying anything new, like cars or houses, was seen as inappropriate, today, buying new cars is seen as a requirement, the more expensive the better. Or going on an expensive holiday, or some other extravagance. I wonder if the gloomy narrative will end up overcoming the influencers. I suppose much will depend on just how much longer the war in Iran continues, as a clear end soon would almost certainly see a major sentiment change and another wave higher in risk assets while the longer it drags on, the more likely negativity overwhelms.

But this morning, having already looked at equity markets, we see a key piece of that story is oil (-2.0%) having slipped back. Perhaps the fact that there have been no new skirmishes has people back to a brighter outlook. Or perhaps, as the conspiracy theorists would explain, governments are in manipulating the price lower again. As I look at the chart, though, it remains remarkable to me that despite the Strait having been closed for two months now, oil prices have not risen further.

Source: tradingeconomics.com

The question at this point is how quickly things can return to any semblance of normal when the hostilities end. From what I have read, and I am not an expert, it almost seems like every day the Strait remains closed will require one and a half days more before things get back to the pre-war situation. Of course, even if that is the case, if the war ends, the zeitgeist will change far faster and that will likely be overlooked.

Meanwhile, given the current gold/oil relationship, we cannot be surprised that gold (+0.6%) and silver (+1.3%) are higher this morning.

In the bond market, after yields rose sharply yesterday (Treasuries +8bps), this morning, things are less dramatic with 10-year Treasury yields slipping -1bp and European sovereign yields all softer with Greece and Italy (-5bps) seeing the largest declines although German bunds (-1bp) were more in line with Treasuries. There has been much discussion lately about 30-year Treasuries and how they have traded back above 5.0% again, indicating it is a sign of the apocalypse. However, if you look at the chart below, you can see we have been at or above that level several times in just the past year. I understand 5.0% is a big round number, but I don’t see this as an imminent disaster because of the move. (Don’t misunderstand, the US fiscal situation is a major problem with many potential problems going forward, I just don’t think this is the final straw.)

Source: tradingeconomics.com

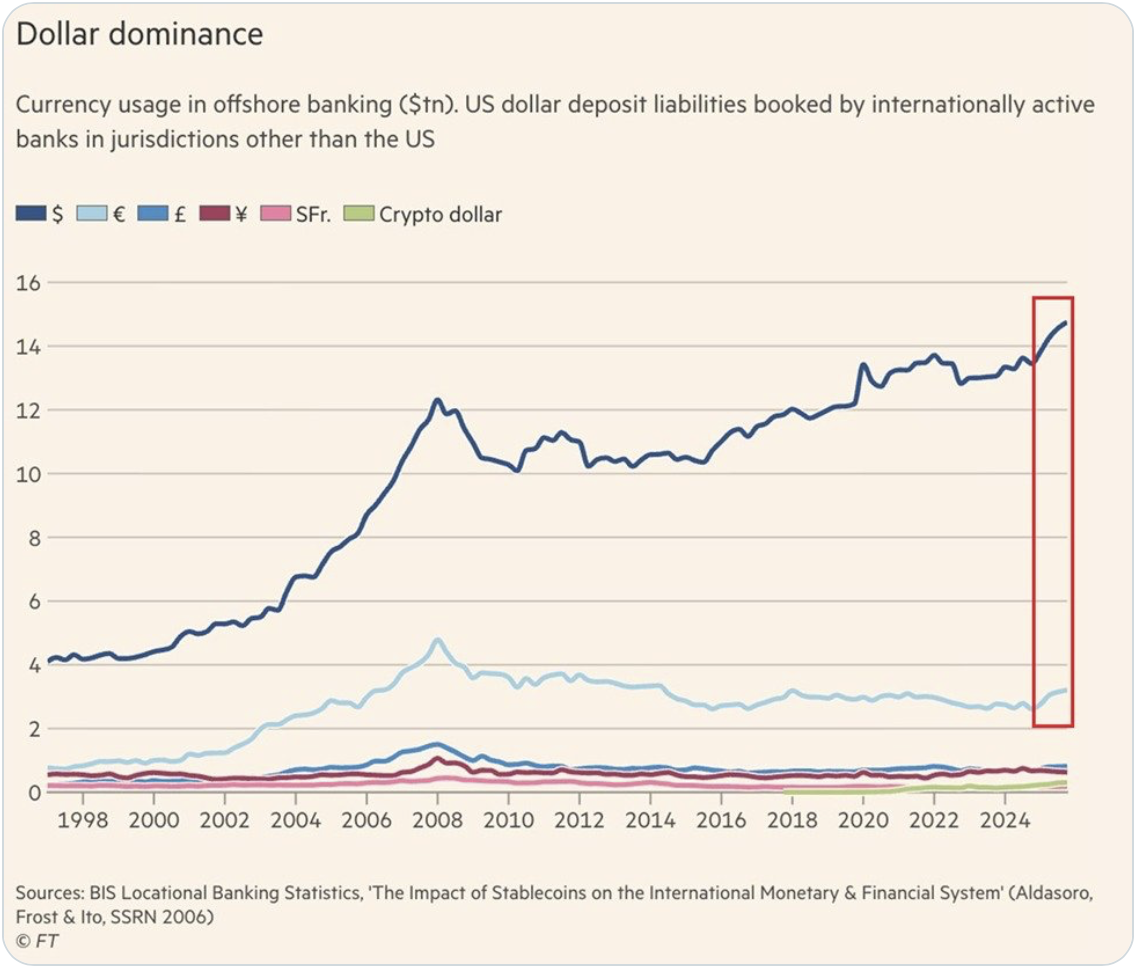

Finally, turning to the dollar, after modest gains yesterday, it is little changed this morning. The RBA raised rates by 25bps, as expected and AUD is unchanged, as are the euro and pound. With the BOJ on holiday, JPY (-0.2%) is slipping slightly, but not showing any major activity. However, we have seen several EMG currencies improve with MXN (+0.3%) and BRL (+0.4%) both benefitting from the increased risk appetite we are seeing in overall markets. The thing about the dollar is it has not been interesting for quite some time, trading within a fairly narrow range. However, while we continue to hear many pundits describe the dollar’s ultimate demise, there is an interesting story in the FT about the dollar’s dominance in global markets as can be seen in the chart below from Kobeissi on X.

This is not a demonstration of the world shunning dollars, just sayin!

On the data front, this morning brings the Trade Balance (exp -$60.5B) along with ISM Services (53.7) and JOLTs Job Openings (6.83M). We also see New Home Sales (668K) and hear from two Fed governors, Bowman and Barr.

But it is all still about the war and oil, and until something definitively changes there, I expect we will chop with every headline.

Good luck

Adf