So, let’s take a sec to discuss

Inflation, and why it’s a plus

At least for some folks.

In gentle broad strokes,

Though most of us see it and cuss

For those who hate Trump it’s a key

To help destroy his legacy

For Congress, they need

Inflation to plead

That taxes must rise like the sea

And what of the Fed and their role

To keep it in check, on the whole

Now, if they’re successful

T’would truly be stressful

For everyone on their payroll

If you were a government and wanted to design the perfect process by which to extract more money from your citizens allowing you to spend more money on the things you wanted, whatever their views, all while explaining that their lying eyes were deceiving them when they complained, it would be hard to come up with a better process than the official inflation figures. Of course, today we get more of those figures with PCE and its variants set to be released at 8:30. While I am here, these are the current market median estimates: PCE (0.5%, 4.1% Y/Y), Core PCE (0.3%, 3.4% Y/Y) although I see no forecast for the Dallas Fed Trimmed Mean reading, the one that Chair Warsh says he wants to focus on. Too, it is key to remember that they are May numbers. How many of you can remember what happened in May?

For instance, looking at the easiest one, oil (-1.0% today), as per the below chart, you can see that WTI ranged between 86.50 and 106.50 during May, mostly sliding, bur arguably averaging in the low 90’s.

Source: tradingeconomics.com

This morning, it is trading below $70/bbl, back to the price on March 2nd, the first market day of the Iran conflict. The BLS indicated that upwards of 60% of the rise in CPI was driven by the rise in energy prices, which tells me that whatever today’s numbers are, they are ancient history and next month’s are going to be lower. I don’t know about you, but I am quite happy that energy prices are falling back to pre-war levels as, a) it makes life more affordable, and b) cheap and abundant energy leads to significant economic output, something good for us all.

But here’s the thing, with energy prices declining, those who benefit from high inflation need a new story, and there is none better than semiconductors. The top headline in the WSJ this morning is The Data-Center Boom Is Sparking a Third Wave of Inflation, right on time for the next big inflation scare. The big winner, at least today, Micron Technology, which had blowout earnings last night and jump-started a serious Techquity™ rally overnight with Tokyo (+4.6%), China (+1.6%) and Korea (+5.4%) leading the way. HK (-1.4%) lagged and the rest of Asia was mixed, but that gives you an idea.

But the point of the article was that we all need to be prepared and accept that higher inflation is coming because the massive resource demands to build AI are coming along before the productivity gains can moderate the price impact. And I have no doubt that the resource demands are going to support prices. I remain uncertain over how quickly AI’s impact will be deflationary, even disinflationary.

And here’s the thing, my lived experience, plus my frequent conversations with The Inflation Guy, Mike Ashton, have me in the camp that CPI is going to live in the mid to high threes for a while to come, regardless of the metrics the Fed uses to measure things.

But I have begun to discern that there is a large community that benefits from rising inflation because it helps them achieve their goals. After all, we know that governments love inflation as it devalues the real value of their outstanding debt, so a steady depreciation is their best friend. As well, Congress’s baseline budgeting ruse, which starts each year from the previous year’s expenditures, not from zero, is a huge beneficiary of inflation. I understand that since about 1980, the BLS has adjusted the CPI calculation somewhere between 30 and 40 times and you can guess the direction of most of those adjustments. Of course, companies that sell products are a big fan as well, as they tend to adjust prices to both include new costs, and increase margins. And they have a natural scapegoat; CPI is out of their hands.

All I’m saying is that while there appears to be a strong effort to fight inflation, I’m not a believer. (And here I should highlight that I use the term ‘inflation’ in the manner it has become understood, rising prices, and not in its classical form of an increase in the money supply, which is 100% the Fed’s doing.)

One other thing. My friend JJ who writes Market Vibes, posted a chart of 1yr breakevens as of yesterday and I reproduce it below.

This is not a signal that the market expects prices to rise, but rather is following the decline in oil prices pretty well. Once again, I will ask, please explain given market signals, why everyone is so sure the Fed is going to hike. I maintain my one cut by year end view which is at least 50bps below the current Fed funds futures market pricing. Ask yourself how the FOMC ‘hawks’, and I use that term loosely, will be able to argue for higher rates if oil continues its trajectory and inflation readings decline. Precautionary? How about they will simply say, we want to screw Trump, at least they would be honest then.

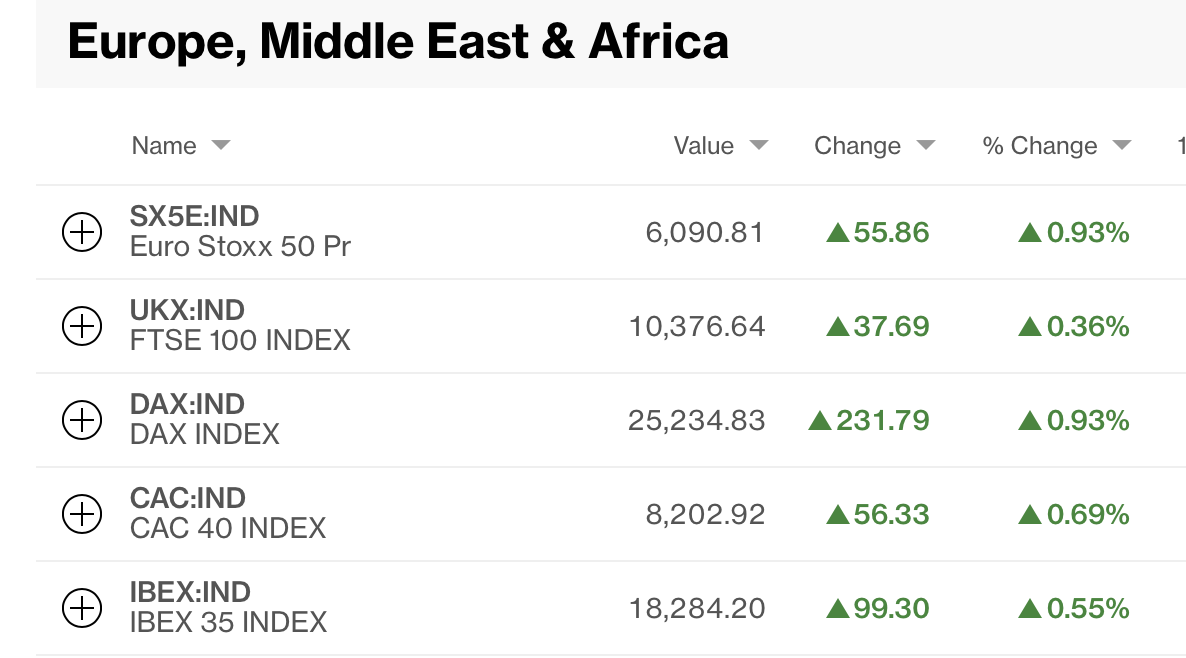

Ok, on to other markets overnight. European bourses are all higher this morning, but since none of them have any real tech exposure, they are not running away. Rather, 0.3% to 0.7% encompasses the magnitude of movement we have seen. As to US futures, at this hour (7:25), NASDAQ (+2.0%) is leading the way, but the whole group is higher.

In the bond market, yesterday saw yields decline about -8bps in the 10-year Treasury and -6bps in the 2-year. this morning they are little changed, consolidating those price gains. As to European sovereigns, yields there also slipped yesterday, but not as dramatically, about -4bps, and this morning they are largely unchanged. Overnight, JGB yields fell -3bps as declining oil prices are feeding through to inflation expectations.

The precious metals complex continues to get hurt, with gold (-0.6%) and silver (-0.5%) still under pressure and at new lows for the year, but copper (+1.25%) seems to have found a short-term floor at $6.00/lb.

And finally, the dollar, which has been en fuego lately, rising for the past six consecutive sessions, as per the below chart, is consolidating for now.

Source: tradingeconomics.com

Nothing has changed the yen story, where the dollar creeps ever so slightly higher each day, now just below 162.00 but overall, today’s movement has been quite muted, about +0.15% in the dollar against most currencies, as the focus turns to inflation, at least for today.

On the data front, in addition to the PCE data we get a bunch more as follows:

| Initial Claims | 225K |

| Continuing Claims | 1800K |

| GDP Q1 Final | 1.6% |

| Personal Income | 0.4% |

| Personal Spending | 0.6% |

| Durable Goods | -4.5% |

| -ex Transport | 0.6% |

| Chicago Fed National Activity | 0.12 |

Source: tradingeconomics.com

Will anyone care about this data? I doubt it, Core PCE is THE thing today, so we will watch and see how that comes out. But mark my words, if it is soft, the hawkish Fed narrative is going to come under real pressure as stocks rally and yields and the dollar slip.

Good luck

Adf