It wasn’t all that long ago

That if people wanted to know

The news, they would turn

To TV to learn

The latest events blow-by-blow

But now TV news when it airs

Has reached the point nobody cares

‘Cause it’s been on X

Without any checks

For networks, the stuff of nightmares

Which brings us to info this morning

That claims, Tehran, talks have been scorning

But also, we hear

A framework is near

For risk takers, this is a warning

I wonder if all of you face the same situation I do, which is answering the question, what is real? The fog of war is truly a descriptive term for the inconsistencies in the information that comes out of the Trump administration, the mainstream media that covers it with their own spin, the Iranians (who seem to be fighting aggressively among themselves) and then looking at prices in financial markets as well as economic data, much of which seems to be inconsistent. How exactly are we to gain an understanding of the big picture, let alone the intricacies of particular markets, given the overwhelming volume of noise we absorb every day.

The below table shows the prices of key markets when I last wrote compared to this morning:

| Market | April 14 | April 20 |

| Oil | $97.35 | $88.50 |

| Gold | $4778 | $4796 |

| 10-year yields | 4.295% | 4.267% |

| S&P 500 futures | 6906 | 7090 |

| DXY | 98.04 | 98.24 |

Source: tradingeconomics.com

I know this is an incomplete listing of things, but I just wanted to touch on the basics. A quick look shows that oil has had, by far, the largest move, nearly a 10% decline, but after that, very little net activity. Sure, there has been some volatility in the interim as you can see in the following charts from tradingeconomics.com, but markets always have a certain amount of inherent volatility, it is the nature of the beast.

In the same order as above:

Oil

Gold

10-year Treasury

S&P 500 Futures

DXY

Of course, much of the movement came after Friday’s announcement by President Trump that the Strait of Hormuz was now open, and the overnight reversals have been a response to the Iranians contradicting that statement and firing on several ships.

It appears that as of now, the Strait is not yet open for free navigation, although apparently there are going to be a second round of talks tomorrow in Islamabad. An interesting story I read indicated that the internal divisions between the IRGC and the secular government in Iran are huge, which is one reason we seem to be hearing multiple things regarding negotiations and goals. We also must remember that all sides in a conflict like this issue propaganda for their own populations that may have nothing to do with their stance in the negotiating room.

The net of all this is, reading about things, no matter how well-read you are, doesn’t really capture the reality on the ground in my view. However, someone else made the point that focusing on the actions, not the words, may be a better tell of the situation, and the action of note is that US troops continue to move into the region, not out of it. I fear there is much more to come here, and the general lack of market volatility is not a sign of calm, but a sign of ignorance on the part of market participants, i.e. nobody really knows what to do!

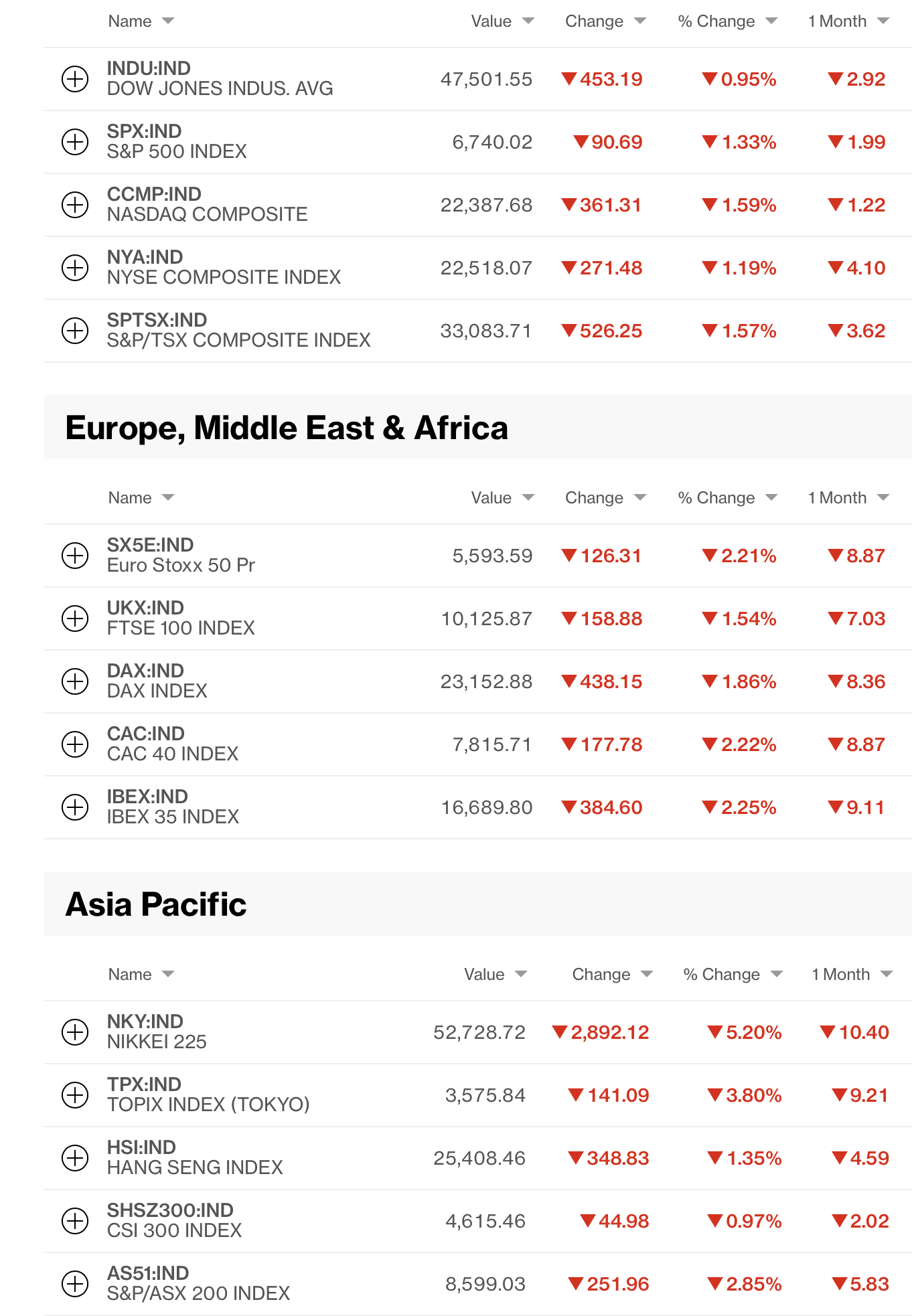

With that in mind, let’s see how markets have behaved in the wake of the Iranian rejection of the statement the Strait was open. Starting in equities, apparently, Asian investors didn’t care as we have seen gains in Tokyo (+0.6%), China (+0.6%), HK (+0.7%) and Korea (+0.4%). In fact, if I look across the entire region, the only notable decline was in Indonesia, and that was only -0.5%. Otherwise, generally speaking, equity investors in the region are sanguine about the current situation. This seems a bit odd to me as Asia is the region that is most negatively impacted by everything going on, but then, I’m just an FX guy.

In Europe, though, things are not as happy with all major indices lower this morning. Germany (-1.4%), Italy (-1.4%), Spain (-1.4%) and France (-1.2%) have set the tone while the UK (-0.8%) is not quite as negatively impacted. I continue to read a great deal about the European rearmament efforts, but net, it doesn’t appear investors are flocking to the continent right now. Uncertainty as to energy availability remains a key impediment, at least in my mind, with respect to a strong investment thesis here. As to US futures, despite the Iranian denial regarding the Strait, the major indices are only lower by -0.6% across the board.

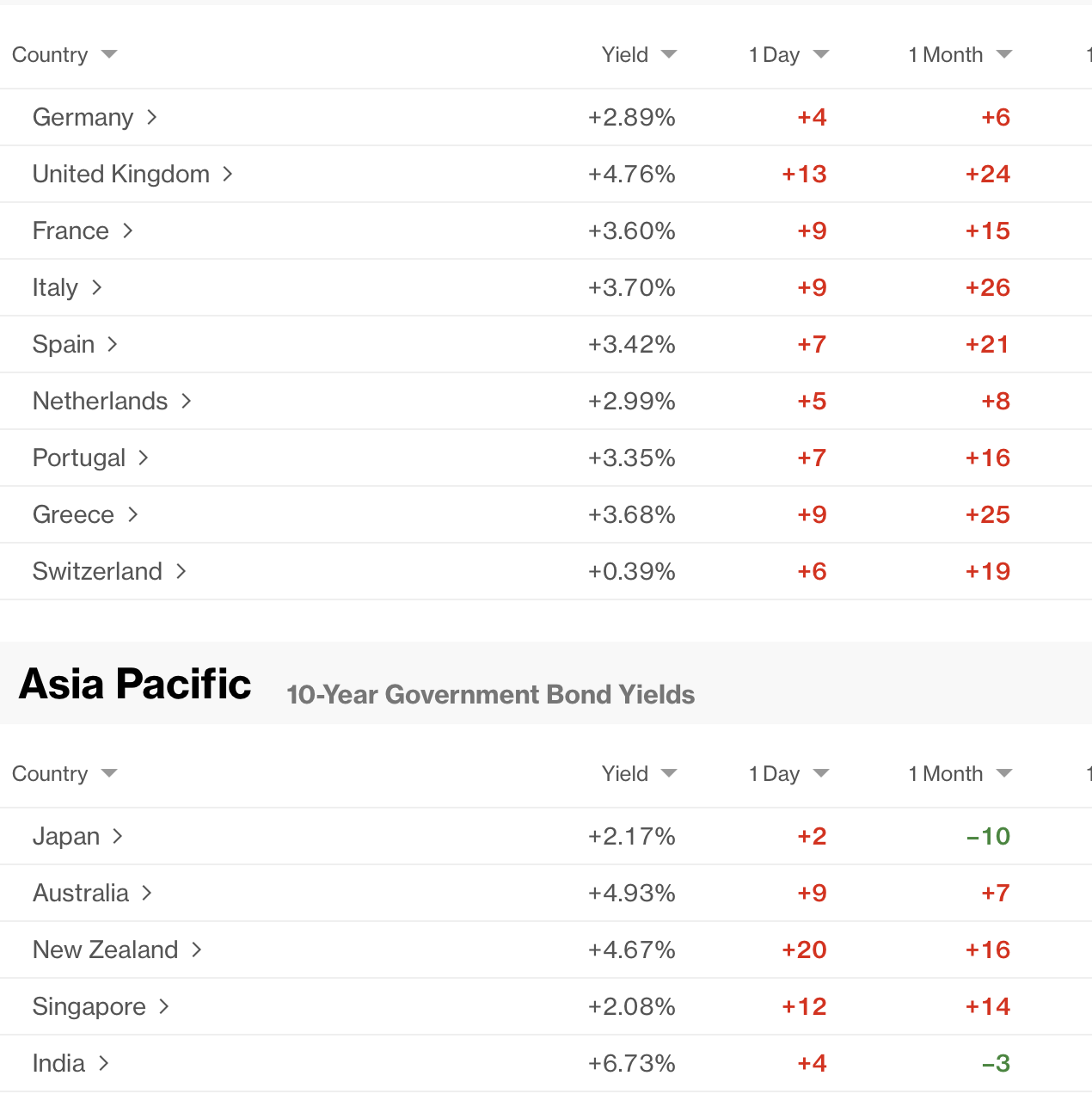

In the bond market, Treasury yields have edged higher by 2bps since Friday, but as you saw above, remain essentially unchanged from last week. European sovereign yields are higher by between 3bps (Germany) and 6bps (Italy) as concerns continue apace regarding the future for European inflation as well as economic activity. JGB yields slipped -2bps overnight amid news that the BOJ is reportedly not considering a rate hike at their meeting next week. In addition, I must note a strong earthquake, measuring 7.4 on the Richter Scale, occurred a few hours ago, so we shall watch closely for how things evolve. Recall it was Fukushima that set off the European madness to end their nuclear power efforts. Hopefully, regardless of the outcome, nothing so incredibly stupid will come of this.

In the commodity space, oil (+5.9%) is obviously higher, but not even back to $90/bbl. There are many conflicting narratives regarding the availability of oil, how much is in storage, how much inventory is around and whether we are going to see production increases outside the Middle East. No market is more directly impacted by the Strait than oil, and since we have no idea how that will evolve, it is hard to see into the near future. Ultimately, I remain of the view that there is loads of oil around and over time, it will come to market keeping prices in check. But it is going to be a bumpy ride. Turning to metals, as has been the case lately, oil and gold (-0.9%) have maintained their negative correlation with the barbarous relic taking silver (-1.7%) and copper (-1.5%) along for the ride.

Finally, the dollar remains an afterthought to traders right now, barely moving against most of its counterparts as the opportunities elsewhere for outsized gains remain far larger. Looking across the major currencies, they are all within 0.2% of Friday’s close, although the direction is uniform with a modest dollar rally.

On the data front this week, perhaps the most interesting thing will be Fed Chair nominee, Kevin Warsh, and his senate confirmation hearings. But here is what the data looks like.

| Tuesday | Retail Sales | 1.4% |

| -ex autos | 1.4% | |

| Control group (ex-gasoline) | 0.2% | |

| Business Inventories | 0.3% | |

| Thursday | Initial Claims | 212K |

| Continuing Claims | 1820K | |

| Flash Manufacturing PMI | 52.5 | |

| Flash Services PMI | 50.0 | |

| Friday | Michigan Sentiment | 47.6 |

Source: tradingeconomics.com

Much has been made lately about the dichotomy between the Michigan sentiment survey printing its lowest level in the 84-year history of the index while the S&P 500 is making new, all-time highs. As I mentioned at the top, what should we believe?

If pressed, my own view is that the US is going to increase the military activity, but that oil prices are already anticipating that action. Much will depend on the success of that situation which remains unknown although I remain positive regarding our military’s capabilities to complete their mission. That will define risk appetite, which I anticipate would be reduced initially, although any signs of success would see that reverse. But again, I’m just an FX guy, so take it for what it’s worth.

Good luck

Adf

PS, this is where I have been the past several days which prevented (?) me from writing, if you care.