The latest pronouncements appear

To indicate Hormuz is clear

As well, Trump explained

He’ll soon have attained

A deal where both sides will adhere

Investors responded by selling

Their oil, as fears, Trump, was quelling

While metals and stocks

Embraced Goldilocks

And rallied with stories, compelling

The word from President Trump is that the Iranians have moved closer to a deal and the ceasefire will remain in place. From what I have read, it appears several ships have, indeed, crossed out of the Strait, although many remain trapped. At this time, nothing is clear, but markets very clearly believe we have passed the peak of the problems as is evident by the below char of WTI (-7.7%) which continues yesterday’s decline and is now back well below $100/bbl.

Source: tradingeconomics.com

Now, we have seen previous situations during this conflict where it appeared that the end was nigh only to be disabused of that notion within days. And we all must still contend with the issue that unless you are in the White House situation room, or the Iranian equivalent, none of us really know what is happening. Propaganda is rife from both sides official pronouncements and then there is a whole cottage industry of pundits who claim expertise in the inner workings of Iranian military capabilities and explain the US is losing the war. But as always, I go back to those with real skin in the game, traders and investors, as opposed to the pundits who when proven wrong simply pivot and say they knew the outcome all along. I certainly hope, for everyone’s sake, that we are in the final stages as we shall all benefit from that outcome.

One other thing helping this story is word that the Chinese have been leaning on the Iranians to reopen the Strait as despite all their preparations and their SPR, the lack of outbound flow is clearly starting to cause Xi some concern. And remember, Xi and Trump are slated to meet in 10 days and I’m guessing he really doesn’t want to have to answer as to why his Iranian allies are holding up the world.

It should be no surprise that with oil prices having retreated so far, the market response elsewhere was strength in equities, strength in precious metals, strength in bonds and weakness in the dollar. After all, those correlations have been solid during this entire engagement. But before we discuss the markets, which are quite positive everywhere, a word about the economy in the US.

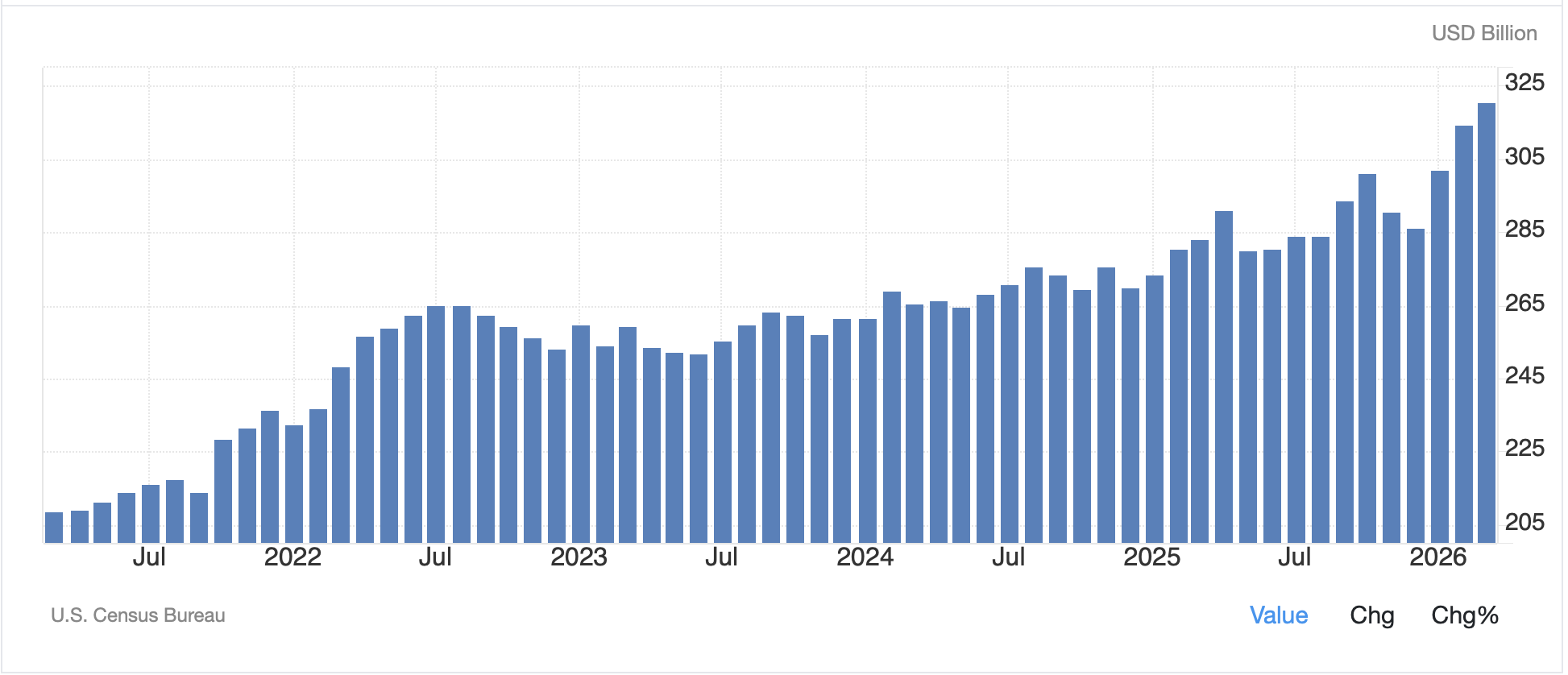

We all know that a key focus of President Trump has been to reshore industry and reduce the trade deficit. While economists have been proselytizing that it’s a great deal for the US; we get cheap stuff and just have to give up paper we print, the Covid pandemic, and more importantly the government responses to it, highlighted just how much the US, and most nations, were at the mercy of China when it came to critical supplies. We all have heard about rare earth metals, but it is a much deeper problem as the US has lost a great deal of institutional knowledge regarding how to simply produce certain things. I raise this point because yesterday the Trade Balance data was released right on expectations of -$60.3B. but I think it is instructive to look at the export data as an indication of just how much change we have seen in the economy over the past several years. as you can see in the chart below, exports have been growing quite significantly of late. Now, one of the reasons is because the US has been exporting significant amounts of oil and gas rather than manufactured goods. But ask yourself, would that have happened under a potential Harris administration who likely would have continued the fight against energy.

Source: tradingeconomics.com

It will be very interesting to see the NFP data on Friday and I will especially be looking at the Manufacturing employment result, as that is something which has clearly been a focus of the administration. I suspect those numbers will look pretty good.

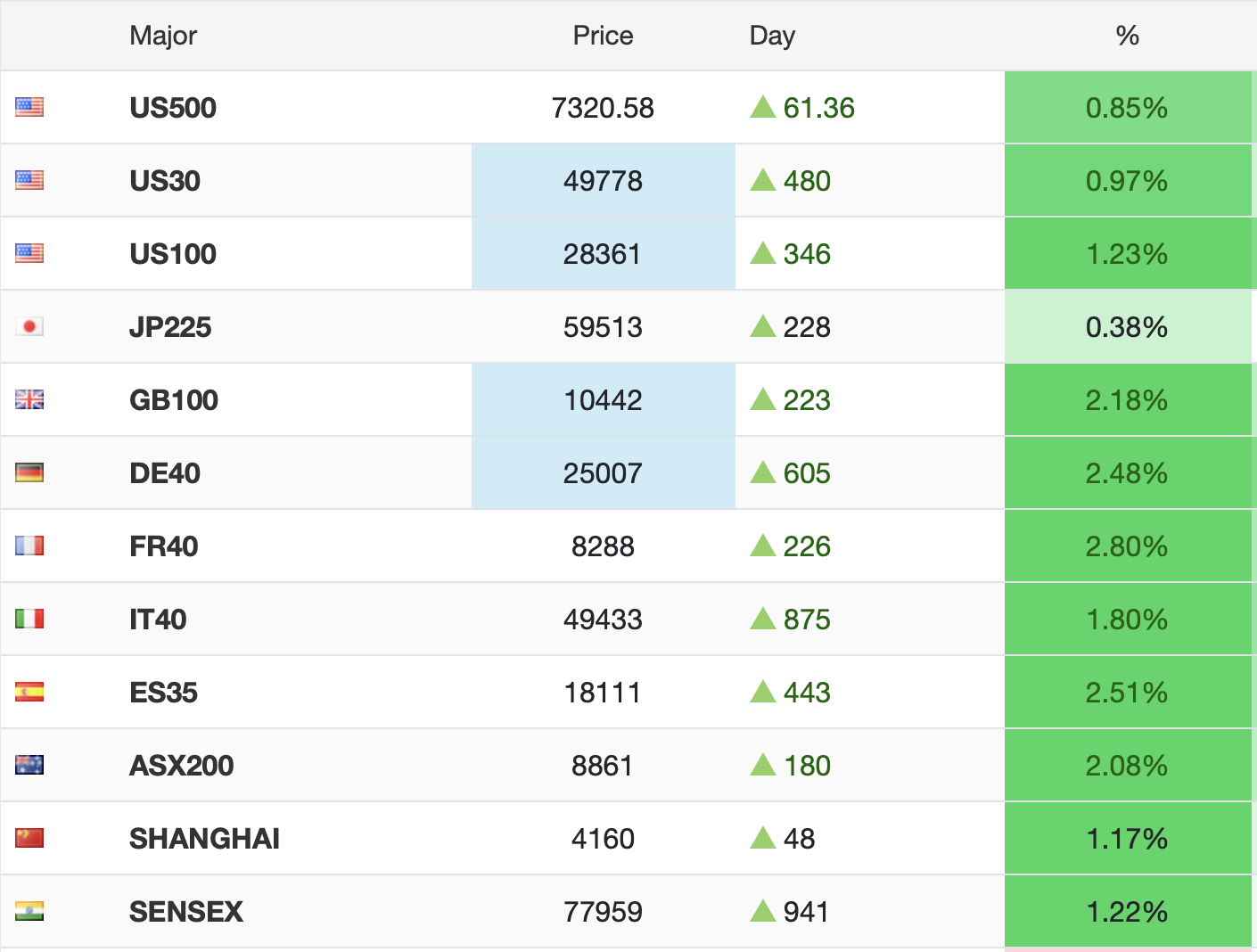

Ok, on to the markets. It is far easier to show a screenshot from tradingeconomics.com of futures prices at 6:30 this morning, than list all the outcomes as below.

Needless to say, there is a lot of happiness in equity markets today. I must note that Japan was still closed last night, so that is not updated, but otherwise, these are all current or from the overnight session. One thing to remember about the US markets as they make consistent new highs is that earnings releases have been remarkably solid thus even though P/E ratios are historically high, there is some rationale behind the moves.

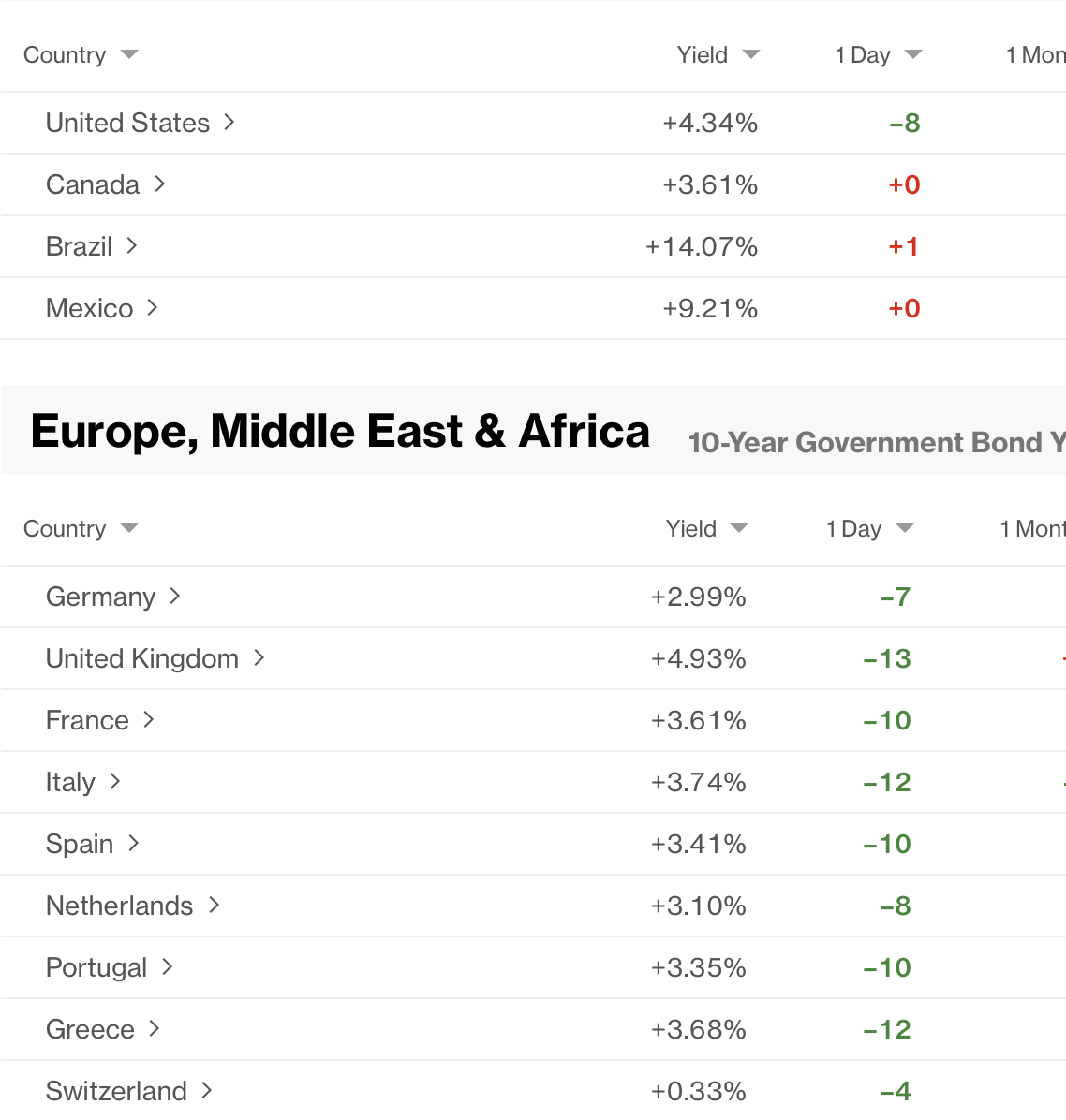

Turning to the bond markets, once again a screenshot, this time from Bloomberg, tells the story eloquently. At this hour, Canada, Brazil and Mexico markets have not yet opened, but I assure you yields there will fall sharply when they do.

As I said, it is happy days everywhere.

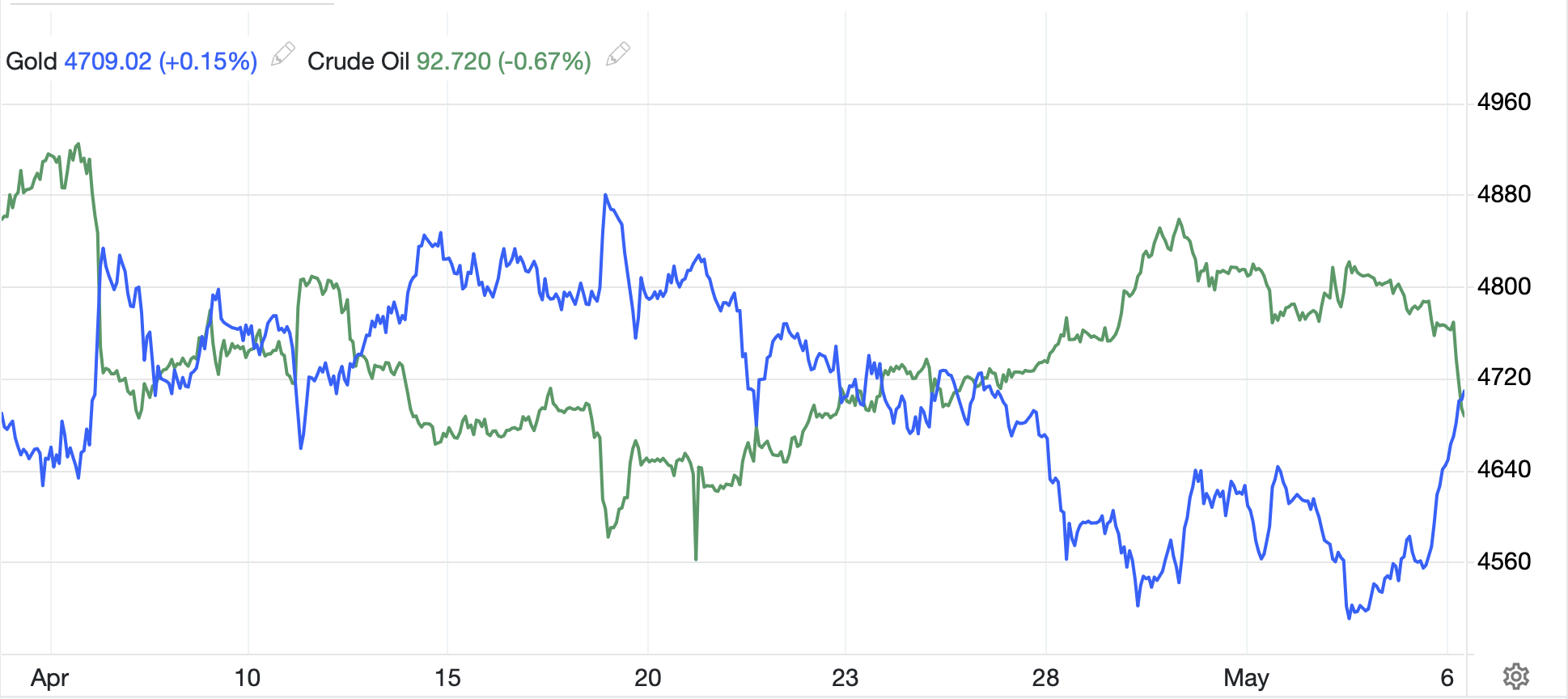

Turning to precious metals, both gold (+3.4%) and silver (+6.4%) are rocketing higher this morning as the recent negative correlation with oil is almost perfect. You can see that below in the chart of price action during the past month.

Source: tradingeconomics.com

Historically, gold and oil tended to trade together, but this event has really destroyed that narrative. I have read an analysis describing gold’s troubles despite the war as a result of fears over higher inflation leading to higher real interest rates and thus less demand for gold. Maybe that is correct, but my take on the bigger picture remains that fiat currencies will remain under general pressure against ‘stuff’ and gold is the most desirable of ‘stuff’ there is. I remain long-term bullish here.

Finally, the dollar is under pressure this morning, as you would expect given the overall market movement. The most noteworthy price action has been in JPY (+1.35%) which appears to have seen some further intervention from the BOJ last night as per the below chart.

Source: tradingeconomics.com

When asked, there was no comment from the BOJ/MOF, but certainly given the velocity of the decline in the dollar and given the type of movement we have seen during the past week, with the first major intervention essentially confirmed, it makes sense. Tokyo markets remain closed, so the timing made sense as liquidity was light allowing a lot of bang for their buck. But remember the history of intervention is that while it can provide a temporary solution to a weakening currency, until policies change, the pressure will remain.

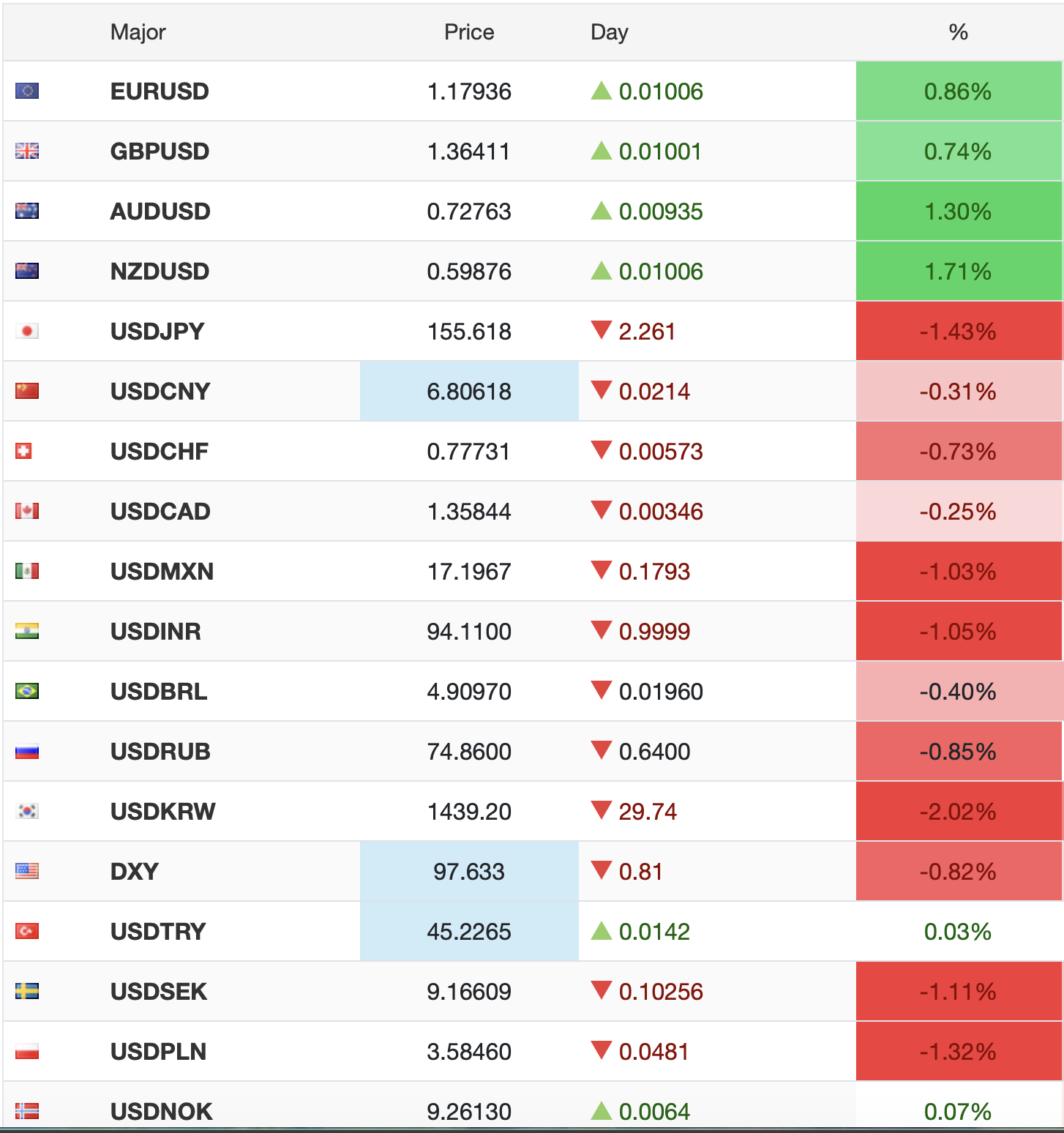

But broadly the dollar has been routed overnight. One more tradingeconomics.com screenshot will give the flavor for the market this morning.

The outliers here are NOK (-0.1%) which is suffering from oil’s sharp decline, along with CAD (+0.25%) which also is feeling that pressure. Not in the shot is ZAR (+2.3%) which has been feeling double pain of weak gold and high oil and seeing a real relief rally today.

If you ask, is this the end of the dollar and now it will decline sharply going forward? I would answer no, but that doesn’t mean we won’t test the bottom of the DXY range at 96.50 before this move is over.

On the data front, today brings ADP Employment (exp 99K) and then the EIA oil inventory data with another draw expected. But I don’t see the data as critical with the peace story driving markets and headlines for now. In this situation, the dollar will likely remain under pressure in the near term, but nothing has changed my longer-term view of relative strength.

Good luck

Adf