Since April, the story has been

The stock market’s yang with no yin

But yesterday’s fall

Reminds one and all

Be wary or there’ll be chagrin

Since the beginning of April, as you can see in the below chart of the S&P 500, stocks have risen sharply (~18%) as up days outnumbered down days 33 to 12, including yesterday’s drop. That’s a pretty good definition of a raging bull market.

Source: tradingeconomics.com

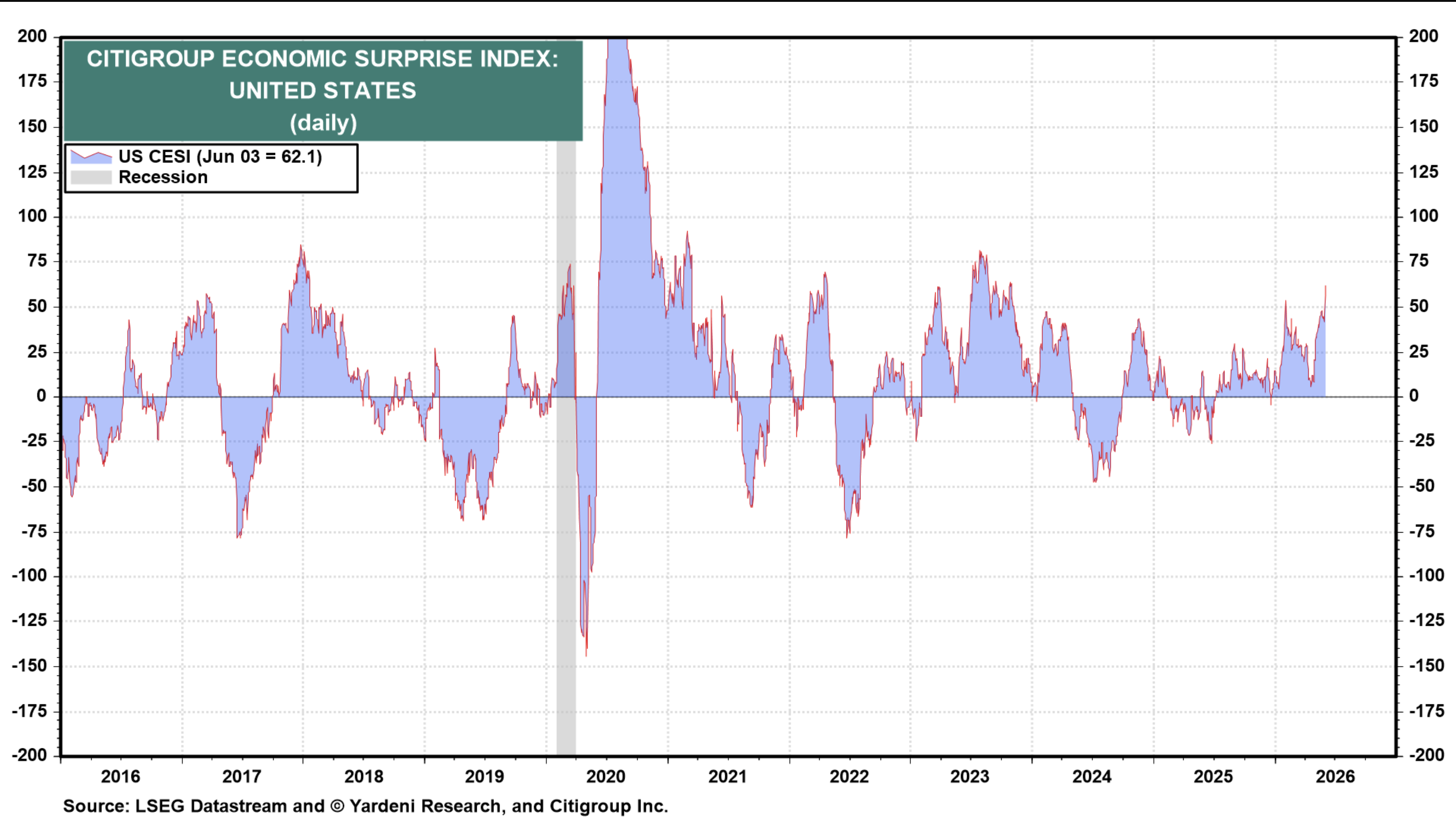

Here’s the thing; nothing really changed yesterday. Certainly, there has been no change in the status with the Iran conflict, and therefore no change in the prospects for oil prices going forward. If anything, the data we have been getting has been demonstrating that the US economy is performing better than expected with yesterday’s ISM and Factory Orders data stronger than forecast as was the ADP Employment Report. If you add that to the JOLTs data from Tuesday, it appears that the overall jobs situation in the US is diverging from the narrative that AI is going to take all the jobs and there is nothing left for people to do. In fact, a look at the Citi Surprise Index, designed to show the difference between actual economic releases and the forecasts ahead of those releases shows it has risen to its highest level since mid-2023 as per the below chart.

This is a strong signal that the economy, despite a lot of negative talk, is doing pretty well. Of course, by now we have all learned that the stock market and the economy are very different things. While historically, the relationship between equity markets and the economy was clearer, with equity markets a reasonable estimator of future economic activities, with somewhere between a 6 month and 1 year lag, ever since the GFC and the financialization of the economy, that relationship has lost much of its luster. Rather, akin to my discussion of the yen being dependent on capital flows, not economic activity, that is also the story of stocks right now.

This brings us to the story that really seems to be percolating around the market, and that is the imminent IPO’s of SpaceX, Anthropic and OpenAI, as well as Google’s $80 billion share sale. For the last 30ish years, between share repurchases by companies and the growth of Private Equity which gobbled up public companies, the number of publicly listed company equities has been shrinking, with the number falling roughly in half during that period. According to Grok, at the end of 2025 there were just 3,657 domestic companies listed on US exchanges, not even enough to fill out the Russell 5000! With that in mind, and remembering the laws of supply and demand, it ought not be a surprise that prices rose while supply fell.

But is that getting set to change? While headline companies like SpaceX will get all the press, it seems likely that PE firms are going to be looking to IPO many of their holdings given current overall valuations. Remember, many of these companies were bought during the era of ZIRP, so debt financing made lots of sense, but once the Fed tightened policy, it has been a problem. Retail investors have been hoovering up equities for a while now, and I suspect we are going to see a lot more equities come available to meet that demand. In fact, this is the best story I have heard about what can halt the rally.

But this can also highlight the difference between the economy and the stock market. Consider the ramifications of the mega names issuing stock and using the funding to continue to build out the AI infrastructure including data centers, power production, turbines, semiconductor fabs, etc., that is all going to result in significant economic activity as people get hired to do the work and all the benefits that accrue from investment lead to real growth in GDP. We could easily see equity markets stall, or stumble while the economy powers ahead. Something to consider for the medium-term view here.

But in the short-term, let’s turn to markets and see how yesterday’s US declines played out overnight. Asia had a generally miserable session with every major and most other regional exchanges sliding. This included Tokyo (-1.4%), HK (-1.5%), China (-0.7%), Korea (1.8%), Taiwan (-1.7%) and Australia (-1.1%). And the smaller markets were no better as India (0.0%) was the top performer. In Europe, though, the picture is not so dire as only the UK (-0.9%) is under real pressure with the continent (France +0.6%, Germany +0.35% and Spain +0.25%) all managing small gains. Perhaps the driver here has been inflation data which showed that it has not risen as fast as feared and therefore there is a bit less concern about more aggressive ECB tightening. As to US futures, they are mixed this morning with NASDAQ (-1.35%) falling sharply on poor Broadcomm earnings although the DJIA (+0.7%) are rebounding from yesterday’s losses as investors rotate a bit from tech to industrials while oil prices have slipped aiding things.

Speaking of oil (-2.3%), it appears to be responding to comments that the US will not resume an all-out war absent the death of US troops. At least that’s one rationale, although the idea of the price heading back to its recent average is viable as well. However, this has helped metals markets (Au +1.25%, Ag +1.8%, Cu +0.5%) as that relationship remains quite solid.

In the bond market, yields are also responding as would be expected with Treasuries (-3bps) leading the way as European sovereign yields all slip between -1bp and -2bps.

Finally, the dollar is giving up some of its recent gains but as you can see in the chart below for the DXY, during the past 3 weeks, the index has traded between 98.85 and 99.55, a very tight range and indicative of the general lack of movement in the dollar.

Source: tradingeconomics.com

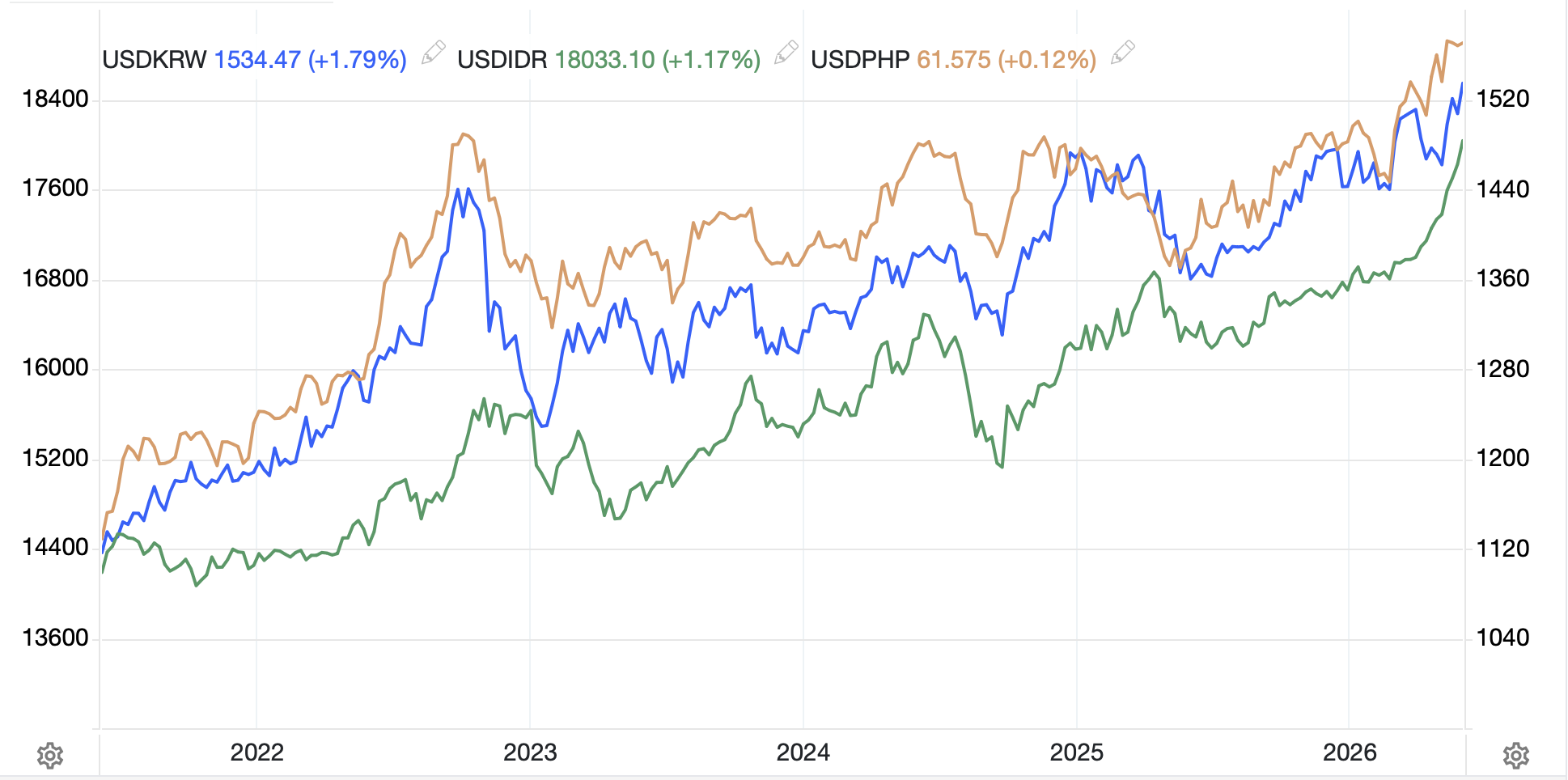

However, that is the dollar writ large vs. major currencies. Against several Asian currencies, the story is not the same. The below chart shows the Korean won, Indonesian rupiah and Philippine peso, all of which are trading at their lowest levels since the GFC as the pressure from higher oil prices and reduced supplies has really impacted their economies and currencies by extension.

Source: tradingeconomics.com

As to the JPY, it managed to trade through 160.00 yesterday, but only just, and this morning sits just below that level with no sign of the BOJ/MOF. The Japan story remains the same, but the changes required there will be politically fraught. However, for the smaller Asian nations, much is out of their hands, and my sense is that while they will all seek to mitigate the pace of decline, there is very little they can do to stop it on their own. That will require the Iran situation to end and oil prices to head back lower with supplies rebuilding.

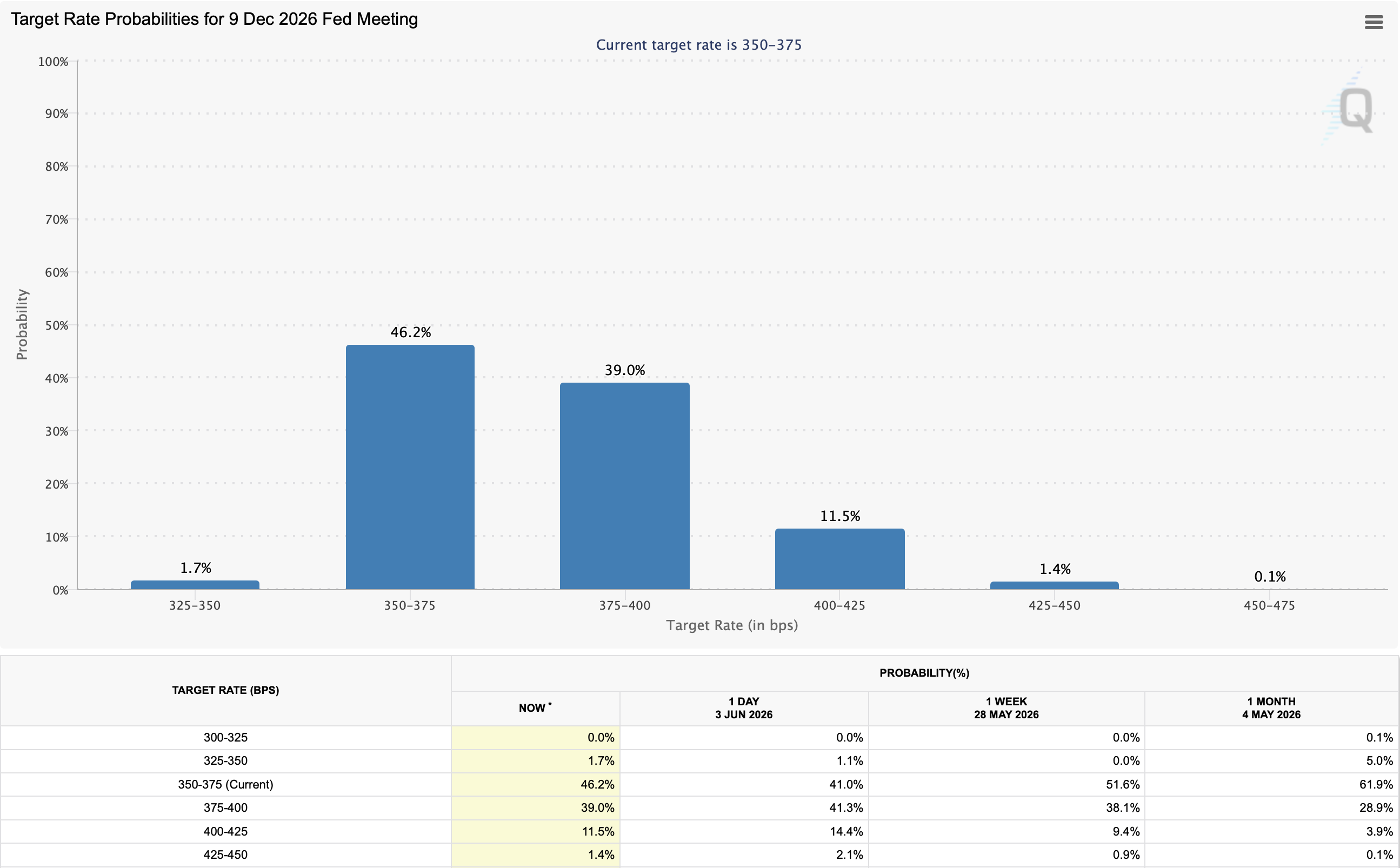

On the data front, this morning brings the weekly Initial (exp 213K) and Continuing (1780K) Claims data as well as Nonfarm Productivity (0.5%) and Unit Labor Costs (2.5%. Too, we hear from several more Fed speakers but given all the other things that are ongoing, their words don’t seem to move markets. For instance, yesterday Dallas Fed president Logan said she thought inflation pressures indicated rates may need to rise. But she is a known hawk, one of the hawkish dissents at the last meeting, and thus this is not new news. Below is the CME’s futures probability page for the December meeting which shows a slightly more than 50% chance of a hike by then. However, if you look at the table at the bottom, you can see that the probability has been creeping higher in the past month, although that is just as likely on the back of the better data than any Fedspeak. Certainly, next week’s first Warsh chaired meeting will get a great deal of attention.

And that’s really it for the day. In the FX market, as well as bonds frankly, I don’t expect anything of note. Oil looks to be drifting lower while metals drift higher and the real wild card is equities, which have been showing inordinate strength. My thoughts above reflect my views for potential later in the year, not today.

Good luck

Adf