So, suddenly, silver and gold

Are both getting bought and not sold

But oil’s still rising

So, what are folks prizing?

Perhaps risk’s now out in the cold

At least, here at home that’s the case

As AI stocks sell off apace

And what of the buck?

It’s basically stuck

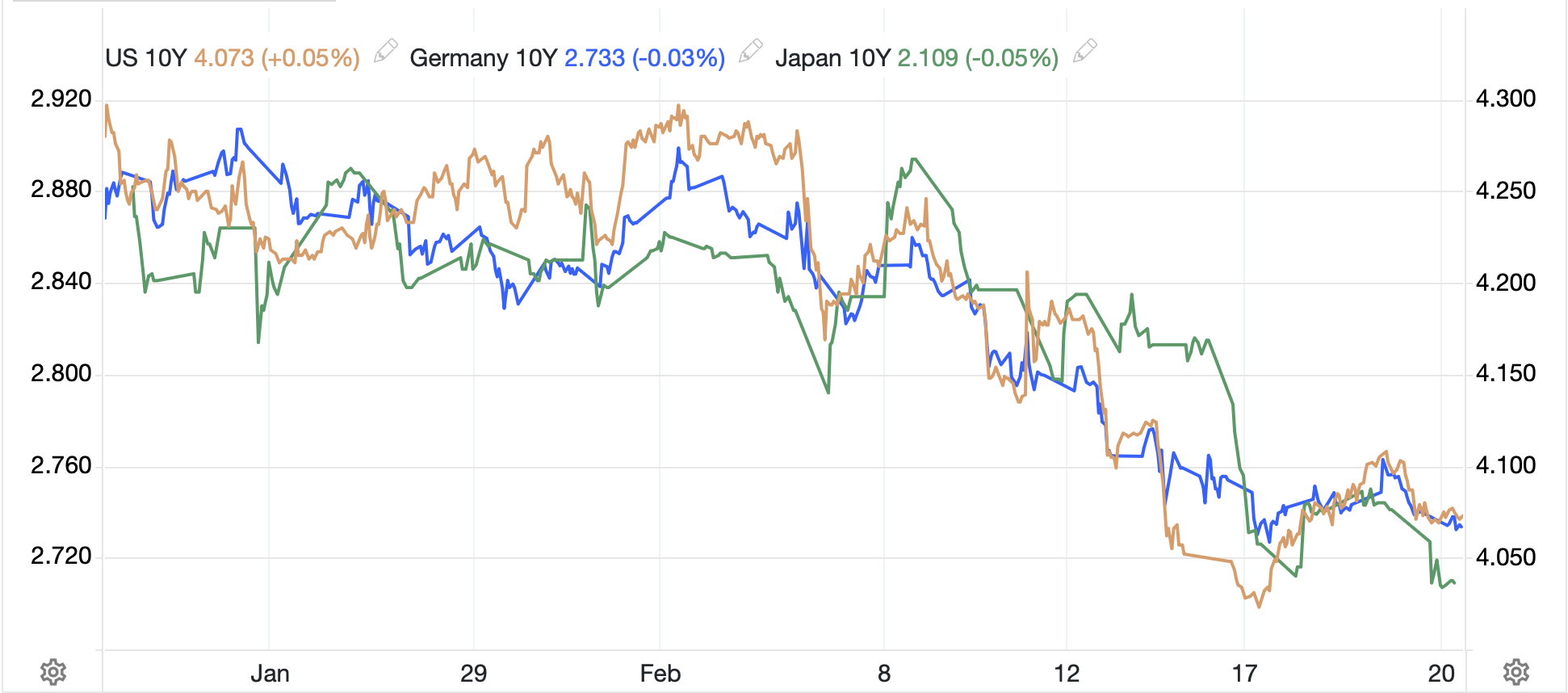

While bonds are just standing in place

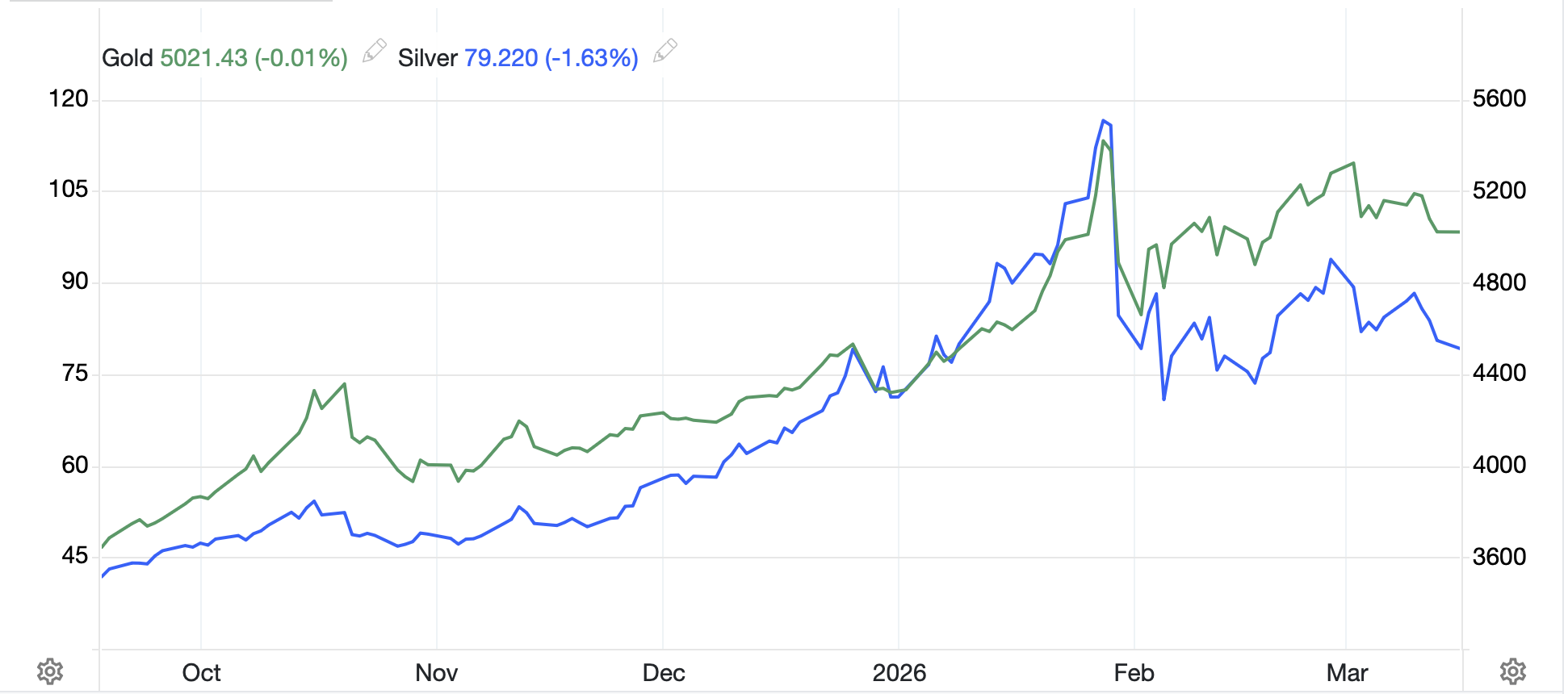

Arguably, the biggest change in market relations in the past two sessions is that the metals markets have rallied alongside the price of oil. Since basically the beginning of this conflict, this has been one of the conundrums in markets. Gold, which has a long history as a safe haven, started selling off (granted from a parabolic move) shortly before the US attacked Iran. In fact, many ascribed the sell off to the naming of Kevin Warsh as Fed Chair given the view he was the most hawkish of the potential candidates. But once the fighting started, gold continued to decline, falling some 27% from its initial burst higher at the beginning to its recent low, below $4000/oz.

Source: tradingeconomics.com

Of course, the oil story is quite different as there were far more twists and turns in the price action as the military activity ebbed and flowed and as comments about ceasefires and peace talks were made and denied on a regular basis.

Source: tradingeconomics.com

But certainly, the impression from the recent price action was that when oil rallied, gold sold off and vice versa. The ostensible rationale was that higher oil prices would drive inflation higher and interest rates would follow thus reducing the attractiveness of holding gold. And perhaps that was true, at least to some extent. However, that was never a satisfying explanation to me. And, throughout the conflict I have maintained that the medium and long-term views for the metals was quite positive.

However, something seemed to have happened yesterday, and I see no indication of exactly what that was, but we saw oil, gold and silver all rally nicely on the day. The oil story is clear as the latest issue is the Houthis now blocking Saudi ships from traversing the Bab-al-Mandeb at the southern tip of the Red Sea and reducing flows. But the metals story remains a mystery. Granted, this has only been ongoing for a bit more than twenty-four hours, but the magnitude of the metals moves (Au +3.0%, Ag +5.7%) in the past two sessions is pretty substantial for markets that had been doing very little but sliding for months.

Source: tradingeconomics.com

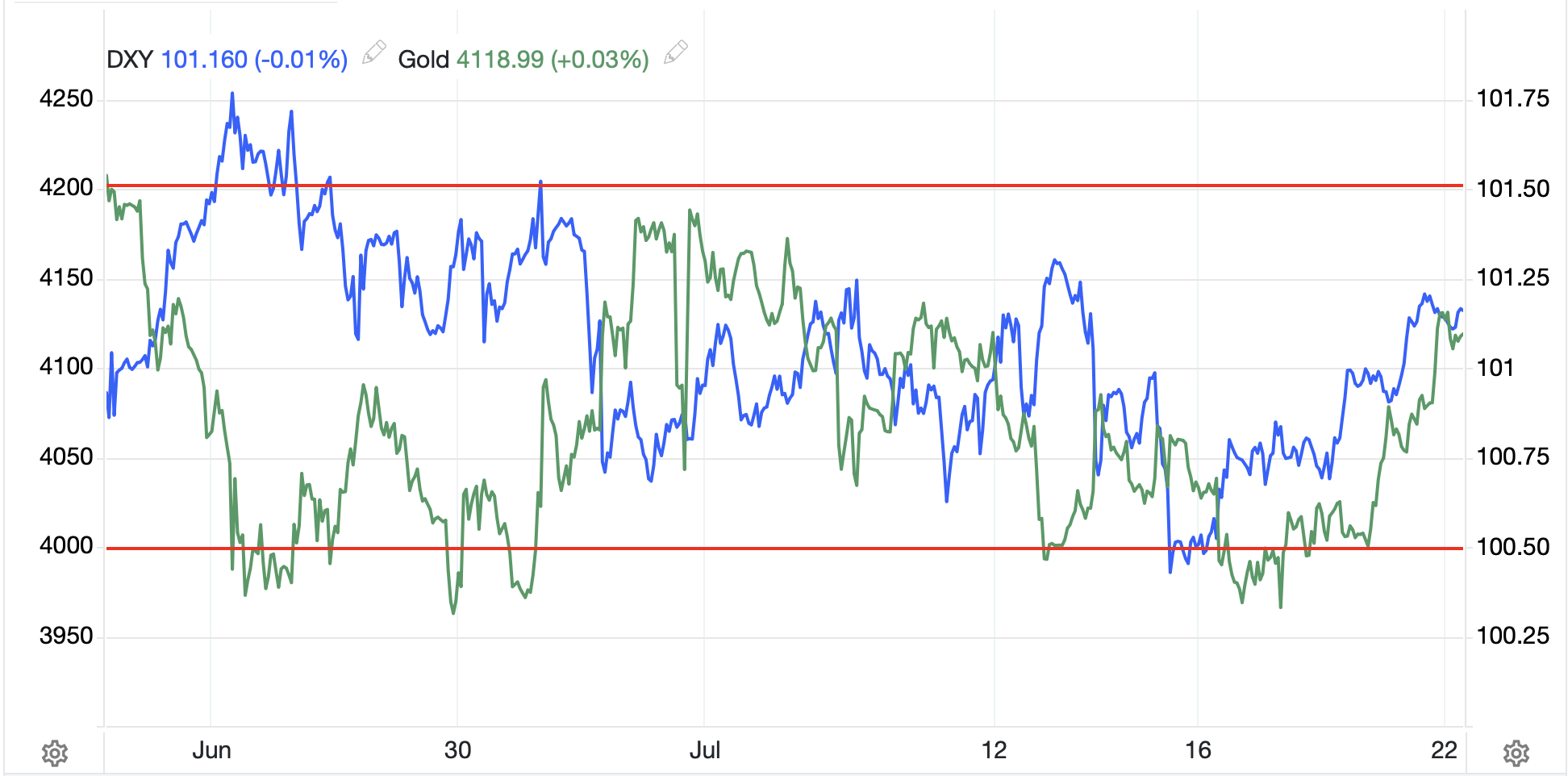

I don’t believe this has been short covering, as in reality, both markets had lost speculative interest given the lack of volatility over the past months, and so short sellers were not involved. There were far too many other, juicier targets for them. As to the dollar, which has long had a negative correlation to the precious metals, as it has traded in a 1% range for the past month, as per the below chart, it is hard to ascribe much causality there.

Source: tradingeconomics.com

However, I sense that we are beginning to see some changes to the relationships that have held for the past several months, so we need to be alert for other seeming anomalies.

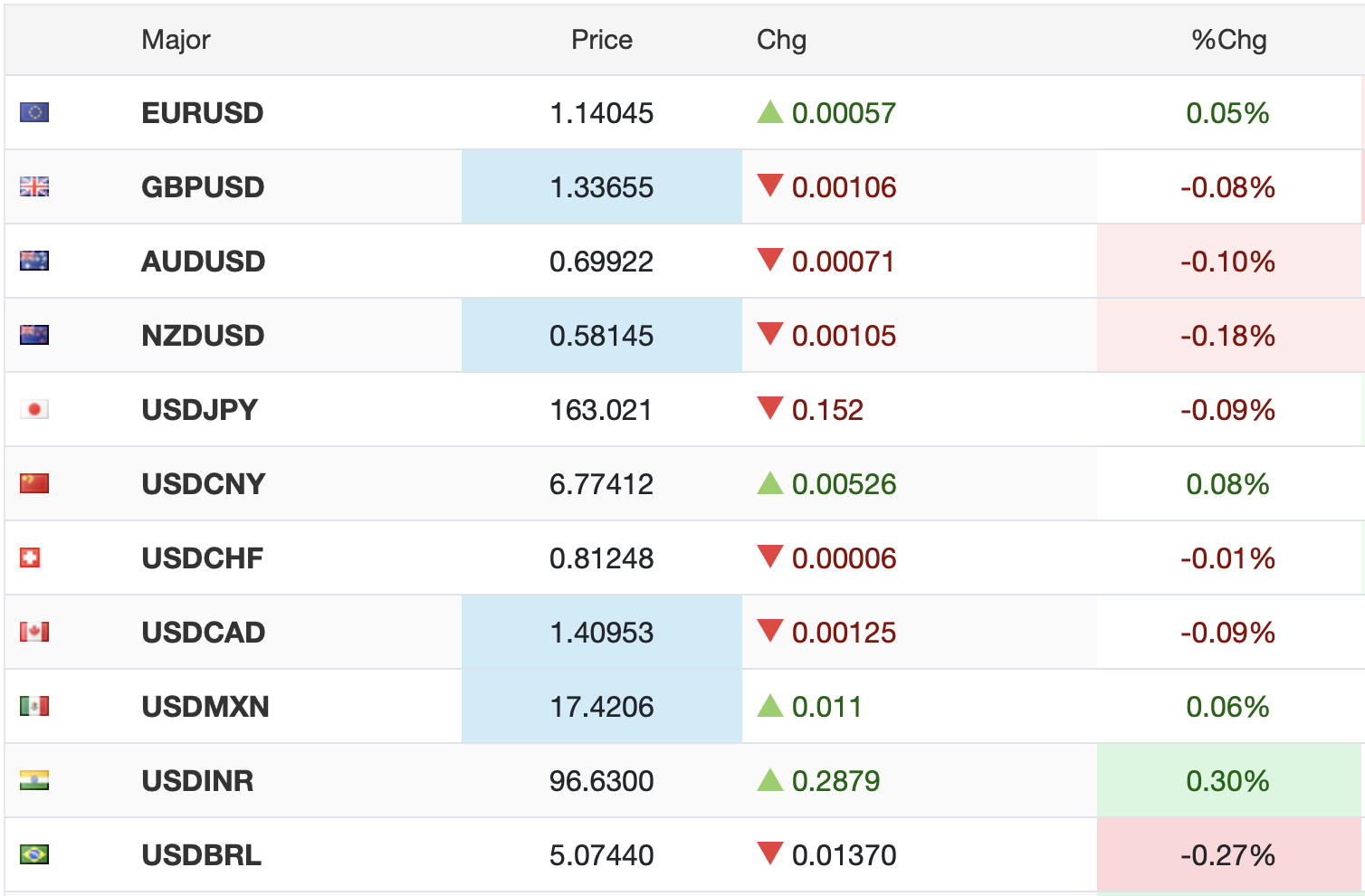

Turning to the other markets, and continuing with FX, while generically today, it is doing very little as per the below screenshot,

Source: tradingeconomics.com

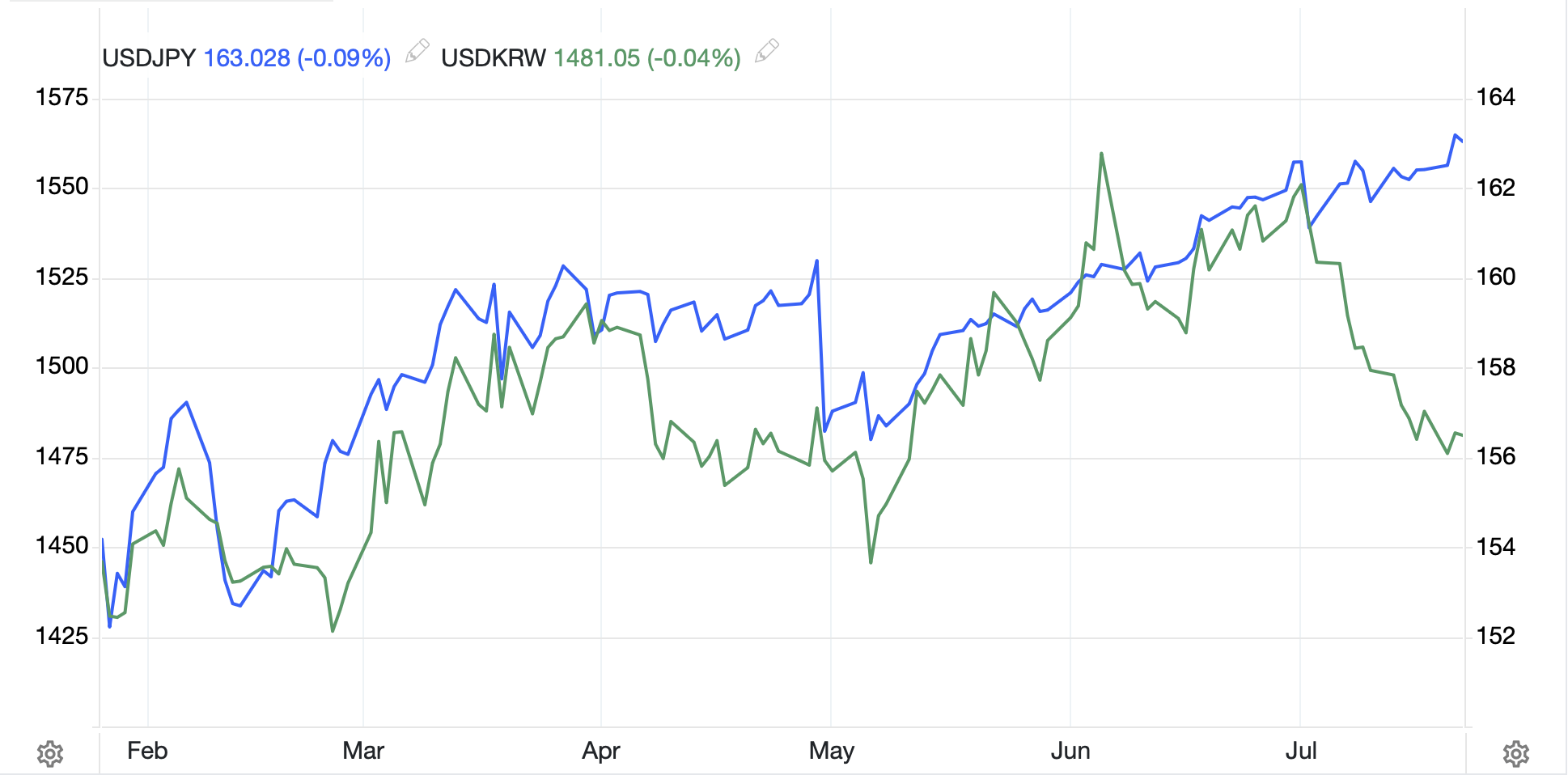

It is worth discussing the yen, which yesterday traded below (dollar above) the 163 level for the first time since 1986. Not surprisingly, we heard from FinMin Katayama as follows: “The situation involving the US and Iran has taken a sudden turn for the worse — a deterioration that the world did not foresee — creating a very difficult environment. Our policy remains completely unchanged: We will take appropriate and bold action at any time, should the need arise.” However, as I have maintained, given the incredibly slow pace of the decline of the currency and given that speed of decline and the volatility in markets has always been an important part of the MOF’s decision matrix regarding intervention, it seems we are not near that step. One need only compare the JPY to KRW, a currency with low historic volatility, to see that the yen has not been very active. In fact, the biggest movements have been caused by the MOF in their intervention and comments.

Source: tradingeconomics.com

There has been an increase in market discussion regarding whether the BOJ is going to hike rates again at the end of this month, which is not the market forecast, nor would it be considered the norm given they hiked rates last month. Most analysts expect the pace of rate hikes to be every six months as they gradually tighten policy. Of course, they could change that, but again, the yen’s weakness has many fundamental drivers with rates being only one of the issues. Personally, I don’t see a hike next week, but I guess anything is possible.

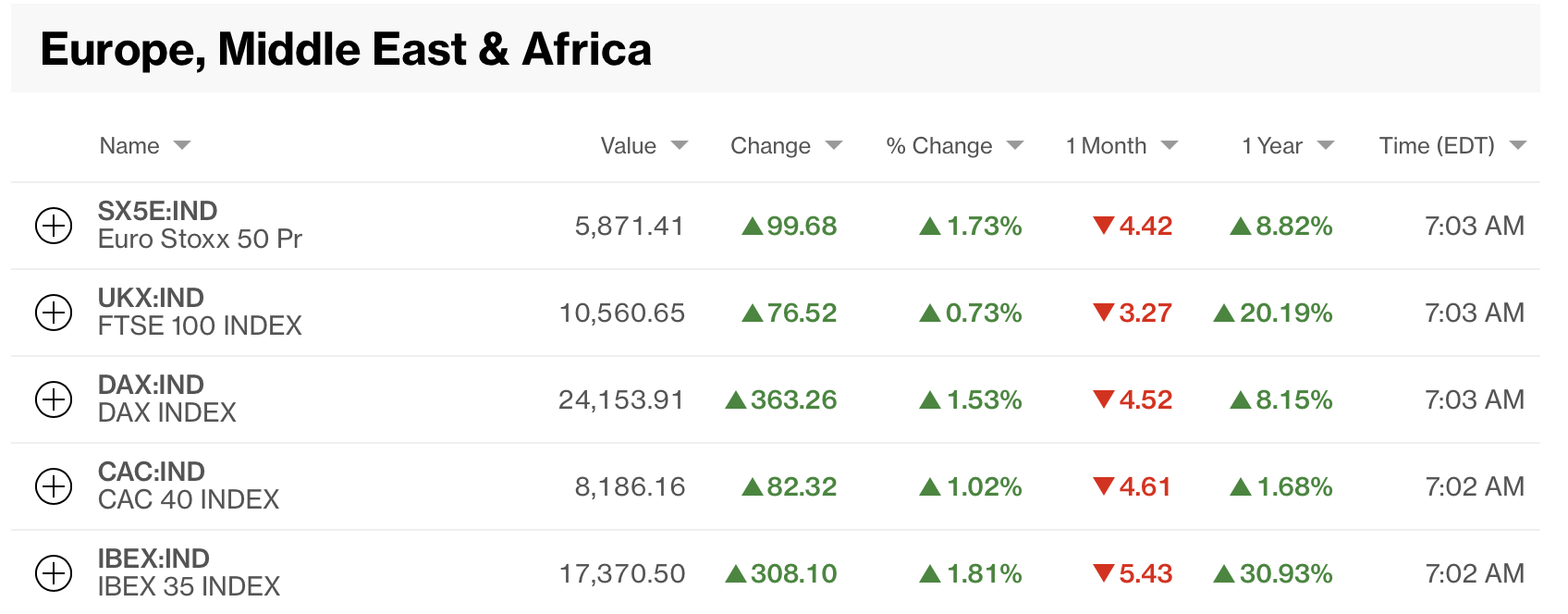

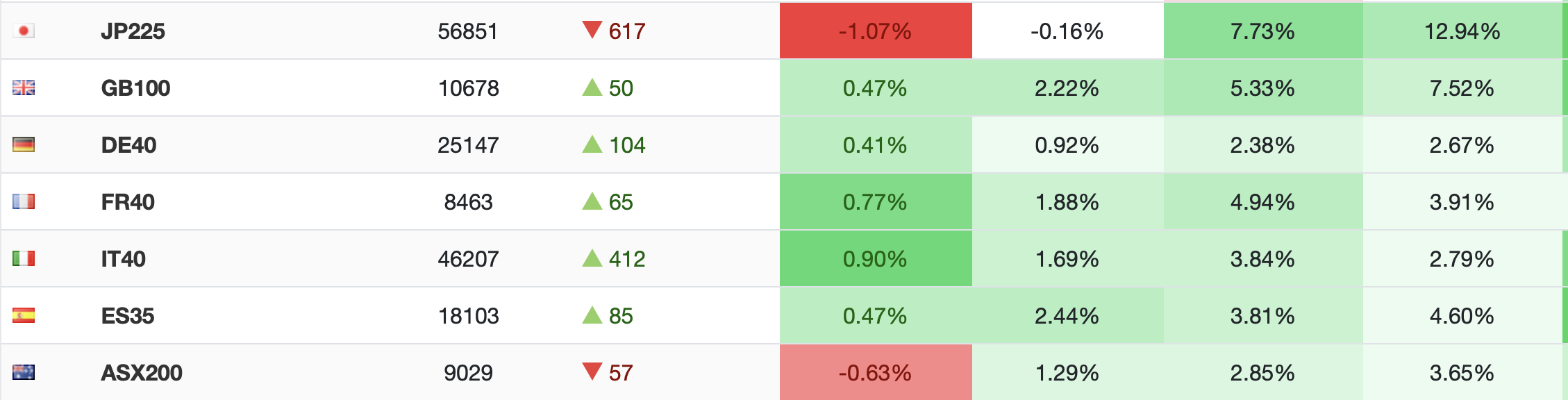

Which leaves us with bonds where yields around the world are creeping higher on a regular basis, Treasuries +1bp, European sovereigns +3bps today, and equities. Yesterday was a solid day in the stock market in the US with tech stocks leading the way higher. And while Europe is following suit this morning (UK +1.2%, France +0.8%, Spain +1.0%, Germany +0.3%), last night’s Asian markets were less buoyant. Tokyo (-0.2%), China (-0.5%) and HK (-1.0%) led the charge lower although there were some bright spots, notably Singapore (+1.2%), Taiwan (+1.3%) and Korea (+0.7%). I guess overall it was a mixed session. As to US futures this morning, as I type at 8:05 they are pointing lower led by NASDAQ futures (-1.5%).

Net, some of the relationships with which we had become familiar seem to be breaking up a bit. I think no matter how you slice the equity market, it is trading at rich levels, so a correction of some sort seems realistic. I presume that if the tech earnings next week disappoint, we will see a pretty big downdraft. As to oil, while there is still plenty around, the war drums are beating louder and that is not helping things. But bonds and the dollar are sitting this move out, at least for now.

There is no data released today and the Fed is in its quiet period, so we remain beholden to headlines from Iran, the White House and other earnings outcomes. I have a sense of uneasiness about the day, but nothing to put my finger on.

Good luck

Adf