While talks in Qatar carry on

No outcome, as yet, is foregone

Thus, traders are waiting

Before speculating

As all seek the great denouement

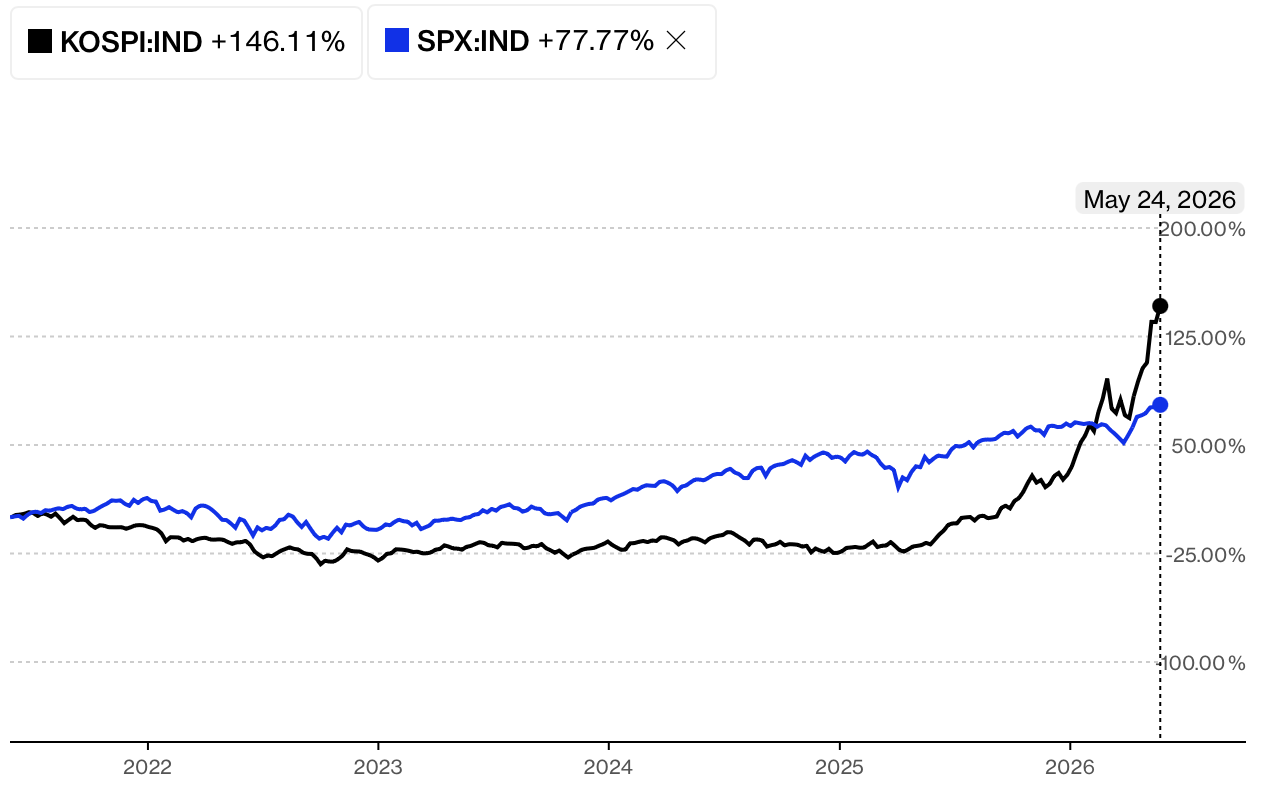

Range trading remains the norm, except for the S&P 500 which continues to make new highs almost every day. At least that is true in US markets. The KOSPI in Korea is also rocketing higher. In fact, when comparing the percentage movement over the past 5 years, the S&P looks quite ordinary, but that is because the KOSPI has been insane!

Source: Bloomberg.com

But away from a few select equity markets, it is getting increasingly difficult to find markets that are doing much more than chopping back and forth. This is especially true if we take a step back and look at movement over the past several years.

For instance, if we look at the 10-year Treasury, where we saw all sorts of angst last week when it traded to its highest level, near 4.70%, in a year, realistically, we have been rangebound for more than two years as per the chart below. And prior to that we were in the massive abnormality of ZIRP. So, if we go back over a longer time frame, the current 10-year yield is right around the long-term average as per the second chart. It is really hard to get excited about this movement.

Source: tradingeconomics.com

Source: finance.yahoo.com

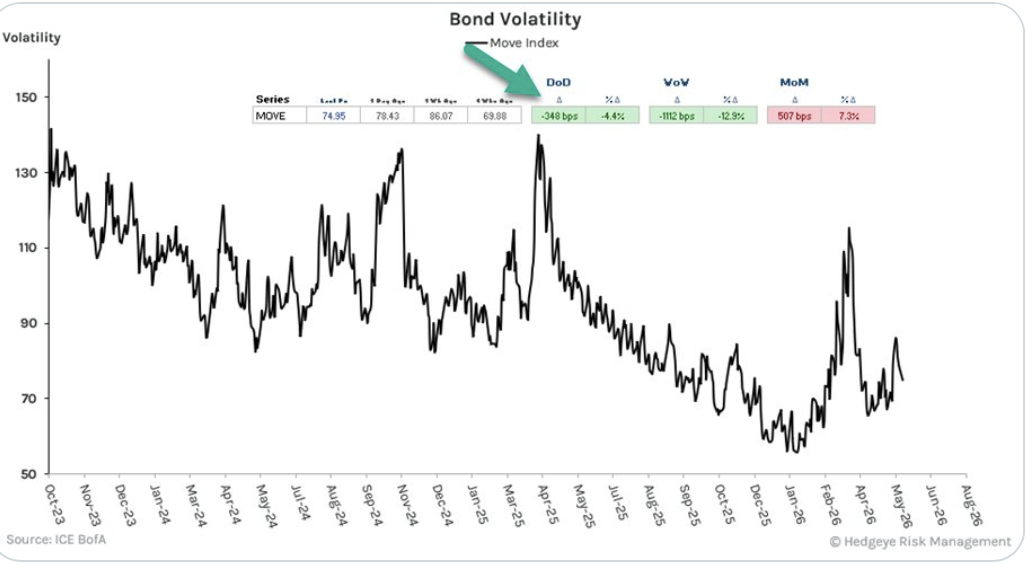

Perhaps we ought not be surprised that bond market volatility is heading lower again as per the below chart of the MOVE Index from Hedgeye

The same story exists in currencies, where major currencies have been in a range for more than a year as per the below chart of the DXY from tradingeconomics.com.

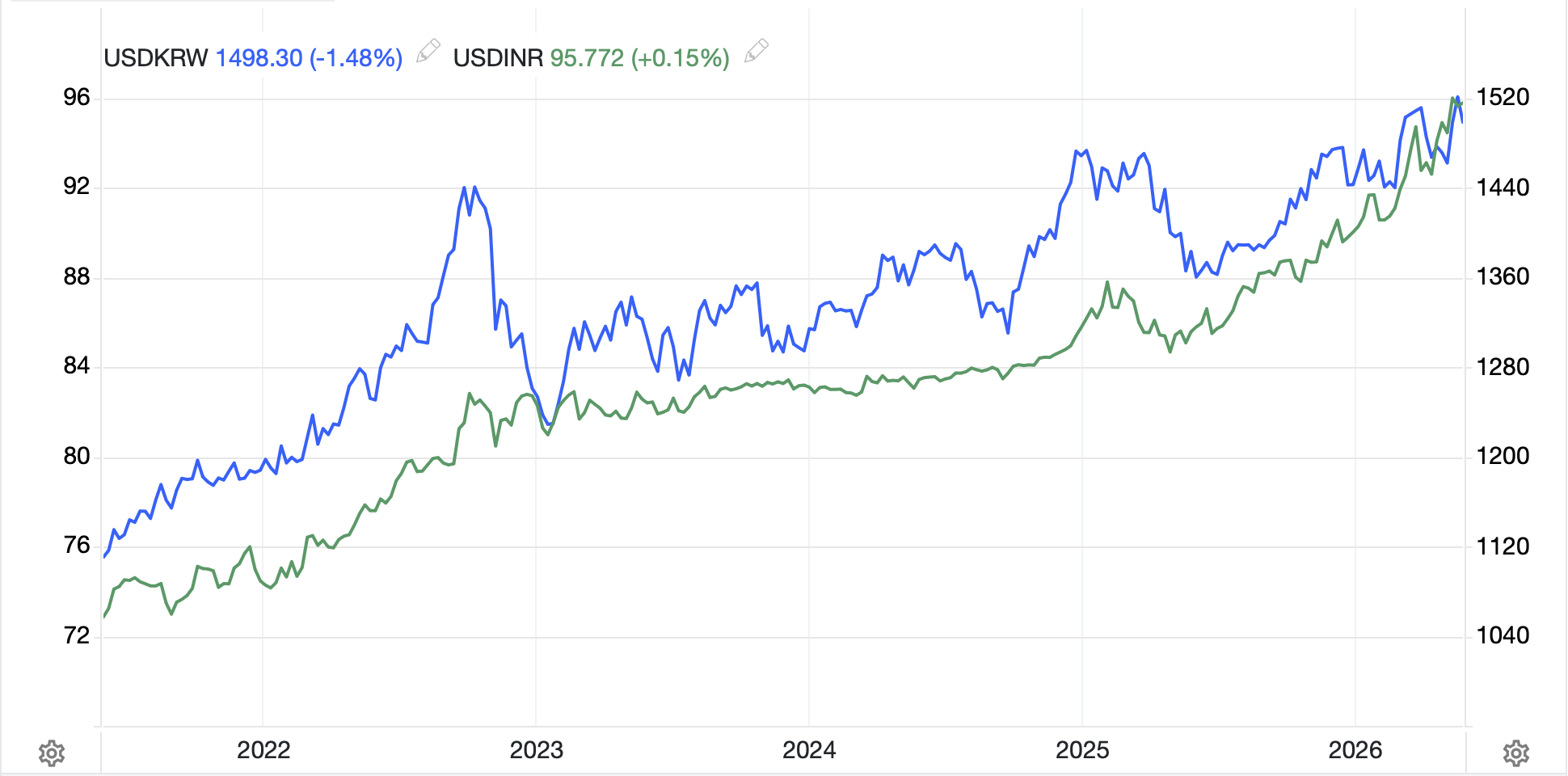

Now, there are currencies that have seen substantial movement over the past year, in both directions. For instance, both KRW and INR have been weakening consistently for the past five years, and this is despite a massive equity rally in both nations, although, in fairness, India’s market has not kept up over the past few months.

Source: tradingecoomics.com

At the same time, BRL has been broadly rallying vs. the dollar for almost 18 months, as per the below chart, as it remains a favorite in the hedge fund community for its high interest rates. And the fact that they continue to find more oil offshore is only helping things.

Source: tradingeconomics.com

But these currencies are secondary in the FX market, which has generally been dull.

Meanwhile, the oil story appears to be one of increasing belief that a deal is going to be done soon. This morning, WTI (-3.7%) is falling again and back to $90/bbl. Obviously, this is higher than where things were before this all started, but if there really was a shortage of the stuff, I expect prices would be much higher. From what I have read this morning, the two sides continue to talk with Iran looking for a release of frozen financial assets while the US still wants the nuclear material.

To me, the interesting thing is the tone of the comments from both sides. President Trump continues to highlight the positive view of a deal coming, although assuring us he won’t make a bad deal. Iran, though, continues with its apocalyptic rhetoric, threatening extremely painful revenge for every US action, although not really doing much at this point. It appears to me that both sides are speaking to the domestic audience, not each other. Trump needs to show progress and a victory, however defined, is near. Iran needs to show they are strong and will not be beaten by their sworn enemies. But at this point, I think both sides really need this to end. The fact that Iran is now talking about money is the tell. They know they are just about broke, and if there is no money to pay their armies, will their armies fight for the leadership? I maintain my July 4th deal timeline.

And that’s really today’s market story; oil’s slide is supporting other markets as we all await the end game. Elsewhere in the news, there is far more excitement over the NY Knicks winning the NBA’s Eastern Conference than there is over the political stories of primary elections which are ongoing around the country. While the mid-term elections are coming up in less than six months, the fields are not yet set, so it is difficult to handicap.

On the data front, there is little of note today in the US although we do hear from several more Fed speakers. But I maintain that their comments, today it is Governors Cook and Jefferson, are largely irrelevant and that can best be seen by the fact that the WSJ barely mentions any of their speeches anymore. They are no longer newsworthy. These two, though, will be an interesting case as both are avowed doves, but also hate President Trump, so will they vote with their belief set (rates should always go lower) or with their politics (Trump wants lower rates so they cannot vote that way)? I guess we’ll find out in a few weeks at the next FOMC meeting.

One aside on central banking was last night the RBNZ met, left rates on hold at 2.25%, but were more hawkish than anticipated in their comments indicating rate hikes were coming. This did help NZD to rally nearly 1%, an outlier in today’s market.

And that’s really it, I think. Until the next headline on Iran, I cannot see a reason to trade in anything.

Good luck

Adf