Tomorrow we’ll hear from the Fed

With pundits not sure where they’ll tread

Some call for a hike

So, Warsh can out psych

Inflation that seems far from dead

But others claim hikes he will thwart

Awaiting the task force report

With oil retreating,

Though some call it fleeting,

The hawks he will likely abort

The one thing we cannot forget

Is all of the outstanding debt

A hike may create

A weaker growth rate

An outcome he’ll surely regret

Let us turn out attention to the FOMC meeting which begins today and culminates in tomorrow’s policy statement and then the press conference that ensues. On the whole, I would say that Chairman Warsh has already achieved a key objective, market uncertainty about the outcome. A point I have been making for a very long time is that uncertainty is what creates an anti-fragile market as positioning is inevitably reduced, and more importantly, so is leverage. And this is true in every market. While there may have been value in forward guidance at the onset of the GFC such that the Fed wanted to calm markets down, that time is long past.

Interestingly, perhaps the one individual who is unhappiest is Nick Timiraos at the WSJ, the former Fed whisperer. He exhibited great power in the market because he was seen as former Chairman Powell’s mouthpiece when Powell wanted to convey information without being directly attributed. However, it appears that there will be no Fed whisperer in a Warsh Fed, although I suspect even if there is someone, it will not be Powell’s man to whom Warsh turns. So Timiraos is on the outs anyway. But you can tell how unhappy he is by the tone of his recent articles like the one last night trying to insinuate that Warsh will not get his way.

At the same time, Bloomberg has an article this morning explaining how Citadel Securities’ chief economist is expecting a hike. In my opinion, this is how it should be. Wall Street economists and analysts make enough money that they should be able to do the work themselves and have their own opinions, not merely regurgitate what they hear from the Fed speakers. (After all, I make no money and have opinions!)

Reiterating my view quickly, I do not see a hike for the following reasons:

- Recent data releases point to cooling inflation offering a respite on concerns of runaway prices

- Delaying any action until the task forces complete their work and help reset the way the Fed approaches things feels like the goal

- The Federal government cannot afford a rate hike as they migrate more and more issuance to the short end of the curve that will directly be impacted.

The counter view basically revolves around the idea that Warsh can ‘earn’ market credibility by hiking now, whether or not it is a policy error. I don’t think he is concerned about losing credibility at this stage and has set the table, via the task forces, to show he means business when it comes to changing the Fed. We all find out tomorrow.

As traders await all the news

On earnings, it seems there are views

That AI is losing

Its luster and cruising

Toward outcomes where stocks sing the blues

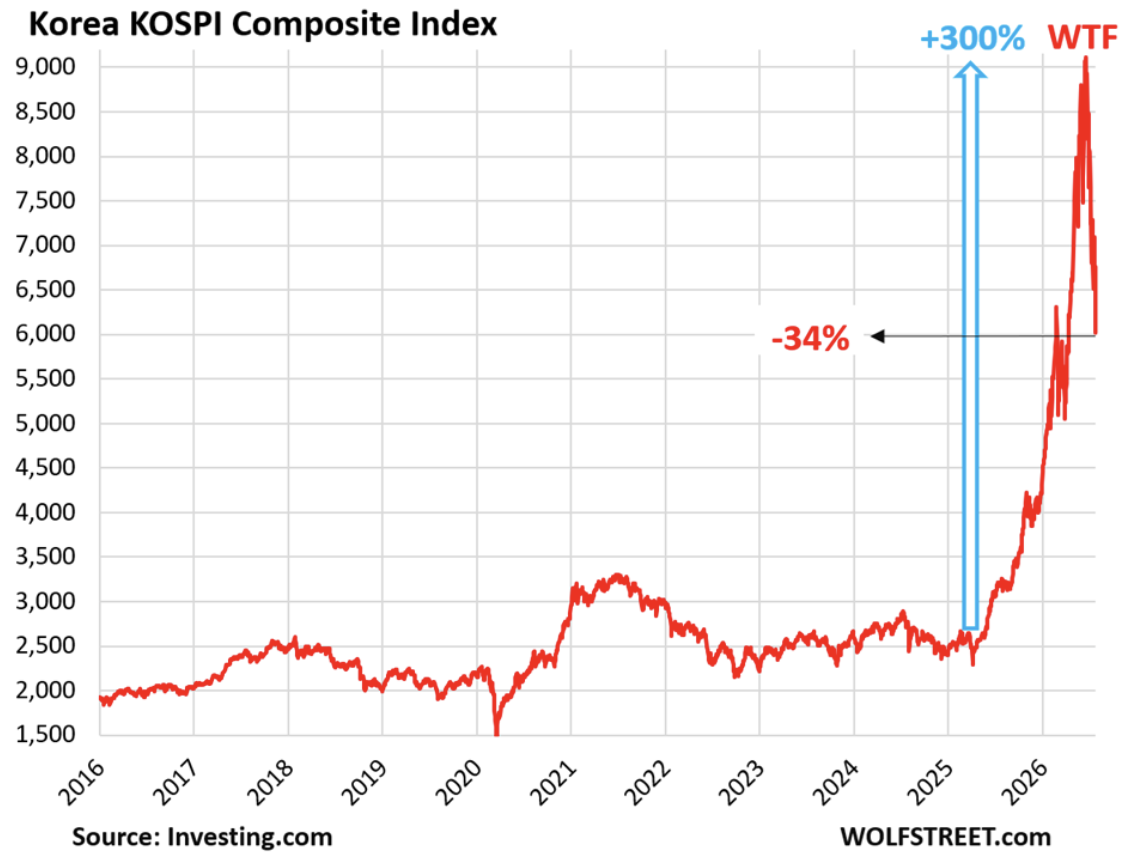

In my discussion about parabolic markets yesterday, I mentioned the Korean KOSPI index but after last night’s price action, I think a picture is in order. This from wolfstreet.com.

As I explained, parabolic moves do not end in a range, they fall like the chart above with pullbacks greater than 50% the norm. This implies that the KOSPI is not done yet, and given the KOSPI is basically two stocks, Samsung and SK Hynix, both of which are major semiconductor manufacturers, it doesn’t speak well to the semiconductor space in the US either. Tomorrow, we hear from MSFT and META and then Thursday we get AAPL and AMZN earnings reports. My take is much is riding on these earnings reports as any indication that growth is starting to slip will feed into my discussion yesterday regarding the second derivative and how that is the driver. In fact, we saw the announcement yesterday by Nvidia that they were guaranteeing $250 billion of debt for OpenAI to build a new datacenter in Ohio. At cycle ends, the pace of activity tends to increase as the players want to get things done before the collapse. I fear that is what we are watching.

Ok, let’s look at markets. As I’ve already touched on the KOSPI, which fell -10.8% last night, it is not surprising that most of the rest of Asia had a rough go as well. Tokyo (-4.0%), Taiwan (-4.65%) and China (-2.8%) were the biggest losers overnight although HK (+0.4%) managed to eke out some gains. In fact, looking across the region, away from the big three mentioned above, it was a more mixed picture. Indonesia (-0.9%) is having its own problems as the central bank governor resigned and there have been numerous scandals and other cabinet resignations lately undermining both the rupiah (-0.1% and back to multidecade lows) and the stock market there.

As to Europe, given they have no tech sector and the tech sector is the area under the most pressure, I guess we should not be surprised that bourses there are modestly higher this morning, mostly up around +0.3% across the board. A very pleasant experience compared to the gyrations seen elsewhere. And US futures at this hour (7:10) are mixed with NASDAQ (-1.1%) suffering while the DJIA (+0.5%) is fine and the SPX is caught in the middle, basically unchanged.

In the bond market, yields continue to edge lower, with Treasuries (-3bps) leading the way and European sovereign yields all lower between -1bp and -2bps. UK gilts (-3bps) are also performing well as the market awaits the BOE’s policy decision on Thursday. Then JGB yields (-2bps) have slipped in concert as the market awaits the BOJ decision Friday. At this point, consensus across the board is for no movement, although there has been a discussion regarding the BOJ with some analysts believing a hike is possible.

Turning to commodities, oil (-1.6%) is not the center of attention today for once, and is pushing back toward $80/bbl. The ongoing decline appears to be based on comments that diplomacy is once again being tried to resolve the Iran situation and the Strait of Hormuz. Perhaps more surprisingly the metals markets are also falling this morning (Au -1.3%, Ag -2.2%, Cu -1.1%) as their inverse relationship with oil is being tested.

Finally, the dollar is ever so slightly firmer this morning, but mostly on the order of 0.1% or 0.2%. AUD (-0.4%) is the worst performer in either G10 or EMG blocs as central bank comments led to a reduction in the probability of a rate hike there next month. One other thing to note is USDJPY, where, as I type, the market is trading at 163.92, a scant 8 pips from the next big, round number at 164.00, a level almost touched last Thursday (163.99 was the high) but when it trades, it will almost certainly be hailed as an important milestone regarding potential intervention. I don’t agree with that assessment.

Source: tradingeconomics.com

Again, a key feature of BOJ intervention has been an effort to address a volatile market, but as you can see below, while the direction of travel has been consistent, the only volatility has come from BOJ interventions. Everything else is a slow, steady deterioration of the yen.

Source: tradingeconomics.com

On the data front, there is plenty upcoming this week in addition to the Fed, including PCE on Thursday.

| Today | Goods Trade Balance | -$100.0B |

| Case-Shiller Home Prices | 1.3% | |

| Consumer Confidence | 92.3 | |

| Wednesday | FOMC Decision | 3.75% (unchanged) |

| Thursday | BOE Rate Decision | 3.75% (unchanged) |

| Initial Claims | 200K | |

| Continuing Claims | 1800K | |

| Q2 GDP | 2.1% | |

| Personal Income | 0.3% | |

| Personal Spending | 0.3% | |

| PCE | -0.1% (3.7% Y/Y) | |

| Core PCE | 0.2% (3.3% Y/Y) | |

| Friday | BOJ Rate Decision | 1.0% (unchanged) |

| Employment Cost Index | 0.8% | |

| Chicago PMI | 56.0 | |

| Michigan Sentiment | 54.0 |

Source: tradingeconomics.com

Obviously, the FOMC meeting will be the big story along with the earnings data, although I imagine that the PCE data may garner some interest for now, at least until we learn what measures of inflation the Fed is going to use going forward. My fear is the equity market can crack, for now, and that will drive overall trading activity. As to the dollar, I see no reason for a large move in either direction until we see new policies.

Good luck

Adf