Stories about yen

Have multiplied like rabbits

Is it really news?

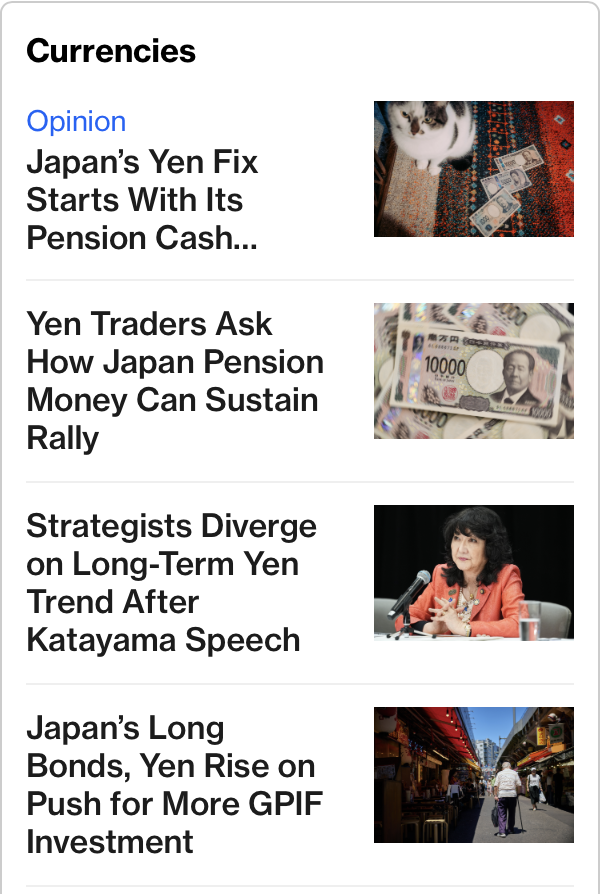

You know it has been a slow session when the yen’s movement, as seen in the chart below, was enough to draw 4 headline stories in Bloomberg.

Source: tradingeconomics.com

And here is a screenshot of the 4 headlines on Bloomberg.com

While it may look dramatic on the screen, that almost one yen move represents less than 0.6%, and as you can see, about half of it has already retraced. The underlying premise is that FinMin Katayama, in a regular speech about general things, suggested that the GPIF (Japan’s national pension fund) ought to consider investing more assets in Japan and JGBs rather than internationally. The idea is that if the GPIF changes its investment mix, so will many other Japanese institutional funds, and they do have a lot of money there, upwards of $2 trillion equivalent. This is not to say that they are going to invest all their money back home, just that the mix could change somewhat.

Now, if they were to do this, it would certainly have an impact on both the FX and global bond markets, with the yen likely to strengthen along with JGB prices (hence JGB yields declining) and potentially Treasury yields rising as a key buyer of US debt would reduce its appetite.

But this is just a suggestion, and one that has been made numerous times in the past with no further action. At the same time, yesterday’s US 30-year Treasury auction was extremely well-received with more than 77% indirect bidders. That statistic is generally seen as foreign investors and central banks. With the yield coming at 5.058%, it is not surprising that foreign bidders, especially the Japanese, would have significant interest. After all, their currency continues under pressure, so if the GPIF holds Treasuries, in yen terms they look better almost every day.

The other spate of stories this morning was about the carry trade, and how Goldman Sachs has just explained to its clients that the carry trade, notably shorting yen to hold dollars, amongst other things, is an excellent risk reward trade right now. I’m guessing Katayama-san didn’t really want to hear that.

My larger point, though, is that despite the yen (+0.4%) having moved a relatively modest amount, it certainly garnered a lot of attention. In other words, there’s not much else to discuss.

Since Warsh and his minions last met

The question was who they would vet

To lead the task forces

Young Turks? Or warhorses?

Alas, tis the latter quintet

The other moment of excitement yesterday came from the Fed when they released the names of the leaders of each of Chairman Warsh’s five task forces. The list is linked here. It certainly did engender a lot of discussion with different analysts taking different views, and while I have some opinions, mine are no more useful than anybody else’s as they are not going to change things. My observation, though, is that there is an awful lot of old school thinking represented by the list, which is somewhat disappointing for those of us who were looking for a new direction from the Fed. As an example, Mervyn King, ex-BOE governor, and active participant in forward guidance, seems unlikely to offer many new views on communications. But that is what we have. Hopefully some new thinking will come about.

And that’s all there is regarding news, I think so let’s turn to market activity. Under the theme, you can’t keep tech stocks down, yesterday’s US equity rally was followed by more strength (Tokyo +1.2%, HK +0.6%, Korea +2.5%, India +1.1% and Australia +0.5%) than weakness (China -2.0%, Taiwan -0.8%) in Asia. The rest of the smaller regional exchanges were largely higher as well. Arguably, the fact that whatever is happening in the Strait of Hormuz, oil prices have no strong bid, is part of that investment thesis. As to Europe, other than Spain (+0.5%), the rest of the continent and the UK are all +/-0.1%. And US futures at this hour (7:15) are showing softness in the NASDAQ (-0.5%) but otherwise not much movement.

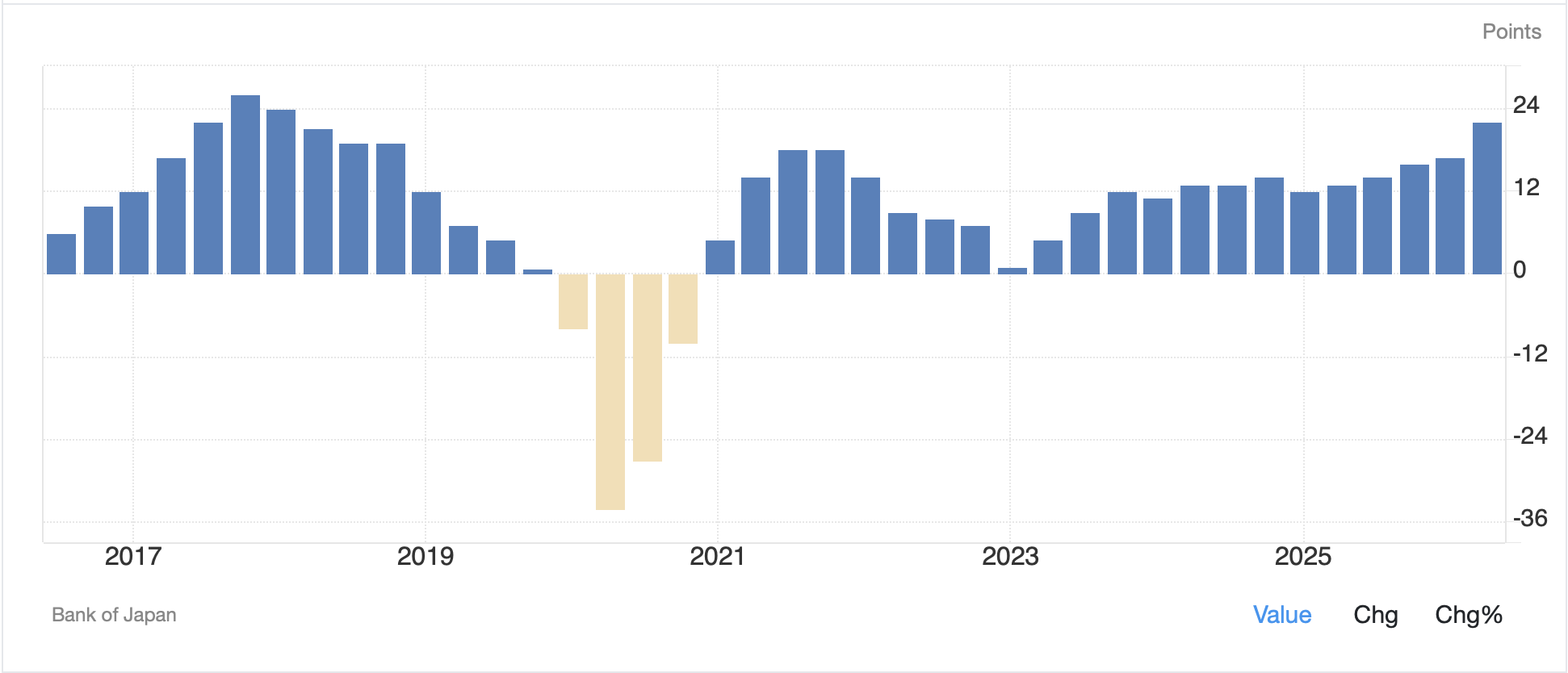

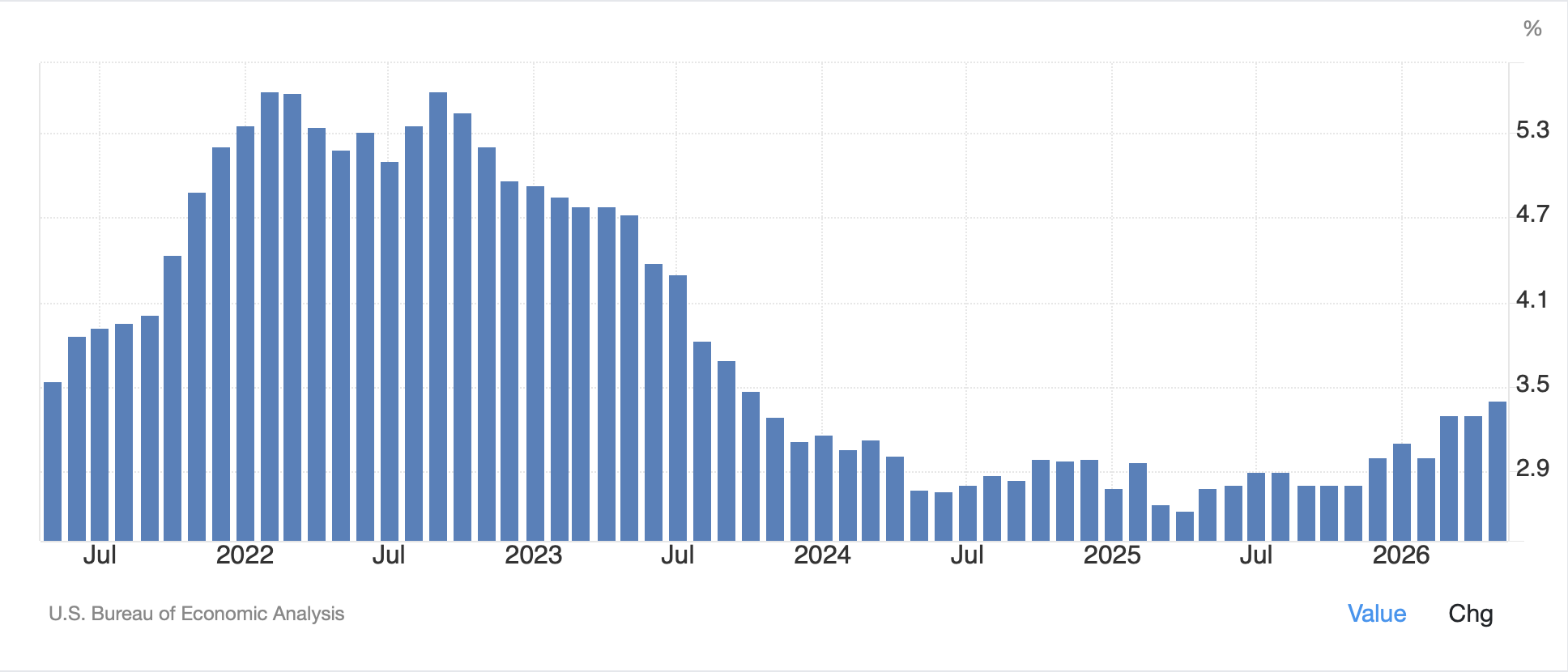

Bond yields, though, are uniformly lower, backing off their recent test of 4.60% in 10-year Treasuries, as now that the auctions have passed, I think a lot of the short positioning into those auctions has been covered. If oil continues to trade either side of $70/bbl, it is hard to make the case inflation will be running away. So, Treasuries (-2bps) continue to back off while European sovereign yields have slipped by a similar amount. The outlier was the JGB market (-13bps) which as you can see in the below chart has really changed vs. its following of Treasury yields, entirely on the GPIF story.

Source: tradingeconomics.com

In the commodity space, oil (+0.3%) continues to erase the gains seen Tuesday after the increase in military activity in the Strait. Even though that seems to be ongoing, the markets just don’t care.

Source: tradingeconomics.com

As to the metals, yesterday’s gains are being moderated with both gold (-0.4%) and silver (-0.7%) slightly softer while copper is unchanged on the day.

Finally, the FX market, away from the yen, remains generally uninteresting. Three weeks ago, much was made of the DXY’s break higher from a longer-term range as it traded through 100.50, almost reaching 102.00. but as you can see in the chart below, for now, that excitement seems to be fading with a nice little downtrend developing since June 24th.

Source: tradingeconomics.com

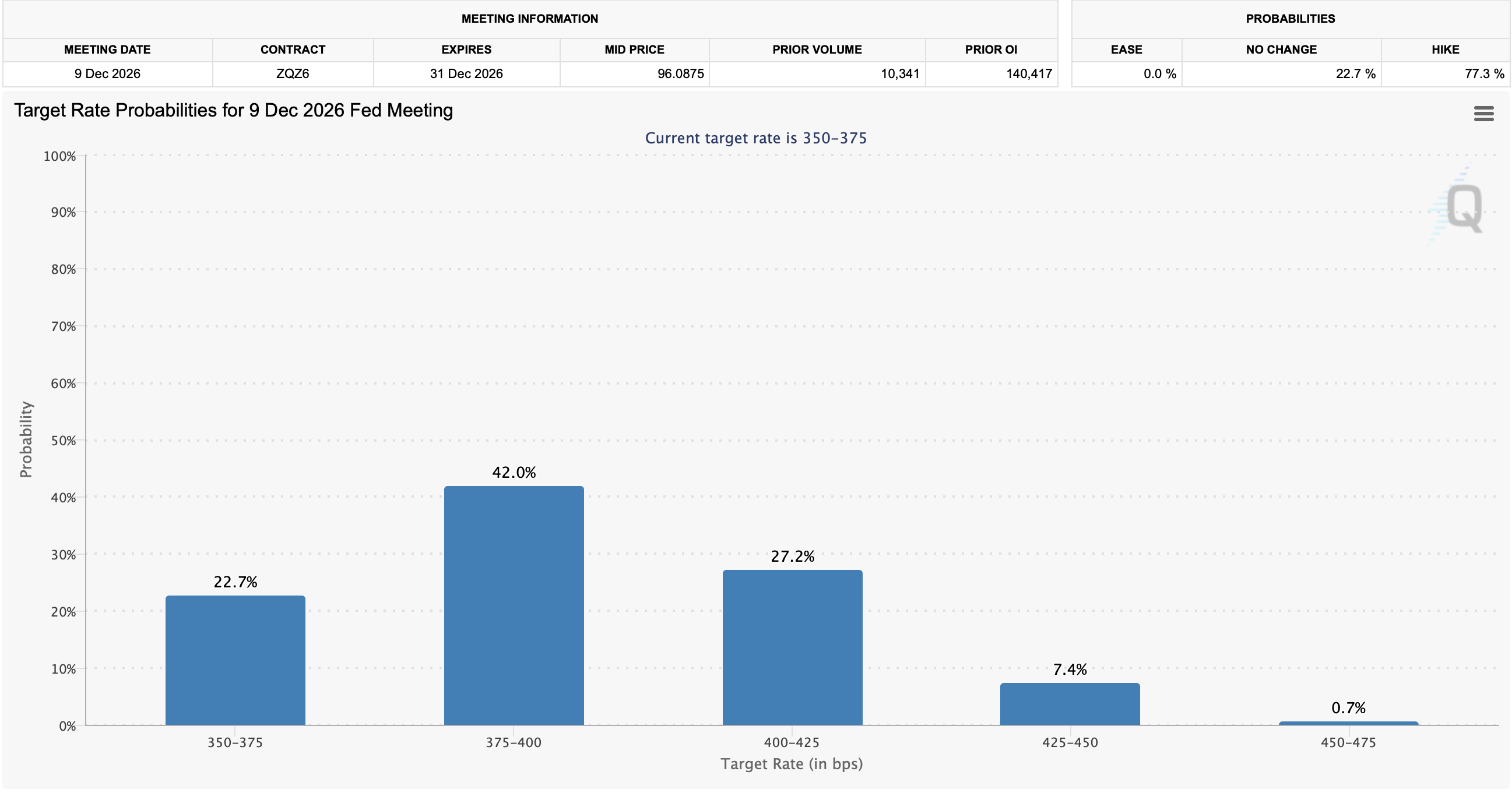

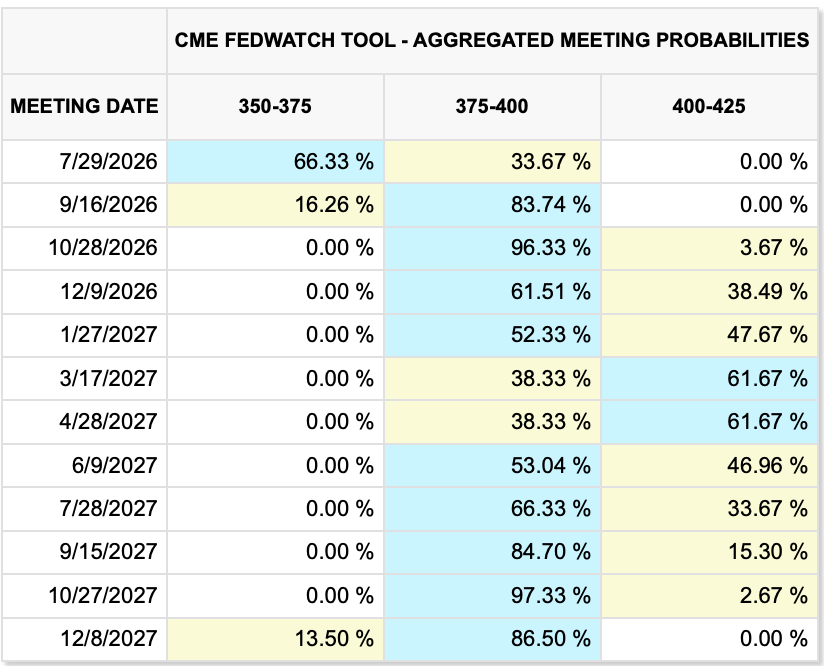

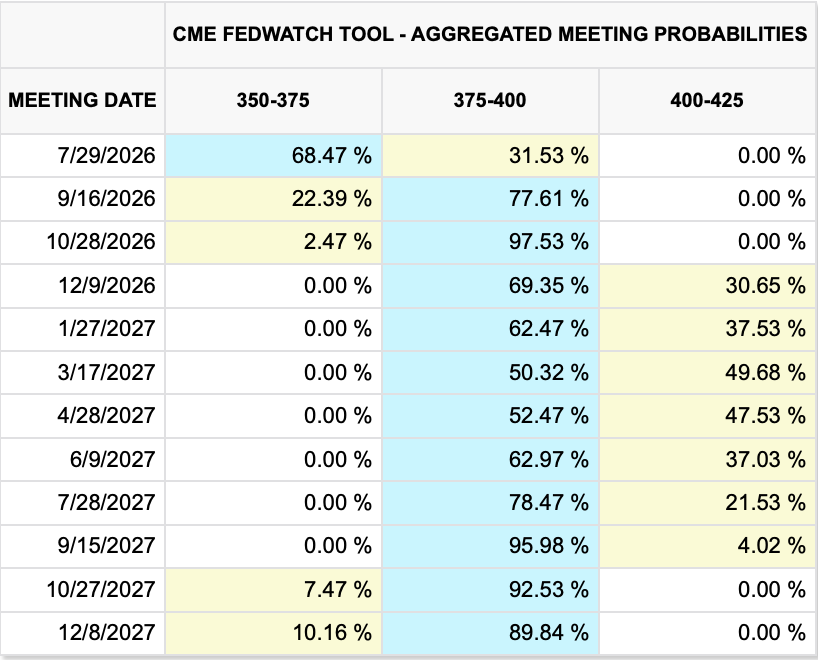

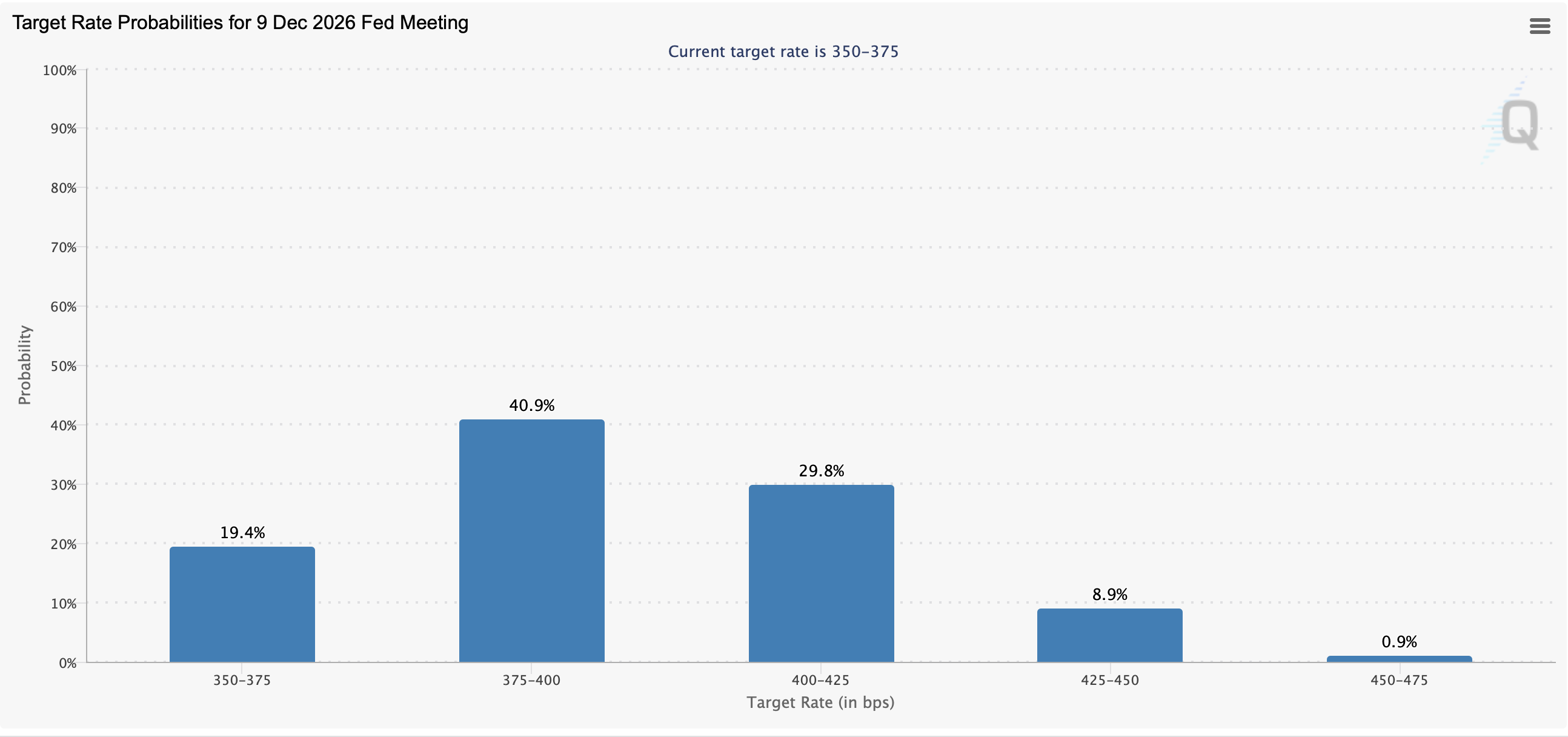

In these dog days of summer, it is hard to get too excited. Generically, while I remain in the camp that the Fed will not adjust rates this year, and so the market will need to reduce the current 33bps of rate hikes priced into the Fed funds futures curve as you can see below, I also think that ongoing inward investment into the US is going to underpin the dollar over the medium term.

There is no data to be released today, and yesterday’s numbers saw a marginally better Initial Claims number (215K vs 218K expected) and a slightly worse than forecast Existing Home Sales number. As well, we heard from NY Fed president Williams who said his new main concern is that demand for AI infrastructure is going to drive inflation higher and he is wary of that. Of course, that is exactly at odds with Chairman Warsh’s view that AI is going to reduce inflationary pressures. Next week, Chairman Warsh will be testifying to Congress and there are four other Fed speakers, but my take is that over time, we will hear less and less from the rest of the Committee. (Or maybe that is just wishful thinking on my part!)

At any rate, it is shaping up to be a quiet one, so close up early and take a long weekend, you’ve earned it!

Good luck and good weekend

Adf