Seems Jay is a narcissist too

Refusing to leave when he’s through

He claims he won’t try

To stop the new guy

But sticking around is the clue

Meanwhile, in his last vote as Chair

The poll, for his views, didn’t care

As one wanted cuts

And three said that’s nuts

Seems politics is in the air

Starting with the FOMC meeting, as universally expected, they left policy on hold with the Fed funds rate target 3.50% to 3.75%. However, in an extension of the last meeting’s three dissents, this time there were four, so the vote was 8-4 to leave rates on hold. However, that seems a bit disingenuous to my eyes, as while Governor Miran wants a 25bp rate cut, as he has said all along, the other three ‘dissents’, regional presidents Hammack, Kashkari and Logan, “did not support inclusion of an easing bias in the statement at this time.”

However, after having read the statement numerous times, I challenge anyone to highlight where they expressed an easing bias. Here is the exact wording:

Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have remained low, on average, and the unemployment rate has been little changed in recent months. Inflation is elevated, in part reflecting the recent increase in global energy prices.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Developments in the Middle East are contributing to a high level of uncertainty about the economic outlook. The Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 3‑1/2 to 3‑3/4 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

But that is the narrative. Of course, the fact that there were four dissents led to much tongue wagging by the narrative set with some claiming that Powell had lost the room, while others claimed that this is a warning to Warsh that he will not be able to get his way.

During Warsh’s nomination hearing, one of the things he discussed in terms of the institutional changes necessary, was that there needed to be less communication by FOMC members as it didn’t do anything to help the process. I heartily agree with this approach, and perhaps this was all the regional presidents, who are looking ahead and seeing that they will not be able to move markets anymore, certainly a heady feeling I’m sure, trying to stake their turf.

Meanwhile, Chair Powell, the arch traditionalist as we have been told, will be breaking with tradition and remaining on the board in his governor’s role after his chairmanship has ended, although he claims this is to ensure the institution remains protected from politics. (🤣🤣🤣🤣🤣🤣🤣🤣🤣). Whatever. I am willing to wager that Mr Powell is a consistent dissent as long as he is on the board.

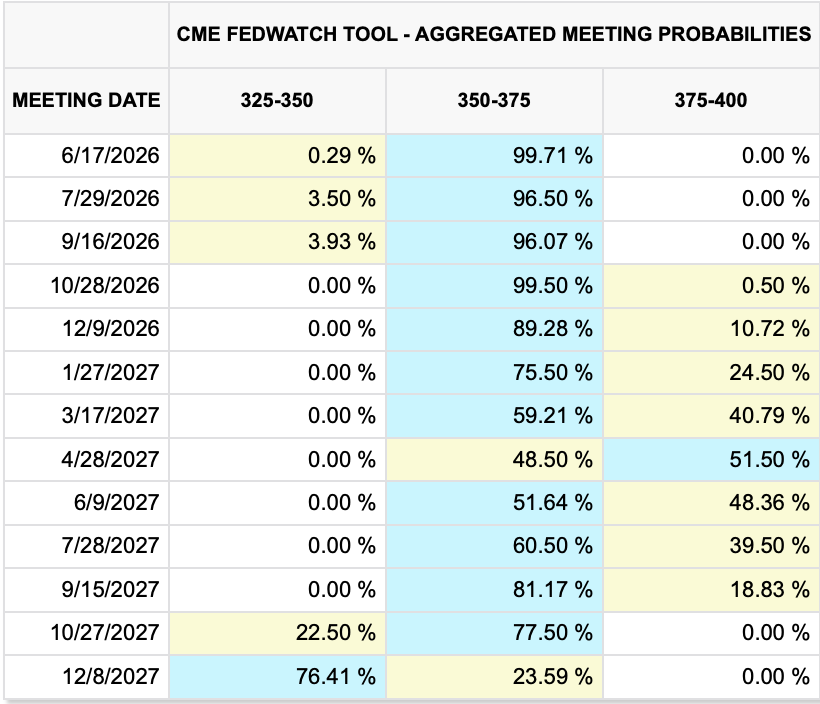

In the end, no policy changes were expected nor forthcoming. As of the close of yesterday’s session, the Fed funds futures market looks like this:

Source: cmegroup.com

Basically, market participants do not believe the Fed is going to do anything for nearly the next two years. I hope they are right!

Remember Monday?

Ueda explained…nothing

That’s what the yen heard

Early this morning

Katayama, with a smile,

Hinted at bold action

Monday’s BOJ meeting resulted in no policy changes, as was widely expected, but Ueda-san perfectly illustrated the futility of central bank chiefs trying to guide markets with their words instead of deeds. Basically, he fumbled around exhibiting no commitment to anything. And, one look at the chart below shows that traders continued to sell the yen in the wake of the BOJ meeting on the 28th. However, traders are nothing if not attentive to signals and while it took her a little while, Japanese FinMin Katayama livened things up a bit after Tokyo markets closed as follows [emphasis added]:“We are nearing the point where bold action on exchange rates will be necessary,” and more entertainingly, “I just want to remind everyone: whether you’re traveling or taking a break, don’t put down your smartphone.”

Source: tradingeconomics.com

One of the problems for them is that we are coming to Golden Week, with the first of the holidays already past yesterday. But Friday through next Wednesday are all Japanese holidays with no markets open. On the one hand, lack of liquidity can suit the BOJ as any intervention may have a much larger than normal impact. On the other, holiday activity is very rare. The term ‘bold action’ is, I believe, step 6 in the 7 steps to intervention and as you can see from the above chart, traders are listening. The problem Katayama and Ueda have is that the fundamentals remain negative for the yen. Is it really speculative to respond to weakening Japanese economic data that is worsened by the current energy situation vs. surprisingly strong US economic data where the energy situation is a benefit for the US?

If history is any guide, the dollar is likely to trade below that 160 level for a little while as traders may not want to test things during the Golden Week lack of liquidity, but ultimately, I suspect that dollar can push higher and the BOJ will be in. Their problem, though, is fundamental, and until the fundamentals change, the yen will be under pressure.

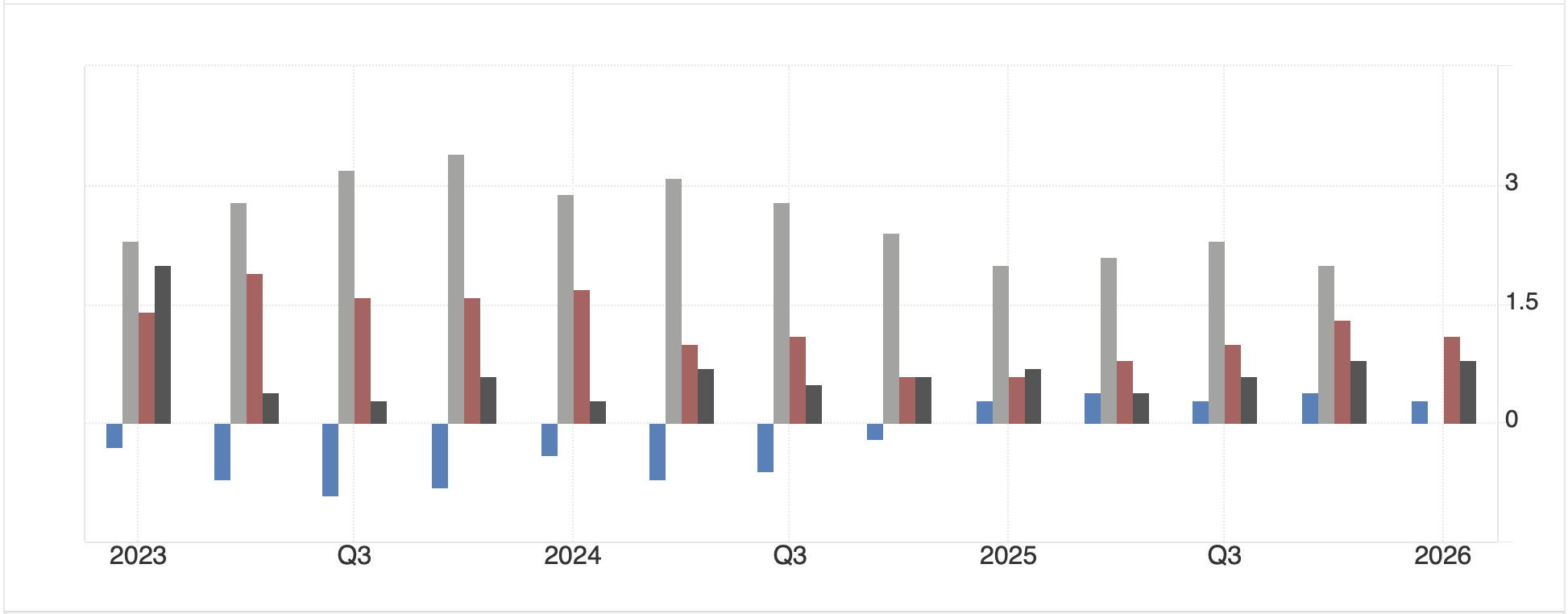

Speaking of fundamentals, let’s take a quick look at GDP figures and ask ourselves about the prospects for currencies in the future. The below chart from tradingeconomics.com shows annual GDP for the US (grey bars), Germany (blue bars), France (red bars) and Italy (black bars). See if you can tell the difference! The US number for Q1 is to be released this morning and expected at 2.3%.

Yesterday’s US data surprised on the high side with strong Durable Goods and Housing data. This follows stronger than expected Retail Sales data as well, which is the opposite of the situation in Europe. In fact, a look at the Citi Surprise Index below shows just how surprisingly bad things are in Europe relative to the US.

Again, please explain to me the case for the euro’s strength.

Ok, on to markets. Bonds were the big tell yesterday as yields in the US rose sharply, up 8bps at their peak, although have since retraced -3bps to 4.40%.

Source: tradgineconomics.com

While that is not the highest yield we have seen since the war began, it is near the upper bound, but I suspect that has more to do with the fact that the US economy, as demonstrated above, is anything but weak right now. Maybe the dollar should be considered a petrocurrency going forward! European sovereign yields tracked Treasury yields and this morning, they too are lower by between -2bps and -4bps. One noteworthy aspect is that ahead of the BOE meeting this morning, 10-year Gilt yields are above 5.0% for the first time since 2008, higher even than during the Liz Truss inspired liability management crisis.

Of course, the other thing weighing on bonds is the oil price (+0.1%) which while it is little changed this morning has climbed steadily and is higher by nearly 12% in the past week. The entire discussion here is about the naval blockade and whether it will be able to force Iran to capitulate soon. Certainly, President Trump is doing all he can to apply increased pressure on the Iranians with more secondary sanctions on all the banks that have surreptitiously handled Iranian money in the past. WTI remains below the spike highs from the first night of the war, but it has been climbing steadily of late. There is no doubt that there has been material damage done to the oil infrastructure in the Middle East and it will take time to repair once the fighting is done. As the blockade continues, it appears some of that destruction is being priced in. However, with the UAE out of OPEC and Venezuela likely to leave as well, there will be a race to see who can pump oil fastest. I remain convinced that there is a firmer cap than floor over time.

Perhaps the biggest surprise today is that gold (+2.0%) and silver (+3.2%) have rebounded sharply despite oil’s continued rally. That inverse correlation had been quite strong, although I continue to have a difficult time understanding its underlying cause. Nonetheless, commodities across the board are in demand today.

In the equity markets, yesterday’s US performance was lackluster ahead of the big earnings releases, two of which were quite strong (GOOG and AMZN) while two were less optimistic (MSFT and META). Asian markets were broadly negative as rising oil prices continue to weigh on the region with the Nikkei (-1.1%) and Hang Seng (-1.1%) leading the way lower amid mostly poor outcomes throughout the region. Only Singapore (+1.1%) and New Zealand (+1.0%) managed to buck the trend, after better-than-expected PMI data. Meanwhile, in Europe the picture is mixed with France (-0.5%) and Spain (-0.3%) softer while Germany (+0.3%) and the UK (+1.0%) are in better shape. The BOE just announced no policy change but seemed to sound more hawkish as they are going to try to use monetary policy to prevent higher oil prices. Historically, that has been a catastrophic central bank error, but I will not be surprised if they go down that road. As to US futures, at this hour (7:15), they are pointing higher across the board by between 0.3% and 0.6%.

Finally, the dollar is softer this morning, with the yen (now +2.0%) leading the way, although that is hardly a dollar story and decidedly limited to the yen. But, vs. the G10, the greenback is universally softer (EUR +0.3%, GBP +0.35%, AUD +0.6%, CHF +0.7%). Frankly, this doesn’t make sense to me, but markets will do that to you. Versus the EMG bloc, the dollar is also softer across the board with KRW (+1.0%) the leader as it follows the yen higher, and the rest of the block showing gains of between 0.25% and 0.5%. I still stand by my view that the dollar benefits over time, but apparently not today.

And while I fear I have gone on too long already today, there is a lot of data coming out as follows: Personal Income (exp 0.3%), Personal Spending (0.9%), Q1 GDP (2.3%), PCE (0.7%, 3.5% Y/Y) and Core PCE (0.3%, 3.2% Y/Y), Initial Claims (215K), Continuing Claims (1820K) and then later this morning, Chicago PMI (53.0) and Leading Indicators (-0.1%). With the Fed ostensibly showing a hawkish bias, all eyes will be on the Core PCE data. But really, my take is the combination of position liquidation in the yen and the twists and turns in the war are going to be today’s drivers. While you cannot catch a falling knife, I do see this dollar downtick as quite temporary.

Good luck

Adf