There’s something that doesn’t make sense

As stock market rallies commence

While word from the Strait

Just doesn’t look great

And politics worldwide is tense

Can every investor ignore

The risk of a much longer war?

Or will, sometime soon

They sing a new tune

And sell stocks whose risks they abhor?

One must be impressed with the way markets, in general, have handled the disruption caused by the ongoing conflict in Iran and the Persian Gulf. The insouciance with which it appears most investors are treating the situation is remarkable. There seem to be endless ways in which this can result in much greater damage to the global economy, mostly related to the impact on energy and food production going forward. You’ve all heard the numbers, I’m sure, about the 20% of daily oil and LNG that traversed the Strait of Hormuz prior to the war. Less well known was the amount of sulfur (~44% according to Grok) and nitrogen fertilizer (~30%-35% according to Grok) that regularly transited the Strait and has now been stopped.

The latter two matter greatly for global food production, but also for mining as sulfuric acid is a key part of almost all metals mining operations. Too, one-third of global helium supplies went through the Strait, and that is critical in semiconductor manufacturing.

The point is, if the conflict continues for too much longer, it is quite possible, if not probable, that parts of the global economy could be impaired for a much longer term with real negative consequences for economic activity. And while this may be a tail risk, the fact that the potential impact could be so large leads me to believe the market is underpricing potential damage from the war, at least economically. Last night, Alyosha posted a very interesting piece regarding potential consequences for the Gulf region as a whole as well as oil markets. His conclusion was that if things don’t end soon, there may be irreversible damage to the Gulf oil industry as well as the Gulf nations themselves as their cashflows are being completely starved for now.

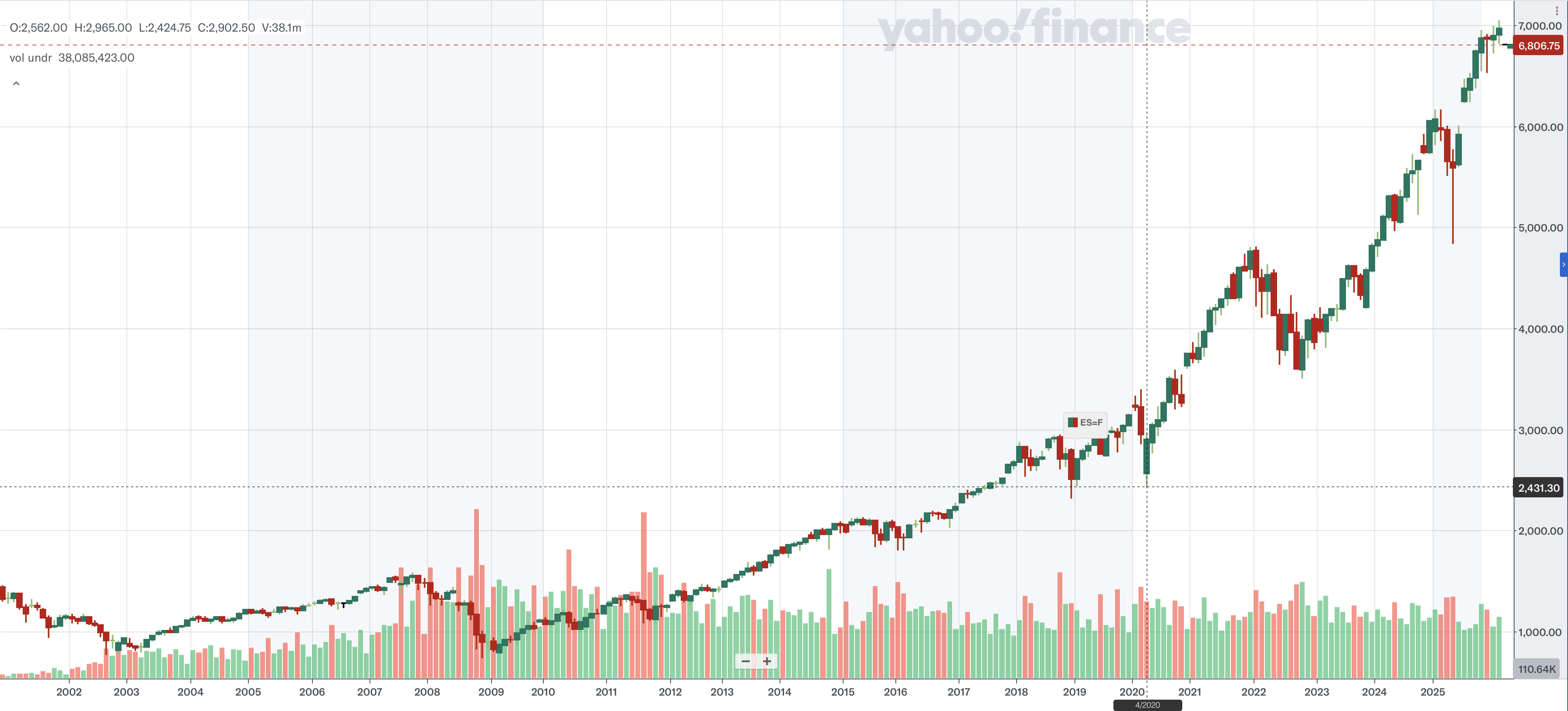

I know that doomsaying is a losing proposition with equity markets over the long run, as the century long trend shows human innovation continues to advance economic prospects and outcomes. But in the shorter term, interruptions of that trend are common and can be quite painful for those investing when they occur. Recall how you felt when Covid shutdowns resulted in a 30% decline in two months in early 2020, as per the below chart. How about the similar drawdown, along with the selloff in bonds, during 2022’s inflation led declines?

Source: finance.yahoo.com

All I’m saying is that markets can ignore things for a long time before suddenly repricing an outcome and I have a feeling that is what we are witnessing right now. So, as we head into today’s FOMC meeting, which seems unlikely to have any impact whatsoever, I would play things close to the vest and am doing just that myself.

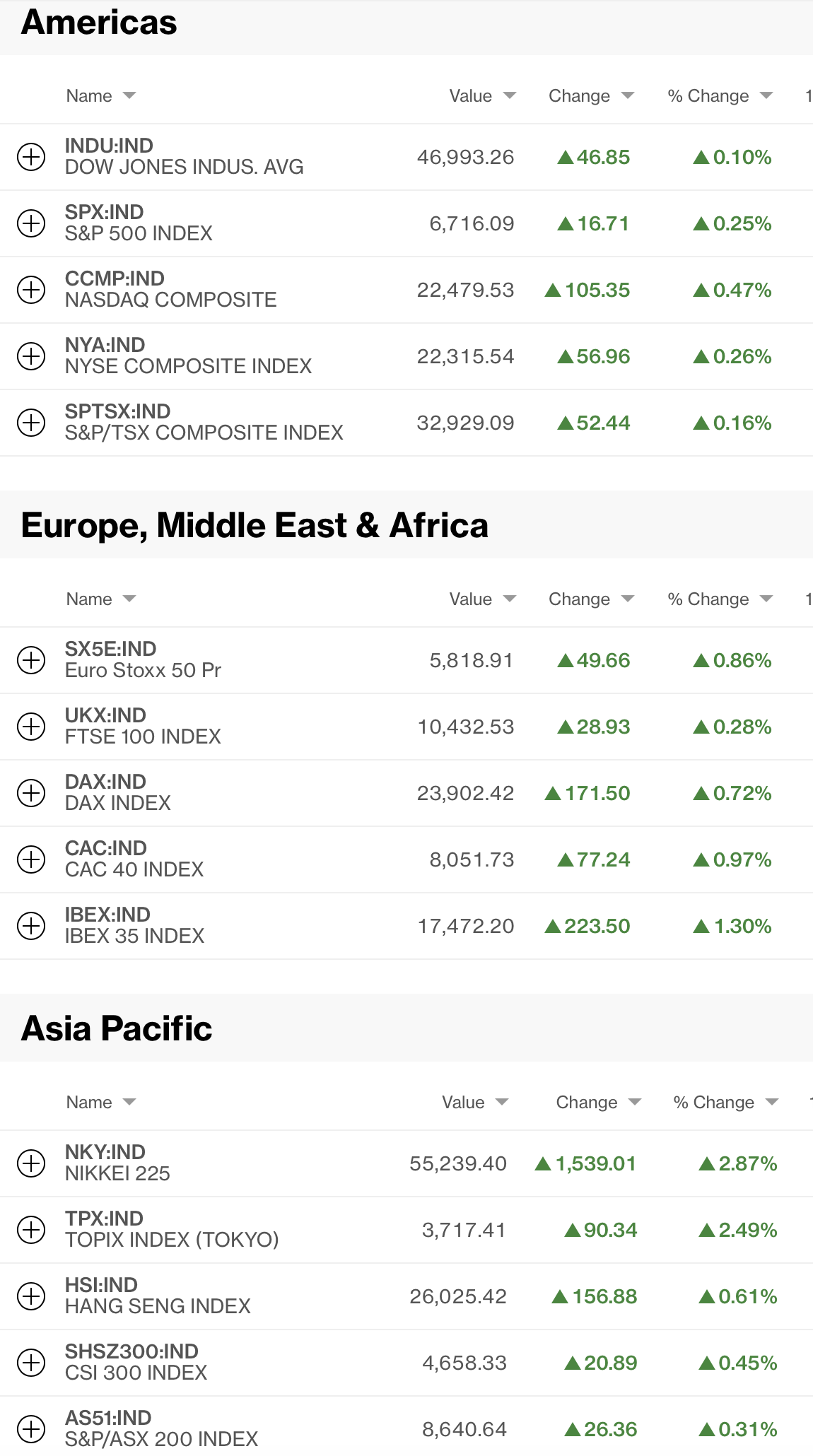

Ok, let’s tour the euphoria in markets, which remains puzzling to me. You have to search far and wide to find an equity index that fell in the past twenty-four hours and here is a Bloomberg snapshot of major indices at 7:10 this morning,

Literally, every market in Asia rallied, some excessively so, Korea (+5.0%) and I could only find two markets in Europe that are down this morning, Denmark and South Africa, both of which have slipped about -0.3%. Otherwise, it’s all green as prospects are, apparently, great. US futures are also higher as I type, up about +0.6% or so. Certainly, there is little concern about potential long-term consequences of this war.

In the bond market, yields everywhere are slipping again with Treasuries (-2bps) falling back into that longer term range, while European sovereign yields are lower between -2bps and -3bps and JGB yields fell -5bps. As per the below chart from tradingeconomics.com, we spent 5 days above the top of the trading range.

Perhaps the market is starting to price in a recession and much weaker growth, although with oil prices firmly above $95/bbl, inflation is coming, at least in the near future. Of course, the Fed response is going to be critical here, and while they will almost certainly make no policy changes today, all eyes will be on their forecasts via the dot plot and SEP. We shall find out at 2:00pm.

Speaking of oil (-1.7%), perhaps its new home is $95/bbl, not $100/bbl like I mentioned yesterday, but for now, there doesn’t seem to be urgency in either direction. The futures market remains in steep backwardation although in the US, there are ample supplies. So, while gasoline prices at the pump are up substantially, there is no rationing here in the US, nor I suspect, will there be given we are pretty self-sufficient on that front. But demand destruction can be real, as even though the short-term elasticity of demand for oil is limited, over time, substitutes will be found. In fact, this is the biggest risk for the Gulf nations, the idea that substitutes can be found and their key resource loses value. I don’t believe that is going to happen on any visible timeline, but stranger things have happened.

In the metals markets, gold (-0.9%) is slipping this morning, but remains right near that $5000/oz level and silver is unchanged, just below $80/oz. The price action in both precious metals and oil is remarkably similar, if offset by one month as metals spiked and dropped first, then found a new home in the middle of those extremes, and oil has done the same thing. You can see the similarities in the two following charts:

Source: tradingeconomics.com

Source: tradingeconomics.com

Finally, whatever people are doing in financial markets, FX is not part of today’s equation. The dollar is virtually unchanged vs. the euro, pound, yen, CAD or CHF. In the EMG bloc, +/- 0.2% pretty much defines the range of movement. There’s really no story here right now.

On the data front, we see PPI (exp 0.3%, 2.9% Y/Y headline and 0.3%, 3.7% Y/Y core) as well as Factory Orders (0.1%). The Bank of Canada will leave rates on hold this morning, and of course the Fed will do the same this afternoon. We also see the EIA oil inventory data with a small draw expected in gasoline and distillates but a crude oil build. Yesterday’s API oil data showed a 6.6-million-barrel build. As I said above, there is no shortage of the stuff in the US.

The uncertainties of war remain the market drivers, but as we frequently see, markets have relatively short attention spans. Absent a significant increase negative news from the Gulf (e.g. more Iranian destruction of other gulf assets) I’m not sure what will change this sentiment. And if something happens that reduces the conflict, the initial view will be extremely bullish I believe.

Good luck

Adf