The status is still very quo

As ships still cannot come or go

However, Iran

Proposed a new plan

With nukes as a part of the show

But thus far, whatever they said

Has not moved discussions ahead

So, oil’s crept higher

As traders require

More certainty ere fears they shed

While President Trump has announced a new plan to help escort ships trapped in the Persian Gulf through the Strait of Hormuz, thus far, none have taken the chance. Over the weekend, Iran ostensibly put forth another peace proposal, and this time their nuclear activities were part of the plan, a major change, although President Trump has rejected it overall. To me, though, this is major progress as it demonstrates that there is a negotiation ongoing.

My armchair analysis, FWIW, is that Ahmed Vahidi is watching his nation crumble and beginning to really feel the pinch of the US naval blockade as his revenues shrink rapidly. While there are many estimates of how long Iran can withstand a lack of revenue, and I have no idea what that answer is, I feel it is reasonable to assume that if he doesn’t have enough to pay his soldiers, many of them will simply go home. Already I have read reports that many of their payments to soldiers and proxies have been dramatically reduced as the US continues to tighten the financial screws via sanctions on banks and companies that have been acting as Iran’s middlemen. I believe it is widely agreed on all sides of the conversation that the Iranian economy has been virtually collapsing with the rial having fallen 95% in value, access to basic staples limited and suffering widespread.

The one thing of which I feel certain is that Vahidi wants to remain in power, and I would estimate as the pain increases, and the money stops flowing, his grip on power is slipping. Staying in power without nuclear weapons is likely much preferred to being deposed.

In the end, like every negotiation, the parties start far apart and get closer over time. Now, my view is likely not worth all that much, but the oil market’s view is worth billions of dollars and if we look at how the price of oil has behaved, while uncertainty remains, (especially after a report this morning that Iran fired on and struck a US naval vessel, although that report has been denied), the market does not appear to believe that this is going to continue that much longer.

Source: tradingeconomics.com

Several things continue to occur as at $100/bbl; there is some level of demand destruction; production elsewhere in the world continues to grow (I read that Venezuelan production rose to 1.25 mm bpd ,more than had been assumed prior to the Iran war); and the Saudi east-west pipeline is now pumping its capacity 7 million bpd, thus the amount of oil ‘missing’ has been reduced from the initial headline 20 mm bpd to somewhere along the lines of 12 mm bpd, still extremely painful to the global economy, but obviously not (yet) catastrophic. However, since oil prices remain around $100/bbl, and have not risen to $150/bbl or $200/bbl as many pundits had forecast, there remains a great deal of confidence that this is going to end before too much more time has passed. I certainly hope so for everyone’s sake.

Away from that, there is precious little other news to note as Asia is basically on holiday until Thursday and the UK is closed today, so market activity has been more muted. But let’s take a look. In the equity markets, weirdly HK (+1.2%) was open despite both China and the UK being closed and given HK’s history, I would have thought it would have responded to one of those situations. But the big news was Korea (+5.1%) which was dramatically higher on rallies in Samsung and SK Hynix shares, both of which have been major beneficiaries of their semiconductor businesses booming alongside AI demand. I guess we shouldn’t be surprised Taiwan (+4.6%) followed that path and in truth, there were more positive outcomes (India, Philippines, Malaysia, Singapore, New Zealand) than laggards (Australia). Remarkably, everything I read is that Asia is the region most negatively affected by the Iran war, yet here we continue to see equity markets rising.

In Europe, things are less optimistic this morning with red across the screen led by Spain (-1.6%) and France (-1.0%) although both the UK and Germany are nigh on unchanged. One of the weekend stories is that the US is now going to be raising tariffs on European auto imports to 25% from the 15% initially agreed as Trump claims the Europeans weren’t following the agreement. As to US futures, this morning they are marginally lower as I type (7:30) but remain just ticks away from the all-time highs set last week. Again, it is difficult to accept the idea that the world is about to end based on the market’s current behavior. Look at the chart below and worry does not seem to be prevalent, nor has it been for any extended length of time in the past 5 years.

Source: tradingeconomics.com

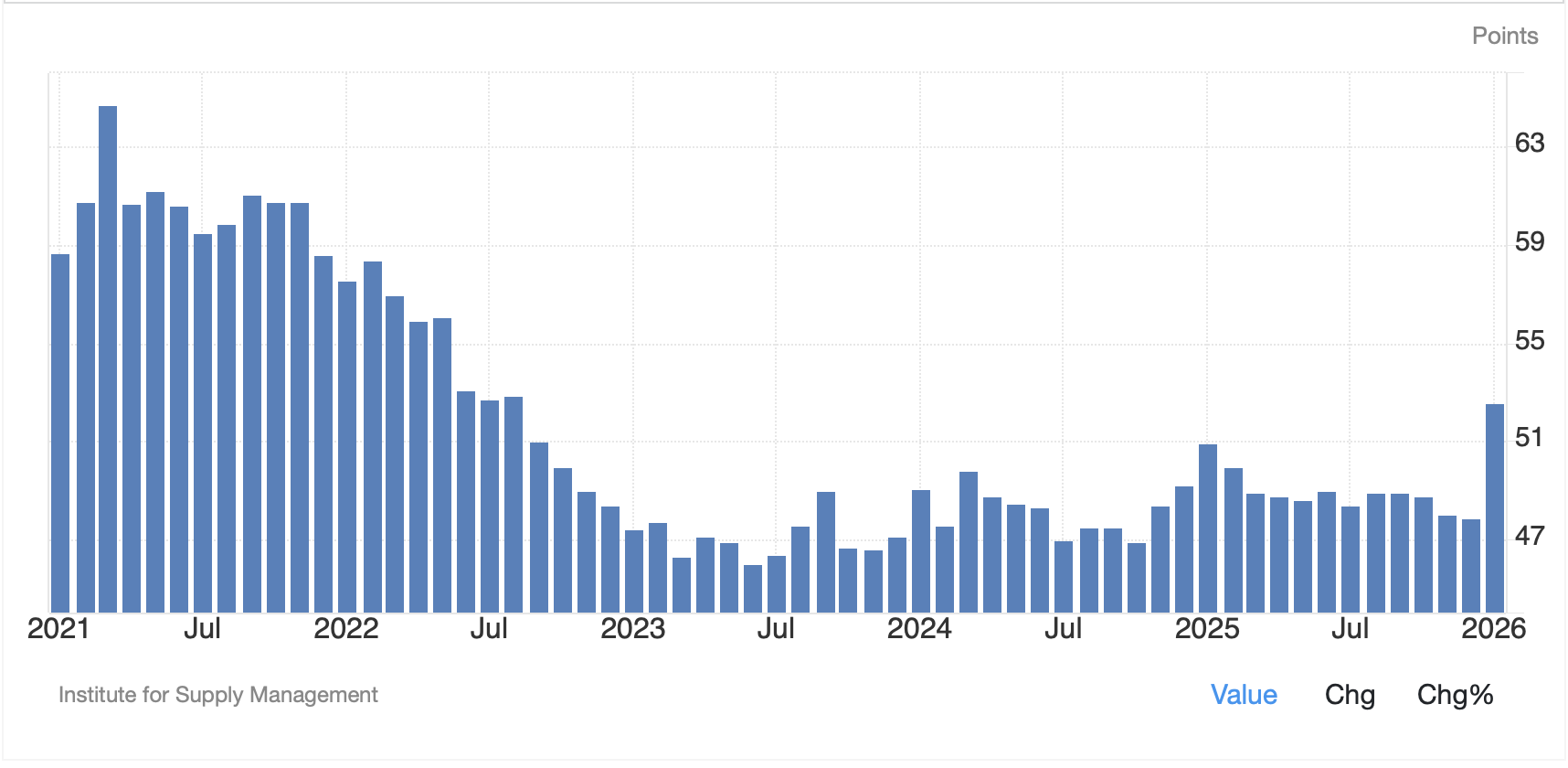

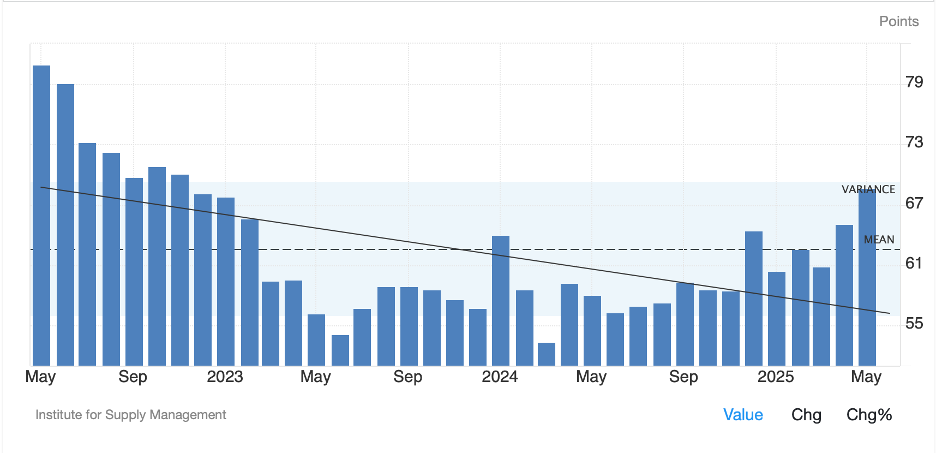

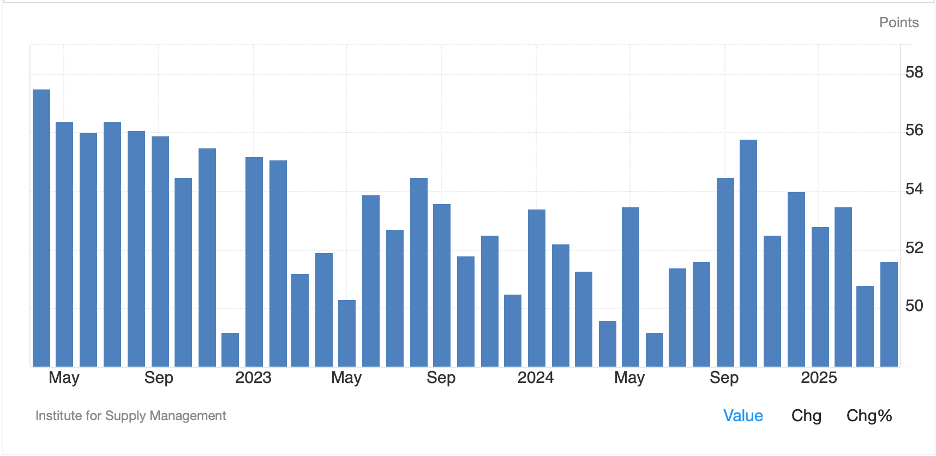

In the bond market, yields are higher this morning with Treasuries (+4bps) leading the way and European sovereigns all higher by between 3bps and 4bps as well. It’s interesting that this is the behavior but I suppose it has to do with the Keynesian view that higher economic activity leads to higher rates. If we look at the PMI data from around the US and Europe, manufacturing has been doing quite well. Look at the ISM Manufacturing chart below for the past 3 years and it is clear that investment is growing there.

Source: tradingeconomics.com

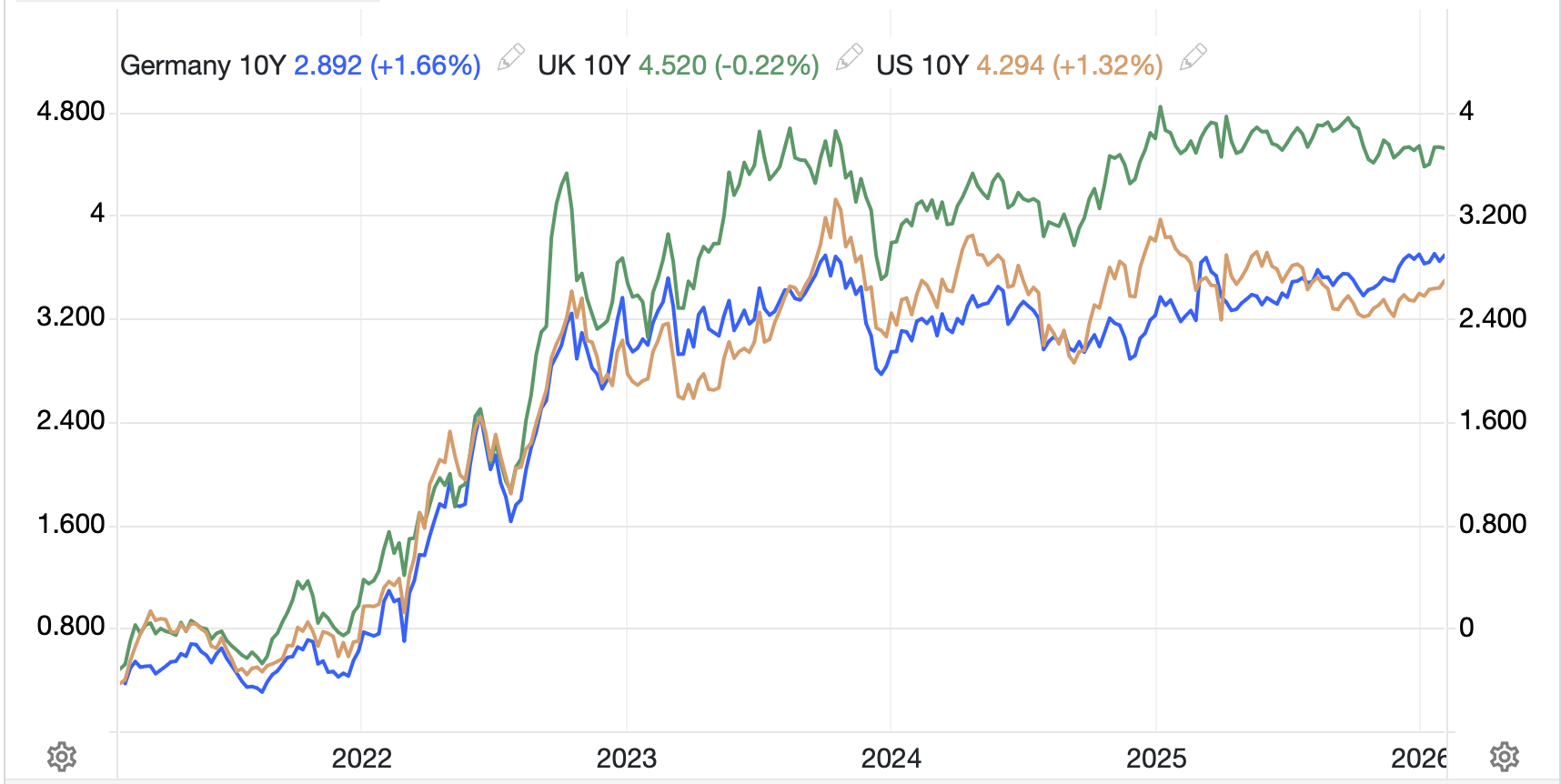

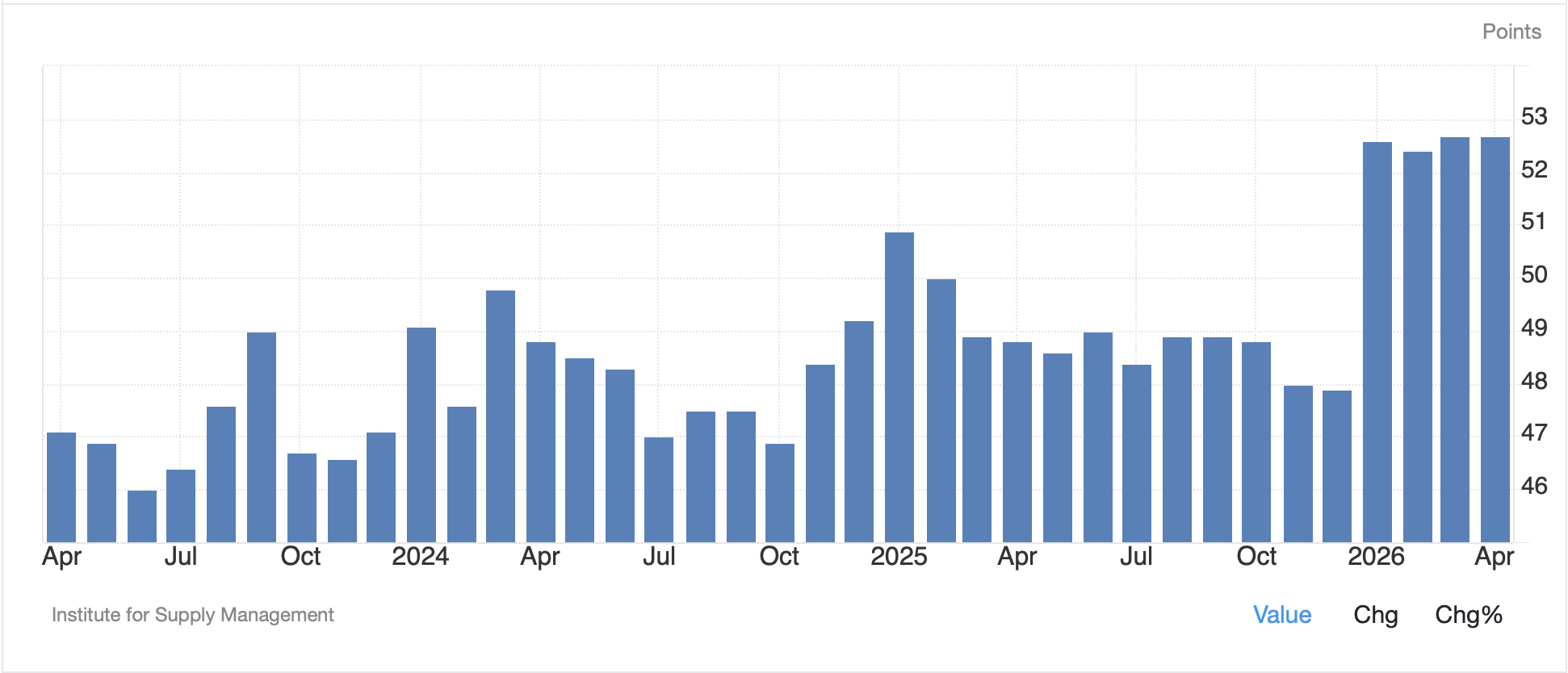

It is a similar tale in Europe with Manufacturing PMI data this morning all being released healthily above the 50 level and rising from last month. The market response to lift yields seems anachronistic, but such is life. However, it is worth highlighting that if we take a bit of a longer-term perspective on 10-year Treasury yields, while they are pushing toward the top of a 4.00% – 4.50% range, you can see that range has largely been intact for the past 3 years. It is not clear to me that it is time to panic on yields yet.

Source: tradingeconomics.com

In the commodity space, with oil (+3.3%) having risen on the reports of a US ship being attacked, we cannot be surprised to see gold (-1.2%) and silver (-2.6%) both slipping along with copper (-1.6%). This is especially true with China and most of Asia on holiday as official buying of gold is probably on hold for now.

Finally, the dollar is firmer this morning as risk is under pressure across the board. US futures are lower, European stocks are lower and oil is higher. So, gains of 0.25% for the dollar against most currencies are the norm. There was a very sharp appreciation in the yen early in the overnight session and another one a few hours ago, as you can see in the chart below, with many believing the BOJ was in again during quiet markets, but it has completely reversed. My take is the BOJ would not have spent reserves like this and would have been far more emphatic if they wanted to move the market again.

Source: tradingeconomics.com

But, as market in Asia were quite thin, any large sell order would have been able to force a move like these. In addition, with the dollar now several percent below their level of concern, I suspect they will save their ammunition. In the EMG bloc, ZAR (-0.5%) continues to feel most of the pressure from Iran as the combination of higher oil prices and lower gold prices are a double whammy. As well, NOK (+0.35%) continues to respond positively to the oil price. Net, the dollar remains in demand for now.

On the data front this week, it is a mixed week until Friday’s NFP data is released.

| Today | Factory Orders | 0.5% |

| -ex Transport | 0.7% | |

| Tuesday | Trade Balance | -$60.5B |

| ISM Services | 53.7 | |

| JOLTs Job Openings | 6.83M | |

| New Home Sales | 668K | |

| Wednesday | ADP Employment | 99K |

| Thursday | Initial Claims | 205K |

| Continuing Claims | 1800K | |

| Nonfarm Productivity | 1.4% | |

| Unit Labor Costs | 2.6% | |

| Consumer Credit | $11.0B | |

| Friday | Nonfarm Payrolls | 60K |

| Private Payrolls | 73K | |

| Manufacturing Payrolls | 5K | |

| Unemployment Rate | 4.3% | |

| Average Hourly Earnings | 0.3% (3.8% y/Y) | |

| Average Weekly Hours | 34.2 | |

| Participation Rate | 61.7% | |

| Michigan Sentiment | 49.5 |

Source: tradingeconomics.com

In addition, Fed speakers are back on the circuit (I sure hope Warsh shuts them all up) with 12 speeches from 9 different speakers. The funny thing is, we already know their views, Miran wants to cut and everybody else is on hold, so what are they going to say?

The war remains the only thing that matters right now, so watch for headlines that an agreement is coming closer. If that happens, oil will slide along with yields and the dollar while metals and stocks will rally. (Of course, apparently, we don’t need anything else to get stocks to rally!)

Good luck

Adf