Though words from both sides are confusing

The markets are clearly enthusing

The war will soon end

Which may well portend

The bears are all in for a bruising

With stocks round the world on a tear

And yields falling down everywhere

Plus, oil is lower

And gold’s a fast grower

Have we seen the end of the scare?

Will there be peace talks soon? President Trump claims things are happening in that direction. Comments from some in Iran say that is not the case. Clearly, both sides are incented to make those claims regardless of the reality. At the same time, US Marines and the 82nd Airborne division are on their way to the Gulf. It is easy to conclude that this is the prelude to a US intensification and effort at physical control of the Strait of Hormuz. Word is that the Saudis and Emiratis are also pleading with President Trump to finish the job and remove the Iranian theocracy to enable a more peaceful Middle East in the long run. But as always, sitting here in the US, and frankly if you are sitting in Europe or China or Japan or Australia, or pretty much anywhere but the Middle East or the White House, we don’t really know the facts on the ground, and we certainly don’t know the next steps. We are just guessing.

However, the best clues we have come from the markets, which admittedly respond to the same news flows we do, although I’m certain that large institutions have better insight than reading Bloomberg or the WSJ or listening to al-Jazeera. But, if we look at the markets this morning, the future is a lot brighter than it was on Monday.

While equity markets in the US were lower yesterday, it was certainly not a rout. Rather, after a weak opening, they rallied back to positive territory as this new dialog appeared, although closed off the highs. This morning, though, as you can see from the screen shot from tradingeconomics.com of equity futures markets, green remains the dominant color. In this table, only Toronto (TSX), Mexico (IPC) and Brazil (IBOVESPA) are not open right now, but otherwise, risk is back in vogue.

As we have seen over the past weeks, economic data has lost its importance, as have the words of central bankers around the world with the only words that matter coming from President Trump or whoever may be a spokesman for Iran these days. It is entirely possible that the global equity markets have gotten this situation completely wrong, and that over the next several weeks, the situation in the Middle East is going to deteriorate, but I am going to lean to the side that has trillions of dollars at risk and go with them for now. After all, given all the talk about rampant insider trading, somebody’s buying a lot of equities!

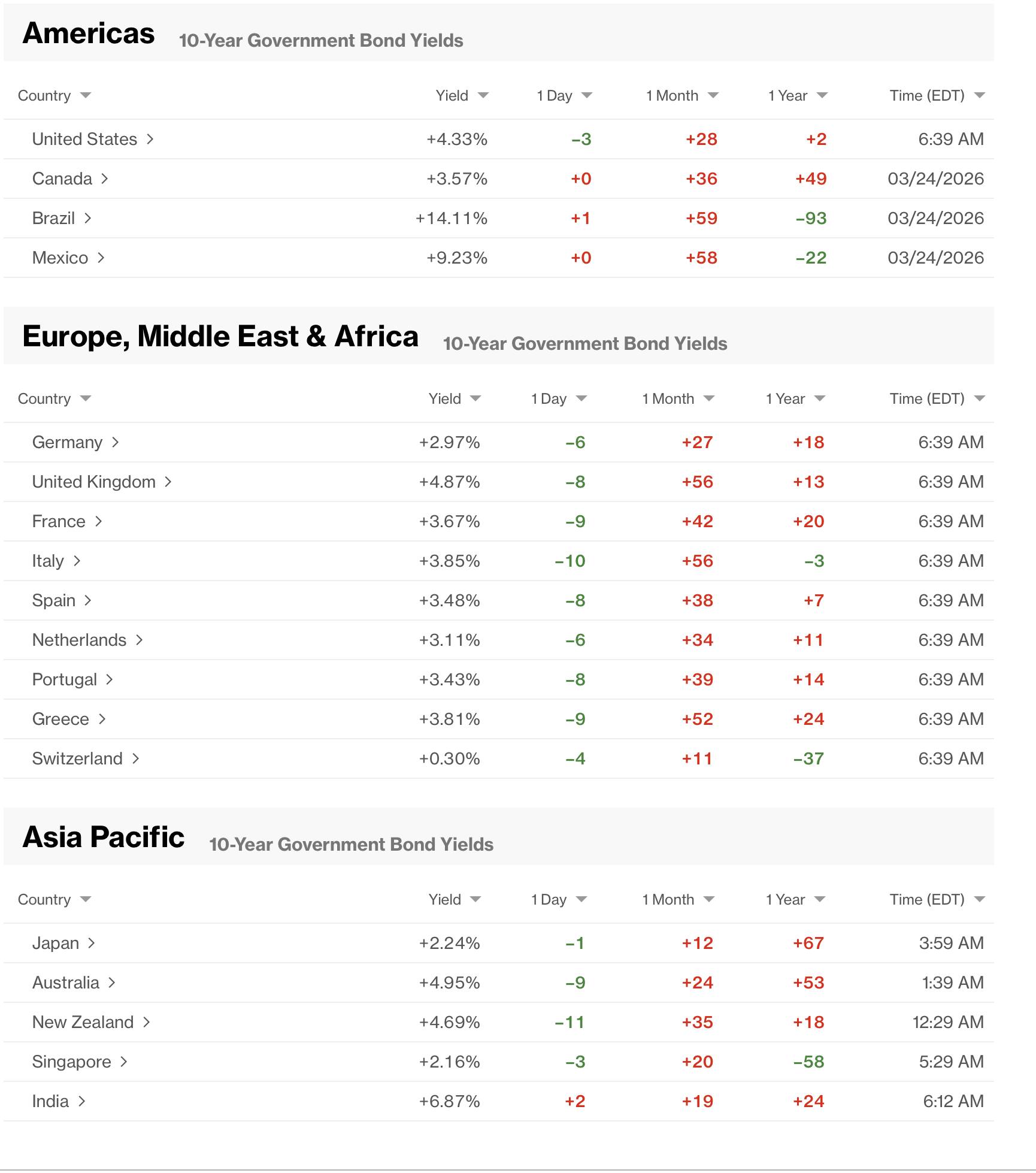

Meanwhile, bond yields around the world are sliding as well. the Bloomberg screen shot below shows that while yields around the world have risen over the past month, today investors are starting to accept that, perhaps, oil prices may not be $100/bbl for a very long time.

We did see February UK inflation data this morning, which printed unchanged and as expected at 3.0%. We also heard from Madame Lagarde, who explained that the ECB would act decisively and swiftly, if necessary, given their absolute commitment to a 2.0% inflation run rate. “We will not act before we have sufficient information on the size and persistence of the shock and its propagation. But we will not be paralyzed by hesitation: our commitment to delivering 2% inflation over the medium term is unconditional.”

The interesting thing about this, to me, is how little the FX market seemed to care about her comments. A look at the chart below of intraday price action with 5-minute candles, shows that her comments were enough to push the euro higher by…20 pips! And that lasted for about 90 minutes.

Source: tradingeconomics.com

As I have been saying, central bank speakers have lost their ability to move markets, something I personally believe is quite healthy. Alas, I am sure that when the hostilities end, or at least become more background noise (see e.g., Russia/Ukraine), they will flood the airwaves with their views in order to reclaim part of the narrative.

As to the FX market overall, movement has been pretty limited with both the euro and pound unchanged on the day, although AUD (-0.4%) is under a bit of pressure, ostensibly on slightly softer than expected inflation figures there. Elsewhere in the G10, the two laggards are CAD (-0.2%) and NOK (-0.4%) as the oil price decline weighs there. In the EMG bloc, ZAR (+0.5%) is benefitting from gold’s rebound with commodity discussions below, and otherwise, FX remains the least interesting market around.

Finally, oil (-6.0%) has fallen back below $90/bbl in the US and $100/bbl in London although the price for crude in the gulf on the correct side of the Hormuz Strait is as high as $150/bbl I’ve seen. Asia is still desperate for more barrels of oil and willing to pay up for them. It certainly seems likely that if the Strait remains effectively closed for much longer, the economic damage will grow apace, but right now, oil traders, at least futures traders, are of the belief the end of this stoppage is nigh.

Source: tradingeconomics.com

At this point, oil has retraced a bit over 50% of its initial spike. Market technicians will be looking at the $84.95 level as the next key Fibonacci retracement level, with a break below there likely to convince some that lower prices are the future.

As to the precious metals, gold (+2.1%), silver (+2.7%) and platinum (+3.9%) are all rebounding sharply on the news as is copper (+1.7%). This simply completes the positive viewpoint that has swept over markets this morning.

On the data front, German Ifo Expectations fell to 86.0, as expected, but it’s not clear that had much impact on anything. From the US this morning we see only the Current Account (exp -$211B) a number that is never discussed, and then EIA oil inventories with a small crude build expected, although a more sizable draw of gasoline and products.

Governor Miran speaks and will certainly explain why rate cuts are appropriate, but nobody is listening to him right now. And that’s all we have. As has been the case for the past three plus weeks, Iran headlines will continue to drive market action with oil the first mover. Close to the vest remains the best call in my view.

Good luck

Adf