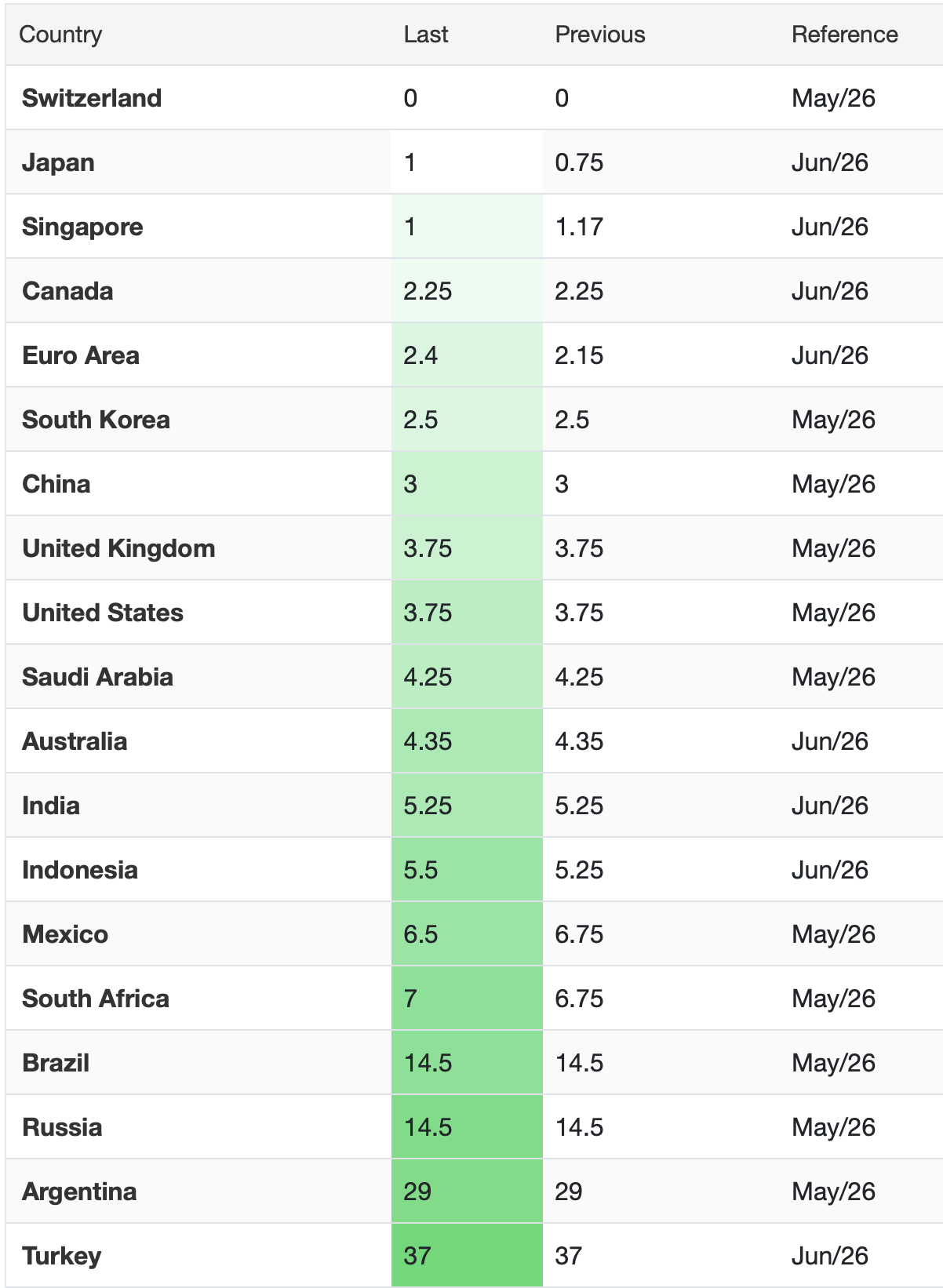

Each day, one more pip

As the yen slides to the next

40-year nadir

The current blame is

The Fed’s recent hawkishness

What if that’s all wrong?

I feel like I must apologize by focusing on the yen again this morning, but quite frankly, there is not that much else to discuss. And in fairness, it is not as though the yen’s move overnight, edging lower by a further -0.1%, is all that much to write about. However, the yen has been getting a great deal of press as there is a cadre of analysts who are ‘certain’ that the MOF/BOJ is going to step in and intervene again soon, although I have seen more discussion of how 170 is in the cards as well.

Now, as it is the beginning of the second half of the year, I thought I might look at what I wrote at the beginning of the year regarding the yen to see how it’s going. And while it is far too early to discern if I was prescient, things are looking pretty good right now. Below, I have copied my yen discussion from back in January. You decide if I’m on track.

A turn to the East where the Sun Also Rises

Will teach us that, really, there are no surprises

To date you’ve heard much ‘bout the rise in yen rates

With pundits opining the Carry Trades’ fates

This year, so they say, look for much stronger yen

As local investors buy yen bonds again

Thus, all the hedge funds who’ve been funding their trades

By borrowing yen, and they’ve done so in spades,

Will need to buy back all that Japanese Money

The outcome, for yen shorts, will not be so sunny

But what if this idea of yen heading home

Is wrong? This implies quite a different syndrome

At this point there’s no sign the government there

Is ready, more spending and debt, to forswear

Instead, what seems likely is more of the same

More government spending in all but its name

So, debt will continue to rise without end

And up to One-Eighty the buck will ascend

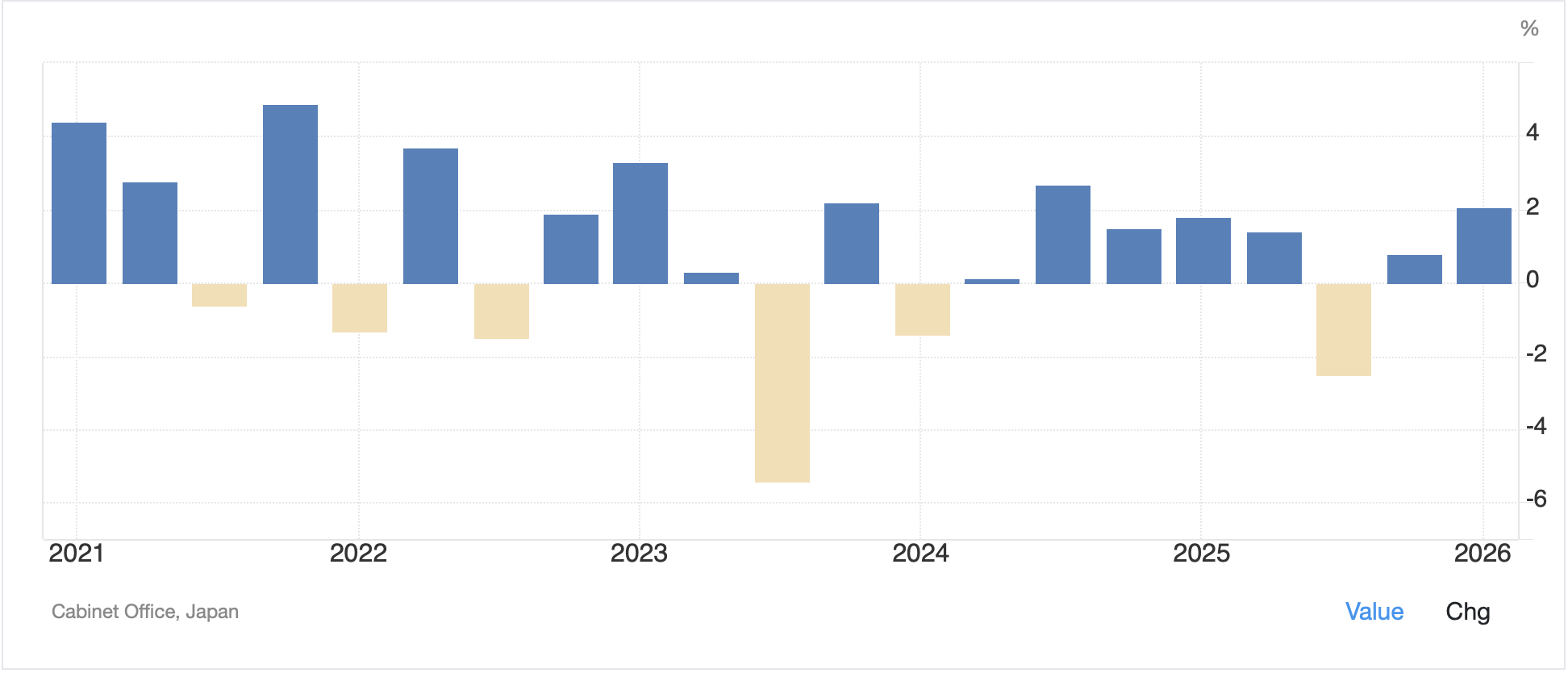

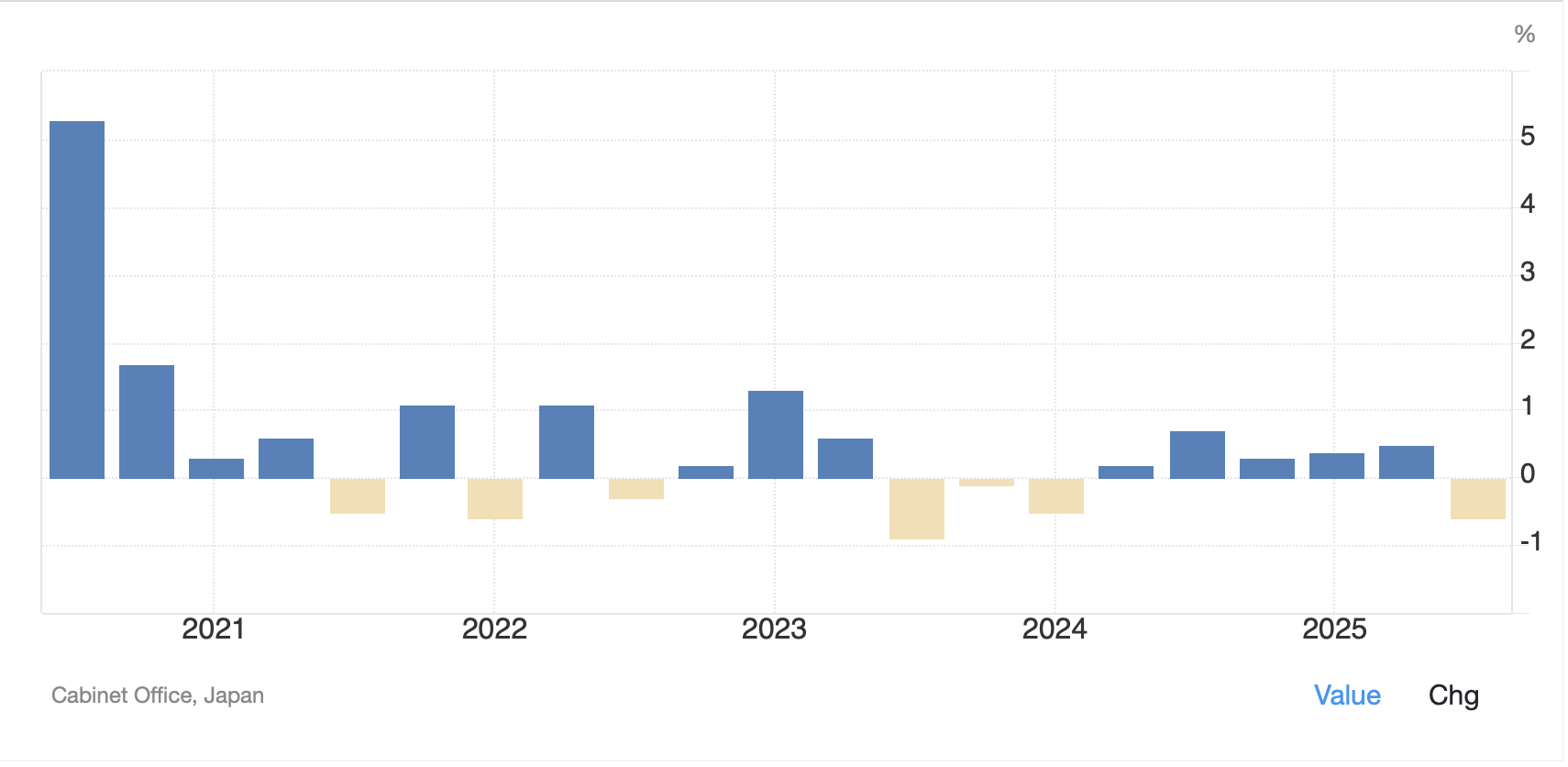

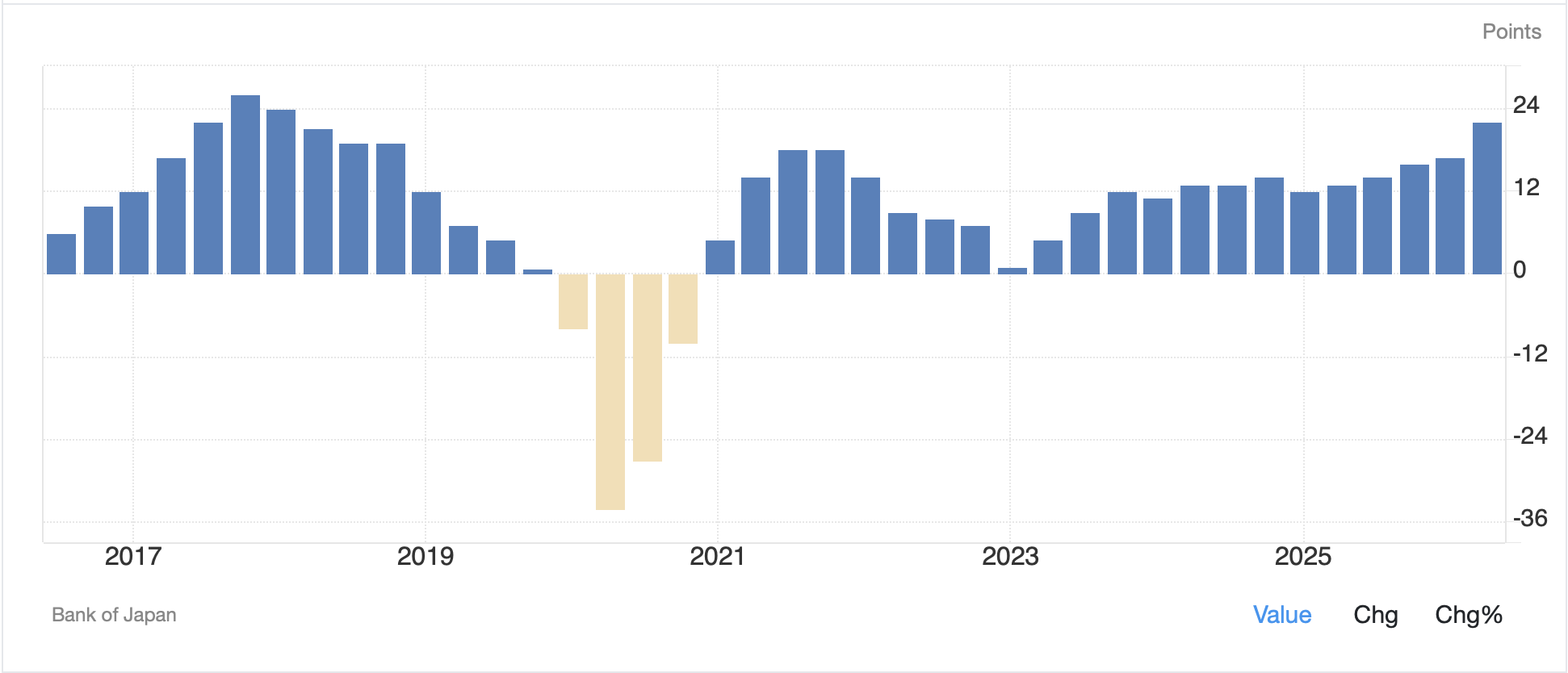

So, with that in mind, let’s see what we learned overnight. First, Japanese Tankan data was released and the economy, or at least the corporate sector, seems in fine fettle. The below chart of the Large Manufacturer’s Index shows the strongest reading since 2017.

Source: tradingeconomics.com

Clearly, the corporate set is not unhappy with the yen’s movement. Now, there was yet another Bloomberg articlediscussing comments from the current Mr Yen, Atsushi Mimura, and reflecting on the fact that the MOF is in regular contact with Secretary Bessent and the Treasury department and there is no obvious concern on then US’s part with the current level of the yen.

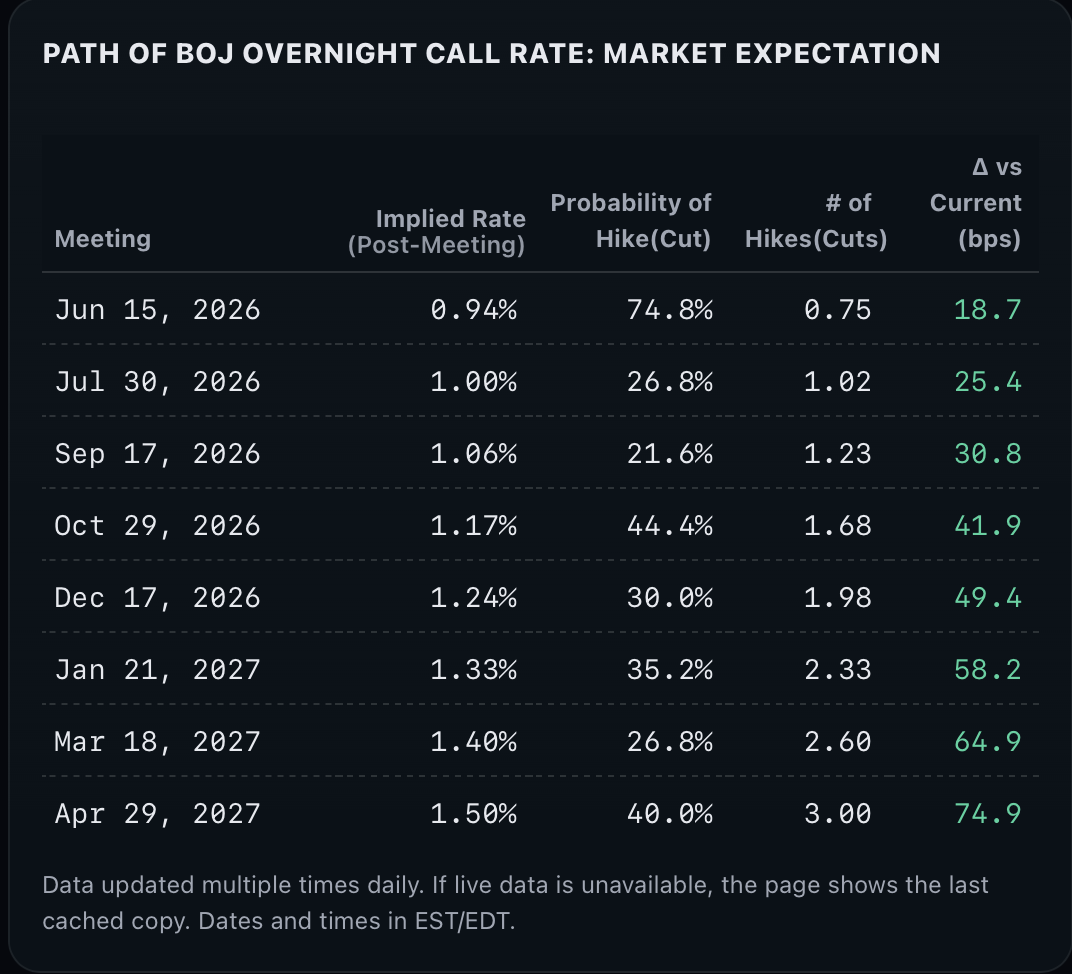

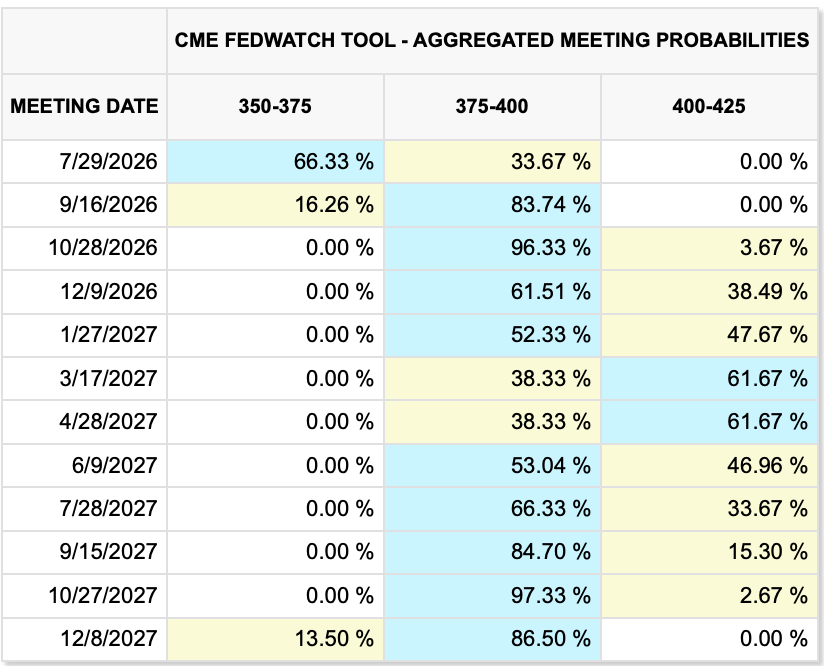

However, the consensus view is that the yen’s recent decline has been driven by the change in attitude regarding the FOMC. The idea is that while the market was anticipating Fed rate cuts back in January, the comments by Chairman Warsh (more of which we will hear later this morning from Sintra, Portugal) have turned things around dramatically and we are now pricing a one-third chance of a hike at the end of July, a certain hike in October and another 40% probability of a second hike in December as per the below CME table.

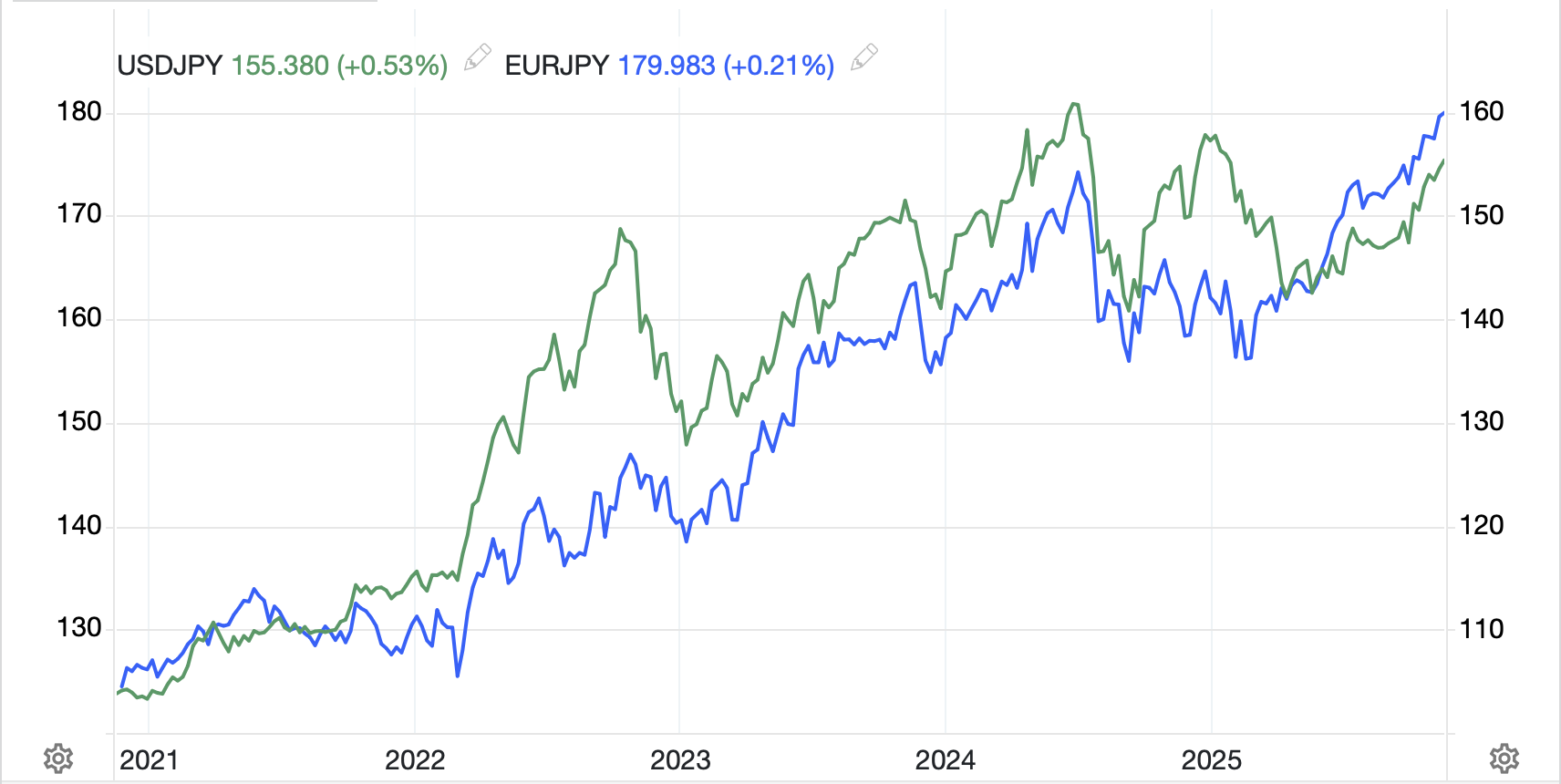

So, if we take this sentiment shift into account, we can look at the last month of trading in USDJPY, which basically encompasses two weeks before the FOMC meeting and two weeks since.

Source: tradingeconomics.com

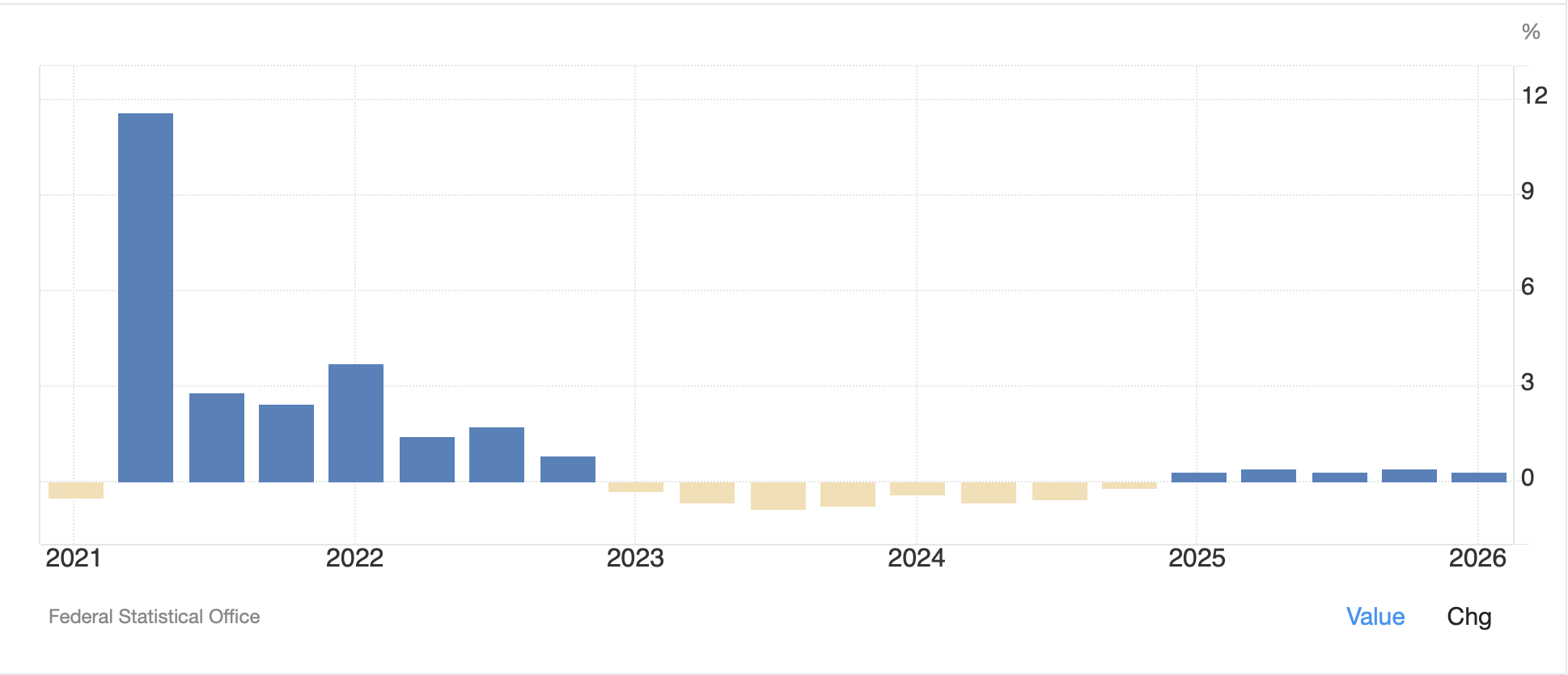

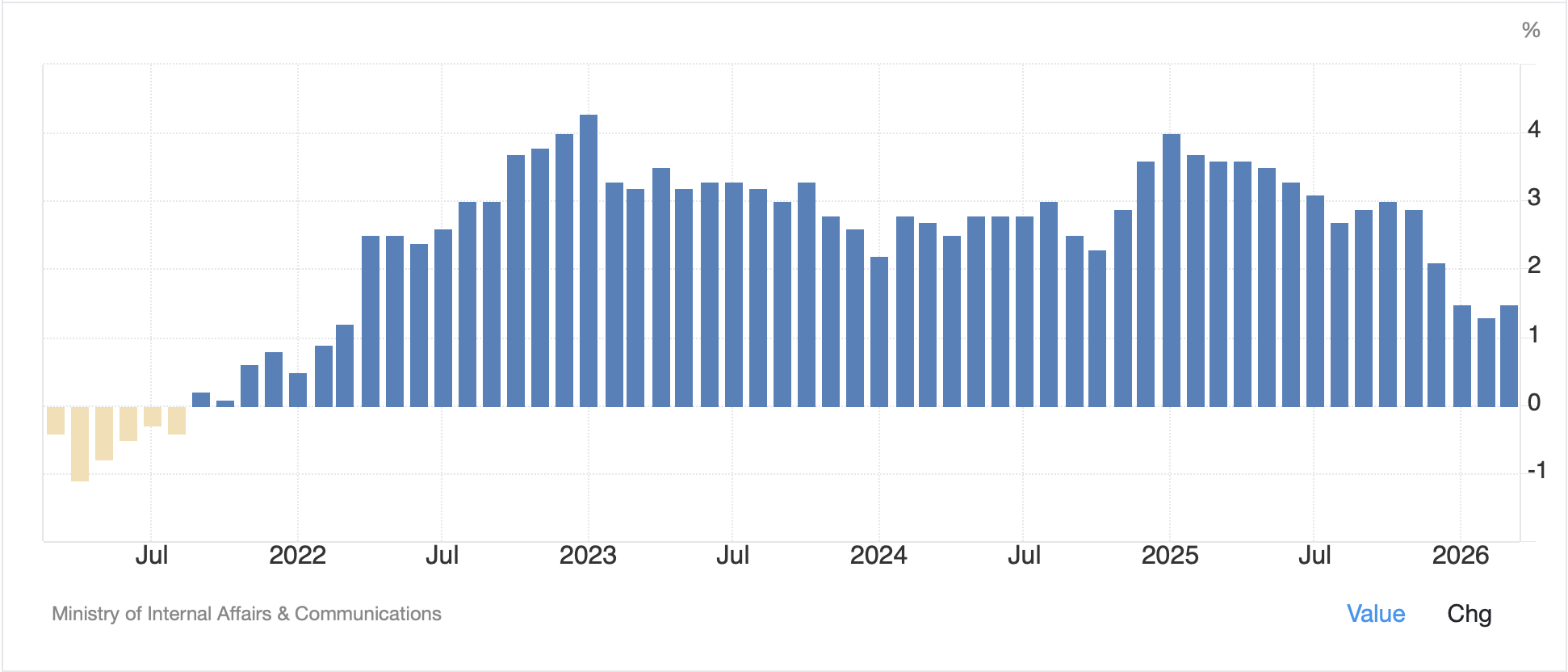

And, if you do the math, it seems that the yen weakened 0.72% (from 159.45 => 160.60) in the first two weeks of June and 1.32% (160.60 => 162.72) since the FOMC meeting. I completely agree that modest change in trajectory is the result of this newfound belief in Fed hawkishness. Of course, you all know that I don’t believe that is what the Fed is going to do, and in fact, my 180 call at the beginning of the year had nothing to do with the Fed raising rates, it was all about deterioration of Japan’s fiscal account. However, as we learned this morning from Europe, where inflation fell to 2.8% headline, 2.4% core, both much lower than last month and forecasts (good thing the ECB hiked into the energy price shock, right?) we can look forward to at least a few months of softening inflation in the US as well based simply on the ongoing decline in oil prices (-1.0% this morning) and continuing to trend lower as per the below chart.

Source: tradingeconomics.com

Softer US inflation numbers are going to undermine the call for rate hikes, and I expect to see those hikes priced out of the markets by the end of July. That alone should help prevent the yen from collapsing in the short-term, although their long-term problems remain extant.

But one thing to keep in mind is that we are coming up to a holiday weekend in the US with market liquidity impaired. It would not be surprising to see the MOF step in to markets Friday when liquidity is thin and they will get more bang for their buck. But the yen is a basket case regardless of US rates. Like I said, short-term, maybe a dip in USDJPY back toward 155 on the back of intervention, but longer-term, unless they change their fiscal policies, lower the yen will go.

Otherwise, there is not much new to discuss. Equity markets finished the quarter with their best result in forever, with the NASDAQ rising ~30%. Seems like it will be hard to repeat that again, and this morning, futures are slightly in the red, about -0.3% or so. As to the rest of the world (do we really care?) last night saw Tokyo (+0.6%) rally along with India (+0.6%) and Taiwan (+1.9%) but the rest of the region slumped led by Korea (-2.0%) which had been the leader, with China (-0.4%) and HK (-0.6%) also falling and the rest of the regional bourses seeing more red than green. In Europe, there is more negativity than not with only the DAX (+0.2%) edging higher after their PMI release (50.3) was slightly better than expected, although still weak. However, the rest of Europe is softer this morning (Spain -0.7%, France -0.65%, UK -0.4%) amid unimpressive PMI results.

In the bond market, yesterday saw US yields pop nearly 10bps in what appeared to be a major futures led move. Certainly, yesterday’s data releases didn’t indicate dramatic strength in the economy, just that things are still fine. But things being what they are as the Treasury market drives global bond yields, we did see yields climb everywhere yesterday and have followed on in Europe this morning with sovereign yields higher by between 3bps and 5bps across the board. JGB yields (+3bps) rose overnight as well, although Treasury yields are little changed this morning. I feel like this move will be reversed by month end, if not sooner.

In the metals markets, oil’s decline has seen support for both gold (+0.4%) and silver (+0.6%) although copper (-1.6%) is struggling this morning. Nonetheless, I continue to like the long-term outlook for metals.

Finally, the rest of the dollar story is one of strength for the greenback with the euro (-0.25%) slipping back below 1.1400 and every G10 currency under pressure. Meanwhile, in the EMG bloc, KRW (-0.7%) is today’s dog, as it approaches its GFC levels as the equity market selling weighed on the currency. Otherwise, broad dollar strength, but nothing dramatic.

On the data front, ISM Manufacturing (exp 54.0) is coming later this morning as are the EIA oil inventory data. And, of course, Mr Warsh’s speech at 9:00am. It will be quite interesting to hear what he has to say, as I think it will be the most critical thing for the session, and frankly, I have no idea where he may go.

So, as we head into a holiday weekend, less positioning is better, and choppiness is to be expected.

Good luck

Adf