Despite faster growth

The yen continues to sink

Are rate hikes anon?

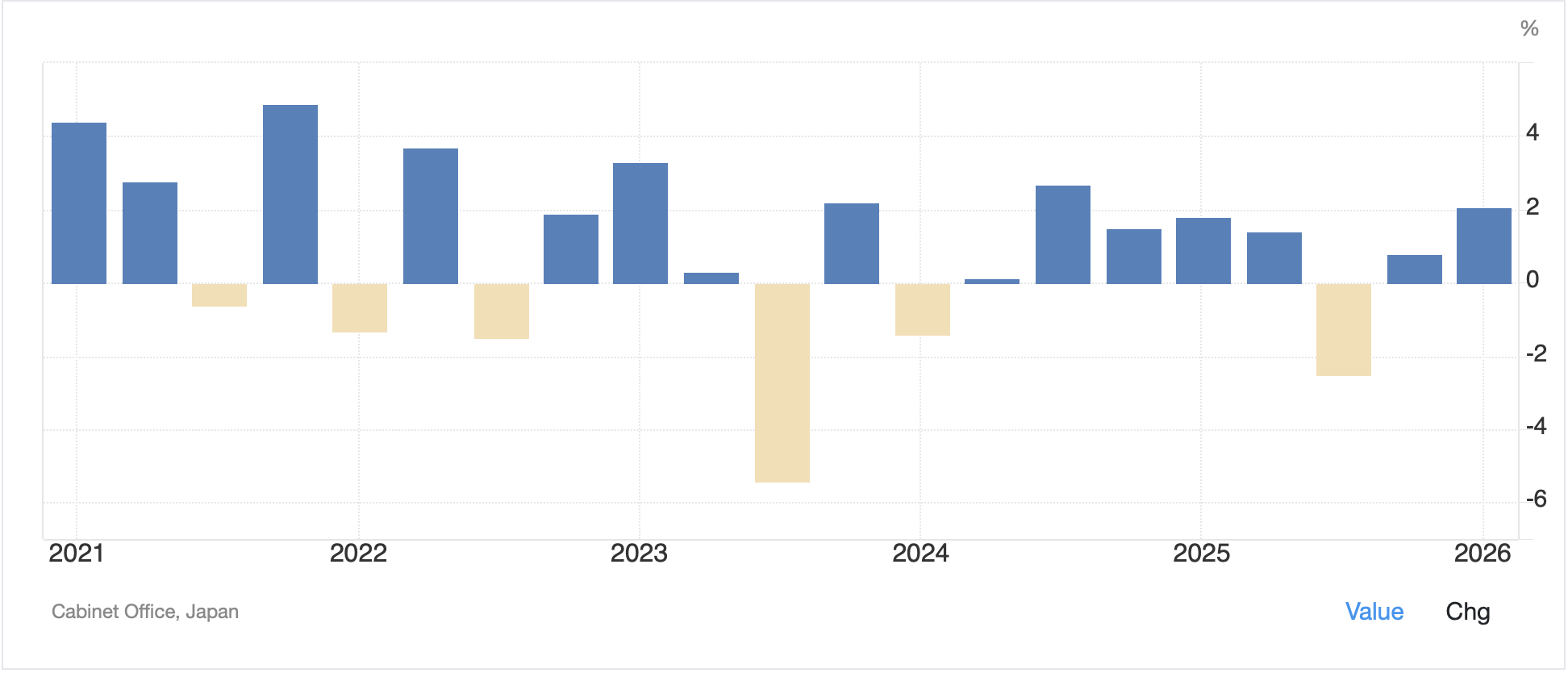

It’s funny, in Japan, there is a great deal of angst amongst government officials that the economic situation is under significant duress, and they appear uncertain how to act. Now, in fairness, the ongoing Iran conflict is clearly problematic for a country that imports essentially 100% of its oil, and most of it travels through the Strait of Hormuz. But if we look at the data, Japan is holding up remarkably well. For instance, below is a chart of annual GDP which was released last night showing 2.1% annualized growth in Q1.

Source: tradingeconomics.com

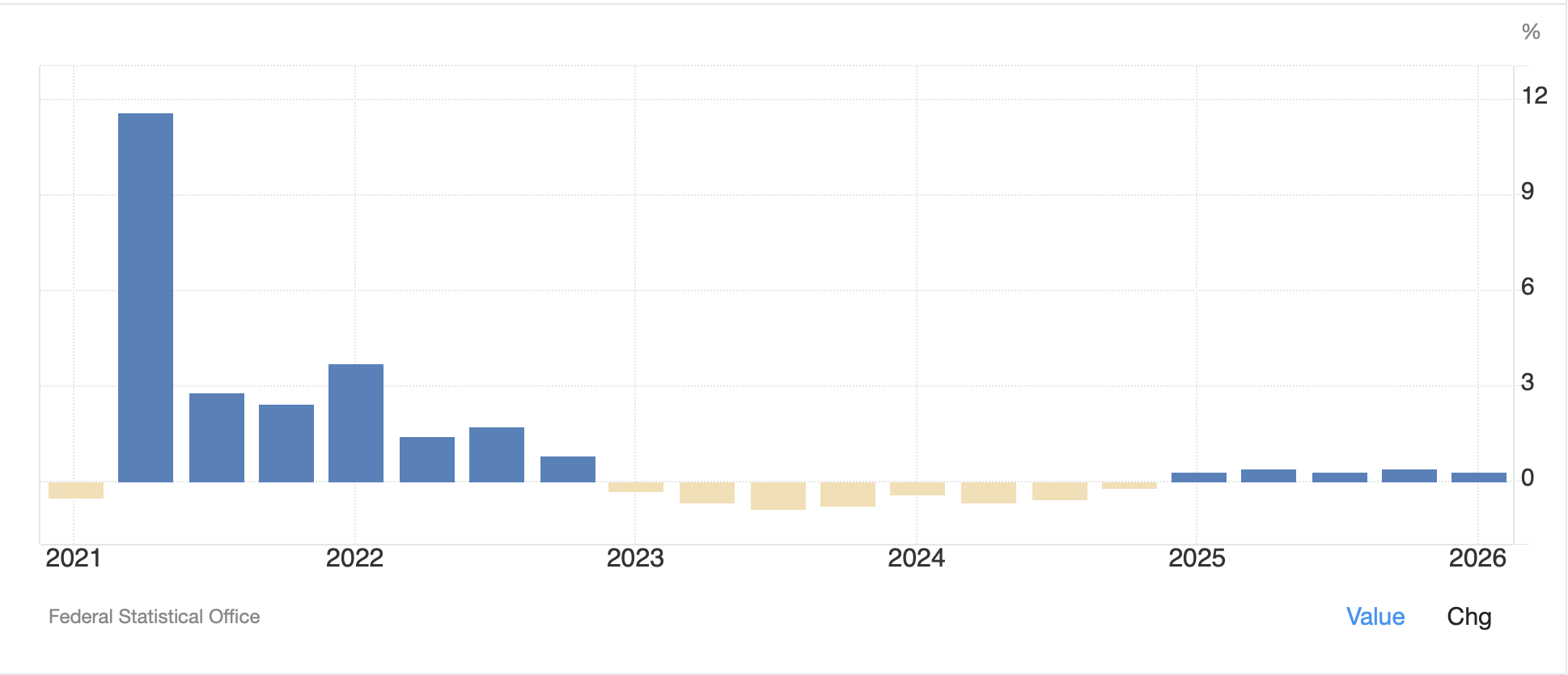

Granted, this is not a chart of an extraordinary expansion, but it is also, relative to its European counterparts, a chart to be envied. For instance, the below chart of German GDP growth (and I use the term growth loosely) shows that after the Covid reopening, things have basically gone into stagnation.

Source: tradingeconomics.com

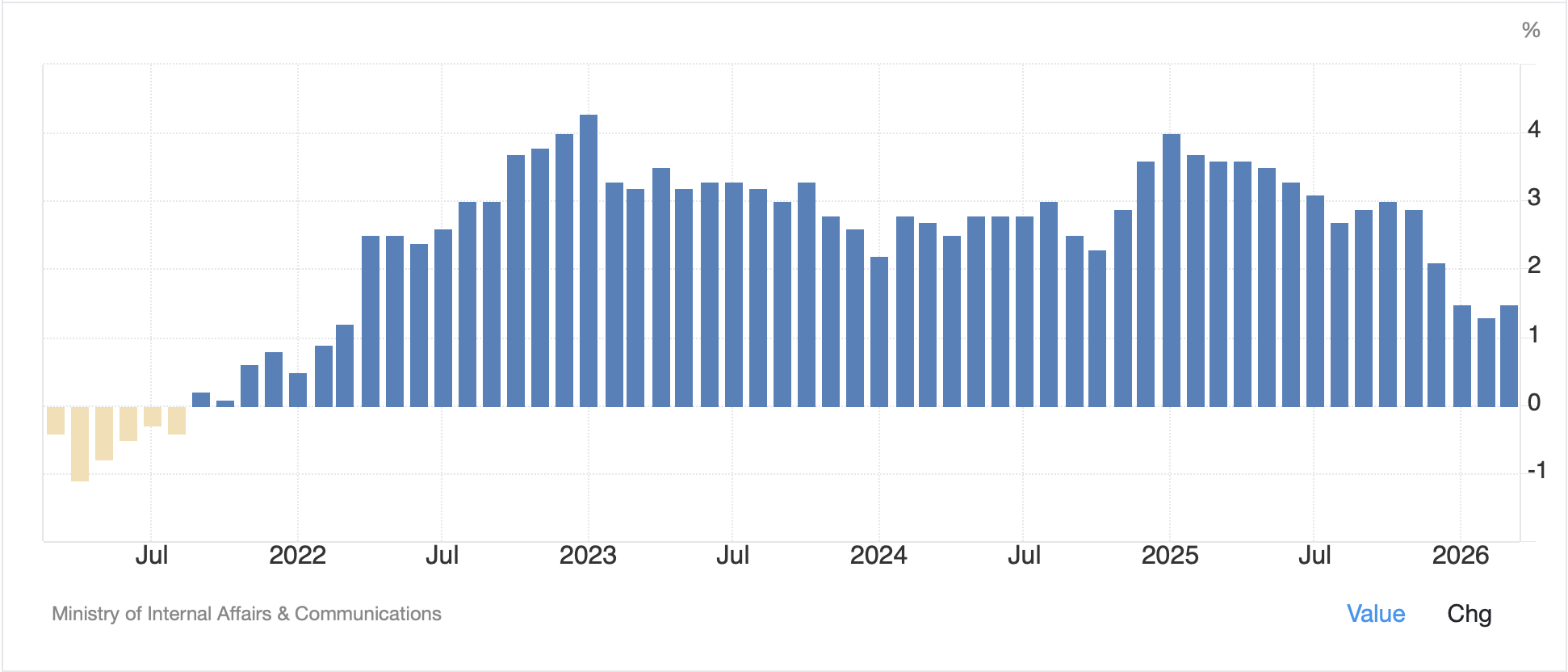

My point is that things in Japan seem to be moving along relatively well, with solid growth, especially when one considers that the population in Japan is shrinking, so given GDP = # people working x output/person, it is hard to grow the economy with a shrinking population. Meanwhile, inflation in Japan remains sticky, although because of government subsidies to ameliorate the costs of electricity and fuel in the wake of the Iran conflict, it is below the 2% target for now. However, apparently it remains a concern amongst the population there.

Source: tradingeconomics.com

Which brings me to the true market related question, what of the yen? You may recall a few weeks ago when the BOJ intervened because the yen had traded through the 160 level vs. the dollar and then there seemed to be a few mini interventions in the days that followed. Yet this morning, as you can see in the below chart, the yen is once again marching toward 160, although I have not seen any commentary from the BOJ or MOF on the subject.

Source: tradingeconomics.com

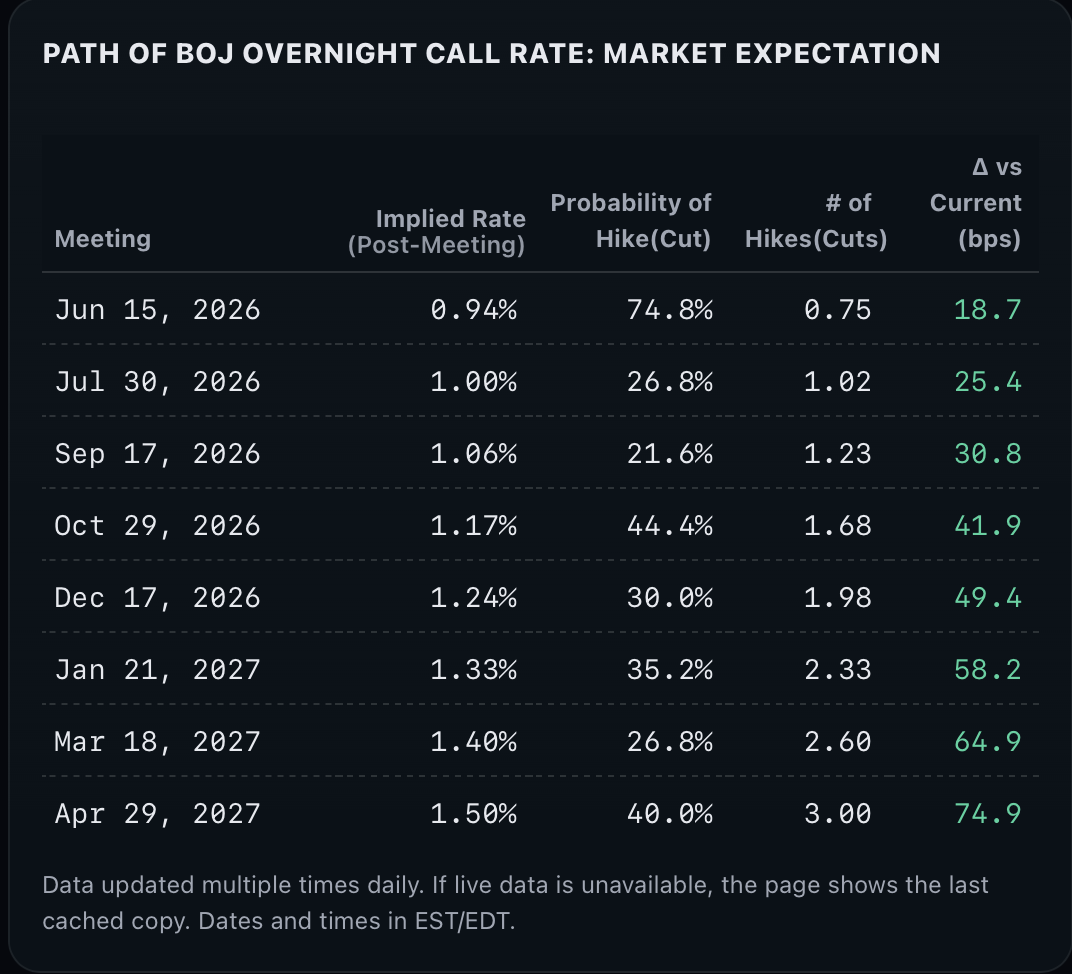

Bringing it all together, the question I would ask is, why is the BOJ even concerned about raising rates at their next meeting in a few weeks? Ueda-san has been around a long time and understands the only way to address persistent currency weakness is via policy changes. Especially now that markets have begun to price rate hikes as the next move in the US (I personally don’t believe that will be the case but that is a different story), the yen will continue to slide unless the BOJ moves. Yet, with GDP growing decently, and underlying price pressures extant, a rate hike should be an easy call. Currently, the probability appears to be about 75% that they will hike in June, but certainty they will hike by July, at least according to rateprobability.com as per the below table. I’m not sure why it is even a question.

The war in Iran’s still on hold

As prices for crude stay controlled

But dollars are bid

And equities skid

While nobody wants any gold

As to the Iran situation, President Trump announced he was delaying, for two or three days, any renewed military action at the behest of the UAE and Qatar who claim that substantive negotiations are underway. Once again, I make no claims of knowledge about what is actually happening there, although that admission is one that most of the punditocracy seems unwilling to make.

But here’s a thought. If you were Ahmad Vahidi, the ostensible leader of Iran, and you have spent the last 3 months in spider holes, caves and basements, moving every 8-12 hours lest someone leaks your location to the Israelis or Americans, how comfortable are you in your position? After all, one of the reasons that people aspire to lead nations is for all the trappings that come with the job. Not only do you get a nice place to live, but you command respect from the people, at least a significant portion of them. Is it impossible to believe that Vahidi is actually looking for a way out as well, perhaps willing to give up his nuclear ambitions for the removal of the price on his head? I know that does not fit the narrative for many folks, and is pure speculation on my part, but is it really that far-fetched?

Ok, in the meantime, as we await the next news from Iran, let’s look at market activities. Starting in the bond market, yields continue to climb higher pretty much all around the world as inflation concerns remain high and there is a growing concern that government bond issuance is going to grow even faster going forward as countries everywhere seek to rearm quickly. So, Treasury yields (+3bps) are pushing back to the levels seen in January 2025, although remain 15bps below those levels as per the below Bloomberg chart.

And as has been the case for quite a while now, Treasury yields are leading the global yield market with European sovereign’s all higher by about 2bps and JGB yields jumping 6bps last night after the GDP data. Certainly, JGB traders believe the BOJ is going to hike rates.

In the equity markets, though, risk appetite remains remarkably robust through all the complexities of the war and economic data. Yesterday’s US session, which started off deeply in the red, rallied back so the DJIA actually closed higher while the other two major indices dramatically reduced their losses. This morning, futures markets are pointing slightly lower with the NASDAQ (-0.8%) the laggard as questions continue to arise about how long AI will drive the thesis there. As to the rest of the world, Asia was mixed with the Nikkei (-0.4%) slipping, although every other index in Tokyo rose, China (+0.4%), HK (+0.5%) and Australia (+1.2%) all gaining. Korea (-3.25%) and Taiwan I-1.75%), though, had rough sessions as those two markets have been driven by semiconductor companies just like the NASDAQ. The only other noteworthy move was in Indonesia (-3.5%) as investors are concerned about the central bank raising rates after their meeting concludes tonight.

Europe is in fine fettle this morning with gains across the board led by the DAX (+1.4%) and followed by the CAC (+0.8%), FTSE 100 (+0.7%) and Spain’s IBEX (+0.4%). I keep reading that there is optimism that an agreement will be reached as the rationale for these moves, but I guess that is the way things go. Never forget this perfect illustration of how market information is passed.

Turning to oil markets, this morning has seen that war ending optimism here as well with WTI (-0.4%) and Brent (-0.9%) both slipping a bit. Interestingly, metals markets are not behaving as they have recently as they, too are lower; gold (-0.65%), silver (-2.1%), copper (-1.1%). In the end, like every market, movement here is entirely dependent on the Iran situation, at least in the short run.

Finally, the dollar is flexing this morning rising against virtually all its major counterparts. In the G10, AUD (-0.7%) is the laggard, but the euro (-0.3%) and pound (-0.2%) are both under continued pressure with both trading near recent lows as per the tradingeconomics.com chart below.

The rest of the block has not fallen as much but is uniformly lower. In the EMG bloc, KRW (-1.3%) suffered after the sharp decline in the equity markets there and ZAR (-0.5%) continues to suffer on the back of weaker gold prices. The one outlier is BRL (+0.3%) which is benefitting despite a weaker economic outlook after some soft data yesterday continues to encourage the potential for further rate cuts there.

And that’s really it for today. There is no data today although there are 3 Fed speakers, including Governor Waller who many have come to believe is a critical voice for the FOMC. Broader movement continues to be all about Iran and how things evolve there. With renewed military engagement on hold, I suspect that the speculators are going to buy stocks again in hopes of a positive outcome.

Good luck

Adf