With things in the Gulf getting hotter

And risk assets heading to slaughter

The question on lips

Can stocks e’er eclipse

Their highs, or ‘stead sink ‘neath the water

But really, the question I’d ask

Is Chairman Warsh up to the task

Of changing the fate

Of the Fed funds rate

And if so, what will he unmask?

It is very difficult to focus on the Gulf situation as not only is it fluid, but there is also no direction of travel whatsoever. So, this morning I want to have a different conversation. Let me start by explaining this isn’t my idea, per se, although the analysis is solely mine. Listening to the Macro Voices podcast Sunday morning while walking the dog, (he’s the one on the left)

Michael Every was on and expressed a very interesting thought, one that I had not considered, nor heard anywhere else. What if the Fed, as Chairman Warsh seeks to adjust how it works, decides that they are going to put their fingers on the scale with respect to the interest rates paid by different industries, not merely by differently rated credits. The idea is that in conjunction with the Treasury, Warsh and Bessent would decide which industries needed to have the most cost-effective funding for the nation to be able to maintain and develop the industries necessary for national defense reasons.

Now, I know this is anathema to almost all of us having been raised on the idea(l) of free markets and that markets are better at allocating, well everything, but in this case credit, than any cabal of central bankers. And in a world where markets were truly free and where everyone competed on a level playing field, I am 100% in agreement with that view. Alas, I’m not sure if you noticed, but that is not the world in which we live.

If Covid taught us nothing else, it was that 40 years of globalization and creating the most efficient processes for manufacturing resulted in significant fragility in those very processes. It turns out that while economists in the US, Europe, Japan, the World Bank and IMF all explained that this was a great outcome (the US prints paper notes and gets lots of stuff for it), that only works when there is peace on earth. During this period, China chose to play by a different set of rules, explaining they were just a poor country so didn’t need to play by the G10’s rules, and massively subsidized numerous industries while essentially ignoring all environmental issues. That tilted the playing field pretty aggressively, and while President Trump has been adamant about that very issue for a decade, he was largely ridiculed, right up until Europe recently figured out that China was eating their lunch too, and now they are looking to impose tariffs on China’s excessive exports. There is an excellent Substack that comes out Sunday mornings called The Brawl Street Journal,written by an analyst in Germany. This week’s, linked here, explains that very issue extremely well.

So, I’ve set the table here, and the key to understand is the table is tilted horribly, with China getting the benefit of the doubt for almost everything.

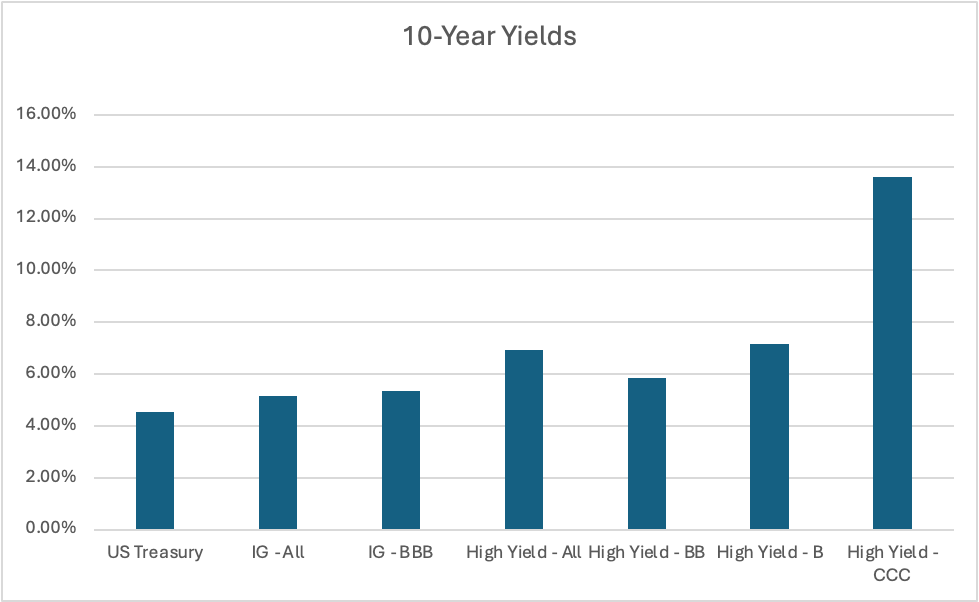

Now, let’s consider what Mr Every’s idea would mean. Below is a chart showing current 10-year yields for Treasuries and a series of corporate bonds delineated by their credit ratings.

Data: streetstats.finance

Makes sense, less creditworthy names pay more. That is how things have always been within a market system as the worse the credit rating, the higher the perceived risk of the investor and therefore the higher yield they demand.

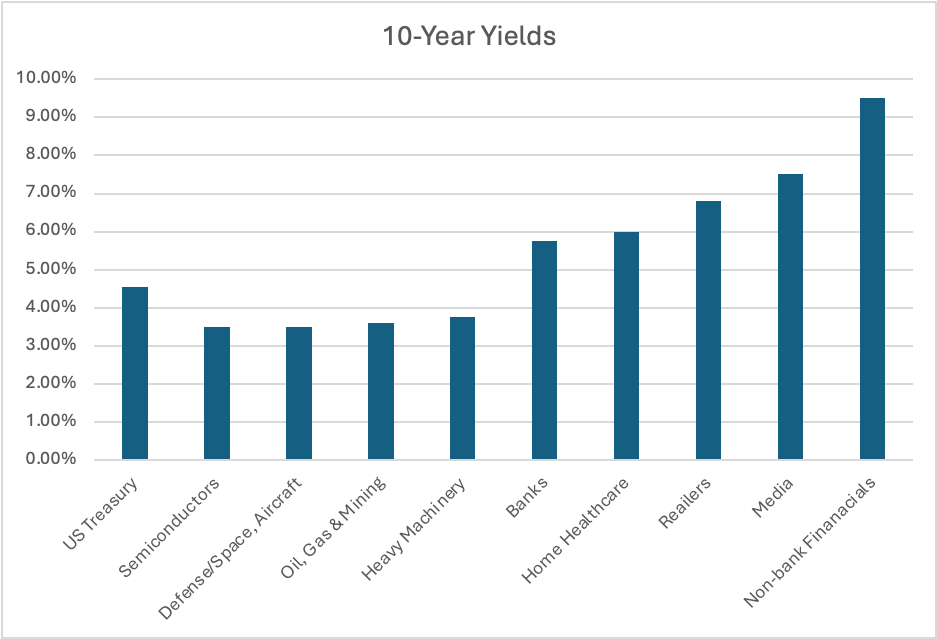

But what if that were to change? What if the Fed and Treasury decided that companies that manufactured products, be they semiconductors, automobiles, tractors, airplanes or flat panel screens, and mining companies that mined in the US (and Canada) and energy extraction companies that drilled in the US (and Canada) needed a lower cost of capital to be more competitive globally as those companies were the ones necessary for the US to maintain its global hegemon status. But media companies, and retailers, non-bank financial institutions and home health services companies, for example, were not deemed as critical. Perhaps the new “credit” curve might look like this instead (all hypothetical)

The point is, China has been subsidizing numerous manufacturing industries for decades with the goal of excess production designed to drive other nations’ competitors out of business and gain a strategic advantage in all those industries. It is why President Trump’s tariffs were a problem for them, and the rest of the world, as the US had been the dumping ground for much excess Chinese production in the past, and now that stuff is going elsewhere.

The world we once knew is no longer the world in which we live. Mr Every’s term, economic statecraft, is much more applicable today than any time in the past 40 years, probably longer, since the end of WWII. Statecraft implies nations will use all the power they have, economic, military and diplomatic, to achieve their desired goals. For more than 70 years, the US did not play by those rules under the assumption that if they created a level playing field, and even tilted it in favor of weaker allies, peace would reign. China doesn’t play by those rules, and that is how we have arrived where we are.

This is all hypothetical, but remember, Chairman Warsh has talked about restructuring the Fed. All the economists think he is talking about shrinking the balance sheet. But what if he is talking about completely changing credit markets with Fed support? I would argue that is not on many bingo cards.

So, briefly, let’s consider how markets would respond to this action by the ‘new’ Fed. Here are my conclusions, I would love to hear yours.

- Stocks – broadly lower, although clearly favored sectors would continue to perform well. But overall leverage would shrink and that has been a huge part of this rally.

- Bonds – a steeper Treasury yield curve seems certain as subsidies for those favored industries will weigh on the US budget. Meanwhile, non-favored industries would find themselves with real difficulties in terms of financing.

- Commodities – offsetting forces here as industrial metals would see increased demand, and getting supply on line takes years if not a decade, but energy may result in a glut sooner as drilling takes much less time to get going. Precious metals would soar, I believe, on the basis of investors and central banks, seeking an asset with no counterpart.

- FX – this is the toughest call as different nations will be impacted in very different manners. Commodity producing nations (e.g., Chile, Norway, US) should see relative strength. Consuming nations would likely suffer somewhat, although Japan and Korea, for instance, could essentially fall within the US umbrella as their key industries are the US focus.

Again, this is all hypothetical but is probably worth some thought. In the meantime, a brief tour of markets overnight after Friday’s sharp declines in the US shows nobody is very happy this morning. The tradingeconomics.com screenshot below shows futures as of 6:10am.

What sticks out to me is Italian equities are bucking the trend, although there has been no data and I cannot find a specific catalyst there. Also, it is interesting that US futures are broadly higher this morning despite growing concerns that the situation in the Gulf is going to heat up again. But Asia had a rough session and most of Europe is feeling a little pain as well.

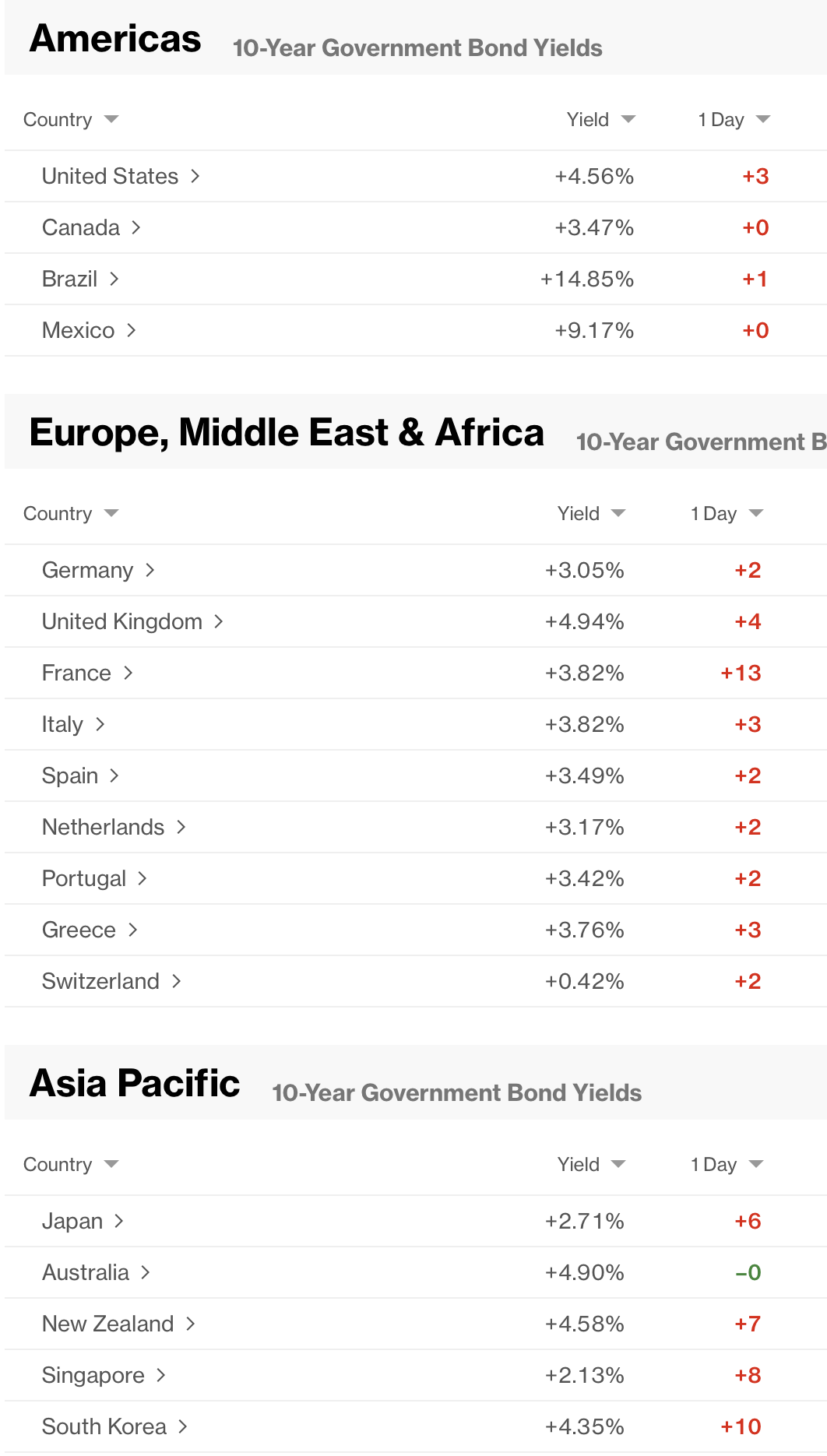

In the bond market, after climbing on Friday, yields continue higher this morning across the board. The below Bloomberg screenshot explains things well. Recognize that Canadian and Mexican markets haven’t opened yet and Australian markets were closed last night for the King’s Birthday. But net, there is growing concern over inflation on a worldwide basis it appears.

Turning to the commodity markets, oil (+3.8%) is higher again, after falling on Friday as there were missile attacks by Iran on Israel in response for Israel’s ongoing attacks on Hezbollah in Lebanon. This situation remains fraught and frankly nobody has any idea when it will settle down into something a bit less volatile. If we look at a chart of the past six months of oil price movement, I have drawn a line at $95/bbl, which to my eye offers a pretty good estimate of the average since things began. There are still many doomsayers who believe $200/bbl oil is coming soon, but that has been their forecast since March. Something to remember about commodity markets is that they do not forecast the future, they are the prices at which physical stuff clears, so it appears that so far, there is ample inventory available.

Source: tradingeconomics.com

Not surprisingly, given the recent relationship between gold and oil, the barbarous relic is lower this morning by -0.7% while silver, though unchanged on the day, suffered dramatically on Friday, falling $6/oz or about 8%.

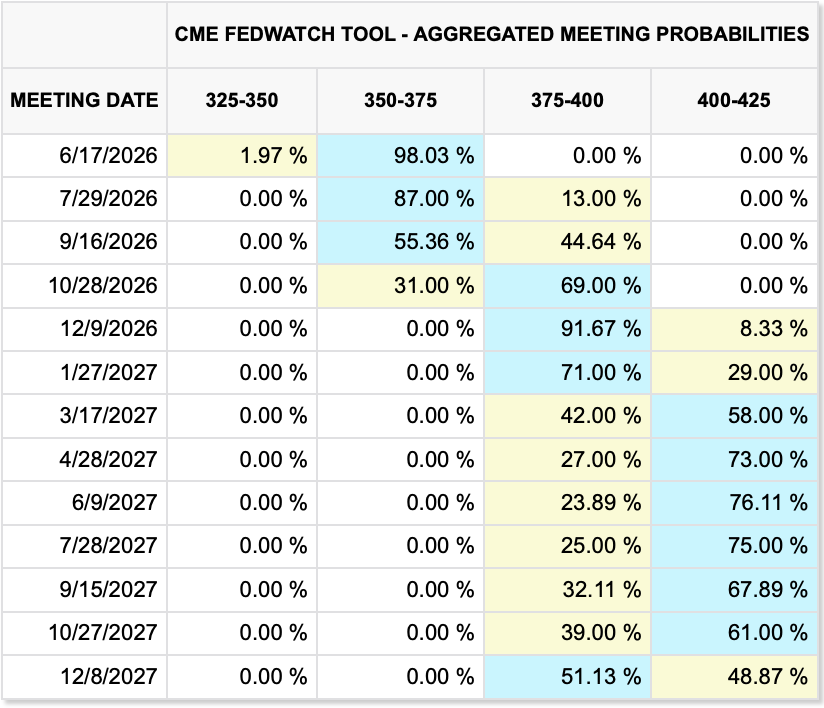

Finally, the dollar is little changed this morning, but that is after a sharp rally on Friday in the wake of the much better than expected NFP data (+172K with revisions higher in the previous two months of +93K) which helped push yields higher as a rate hike this year has now been priced by the futures market as per the below CME table.

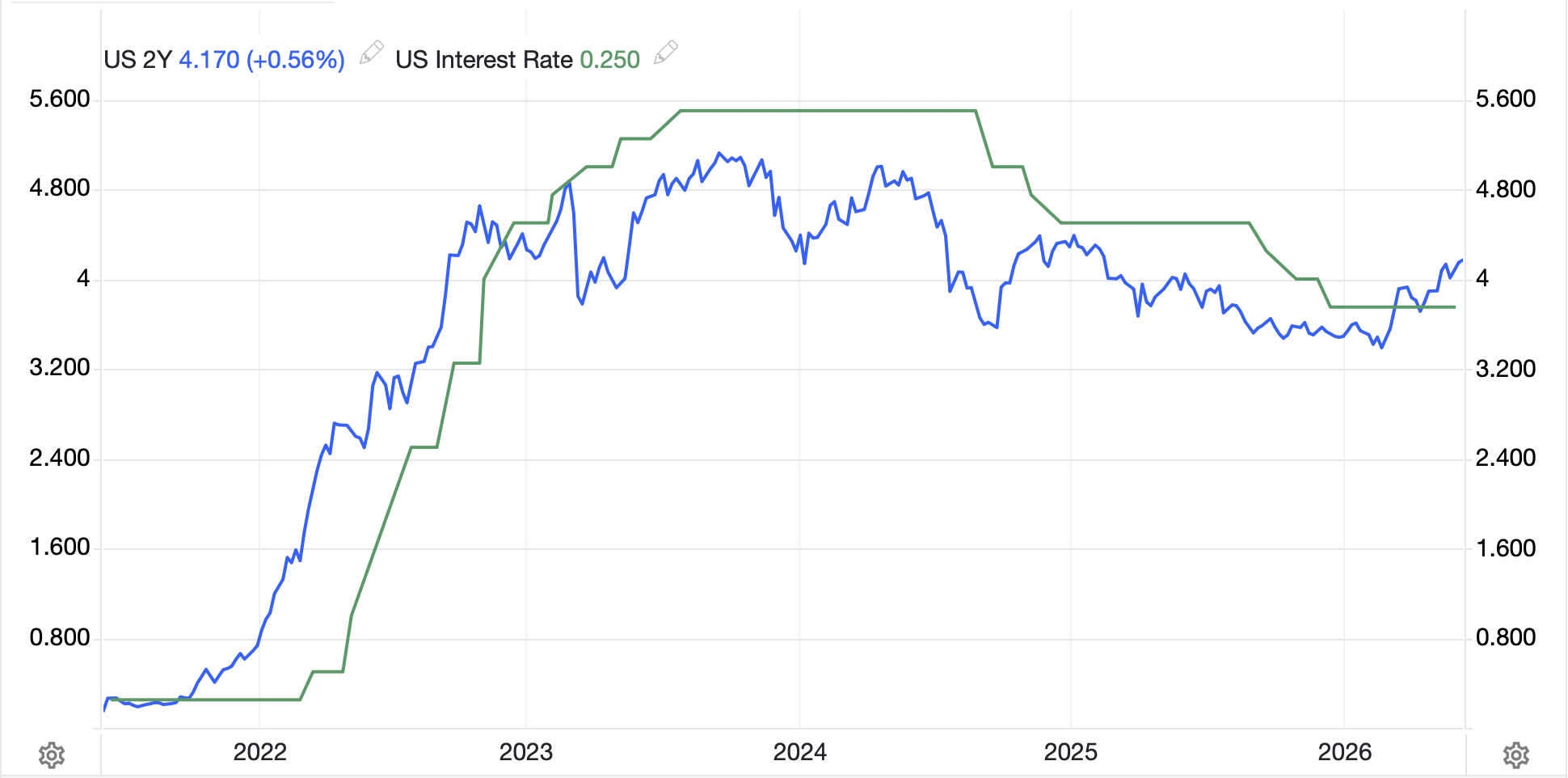

But more than just the futures market is thinking that way. The below chart showing the 2-year Treasury vs. Fed Funds shows that not only have 2-year yields moved above Fed funds, but they are accelerating higher. This is seen as another harbinger of a higher Fed funds rate.

Source: tradingeconomics.com

So, the DXY is back over 100.00, USDJPY breeched 160.00, and is right on that number as I type at 6:50am, and generally, the dollar is pushing the top of its recent ranges. The one exception here is KRW (+1.6%) where the central bank and Finance Ministry both were actively jawboning the currency higher after it traded to yet another new low (dollar high).

As there is no data of note this morning, I will go through that tomorrow given how long things got today. The world is changing rapidly and the most important thing, I think, is to recognize that old relationships may no longer be valid. Nimbleness is critical, whether investing or hedging.

Good luck

Adf