In England and Scotland and Wales

Kier Starmer has gone off the rails

A buffoon-like clown

He’s set to step down

As from the Brits eyes, fall their scales

But will his replacement gain traction

Or will Burnham be a distraction

From solving their woes

As Lord only knows

They’ve many, and no plan of action

It has been an eventful weekend for me so let me start by telling you that Marvel was Best of Breed in back-to-back shows last Thursday. We are very proud and happy.

Second, Friday was a more difficult day for me as I wound up having emergency surgery, although everything is fine. But I am still in recovery mode. Sometimes, aging is harder than other times.

With that in mind, we can talk about the three things that matter, I believe, the change of PM in the UK, the on-again-off-again peace talks in Iran and the fact that the yen is now weaker than the level that got the MOF to intervene back in April.

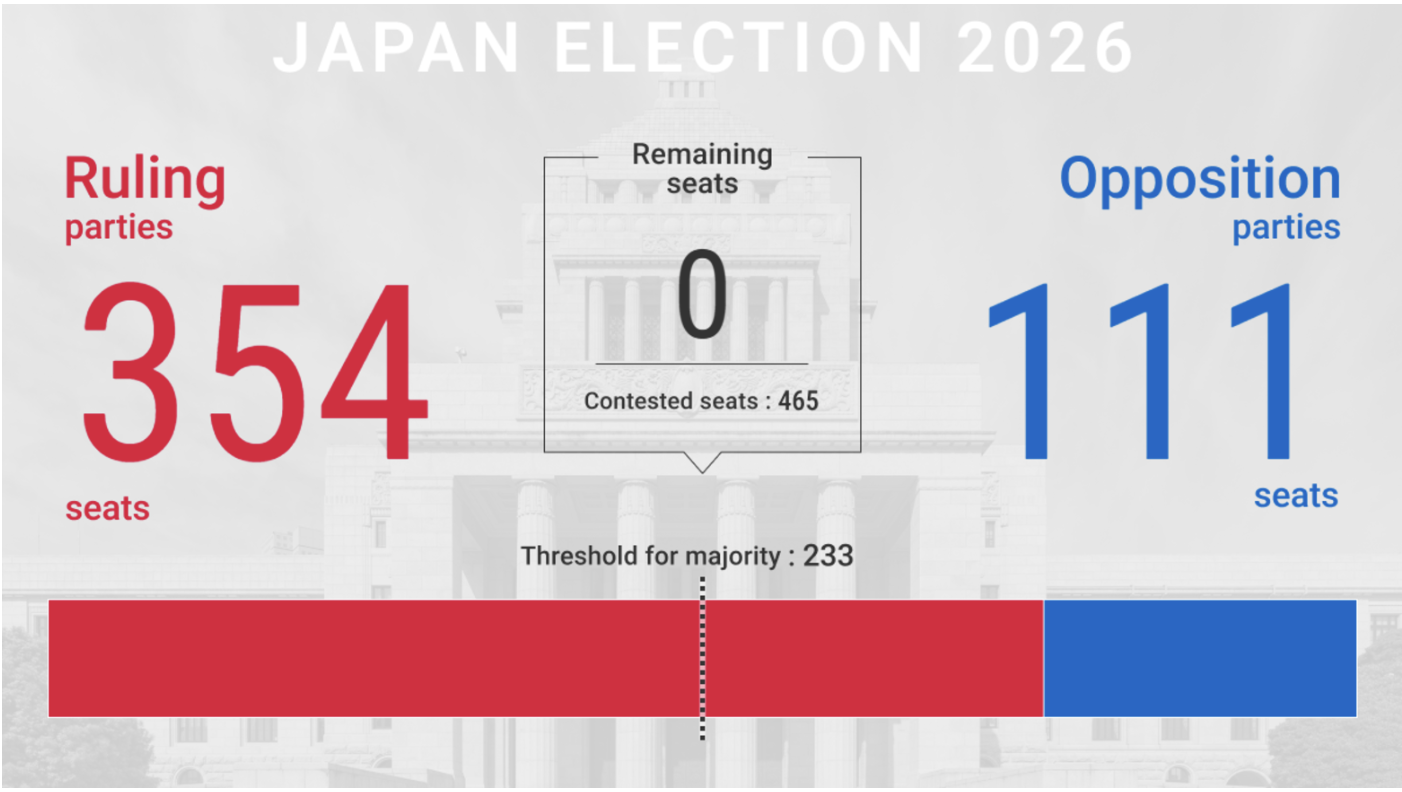

Starting with the UK, PM Starmer has promised to step down now that his most likely successor, Andy Burnham, the former mayor of Manchester, is in Parliament and will now become PM sometime in the next several months depending on the actual timing of certain technicalities. He is described as left-wing, even by the press, which tells you that he must be quite far to the left. But the UK has serious problems with respect to their economy, slowing growth and high inflation, and the social structure due to massive immigration, both legal and illegal. As well, the report that just dropped about the Pakistani grooming gangs that were systematically raping young English girls is so damning, it is hard to believe, yet it was all covered up. The government doesn’t have to go to the national polls until 2029, so Burnham will have time to try to implement policies, but the nation has many troubles ahead.

As to UK markets, both the pound and FTSE 100 have been underperformers relative to their peer European counterparts over the past month or so as this process has heated up, but in truth, not by very much. Much of the pound’s weakness can be attributed to dollar strength (see chart below), where the dollar has broken through key technical resistance in the DXY, while the FTSE is just drifting given the lack of positive news. Certainly, this story didn’t help either one, as both are unchanged on the day.

Source: tradingeconomics.com

In Switzerland, talks are ongoing

As Trump and the Mullahs try showing

That they are the ones

Who have the most guns

But progress seems like it is growing

It cannot be a great surprise that there is a lot of bluster from both sides of this negotiation between the US and Iran as President Trump tries to end the conflict in Iran. After all, both sides are famous for their bluster! And you can read whatever you like from whatever source you want to get your spin, but I’m not smart enough to understand the intricacies of international diplomacy. However, what I do understand is market price movement, and here we are this morning, with oil prices falling further, down -2.5%, and back to levels last seen in early March, right at the beginning of this conflict.

source tradingeconomics.com

Thus far, every story about tank bottoms being reached and an insufficient amount of oil for the pipeline infrastructure to be effective has proven not to be true. There is still a large group of analysts who are calling for end of days, but the market signals just don’t agree. I suspect that the only ones who really want to see oil prices remain high are the oil companies who sell the stuff, but for the rest of the world, lower is clearly better. Obviously, anything can still happen, but by all appearances, it seems that more and more traffic is flowing through the Strait and we are going to see lower prices going forward.

In the end, from my vantage point thousands of miles away from the action, it appears that Iran was greatly weakened by this conflict on a military basis, but more importantly, every one of its Gulf neighbors realized that they needed alternative routes to get their oil to market, and we are going to see a lot more pipeline infrastructure built to do just that, so as time goes by, this choke point is going to lose its effectiveness. And that is probably a bigger weakness for Iran, as that was something they held over the world, but now it seems it is not as impressive a strength as it had been made out to be in the past.

It’s no waterfall

But the yen keeps dripping down

Whence the BOJ?

Finally, the yen (-0.3%) is having a tough time right now as it has traded back to its lowest level vs. the dollar since 1986! That’s right folks, it has been forty years since USDJPY traded above 162.00, and we are pushing that level right now as you can see in the chart below.

The last two times the yen reached these levels, back in April and in July 2024, the BOJ intervened in the markets aggressively. But so far, crickets. I think the issue for them is the dollar continues to be quite strong, especially as traders are now pricing in rate hikes by the Fed, and so intervening is going to be a waste of money. And it’s true, if the dollar is rallying across the board, there is very little Ueda-san can do. As I have repeatedly said, the only way for the yen to break this slide is for serious fiscal and monetary policy changes, and frankly, that doesn’t look like it is in the cards right now. While I know there are many who think the dollar is heading to its graveyard, it apparently still has a bit of life left in it.

Which takes us to the overnight activity. Equity markets have been mixed as all this new information gets digested. In Asia, Tokyo (+1.6%) and China (+2.4%) both had strong sessions although HK (-0.7%) couldn’t keep up. Elsewhere in the region, there was slightly more green than red led by Taiwan (+2.75%) while the Philippines (-1.65%) was the biggest laggard. Uncertainty continues to reign although as the Iran situation slowly resolves, I expect to see things brighten here as Asia was the region hurt most by the entire conflict.

In Europe it is also a mixed picture with the UK (+0.3%) now rallying on the news that Starmer is leaving and Spain (+0.4%) has managed a gain as well while both Germany (-0.3%) and France (-0.7%) are lagging this morning, although there is no news of note in either place. US futures are basically unchanged at this hour (7:15).

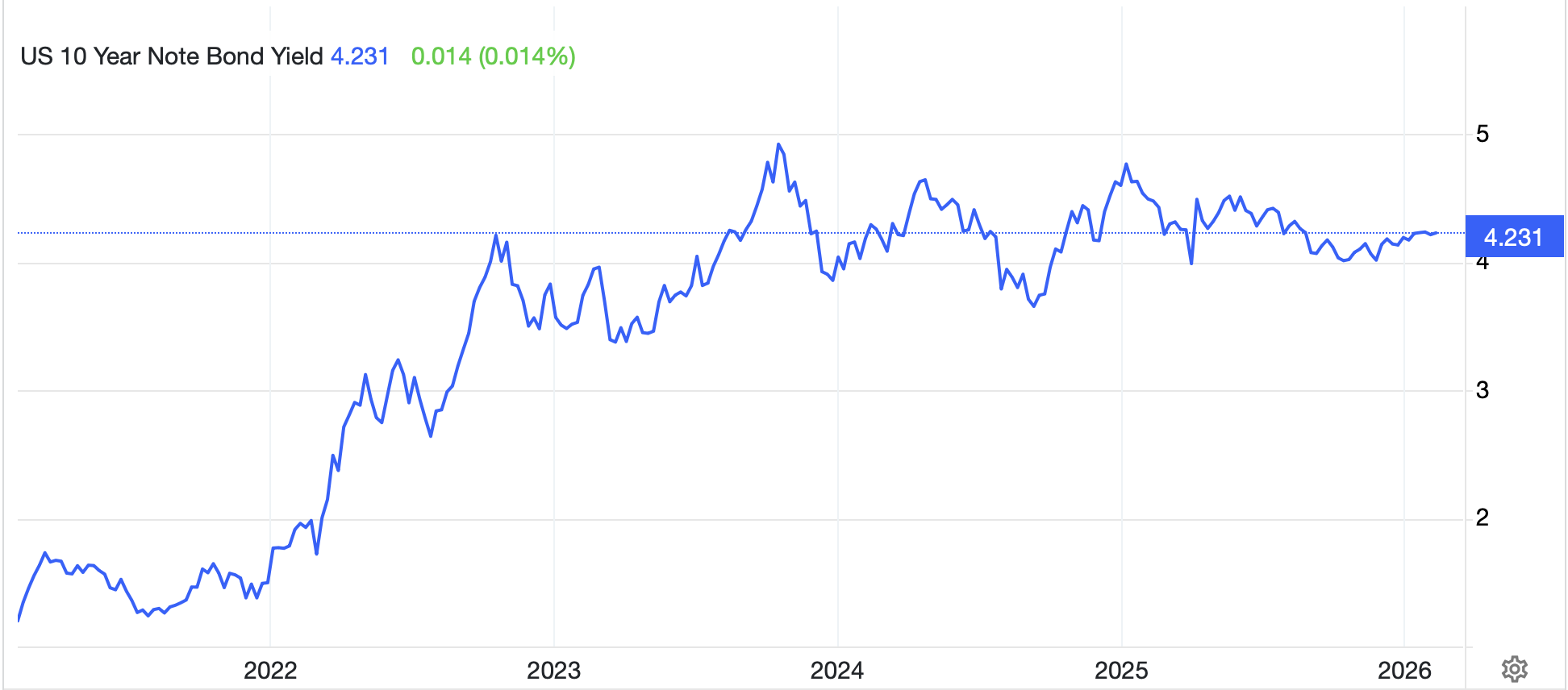

In the bond market, Treasury yields (+3bps) have edged higher this morning, I guess on this new belief in higher Fed funds, although I would have thought the bond market would appreciate a hawkish Fed fighting inflation. European sovereign yields, though, are lower across the board down about -2bps everywhere. Bonds remain less interesting now that they are back in their ranges and not breaking out as so many though was occurring back in May as per the below chart.

Source: tradingeconomics.com

With oil prices lower, it should be no surprise that gold (+1.35%) and silver (+2.4%) are both higher this morning. Many have made the case that with the dollar strengthening, the precious metals complex will remain under pressure, and it is a valid case, but for some reason, I have a feeling it will not be as dramatic as they believe.

Finally, the dollar is firmer across the board this morning, albeit not by very much. Wednesday and Thursday of last week were the big moving days in the wake of the FOMC meeting and the new hawkish read. Since then, not much has happened, just a slow drift higher across the board. FWIW, I don’t think that Chairman Warsh is going to be that hawkish, but I look forward to the structural changes that he makes. However, for now, that is the market assessment.

On the data front, there is nothing today and really nothing of import until Thursday so I will go through it tomorrow.

That’s how things are shaping up, with the dollar gaining, oil sliding and stocks uncertain what to do next. I am a fan of uncertainty as it will reduce systemic risk, and that is something we really need to see.

Good luck

Adf