The president’s on his way home

And pundits with TD Syndrome

All say that the trip

Did not flip the script

And still see the world in a gloam

But markets, one thing, seemed to hear

That though China wants Hormuz clear

The President said

To him the Strait’s dead

And markets responded with fear

With President Trump on his way back home from his trip to Beijing and meeting with Chinese President Xi, we can now expect reams of stories about all the things that he either did or didn’t accomplish. Much has been made of Xi’s opening comments about Taiwan and how it is a critical issue that cannot be mishandled or it would impact the relationship between the two nations. But as I think about Taiwan and China, I certainly understand Xi’s interest in having the island reintegrate into China as it would bring an enormous number of technological skills and abilities in areas currently absent on the mainland. And, of course, Xi will point to history and claim it has always been part of China, yada, yada, yada.

However, ask yourself why any Taiwanese would want to become part of China. After all, per capita income in Taiwan is ~$42K annually compared to ~$14K on the mainland. That is a serious reduction in living standards. Add to that the ability to vote in free elections and the accompanying belief that one’s voice can be heard, and that is a powerful argument to remain independent. Now, as TSMC builds out is fabs in Arizona and elsewhere in the world, it seems to me that the US will lose interest in the Taiwan independence issue overall because, especially for President Trump, who views almost everything transactionally, if the US can get its semiconductors from elsewhere with no problems, notably domestically, defending an island on the other side of the world, one that is decidedly not in the Western Hemisphere, seems far less critical.

Here’s a forecast, by the end of Trump’s term, with TSMC fabs up and running in Arizona, Japan and even Germany, we can see a Taiwan deal similar to the Hong Kong deal, which will sound great but over time China will absorb it in the same way it has done Hong Kong, removing freedoms and its appeal as a manufacturing center.

On to the other part of the trip that has had a much larger impact on markets, when Mr Trump explained, “We don’t need the Strait of Hormuz open.” While the comments from the trip were that China wants it open and agrees tolls are inappropriate, the last throwaway line is what has markets on edge this morning. And on edge, they certainly are!

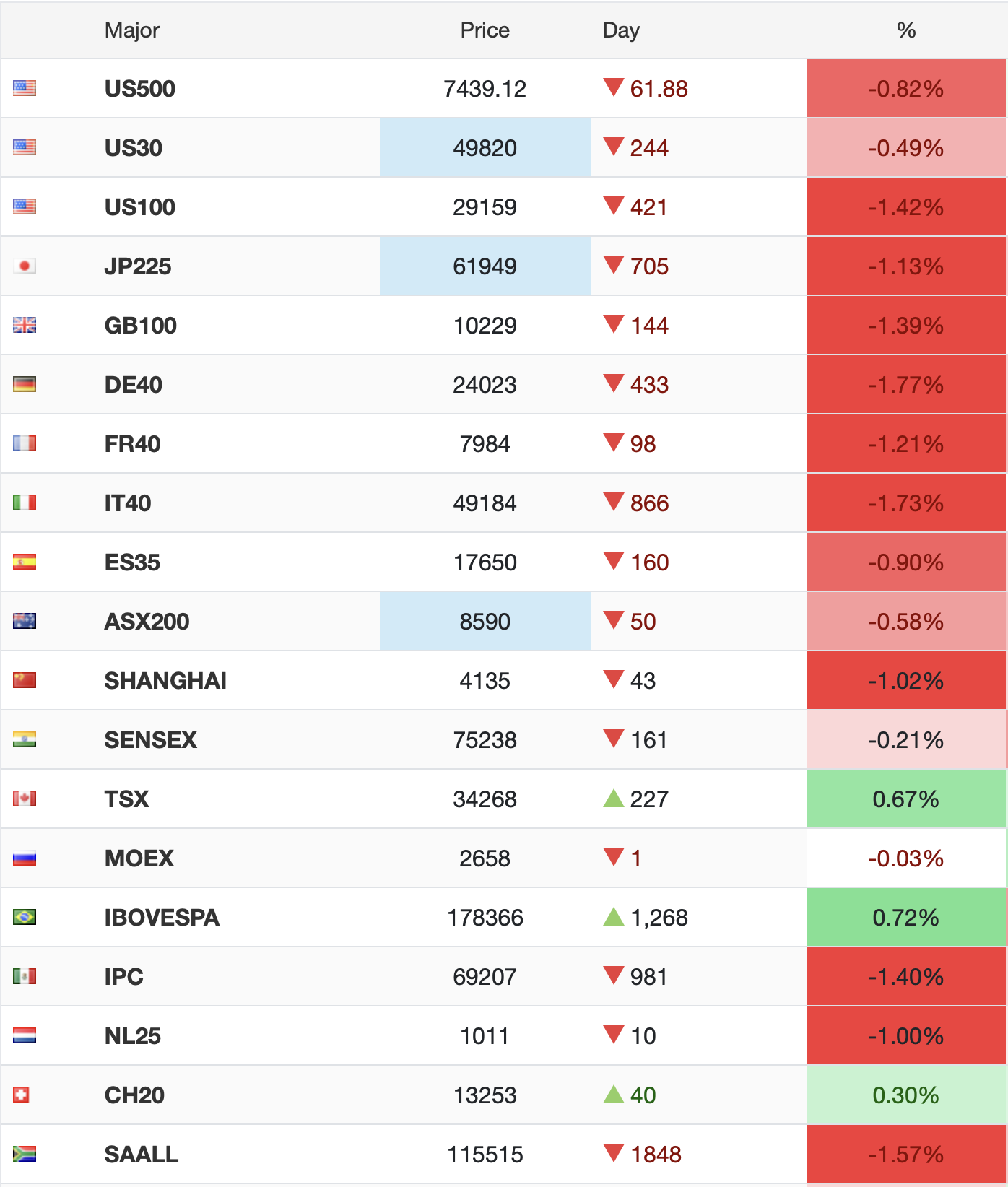

Thus, without further ado, let’s take a look with pictures serving their purpose. As of 7:15 this morning, here are the major equity index futures from tradingeconomics.com

The caveats here are that Toronto’s TSX and Brazil’s IBOVESPA futures markets are not yet open, but I’m confident both will open lower. Russia’s MOEX is irrelevant which makes the Swiss Market Index the only equity market anywhere that is not falling. Perhaps more than the Swiss franc, their stock market has achieved some haven status.

The thing to remember about this sell-off, though, is that we have had a remarkably strong week overall, and so this feels more like a profit taking retracement than the beginning of a new move lower, at least to me.

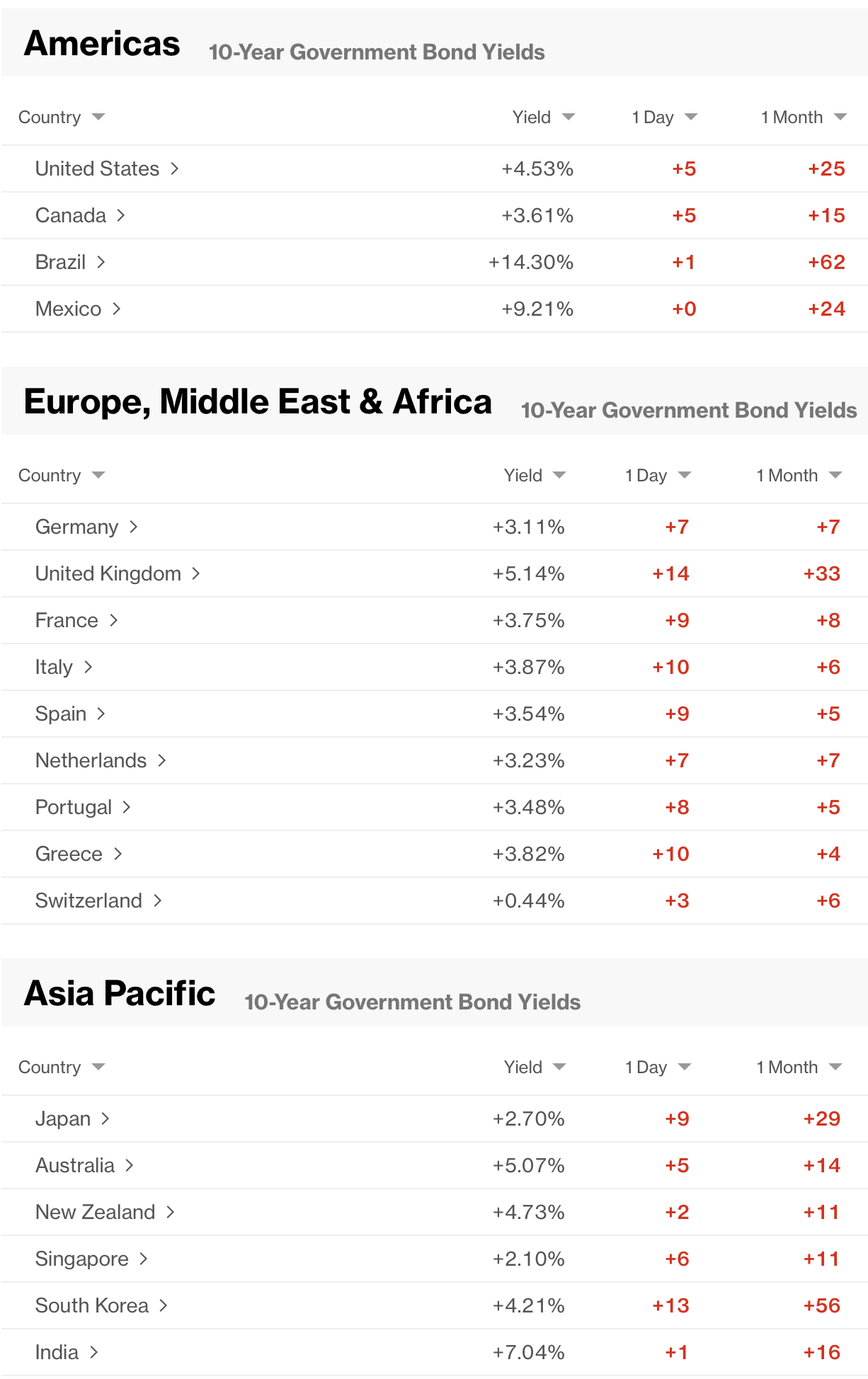

In the bond market, sellers are the dominant force with yields higher everywhere around the world as per the below Bloomberg screenshot.

Much has already been written about 10-year Treasury yields trading at their highest level in almost exactly a year, and 30-year Treasury yields now firmly above 5.0% and how that spells the end of the good times in the US. Maybe that is the case, but I am not convinced. My take of the biggest problem is in the UK, where PM Starmer is under even more pressure this morning after several moves where a key cabinet member, Wes Streeting, resigned to open his path to run for PM as well as where a Labour party member stepped aside so that the very popular Andy Burnham, who is Mayor of Manchester, can now run for parliament and be in a position to become PM. The issue here is that since Starmer will do all he can to hold on to his seat, and the Chancellor, Rachel Reeves, is in his corner, we will see even more deficit spending there to try to help Starmer stay in power. Apparently gilt investors are not impressed with that potential. Of course, neither is anybody holding pounds as a position as is apparent in the FX markets.

While the pound (-0.25%) is only modestly lower this morning, since Monday, as you can see below, it has fallen 3 cents and does not yet seem to have found a bottom.

Source: tradingeconomics.com

But this is of a piece with the dollar writ large this morning, which is higher virtually across the board. In fact, as you can see, in what may be my most frequently printed chart to dispel the idea that the dollar is dying, the DXY remains firmly in its range for the past year and is now heading toward the upper band. If you look at the calculated mean/variance of the DXY, you can see the trend line (the black line in the center) is completely flat, i.e. the dollar is trending neither higher nor lower over the past year.

Source: tradingeconomics.com

Looking at specific currencies, AUD (-1.0%) and NZD (-1.45%) are the worst performers in the G10, although NOK (-0.9%) and SEK (-0.9%) are giving them a run. Kind of surprising for NOK given oil is much higher this morning. in the EMG bloc, ZAR (-1.0%), CLP (-1.0%), MXN (-0.8%), and KRW (-0.5%) are the laggards in their respective regions with ZAR suffering from the commodity movements, as is CLP with copper sharply lower this morning. MXN seems to be reacting to the news that the US has been stepping up its aggressive tactics against the drug cartels there and concerns about how that will end up.

Finally, on to commodities where oil (+3.0%) has responded exactly how you would expect to the Trump comment about his cares about Hormuz. Meanwhile, the metals are back in full negative correlation mode with oil as all of them are sharply lower this morning (Au -2.0%, Ag -5.9%, Cu -4.3%, Pt -4.0%). The one thing you have to admit about the commodities markets these days is that they are living up to their reputation of extreme volatility.

On the data front, this morning brings Empire State Manufacturing (exp 7.5), IP (0.3%) and Capacity Utilization (75.8%), none of which typically have a big impact and given the oil/Hormuz fears extant this morning, will almost certainly be completely ignored. There are no Fed speakers today but I do want to mention one from yesterday, Governor Michael Barr, who directly contradicted everything Chairman Warsh has been saying about the size of the Fed’s balance sheet, explaining that if they move away from their current ‘ample reserves’ model, it could have very negative impacts on the functioning of money markets.

There is an irony here as prior to the ‘ample reserves’ framework, there was a very active Fed funds trading market on an interbank basis and banks were able to borrow from each other whatever they needed for liquidity purposes. The Fed has usurped that role ever since the GFC and are now clearly concerned (afraid?) about going back. The thing is, it seems to me that there continues to be a tremendous amount of liquidity around and it would be quite feasible to create an intraday loan market to help alleviate those concerns. In fact, cash rich corporates (Berkshire Hathaway anyone?) could be part of the market as it would be entirely interbank and those corporates would know the counterparties quite well. Suffice it to say that Mr Warsh will have quite a time getting his way at this stage.

And that’s what we have going into the weekend. Gloom and doom about the near future, or profit taking, I’m not sure which. As I have said all along, play it close to the vest, in think.

Good luck and good weekend

Adf