While narrative writers obsessed

For some this was a Warshach test

The doves and the hawks

Each messaged their flocks

That Warsh, to their views, acquiesced

Meanwhile, in Iran bombs are falling

And President Trump is name calling

However, despite

The restarting fight

Risk assets keep on, higher, crawling

So, the FOMC Minutes were released, and they were hawkish dovish irrelevant. The best expression of this came from Bloomberg’s Joe Weisenthal when he posted this on X,

Two simultaneous takes on the release that he received. And I confess, I read those Minutes and didn’t learn anything at all. It seems that the decision to leave rates on hold was unanimous although several committee members would have voted for a hike as well.

What does this say about the state of things? I am very hopeful that we are on our way to a Fed that is less intrusive in market activities, both by reducing its balance sheet size, something that Chairman Warsh has expressly indicated as a goal, and by hearing less from committee members. As @inflation_guy, Mike Ashton explains here, if forward guidance is dead, then why do we need to hear from any FOMC members about anything? All those speeches were simply each member’s way to get their opinion out there and try to influence markets. As I have frequently written, we would be much better off if the Fed were opaquer in their decision making as it would reduce risk and leverage and that would enhance financial market stability. For everyone who wants Warsh to be Volcker redux, remember, back then, there were probably fewer than 10 people on Wall Street, let alone anywhere else, who could name a single member of the FOMC other than Mr Volcker himself. That is an aspirational goal!

How did the market respond to the Minutes? They basically ignored them. Equity markets, which had opened much lower, were already in the process of reclaiming those losses when the Minutes were released and edged higher from there, with no meaningful change in trajectory as you can see in the below chart of the S&P 500.

Source: tradingeconomics.com

How about bonds? Well, here is the 10-year chart and you tell me if the Minutes had an impact.

Source: tradingeconomics.com

I guess the real question is will the rest of the world’s central banks follow Mr Warsh’s lead and seek to end forward guidance and simply go about their job of managing inflation? One can always hope.

Which takes us to the other story of note, the apparent end of the ceasefire in Iran and the question of what is now happening in the Strait of Hormuz. First, let’s be clear, nobody really knows as the fog of war remains thick. Obviously, yesterday saw a sharp rise in the price of oil as concerns over future transits of the Strait rose dramatically. However, as of this morning, while WTI (+0.6%) has edged slightly higher from yesterday’s closing levels, as you can see from the chart below, it seems to have found a new short-term home here around $74/bbl.

Source: tradingeconomics.com

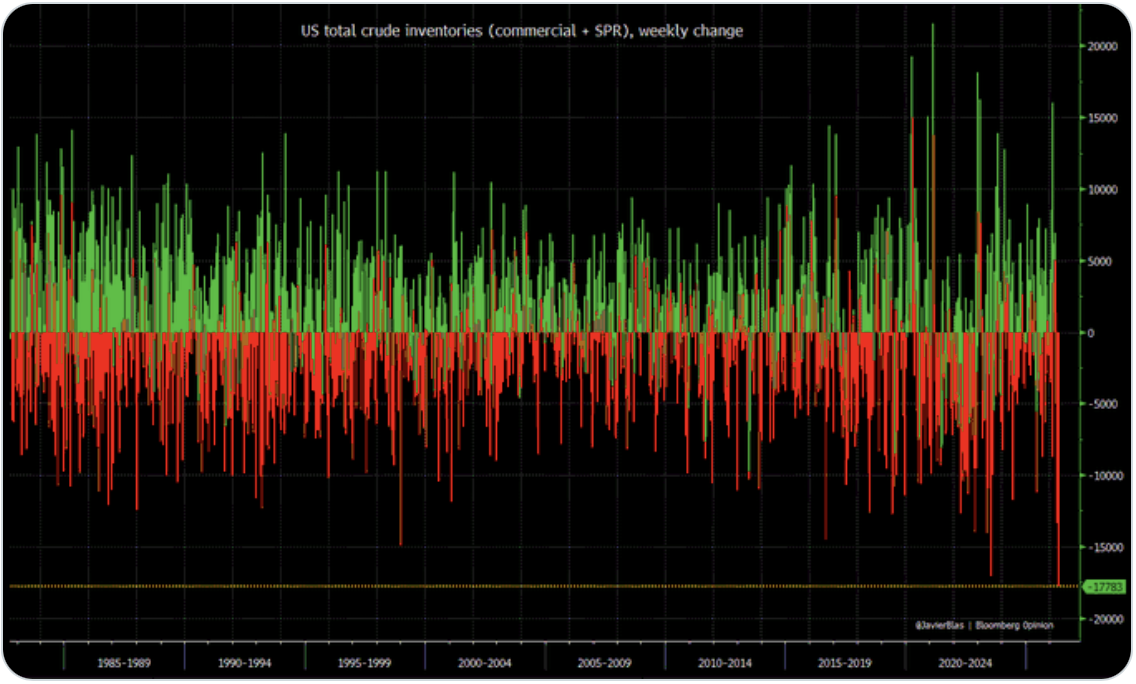

Scrolling through X this morning, the $200/bbl analysts were back at it, explaining that this time, with all those inventories having already been used up, we are going to see much higher prices. But weirdly, yesterday’s EIA data showed an inventory build of 3 million barrels. I keep seeing charts of the US SPR and how it is at its lowest level since 1982 implying that we are on the cusp of running out like this one from Bob Elliott. Now, Bob Elliott is a really smart guy, but I feel like the piece of the puzzle that is missing in these analyses is that right now, the US is producing just under 14 million bpd of oil, plus another ~7.5 million bpd of natural gas liquids and 110 billion cubic feet/day of dry natural gas. In fact, we are a massive exporter of oil and products, so perhaps a better question is, why do we need an SPR anymore? After all, it was created when we were at the mercy of the Middle East and producing just 8.6 million bpd. That is no longer the case.

My take is the world can run perfectly well on $75/bbl oil and there is plenty of supply at that level. In addition, we have seen numerous announcements of how Gulf oil producers are building new methods of transport away from the Strait, and over time, that will no longer be a choke point with any meaning. War is exciting to market participants for about two weeks, at which point they get bored and move on to the next big thing. After all, the Ukraine war has been ongoing for 4 years and it doesn’t get a mention in market commentary. Next week we start to see earnings releases for Q2 and that will be much more interesting for equity, and likely all other, markets.

In the meantime, let’s see what happened overnight. Based on the mix of information, we cannot be surprised that there were mixed outcomes in equity markets around the world. Yesterday’s US split (DJIA -1.1%, NASDAQ +0.2%) was followed by gains in Tokyo (+1.4%), China (+2.5%), Korea (+0.6%) and India (+0.3%) while HK (-0.7%), Taiwan (-0.8%) and the Philippines (-0.8%) all slid a bit. There was no rhyme or reason here. The only data of note overnight was Chinese inflation data where CPI fell to +1.0%, while PPI rose to +4.1%. It strikes me that Chinese companies will continue to see pressure on their margins.

In Europe, things are also mixed with Spain (+0.8%), Italy (+0.7%) and France (+0.3%) all higher while the UK (-0.6%) is slipping and Germany is little changed. As to US futures, they are leaning higher at this hour (7:50).

Bond markets seem to have stopped selling off as yields this morning are little changed (Treasury +1bp, Bunds +1bp, Gilts -3bps, OATs -3bps). JGBs were unchanged overnight. The 10-year auction yesterday went pretty well with a bid-to-cover ratio of 2.59, although with yields at 4.58%, it is not that surprising there was real demand. I will say this, bonds, too, are a market with some smart folks with diametrically opposed views of the future outcome. Both 3% and 6% are seen as the next major destination depending on the analyst.

Interestingly, metals markets are showing some life this morning with gold (+0.8%), silver (+1.4%) and copper (+2.2%) all bouncing off recent lows. This is a bit out of character compared to recent price action relative to oil, but maybe we are putting in some bottoms here.

Finally, the dollar is, net, little changed this morning. In the G10, NZD (+0.65%) is the big mover, which continues on the back of their rate hike from yesterday. But otherwise, +/-0.1% is the norm here. In the EMG bloc, KRW (-0.5%) is giving back some of its recent gains but continues to hover near multi-decade lows. The recent gains have been on the back of a record current account surplus, but it remains an interesting conundrum that despite the massive gains in the Korean stock market, the currency has not attracted more buying interest. Otherwise, modest EMG gains on the order of +0.1% are today’s story.

On the data front, we see Initial (218K) and Continuing (1820K) Claims as well as Existing Home Sales (4.20M) today. In addition, there are two Fed speakers as I imagine getting them to shut up will take some time. However, I wonder, will they really add to the discussion?

Oil continues to be the driving force in markets, but right now, my sense is eyes are turning to upcoming earnings releases. Of course, we also get CPI next week, which will be a critical number for markets, at least for now.

Good luck

Adf